Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

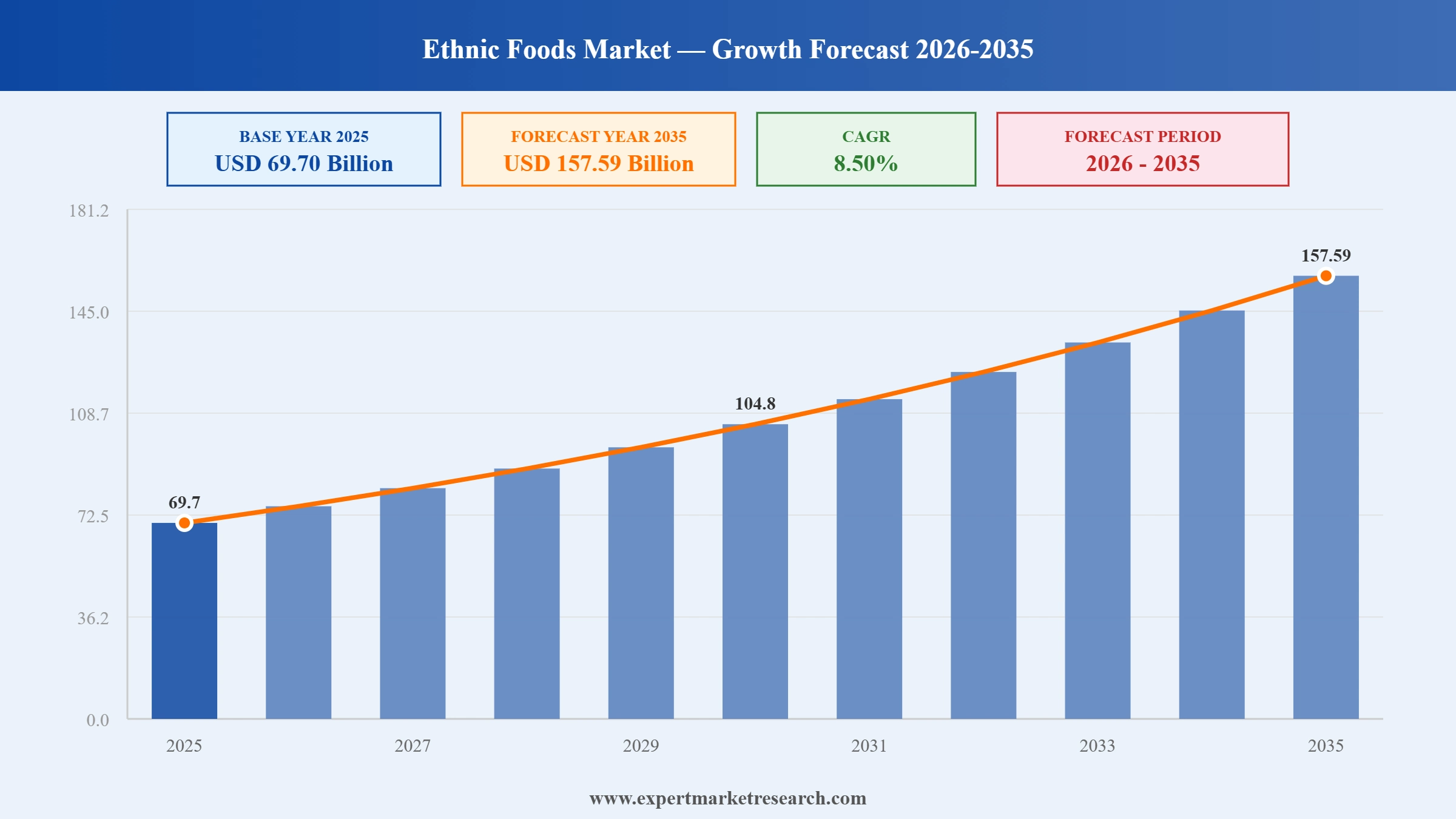

The global ethnic foods market was valued at USD 69.70 Billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 8.50% during the forecast period of 2026 to 2035, reaching USD 157.59 Billion by 2035, according to Expert Market Research. The ethnic foods market encompasses commercially produced and distributed food products, ingredients, condiments, sauces, ready-to-eat meals, and packaged goods that are associated with the culinary traditions of specific national, cultural, or regional cuisines spanning Asian (Chinese, Japanese, Indian, Thai, Vietnamese, Korean, Southeast Asian), Latin American, Mexican, Middle Eastern, Mediterranean, African, and European ethnic cuisine categories.

The market's robust 8.50% CAGR reflects the accelerating mainstreaming of global culinary diversity across consumer food cultures worldwide. Globalisation and intensifying cross-cultural exchange have systematically expanded consumer culinary horizons, creating sustained demand for authentic ethnic flavours, ingredients, and meal formats in retail grocery channels, foodservice establishments, and increasingly through direct-to-consumer e-commerce platforms. The rapid growth of diaspora and immigrant population communities across North America, Western Europe, and Australia has simultaneously created a large, authenticity-demanding consumer base and a cultural transfer mechanism through which ethnic cuisines achieve mainstream adoption among broader consumer populations.

