Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

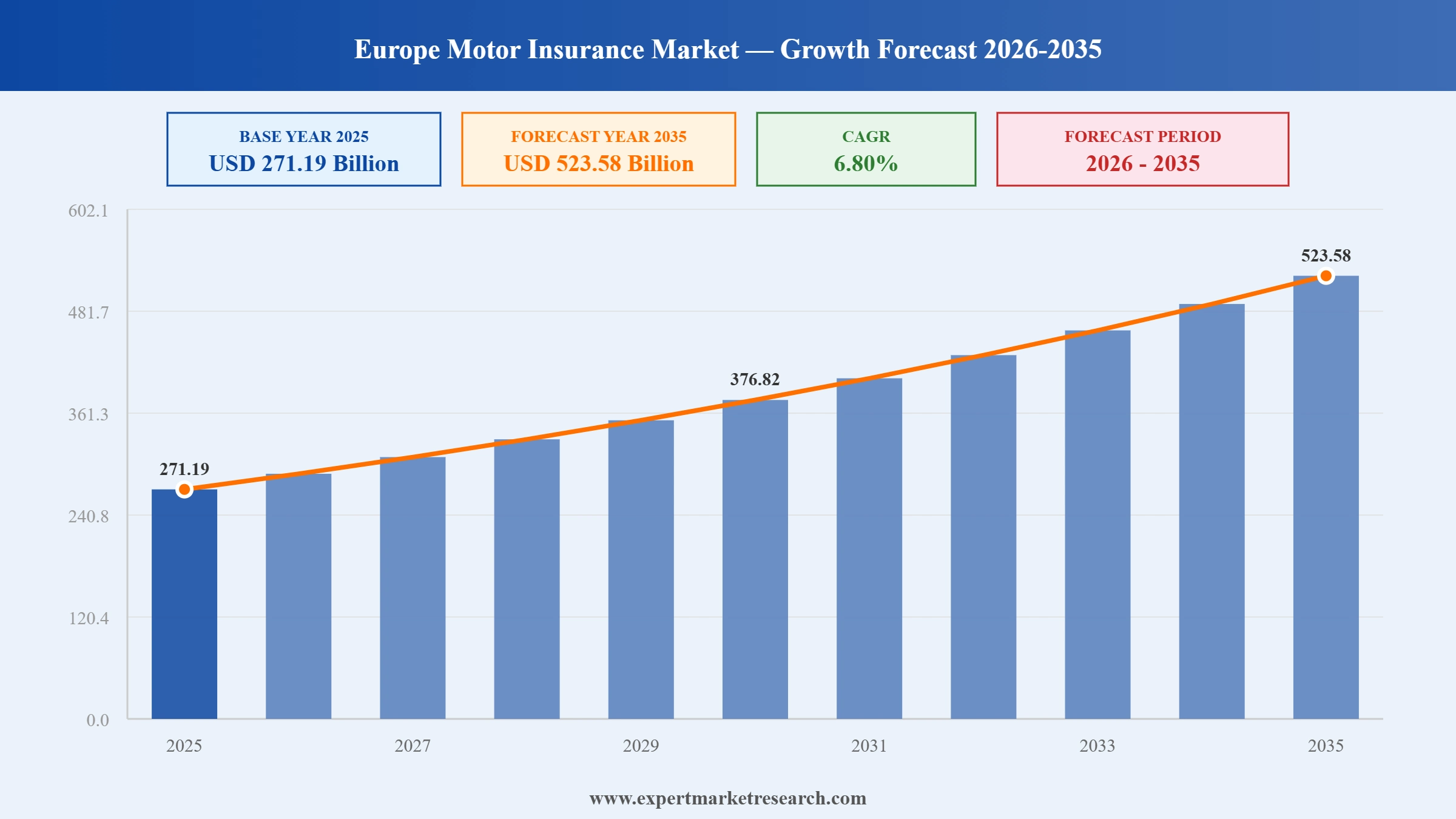

The Europe motor insurance market attained a value of USD 271.19 Billion in 2025 and is projected to expand at a CAGR of 6.80% through 2035. The market is further expected to achieve USD 523.58 Billion by 2035. Rising cross border vehicle usage and gig economy fleets are increasing demand for flexible pan European motor insurance products that support rapid policy activation real time risk scoring at scale.

