Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

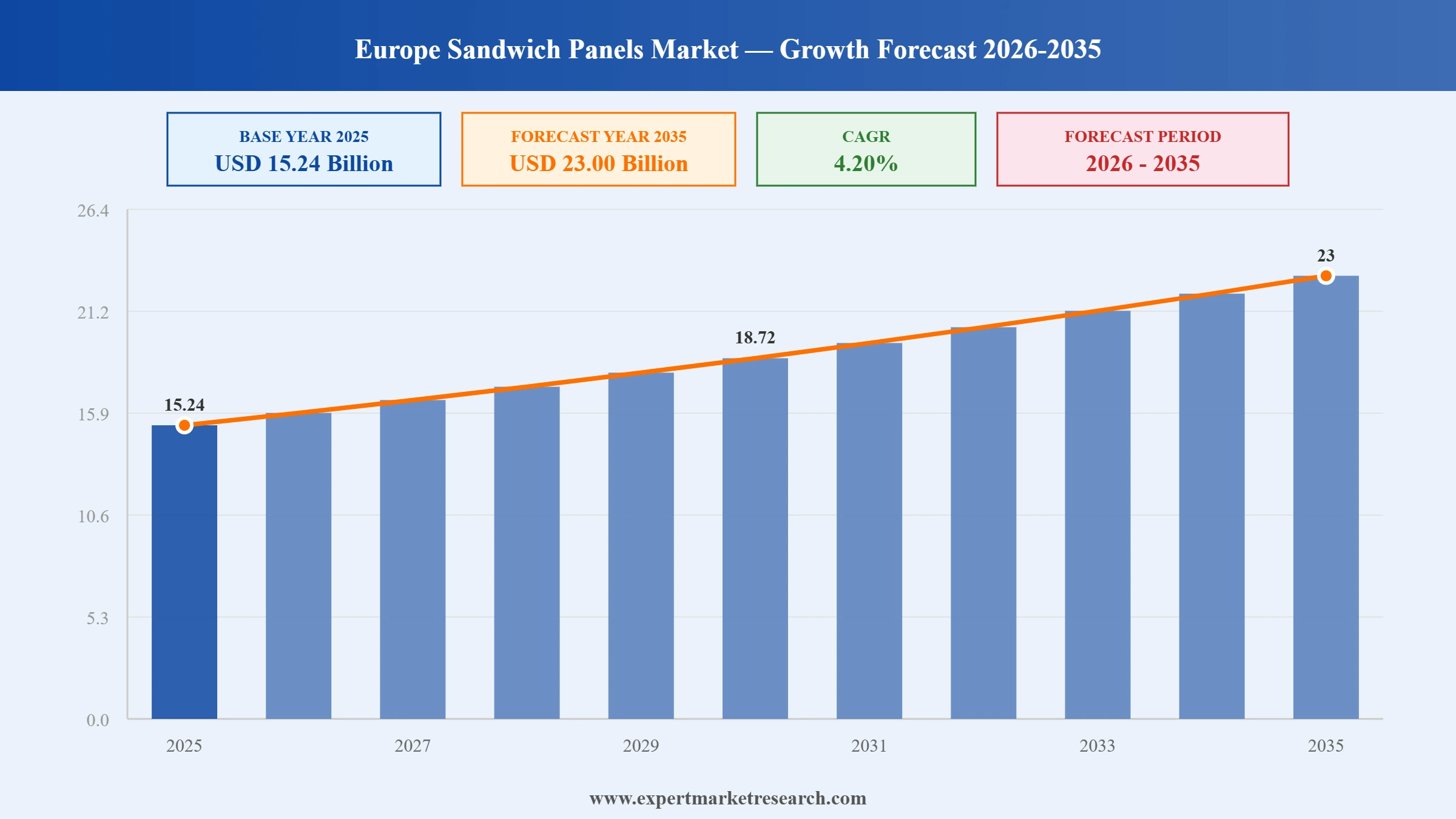

The Europe sandwich panels market reached a value of USD 15.24 Billion at 2025 and is projected to expand at a CAGR of around 4.20% during the forecast period of 2026-2035. With tightening EU energy-efficiency rules, fast-growing demand from logistics and cold-storage construction, a shift toward low-carbon and recycled-steel panels, and the speed advantages of prefabricated building envelopes, the market is expected to reach USD 23.00 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe's sandwich panels market is being driven by stringent EU energy rules, a logistics and cold-storage building boom, and a clear pivot toward low-carbon construction. Manufacturers are consolidating through cross-border acquisitions and joint ventures, while leaders race to cut embodied carbon using recycled steel and greener insulation cores. Fire-safety regulation is reshaping core choices, nudging demand toward mineral wool in the most sensitive building types.

In October 2025, Kingspan completed the acquisition of Mercor's daylighting and ventilation business in Poland, adding a growth platform across Central and Eastern Europe. The deal complements Kingspan's insulated-panel core and broadens its building-envelope offer in the regional sandwich panels market.

In September 2025, ArcelorMittal Construction was renamed ArcelorMittal Building Solutions. As the only European manufacturer managing the full coil-coating process in-house, the unit produces insulated and sandwich panels, with panels and insulation forming a substantial part of its construction business.

In July 2024, Marcegaglia Steel and Manni Group launched a joint venture in insulated and sectional door panels. The new entity became one of Europe's largest panel producers, serving clients across more than 70 countries and intensifying competition in the Europe sandwich panels market.