The ethnic foods market operates across two primary consumption channels: retail (supermarket ethnic food aisles, specialty ethnic grocery stores, warehouse clubs, and online retail platforms) and foodservice (standalone ethnic restaurants, fast-casual ethnic dining formats, food truck operations, ghost kitchens, and food delivery platform services). Both channels are expanding, with the foodservice channel historically representing the point of initial consumer exposure to new ethnic cuisines and the retail channel enabling ongoing at-home consumption of ethnic food products following restaurant-driven trial and adoption.

Recent Developments (Jan 2026 - June 2026)

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global ethnic foods market's impressive 8.50% CAGR over the 2026 to 2035 forecast period is supported by a powerful combination of demographic, cultural, and commercial demand drivers. Globalisation and westernisation are the broadest structural forces expanding ethnic food demand. The progressive globalisation of trade, travel, media, and cultural exchange has systematically eroded the cultural boundaries that once restricted certain cuisines to specific ethnic communities, creating a genuinely borderless global food culture in which mainstream consumers across North America, Western Europe, and increasingly Asia Pacific actively seek out and regularly consume food products from cuisines historically outside their cultural experience. Social media platforms particularly Instagram, TikTok, and YouTube have dramatically accelerated this process by enabling global viral dissemination of food content, creating demand for authentic ethnic ingredients and meal formats among consumer cohorts who have experienced a cuisine virtually before ever tasting it physically.

Demographic shifts driven by international migration are creating structural demand foundations that support sustained long-term ethnic food market growth. The United States' Hispanic population now exceeding 63 million people represents the world's largest single ethnic food consumer community outside of Latin America, creating a massive and continuously expanding domestic market for authentic Mexican, Central American, and Caribbean food products that mainstream food companies are increasingly prioritising. Similarly, the South Asian diaspora communities in the United Kingdom, Canada, and the UAE generate persistent demand for authentic Indian, Pakistani, Bangladeshi, and Sri Lankan food products that has expanded into broader mainstream consumer adoption of South Asian flavours including curry, turmeric, chutney, and basmati rice as pantry staples. Asian diaspora communities in North America and Western Europe are similarly expanding the authentic Asian food consumer base while simultaneously serving as cultural arbiters who validate ethnic cuisine adoption by mainstream consumers.

The foodservice industry has been a critical amplification mechanism for ethnic food market growth, converting consumer curiosity into regular purchasing behaviour through restaurant dining experiences that create familiarity and confidence with ethnic cuisine formats. The explosion of standalone ethnic restaurants, fast-casual ethnic dining formats including Chipotle's popularisation of Mexican fast-casual and the rapid growth of Korean, Vietnamese, Indian, and Middle Eastern fast-casual concepts and the proliferation of ethnic cuisine food trucks and delivery-only dark kitchen operations have collectively driven a step-change in mainstream consumer exposure to and comfort with ethnic food flavours and formats. Food delivery platforms including DoorDash, Uber Eats, and Deliveroo have materially amplified ethnic restaurant reach by connecting consumers with ethnic dining options regardless of geographic proximity, effectively democratising access to ethnic cuisines and converting occasional restaurant trial into regular at-home consumption of retail ethnic food products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asian cuisine collectively represents the largest and fastest-growing sub-segment within the global ethnic foods market, driven by the extraordinary breadth of the Asian culinary tradition, the growing global recognition of Asian cuisines' health and nutritional credentials, and the viral cultural influence of Korean pop culture (K-pop, K-drama) in driving global consumer interest in Korean food and beverages. Chinese, Japanese, Thai, Vietnamese, Korean, and Indian cuisines each have distinct and large global consumer followings, with the collective Asian cuisine segment accounting for approximately 42% of total ethnic food market revenues in 2025. Soy sauce, fish sauce, miso, coconut milk, curry pastes, kimchi, and instant noodle products have achieved true mainstream pantry staple status across North American and European grocery markets, driving sustained volume growth for Asian condiment and ingredient manufacturers including Kikkoman, Lee Kum Kee, Ajinomoto, and S&B Foods.

A significant and growing share of ethnic food market growth is being driven by the intersection of authentic ethnic cuisine with contemporary health and wellness consumer priorities. Mediterranean, Japanese, Indian, and Middle Eastern cuisines are actively marketed and purchased on the basis of their health attributes the Mediterranean diet's documented cardiovascular benefits, the Japanese diet's association with longevity, Ayurvedic Indian ingredients' wellness positioning, and Middle Eastern cuisine's naturally plant-forward protein sources (hummus, falafel, tahini, labneh) all align strongly with mainstream consumer health priorities. Brands including Cedar's, Sabra, and Boar's Head have successfully mainstreamed Middle Eastern food staples through health-positioned marketing in North American supermarkets. The clean label trend consumer preference for short, recognisable ingredient lists is particularly well-suited to traditional ethnic food formulations that rely on natural spices, herbs, and fermented ingredients without the artificial additives common in conventional processed food categories.