Growth in the Europe motor insurance market is mainly due to the support of mandatory insurance enforcement and connected vehicle data access. Stricter roadside enforcement and the introduction of digital vehicle registries are leading to a decrease in uninsured driving in Eastern Europe. At the same time, OEM insurer data partnerships are on the rise, which means that insurers get direct access to diagnostic and mileage data from vehicles. This supports usage-based pricing and proactive maintenance alerts. Such factors improve underwriting accuracy while lowering fraud exposure, making motor insurance portfolios more predictable and attractive for long term capital deployment.

Product redesigns focused on telematics and dynamic pricing are also transforming the market. For instance, Allianz Partners and Lynk & Co are teaming up to offer a new mobility insurance product for monthly subscription members throughout Europe. According to the Europe motor insurance market analysis, new registrations of electric vehicles in the EU rose by 23.9% in the first quarter of 2025 compared to the same period last year, reaching 412,997 units. Insurers are using this information to lower their loss ratios and at the same time they provide flexible pricing, thereby changing the competition from static policies to behavior based underwriting models.

Regulatory pressure and data driven fraud prevention are also shaping insurer strategies. European insurers are investing in AI-based claims triage and image recognition to shorten settlement cycles and detect staged accidents. For example, the Estonian startup, DriveX is developing a technology that uses artificial intelligence to automate the verification of motor vehicles and can detect any damage. Companies like Generali are embedding analytics into fleet and SME motor insurance products, targeting lower combined ratios, opening up new Europe motor insurance market opportunities.

In 2020, motor insurance premiums represented 36% of the total property and casualty insurance market in Europe, amounting to €149 billion.

In 2023, the European Union reported a surplus of €90.6 billion in the trade of new automobiles.

The European Union solidified its position as the world's second-largest automobile producer, with a total output of 12.1 million units, marking an increase of over 11% in 2023.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Europe Motor Insurance Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 271.19 |

| Market Size 2035 | USD Billion | 523.58 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 6.80% |