In May 2024, ArcelorMittal Construction completed the purchase of Italpannelli's Italy and Spain operations, adding plants in Abruzzo and Zaragoza with around 13 million square metres of annual capacity. The deal expanded its lightweight insulated sandwich panel range across Europe.

Tightening EU energy-savings obligations make high-performance insulation essential for new and refurbished buildings. Rising required savings through 2030 keep specifiers choosing insulated panels for walls and roofs, underpinning durable Europe sandwich panels market growth across residential, commercial, and industrial construction.

Deal activity is concentrating capacity among scaled players. ArcelorMittal's Italpannelli acquisitions and the July 2024 Marcegaglia-Manni joint venture show how mergers and acquisitions are reshaping the European panels supply base, lifting production scale and broadening geographic reach within the sandwich panels market.

Decarbonisation is moving from pledge to product. Kingspan's expanding low-embodied-carbon range and the use of recycled, renewably produced steel by producers such as Invespanel reflect a clear shift toward greener building envelopes across the Europe sandwich panels market and EN-standard lifecycle reporting.

The warehouse, logistics, and cold-chain boom is a major demand pull. Large-span industrial buildings rely on insulated wall and roof panels for speed, thermal control, and cost, sustaining strong order books and reinforcing the industrial end-use segment of the Europe sandwich panels market.

Post-Grenfell scrutiny and stricter fire codes are nudging specifiers toward non-combustible cores in sensitive buildings. This regulatory shift is lifting mineral wool demand fastest, even as PUR/PIR remains dominant overall, gradually rebalancing the core-material mix within the Europe sandwich panels market.

The report by Expert Market Research's titled “Europe Sandwich Panels Market Report and Forecast 2026-2035”, offers a detailed analysis of the market based on the following segments:

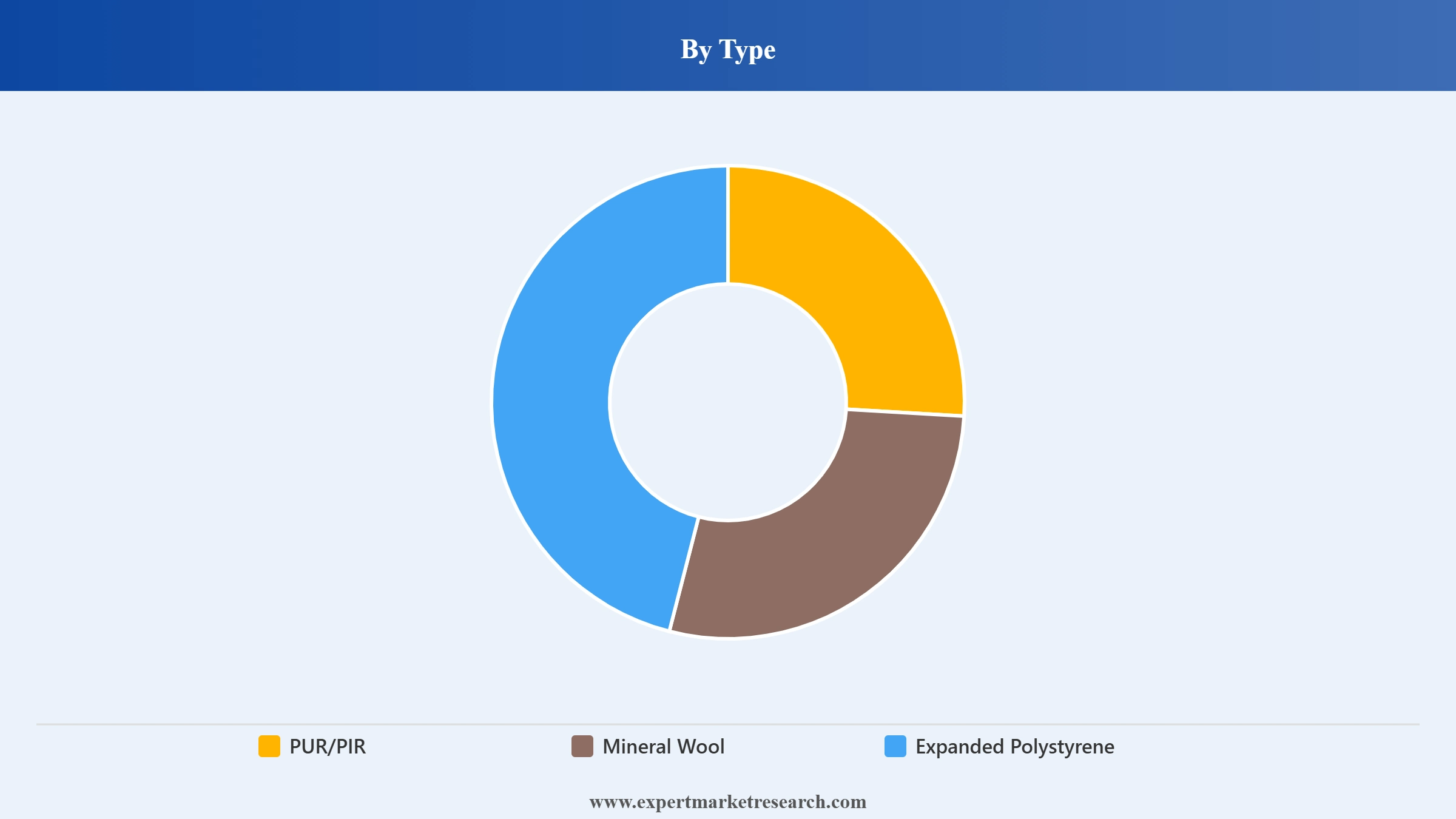

Market Breakup by Type

Key Insight: PUR/PIR cores lead the Europe sandwich panels market thanks to excellent thermal performance per unit thickness, light weight, and competitive cost, making them the default for energy-efficient walls and roofs. Mineral wool is the fastest-growing type, favoured where fire safety and acoustics are critical, a trend reinforced by stricter post-Grenfell codes. EPS serves cost-sensitive and cold-storage uses. This split lets specifiers balance insulation value, fire rating, and budget across diverse building projects.