The ready-to-eat (RTE) and easy-to-prepare ethnic food format has been the fastest-growing product sub-category within the ethnic foods market, driven by the busy lifestyle demands of dual-income urban households who want to consume authentic ethnic flavours without the time investment of traditional from-scratch ethnic cooking. Microwaveable Indian curry pouches (Tasty Bite, Patak's ready meals), Korean bibimbap bowls, Vietnamese pho soup kits, Japanese ramen starter packs, and Mexican street taco kits have achieved strong mainstream retail penetration across North American and European supermarkets. The COVID-19 pandemic's at-home cooking elevation effect materially accelerated RTE ethnic food adoption, as consumers sought to replicate restaurant ethnic dining experiences at home during restaurant closure periods. The habit formation that occurred during this period has proved structurally durable, with RTE ethnic food consumption maintaining elevated levels relative to pre-pandemic baselines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The foodservice channel has been the primary vehicle through which new ethnic cuisines achieve mainstream consumer adoption across North American and European markets. The rapid proliferation of Korean barbecue restaurants, Vietnamese pho houses, Indian street food concepts, Peruvian ceviche bars, and Middle Eastern shawarma fast-casual formats in major urban markets has exposed mainstream consumer audiences to ethnic cuisines they subsequently seek in retail channels. Food delivery platform expansion through DoorDash, Uber Eats, Deliveroo, Swiggy, and Zomato has dramatically extended the geographic reach of ethnic restaurant cuisine, enabling consumers in suburban and secondary markets to access ethnic food experiences they previously could only obtain in multicultural urban centres. Ghost kitchens and virtual restaurant brands operating exclusively through delivery channels are enabling ethnic food entrepreneurs to launch commercial-scale ethnic cuisine operations without the capital investment of a full-service restaurant, accelerating the pace at which new ethnic cuisine formats achieve consumer trial.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The ethnic foods market faces several meaningful operational and commercial challenges that constrain profitability and limit growth velocity in specific market contexts. Supply chain complexity is the most persistent operational challenge: sourcing authentic ethnic ingredients particularly specialist spices, condiments, fermented products, and fresh produce varieties often requires working with fragmented supply networks of small-scale producers and specialist importers across multiple countries, creating significant logistics complexity, quality consistency challenges, and food safety compliance burdens that increase costs and management overhead relative to conventional food product supply chains. Maintaining authentic quality standards while achieving the price-competitiveness necessary to secure mainstream retail distribution is a constant tension that ethnic food manufacturers must navigate carefully: over-reformulating for mainstream taste preferences and cost reduction risks alienating the authenticity-demanding diaspora consumer base, while maintaining authentic formulations risks pricing out cost-sensitive mainstream consumers. Regulatory complexity particularly the USDA, EU, and UK Food Standards Agency requirements for novel ingredient approvals, allergen labelling, and biocide certifications for certain traditional fermented or preserved ethnic food ingredients adds compliance costs and delays that disproportionately burden smaller ethnic food businesses lacking dedicated regulatory affairs capabilities.

Several structural dynamics restrain the pace of ethnic foods market expansion beyond the operational challenges individual companies face. Consumer unfamiliarity remains a significant restraint for less-established ethnic cuisine categories cuisines including West African, East African, Central Asian, and certain Southeast Asian traditions lack the mainstream consumer exposure and culinary literacy that allows Asian, Mexican, and Mediterranean cuisines to achieve broad retail penetration. Without the restaurant dining trial mechanism that enables new cuisine adoption, these culinary traditions struggle to achieve sufficient mainstream consumer confidence to drive retail volume at commercially viable scale. Private label competition from mainstream grocery retailers who develop own-brand ethnic food ranges at price points below branded ethnic food products represents a structural commercial restraint on branded ethnic food manufacturers' revenue and margin prospects, particularly in European grocery markets where retailer own-brand penetration in food categories is highest. Distribution gaps in secondary and tertiary cities and suburban markets where specialty ethnic grocery infrastructure is limited continue to restrict the addressable retail market for authentic ethnic food products to large urban multicultural centres where specialist channels are concentrated.