| CAGR 2026-2035 - Market by Country | United Kingdom | 7.4% |

| CAGR 2026-2035 - Market by Country | Germany | 7.0% |

| CAGR 2026-2035 - Market by Type | Commercial Motor Insurance | 7.3% |

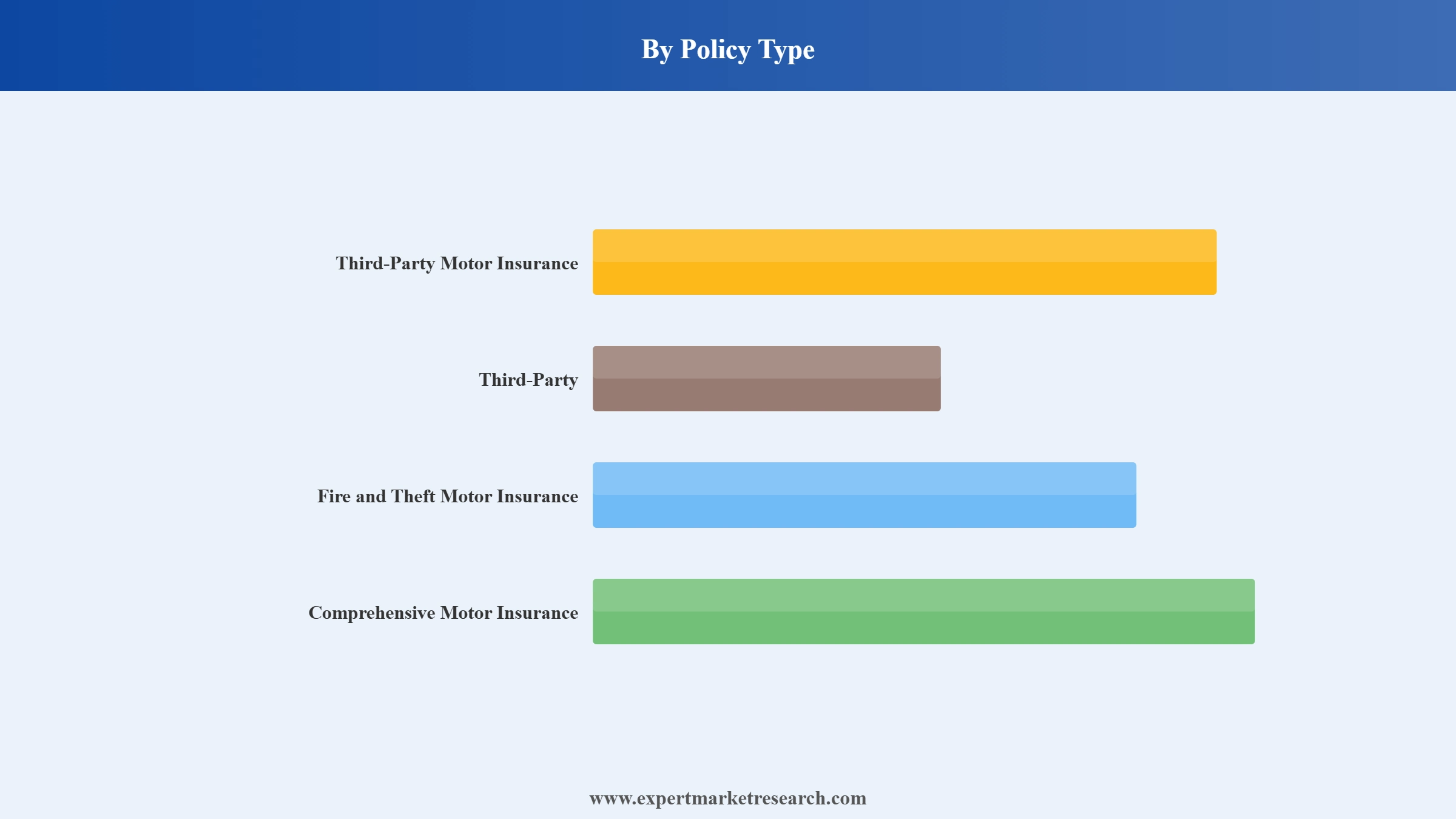

| CAGR 2026-2035 - Market by Policy Type | Comprehensive Motor Insurance | 7.7% |

| 2025 Market Share by Country | Italy | 11.8% |

Orange Poland revealed the launch of Insure with Orange, a new digital insurance comparison platform created in Poland with the help of the international insurtech company Bolttech. Therefore, telecom-led platforms are revolutionizing the distribution of motor insurance, pushing insurers to introduce their products in non-insurance-based ecosystems to reach digitally native customers at lower acquisition costs.

In the United Kingdom, Bentley Motors unveiled its first personalized insurance program specifically for Bentley owners. This Europe motor insurance market trend is a clear indication of the growing demand for OEM, backed, vehicle, specific coverage, giving insurers the chance to co-develop premium motor products with automakers and authorized repair networks.

Feather, a digital-first insurer targeting foreigners living in Europe, launched its auto insurance product for expats. Companies can use this trend of rising cross-border mobility to develop multilingual, portable motor policies tailored for mobile professionals and foreign residents, accelerating overall Europe motor insurance market opportunities.

Qover collaborated with BMW and MINI to come up with a complete car insurance solution that meets the Irish market requirements. Companies can use such insurance models to increase customer retention among car owners.

Telematics is one of the main factors that influence motor insurance pricing in Europe. Insurance companies are gradually inclining towards embedded vehicle data and smartphone-based scoring. Insurers such as Allianz, Generali, and AXA offer pay-how-you-drive and pay-as-you-drive products primarily for younger and urban consumers. This trend in the Europe motor insurance market matches the EU mobility data policies aimed at granting standardized access to the vehicle data. For example, in January 2026, with the help of Cambridge Mobile Telematics, DriveWell Fleet was launched. It is a telematics solution for the whole fleet that provides insurers with unified data from connected and unconnected commercial vehicles for the purposes of better risk pricing and safety outcomes.

The rapid increase in electric vehicles (EVs) is making insurance companies change their car insurance product offerings. EVs have an average repair cost that is 30-40% higher than conventional vehicles because of their batteries, sensors, and limited repair facilities. Firms like Zurich and AXA are offering EV, specific motor policies which cover battery degradation, charging equipment, and software updates. This trend in the Europe motor insurance market is in line with EU Fit for 55 targets that aim for quick EV uptake in the member states. Insurers can use this opportunity to offer customers packaged services that include warranty, roadside assistance, and access to authorized repair shops. For example, Tryg Norway offers a tailored EV insurance using AI-optimized package, since January 2022.

Claims automation is becoming a core competitive advantage in the market. Insurers are deploying AI for image-based damage assessment, instant payouts, and fraud detection. Companies like Generali and Aviva have integrated AI claims triage to reduce settlement times. This shift aligns with EU digitalization initiatives promoting AI adoption under regulated frameworks. Governments are tightening fraud monitoring, especially for staged accidents and exaggerated injury claims, reshaping the entire Europe motor insurance market dynamics. Faster claims handling improves customer satisfaction while lowering operational costs. Insurers investing in automation gain scalability without proportional staffing increases. For example, in November 2025, Allianz launched its first agentic AI solution to automate food spoilage claims and drastically cut processing times from days to hours.

EU regulations are accelerating cross-border motor insurance distribution. Large insurers are launching standardized digital platforms that serve multiple countries with localized compliance layers. Companies like Direct Line and Allianz Direct are expanding digital-only motor products across Western and Central Europe. This trend reduces customer acquisition costs and enables rapid scaling, creating new Europe motor insurance market opportunities. In October 2025, AXA Partners partnered with bolttech, a global insurtech, to launch embedded insurance and assistance solutions across the European Union, United Kingdom, and Switzerland.

The growth of shared mobility in the gig economy is reshaping motor insurance demand. Ride-hailing, delivery fleets, and car-sharing platforms require flexible, short-duration coverage. Insurers are developing fleet motor insurance with real-time activation and usage tracking. This aligns with government regulation of gig platforms across Europe, particularly in France and Germany. Insurers like AXA XL are focusing on SME and fleet solutions with integrated risk management, expanding the Europe motor insurance market scope. In January 2026, Greenval Insurance, owned by Arval, hit one million insured vehicles across Europe, boosting its fleet insurance leadership with data-driven solutions and broader coverage flexibility for businesses.

The EMR’s report titled “Europe Motor Insurance Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