The global ethnic foods market presents exceptional commercial opportunities that position the sector for sustained high-growth through 2035 and beyond. The mainstreaming of previously niche ethnic cuisine categories exemplified by hummus' transformation from a specialty Middle Eastern ingredient to a USD 1 billion-plus annual retail category in North America, or Sriracha hot sauce's ubiquitous presence across restaurant and retail channels globally illustrates the transformative commercial upside available when ethnic food products successfully cross cultural adoption thresholds. The e-commerce channel is creating structurally new distribution opportunities for authentic ethnic food brands that previously lacked the retail channel access to achieve commercial viability at scale: Amazon, Thrive Market, and specialist ethnic food e-tailers provide national or global distribution reach for authentic ethnic brands without the slotting fee and promotional investment burden of traditional grocery channel entry, enabling a new generation of authentic ethnic food startups including Omsom (Asian cooking sauces), Yai's Thai, and Fly By Jing (Sichuan condiments) to build substantial consumer followings and achieve commercial success. The health positioning opportunity within ethnic foods is particularly compelling: as mainstream consumers increasingly seek food products that offer functional health benefits alongside culinary enjoyment, the documented wellness attributes of Mediterranean, Japanese, Indian, and Middle Eastern dietary patterns provide a powerful marketing platform for authentic ethnic food brands seeking to command premium pricing and capture health-motivated consumer segments. Expert Market Research's full report provides investment-grade opportunity sizing and market entry strategy frameworks across all ethnic cuisine segments, distribution channels, and geographic markets.

Expert Market Research's Ethnic Foods Market report provides comprehensive segmentation analysis across cuisine type, food type, and distribution channel dimensions, with market size, share, and CAGR data for each segment over the full 2026 to 2035 forecast period.

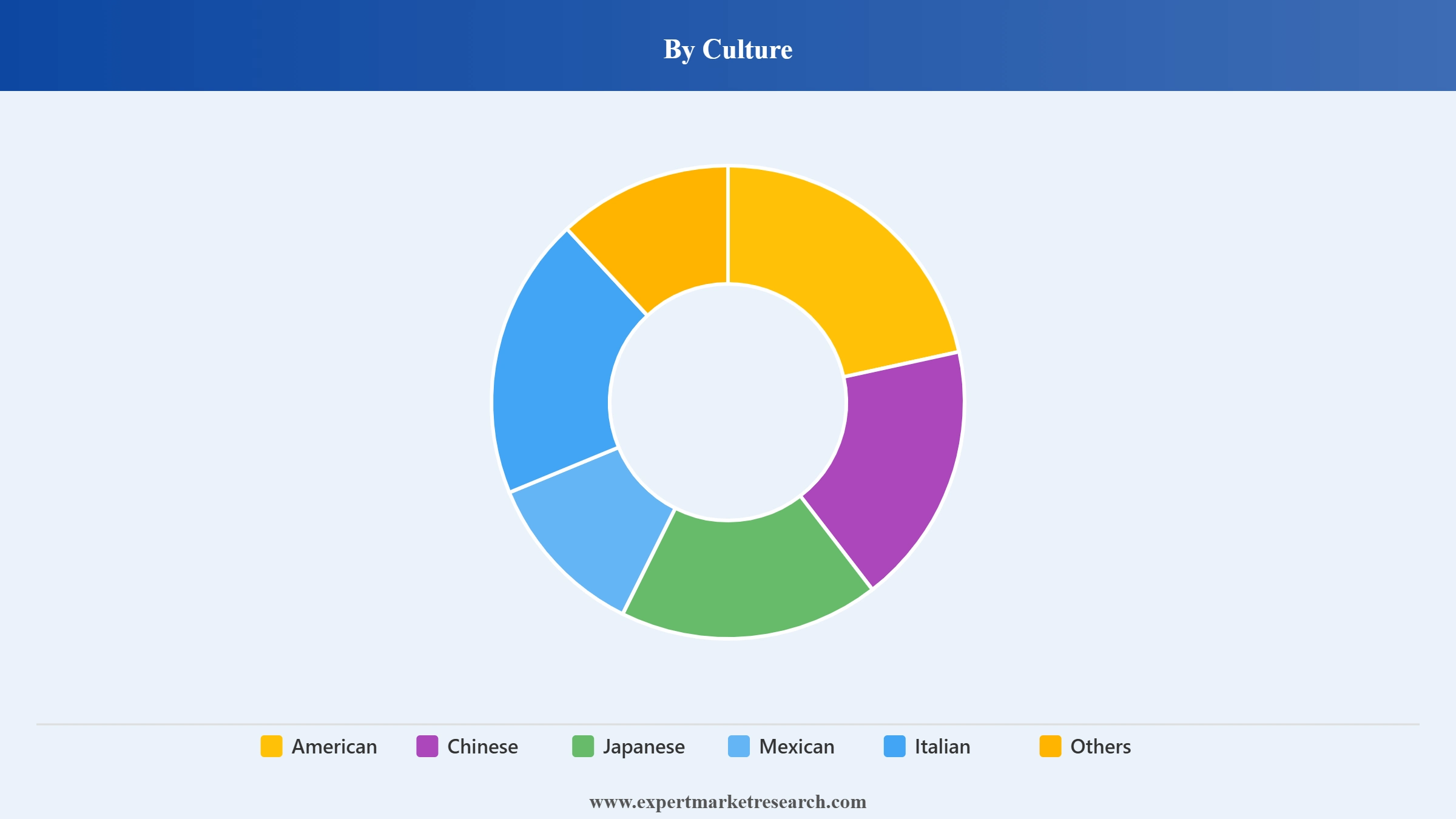

Market Breakup by Culture

American ethnic cuisine encompassing Tex-Mex, Cajun, Southern BBQ, and New England seafood traditions is gaining commercial traction as a globally exported food experience. American-style condiments and BBQ sauces command growing international retail and foodservice presence.