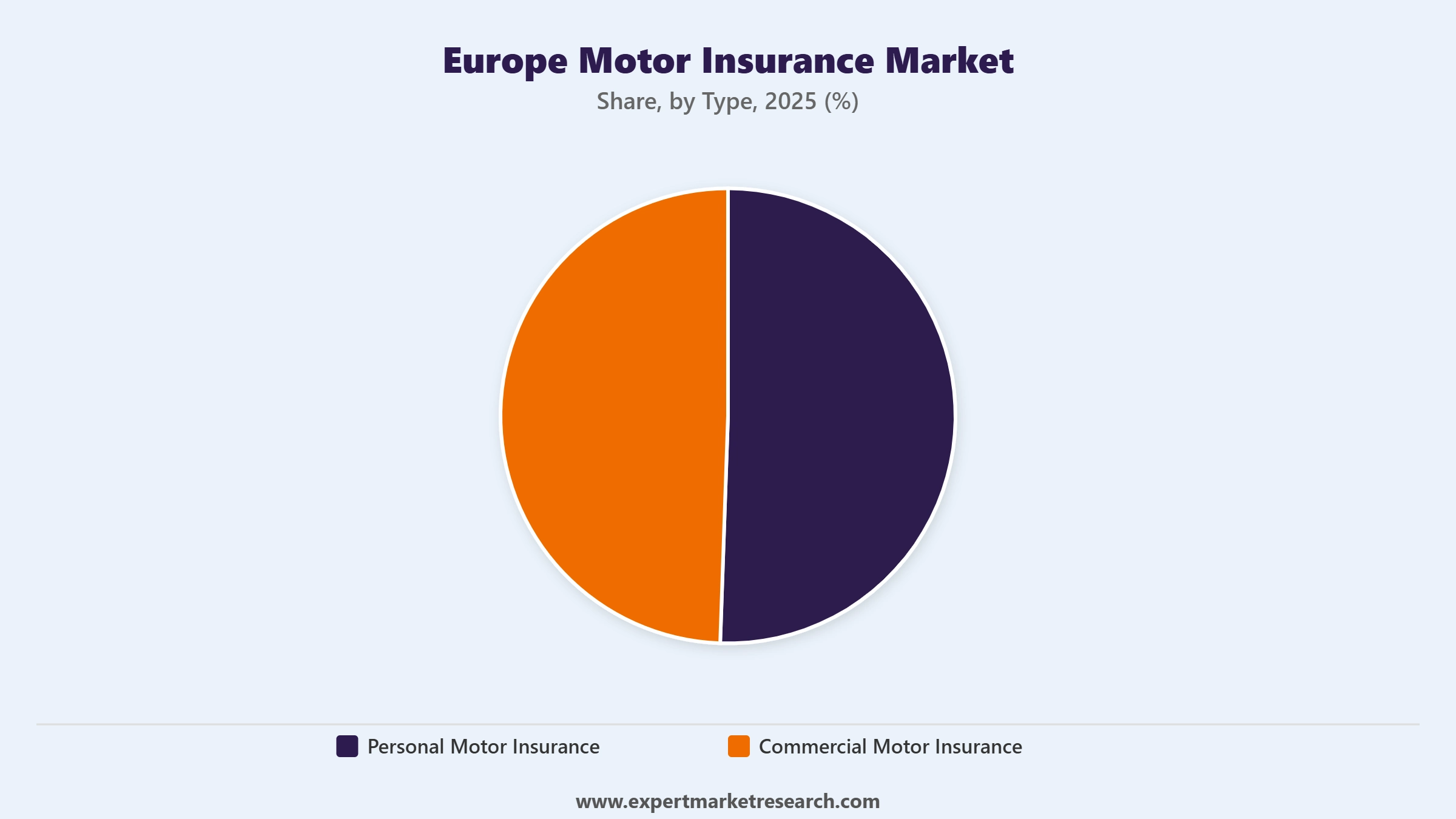

Market Breakup by Type

Key Insight: Personal motor insurance largely contributes to the Europe motor insurance market penetration through compulsory coverage and predictable renewals. Commercial motor insurance drives innovation and margin opportunities through fleet analytics and flexible policy design. In January 2024, Qover entered the United Kingdom motor insurance market with innovative embedded solutions, redefining the insurance experience for OEMs.

Market Breakup by Policy Type

Key Insight: As per the Europe motor insurance market report, comprehensive insurance leads the industry due to vehicle complexity and repair economics. Third-party fire and theft gain momentum as a mid-tier option for value driven buyers. Pure third-party coverage remains mandatory driven but price sensitive. Insurers design tiered pathways allowing customers to shift their policies as per their convenience.

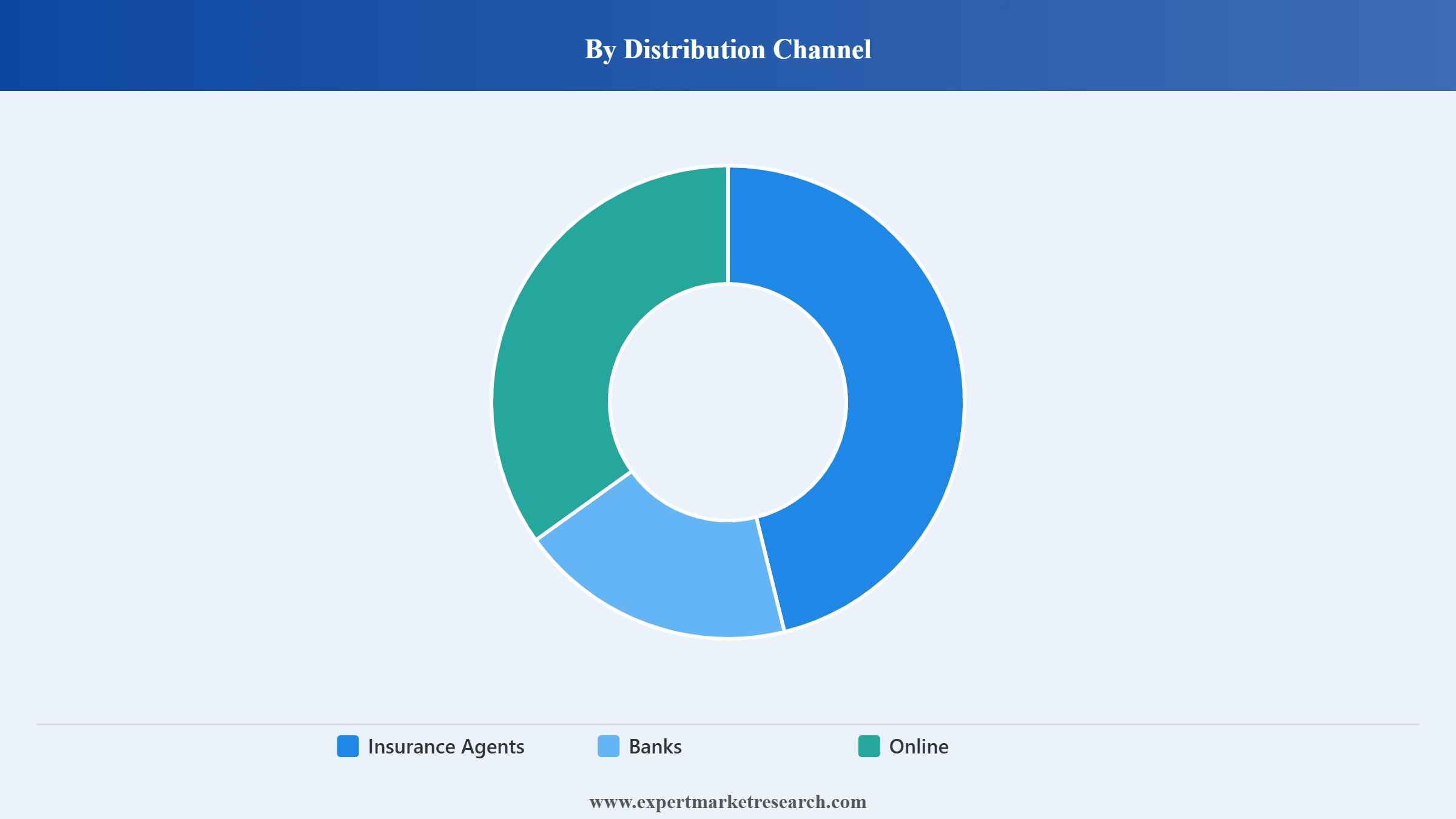

Market Breakup by Distribution Channel

Key Insight: Insurance agents continue dominating trust driven sales for complex policies and renewals. Online channels are expanding their share in the Europe motor insurance market revenue, improving reach, speed, and acquisition efficiency through comparison platforms. Banks and alternative channels support niche bundling, particularly financing and leasing linked insurance. Insurers are increasingly orchestrating channels through unified pricing and data systems instead of internal competition. This coordinated approach improves profitability, strengthens retention, and delivers consistent customer experience across markets regionally.