Chinese cuisine is the most broadly distributed ethnic food category globally, with soy sauce, oyster sauce, hoisin, tofu, and frozen dim sum achieving mainstream supermarket presence across North America and Europe. Lee Kum Kee, Pearl River Bridge, and Kikkoman's Chinese sauce lines lead this segment.

Japanese ethnic food including miso, teriyaki sauce, instant ramen, matcha, and frozen gyoza has achieved near-universal mainstream supermarket presence in North American and Western European markets. Ajinomoto, Kikkoman, and S&B Foods are the dominant commercial players.

Mexican cuisine is the largest ethnic food segment in North America, with salsas, tortillas, taco seasoning, and enchilada sauces achieving true pantry staple status across US grocery retail. Goya Foods leads the authentic Hispanic segment while General Mills' Old El Paso dominates the mainstream Mexican food aisle.

Italian cuisine holds the most established position of any European ethnic food sub-category, with pasta, tomato sauces, olive oil, and pesto commanding consistent high-volume sales in mainstream supermarkets globally. Barilla, Bertolli, and De Cecco are among the internationally dominant brands.

This segment covers Korean, Indian, Thai, Vietnamese, Middle Eastern, Mediterranean, and African cuisines collectively the fastest-growing cluster within the ethnic foods market. Korean cuisine leads growth, propelled by K-pop and K-drama cultural influence driving global demand for kimchi, gochujang, and Korean BBQ marinades.