Market Breakup by Country

Key Insight: Germany anchors the Europe motor insurance market growth with scale, stability, and disciplined underwriting practices. Italy drives growth through telematics adoption and data led pricing innovation. The United Kingdom remains highly competitive on price, shaping efficiency focused product designs. France balances regulatory oversight with steady demand for comprehensive coverage. Other European markets exhibit selective growth tied to enforcement improvements and digital distribution.

By type, personal motor insurance leads market growth due to compulsory ownership coverage

Personal motor insurance accounts for the largest share of the Europe motor insurance market due to mandatory coverage laws and high private vehicle ownership. Insurers focus on pricing accuracy retention and claims efficiency rather than pure volume expansion. Product development emphasizes telematics enabled pricing, claim bonus optimization, and modular add-on services. Major players design policies that adjust premiums based on driving behavior mileage and vehicle type. In July 2024, Qover announced the launch of its innovative motor insurance solution in Ireland, aligning with this trend in the market.

Commercial motor insurance is growing faster due to fleet expansion, gig economy logistics, and SME delivery services. Insurers are developing flexible fleet products with usage-based pricing and real-time policy activation. Commercial customers value downtime reduction and claims turnaround speed. Providers now bundle risk management analytics, driver monitoring, and preventive services. Product innovation focuses on short term coverage scalable fleet sizes and cross border operations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By policy type, comprehensive motor insurance dominated due to broader risk coverage

Comprehensive motor insurance dominates the market due to higher vehicle values, repair complexity, and consumer risk awareness. Insurers emphasize coverage depth including own damage theft, weather events, and vandalism. Product differentiation centers on repair network access, replacement vehicle guarantees, and faster settlement timelines. Comprehensive policies also support add-ons like battery protection for electric vehicles. Insurers prefer this policy category due to higher premiums and better cross-sell potential.

Third party fire and theft insurance observes exponential growth in the Europe motor insurance market among cost sensitive consumers and older vehicle owners. Insurers position this policy as a balance between affordability and asset protection. Growth is driven by used car markets and urban ownership patterns. Product innovation includes flexible deductibles and theft focused analytics. Insurers also use this segment to upsell comprehensive coverage over time. In January 2026, Sedgwick announced the launch of its Global Specialty platform, expanding its capabilities in handling large and complex losses.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By distribution channel, insurance agents dominate the market due to trust-led advisory models

Insurance agents dominate distribution due to trust relationship management and advisory support. Complex policy options and claims assistance reinforce agent relevance. Insurers rely on agents to manage retention upselling and regulatory compliance. Agents are particularly strong in personal and SME segments. Product launches are often routed through agent networks for controlled adoption. Despite digital growth, agents remain central to premium portfolios in Europe. Insurers invest in agent digitization tools rather than bypassing channels entirely.

Online distribution, driven by price comparison platforms and direct to consumer strategies, experiences rapid growth in the Europe motor insurance market. Insurers launch digital only brands targeting younger customers. Online channels reduce acquisition costs and enable rapid scaling. Product design emphasizes simplicity, transparency, and instant issuance. Claims reporting and renewals are fully digital in this particular category. Online growth complements rather than replaces traditional channels. For example, Swiss InsurTech company Radity partnered with Bridger Insurance to launch a new digital distribution platform in November 2025.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Germany continues to dominate the market owing to a high volume of registered and insured cars

Germany dominates the Europe motor insurance market because of the large number of insured vehicles, the strict enforcement of the compulsory coverage, and the disciplined underwriting culture. Insurers in Germany tend to focus more on operational efficiency, claims predictability, and cost containment rather than on the aggressive acquisition of customers. Leading insurers are gradually introducing telematics, based pricing models, but their main focus is risk selection rather than offering steep discounts. For example, German ICMIF member, HUK, COBURG offers Telematik Plus, its new telematics insurance program available for drivers of all ages.