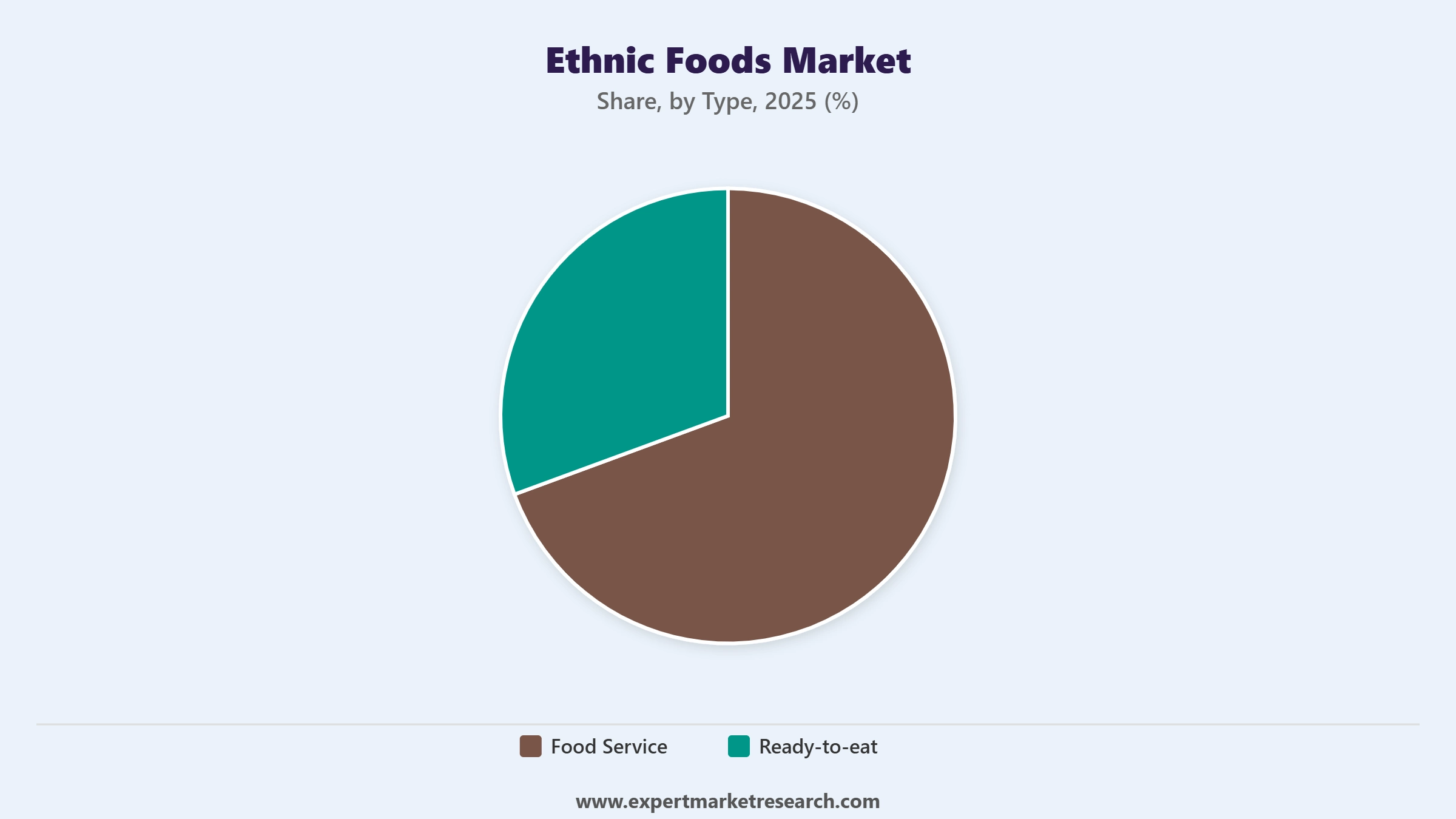

Market Breakup by Type

Food service covers ethnic food products supplied to restaurants, fast-casual chains, ghost kitchens, and delivery-only operations. The expansion of Korean BBQ chains, Vietnamese pho concepts, and Middle Eastern fast-casual formats, alongside platforms including DoorDash, Uber Eats, and Deliveroo, has structurally expanded this segment across all major markets.

Ready-to-eat is the fastest-growing type within the ethnic foods market, driven by urban consumers seeking authentic ethnic flavours without the time investment of traditional cooking. Microwaveable Indian curry pouches, Korean bibimbap bowls, Japanese frozen ramen, and Mexican taco kits are achieving strong mainstream retail penetration across North American and European supermarkets.

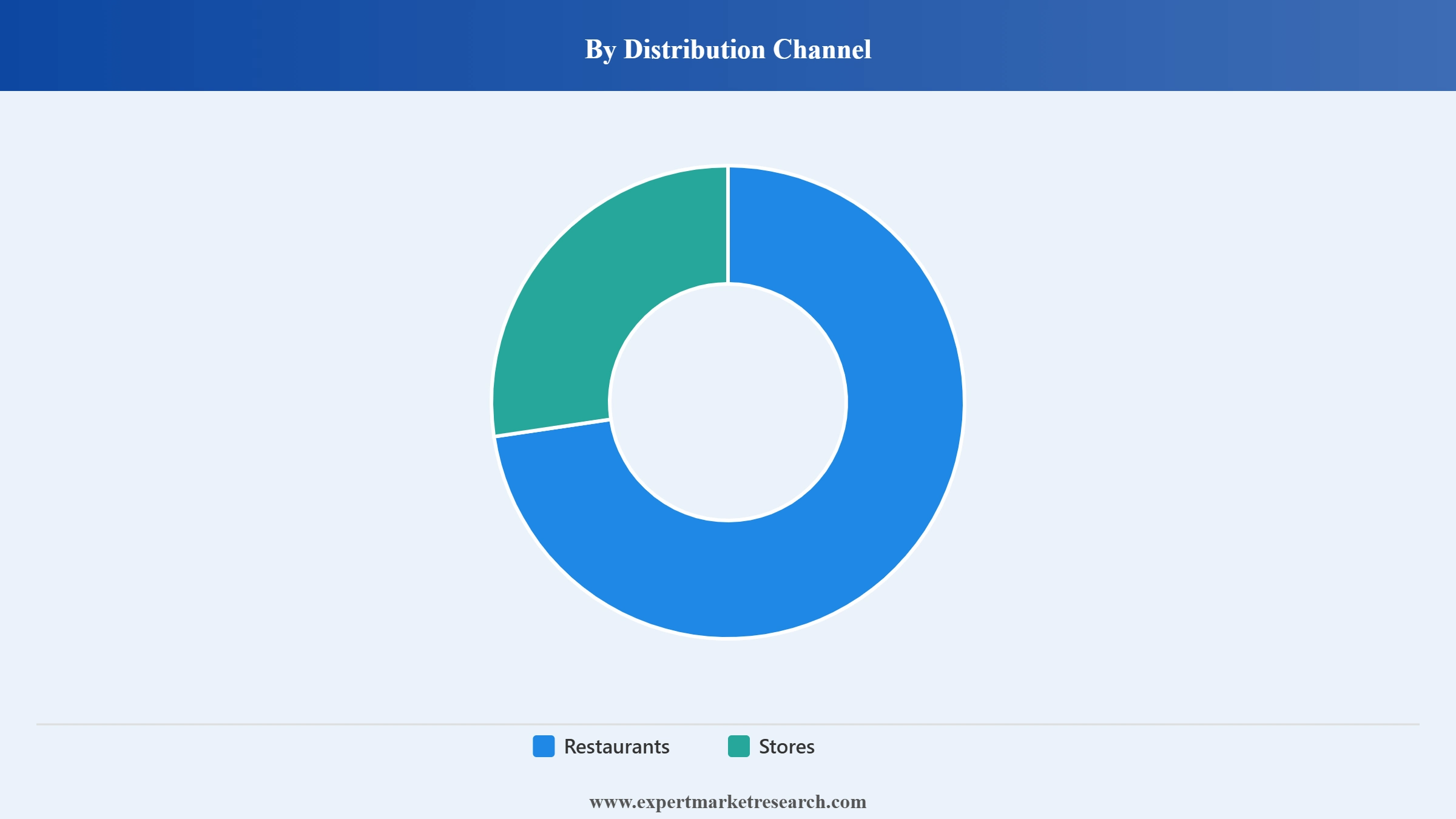

Market Breakup by Distribution Channel

Restaurants including standalone ethnic dining, fast-casual formats, food trucks, and ghost kitchens are the primary channel through which consumers first discover ethnic cuisines before seeking retail products for at-home use.

Serves impulse and on-the-go ethnic food occasions particularly instant noodles, ethnic-flavoured snacks, and grab-and-go prepared ethnic meal formats targeting urban convenience-seeking consumers.

The fastest-growing distribution channel, enabling authentic niche brands including Omsom, Fly By Jing, and Foo Foods to build national consumer bases without traditional retail slotting fees. Amazon, specialist ethnic e-tailers, and DTC brand websites lead this channel.

Includes specialty ethnic grocery chains (H Mart, Patel Brothers, 99 Ranch Market), warehouse clubs (Costco, Sam's Club), and health food stores providing authentic product depth that mainstream supermarkets cannot match.

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the world's largest ethnic foods market by revenue, accounting for approximately 38% of global ethnic food revenues in 2025, with the United States as the dominant national market. The extraordinary size of the US ethnic food market reflects the diversity of the country's multicultural consumer population the US Hispanic population of 63+ million, the Asian-American population of 22+ million, and the rapidly growing South Asian-American, Middle Eastern-American, and African-American communities collectively constitute an enormous authenticity-demanding ethnic food consumer base. Mexican and Latin American cuisine dominates US ethnic food retail by revenue through Goya Foods, Old El Paso, and category-defining salsa, tortilla, and hot sauce brands. Asian cuisine holds the second-largest revenue share and is growing fastest, driven by the expanding mainstream adoption of Korean, Vietnamese, Thai, and Japanese flavour profiles. Canada's ethnic food market mirrors the US in its cuisine preference profile while growing at a slightly faster pace driven by proportionally higher immigration rates.

Europe is the world's second-largest ethnic foods market by revenue, accounting for approximately 28% of global revenues in 2025, and is characterised by significant variation in ethnic cuisine preference profiles across national markets reflecting differences in colonial history, immigration patterns, and geographic proximity to ethnic cuisine origin countries. The United Kingdom is Europe's largest ethnic food market, with South Asian (Indian, Pakistani, Bangladeshi) cuisine representing the dominant ethnic food category driven by a South Asian diaspora community of over 4 million people and the broader UK population's deep affinity for curry-house cuisine that has become a defining element of British culinary culture. Germany is Europe's second-largest ethnic food market, with Turkish cuisine products doner kebab preparations, Turkish bread, ayran alongside strong Southeast Asian and South Asian segments reflecting Germany's large Turkish-origin population. France, the Netherlands, and Belgium each have distinct ethnic cuisine profiles reflecting their specific immigration histories and geographic positions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific represents approximately 22% of global ethnic food revenues a significant market in absolute terms, but one that differs structurally from Western markets in that ethnic food consumption predominantly involves intra-regional Asian cuisine adoption (Japanese consumers eating Korean food, Thai consumers eating Japanese-influenced dishes) rather than the cross-cultural Western adoption pattern that characterises North American and European ethnic food markets. Australia and New Zealand within the Asia Pacific grouping share more closely the North American and European pattern of multi-cuisine ethnic food adoption across a multicultural migrant population, with Asian cuisine particularly Chinese, Vietnamese, Indian, and Japanese representing the dominant ethnic food category in Australian supermarkets. Japan's domestic market includes a significant ethnic food sector through yakitori-influenced Korean BBQ adoption and the mainstreaming of Chinese, Italian, and Indian-inspired product categories.