Italy represents the fastest growing motor insurance market in Europe, driven largely by deep telematics penetration and strong fraud mitigation frameworks. Usage based insurance has moved from niche to mainstream, allowing insurers to price risk with greater accuracy. Italian insurers actively leverage driving behavior data to reduce claims frequency and improve combined ratios. Regulatory acceptance of telematics data in claims and liability disputes has strengthened insurer confidence. Digital claims management tools are widely deployed to shorten settlement cycles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Major Europe motor insurance market players are concentrating on telematics integration, EV-specific coverage, and AI-driven claims handling to maintain their profits in mature markets. The strongest opportunities exist in usage, based insurance, fleet and gig economy coverage, and cross, border digital distribution enabled by EU passporting rules. Besides this, insurers are also focusing on repair network partnerships to limit increasing claims severity, particularly for electric and connected vehicles.

Differentiation is coming now through faster settlement cycles, flexible coverage structures, and risk prevention services rather than lower prices. Europe motor insurance companies that have the scale to operate locally and comply with the evolving EU rules are in a better position to defend their market share. The competitive environment is changing in favor of insurers that can combine advanced analytics, strong capital discipline, and customer, centric digital platforms while quickly responding to regulatory and mobility changes across Europe.

AXA SA, founded in 1816 and headquartered in Paris, France, is a leading motor insurer in Europe. Besides being a leader in the industry, the company puts great emphasis on digital claims automation and EV insurance solutions. Furthermore, the company provides telematics, based motor products and, at the same time, it promotes prevention services through driver behavior insights.

GEICO was formed in 1936 and its main office is located in Chevy Chase, Maryland, United States. GEICO, which mainly concentrates on the United States, affects the European motor insurance market indirectly through its digital, first pricing and underwriting models. The company's focus on direct-to-consumer distribution and the use of automation have set competitive benchmarks.

Liberty Mutual Insurance has been in the insurance market since 1912 and is based in Boston, United States. In Europe, the company's presence is mainly through insurance of specialty and commercial motor segments. The company’s focus is on fleet, logistics, and corporate mobility. Liberty Mutual puts emphasis on risk engineering, analytics, driven underwriting, and commercial motor solutions that are tailor, made.

Allianz SE, established in 1890, with the main office located in Munich, Germany, has emerged to be a leading motor insurer in Europe offering both personal and commercial lines. The company is a pioneer in telematics, based pricing, digital, only brands, and provides EV, focused coverage. Allianz allocates substantial resources to AI claims processing and cross-border digital platforms.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Admiral Group plc, Assicurazioni Generali SpA, Chubb Group Holdings Inc., Nationwide Mutual Insurance Company, Royal & Sun Alliance Insurance Ltd, and Liverpool Victoria, among others.

Unlock the latest insights with our Europe motor insurance market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 271.19 Billion.

The market is projected to grow at a CAGR of 6.80% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 523.58 Billion by 2035.

Insurers are investing in telematics analytics expanding EV repair partnerships deploying AI claims tools strengthening digital distribution and tailoring products to fleet and mobility platform customers across Europe.

The key trends aiding the market expansion include the adoption of digital platforms for insurance and increasing consumer awareness of the insurance market.

The major types of insurance in the market are personal motor insurance and commercial motor insurance.

The major countries considered in the market are the United Kingdom, Germany, France, and Italy, among others.

The key players in the market include AXA SA, GEICO, Liberty Mutual Insurance, Allianz SE, Admiral Group plc, Assicurazioni Generali SpA, Chubb Group Holdings Inc., Nationwide Mutual Insurance Company, Royal & Sun Alliance Insurance Ltd, and Liverpool Victoria, among others.

Rising claims severity EV repair costs regulatory complexity price comparison pressure fraud risks and balancing digital investment with profitability remain persistent challenges for motor insurers across competitive European markets.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Policy Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.