The Middle East and Africa region accounts for approximately 7% of global ethnic food revenues, with the Gulf Cooperation Council states UAE, Saudi Arabia, Qatar, and Kuwait representing the most commercially developed sub-regional ethnic food markets driven by their large South Asian and Southeast Asian expatriate populations that demand authentic Indian, Pakistani, Filipino, and Indonesian food products. The UAE's Dubai market in particular functions as a global ethnic food hub, with retail distribution of authentic ethnic food products from over 50 national cuisine traditions serving a residential population where non-UAE nationals account for approximately 89% of the total population. Sub-Saharan Africa's ethnic food market is primarily driven by intra-continental diaspora food trade and the growing availability of Asian and European ethnic food products in premium urban supermarkets serving affluent and expatriate consumer segments.

Latin America accounts for approximately 5% of global ethnic food revenues, with Brazil and Mexico representing the region's largest ethnic food consuming markets. The ethnic food market in Latin America is driven primarily by intra-regional cuisine cross-adoption Brazilian consumers consuming Peruvian ceviche, Chilean consumers adopting Japanese-Peruvian Nikkei cuisine, Argentine consumers engaging with Italian and Spanish ethnic food traditions alongside growing consumption of Asian (particularly Chinese, Japanese, and Korean) ethnic food products driven by significant Asian diaspora communities in Brazil, Peru, and other Latin American countries. The export dimension of Latin American ethnic food is also commercially significant: Mexican, Brazilian, and Peruvian culinary traditions are among the most globally influential cuisines, driving significant export revenues for authentic Latin American food ingredient and packaged product brands serving diaspora and mainstream consumers in North America, Europe, and Asia.

Major ethic foods market players are engaging in mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds. Ethnic food companies are expanding their product lines to include a wide variety of authentic and culturally diverse options which includes ready-to-eat meals, spice blends, sauces, frozen products, and packaged meal kits, among others, which consist of traditional recipes from various regions. Furthermore, some companies are collaborating with local chefs and culinary experts to maintain authenticity.

Ajinomoto Co., Inc. is a prominent Japanese food and biotechnology company, with its headquarters in Tokyo, Japan. Founded in 1909, the company is well-known for its production of food seasonings, especially monosodium glutamate (MSG), which has contributed significantly to its global reputation.

McCormick & Company, Incorporated is a leading American multinational food corporation in the ethnic foods market, based in Hunt Valley, Maryland. Established in 1889, the company focuses on the manufacturing, marketing, and distribution of spices, seasoning blends, condiments, and flavoring products, catering to both retail and food service markets.

Associated British Foods PLC (ABF) is a British multinational company for food processing and retail, with its headquarters in London, UK. It was founded in 1935 and since then ABF has diversified its operations across various sectors, including sugar production, grocery items, agriculture, and food ingredients, among others.

General Mills Inc., established in 1866 and located in Mississippi is a leading player in the ethnic foods space. The company’s principal products include Old El Paso taco shell or Takis snacks. They entirely focus on new developments or introductions of new products with a particular emphasis on its market-to-global operations, specifically found in the developing countries.

The global ethnic foods market's competitive landscape encompasses a diverse ecosystem of multinational food corporations with significant ethnic food portfolio investments alongside a large and growing number of specialist ethnic food brands, regional manufacturers, and food startups. Goya Foods is the largest privately held Hispanic-owned food company in the United States, operating an extensive portfolio of Latino and Caribbean cuisine products across more than 2,500 SKUs spanning staple foods, condiments, beverages, and snacks distributed across 90+ countries. McCormick & Company has built a significant ethnic spice and seasoning portfolio through organic brand development and strategic acquisitions including the Cholula hot sauce brand (acquired 2020), Stubbs BBQ sauces, and Zatarain's Cajun and Creole products.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Startups are increasingly focusing on clean-label, non-GMO, organic, and sustainably sourced ingredients. Due to the rising demand from health-conscious consumers for ethnic cuisine, these companies are adapting traditional recipes to offer gluten-free, vegan, and low-sodium versions of classic dishes to enhance their appeal. Many businesses and startups in the ethnic foods market are also focusing on authenticity in their branding and storytelling. By showcasing the cultural heritage, history, and culinary traditions linked to their products, they appeal to consumers looking for more than just a meal.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The ethnic foods market is assessed to grow at a CAGR of 8.50% between 2026 and 2035.

The major drivers of the market include westernisation, increasing population and urbanisation, new and innovative cuisines, increasing disposable income, and changing food habits of customers.

The increasing global employment opportunities and rising immigration are the key industry trends propelling the market's growth.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Based on the culture, ethnic foods are classified into American, Chinese, Japanese, Mexican, and Italian, among others.

Food service and ready-to-eat are the types of ethnic foods in the market.

Restaurants and stores are the several distribution channels of the market. The stores are further segmented into hypermarkets/supermarkets, convenience stores, and online stores, among others.

The major players in the industry are Ajinomoto Co. Inc., McCormick & Company, Incorporated, Associated British Foods PLC, General Mills, Inc., and Paulig Group, among others.

In 2025, the market reached an approximate value of USD 69.70 Billion.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 157.59 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Culture |

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.