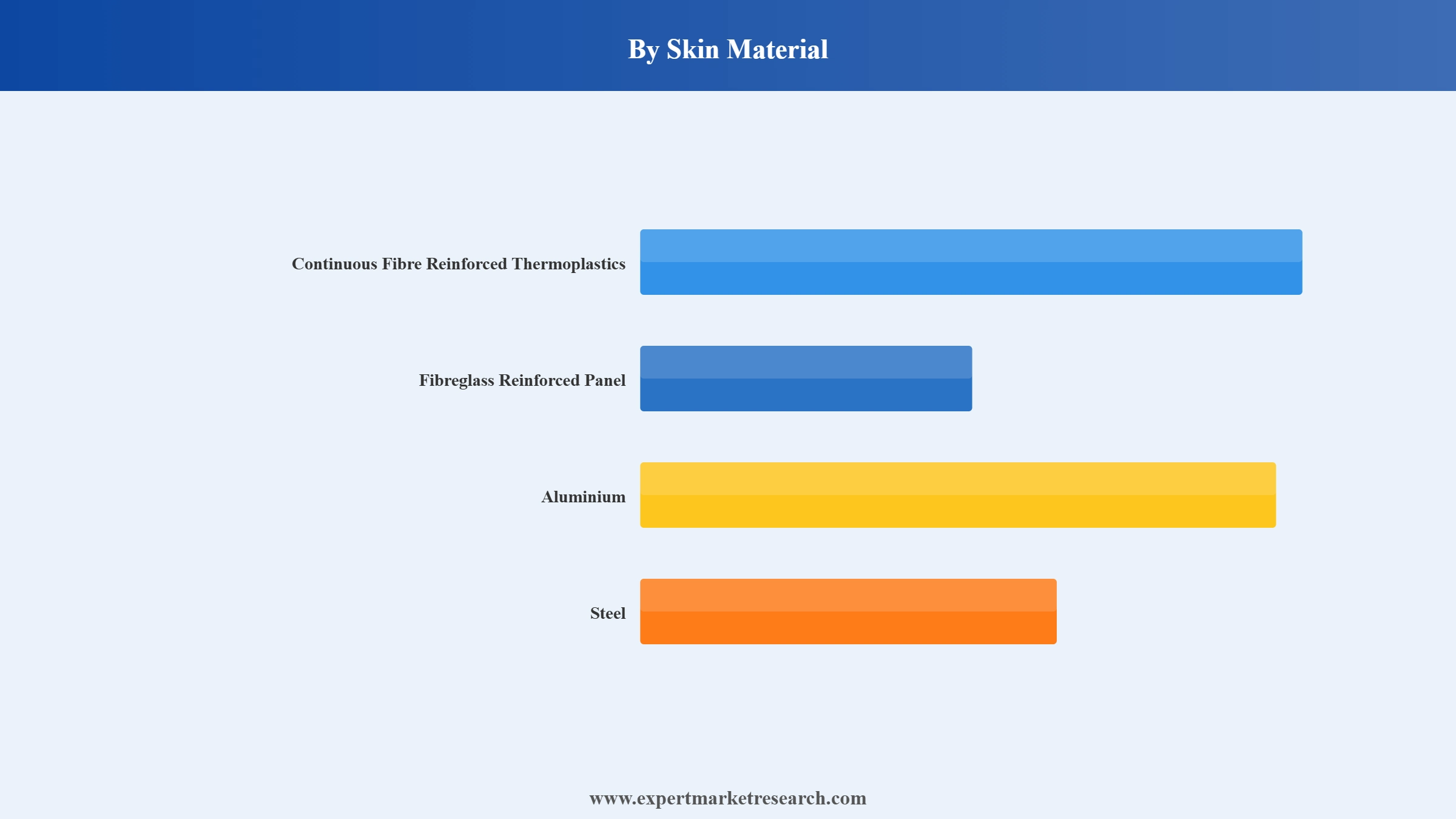

Market Breakup by Skin Material

Key Insight: Steel skins dominate the Europe sandwich panels market because they offer strength, durability, fire resistance, and easy coating for weatherproofing and aesthetics, making them standard for industrial and commercial envelopes. Aluminium suits lightweight and corrosion-prone applications, while FRP and CFRT serve specialised hygienic, chemical, and transport uses. Producers increasingly specify recycled and lower-carbon steel to meet EU sustainability goals, keeping steel the workhorse skin while greening its footprint.

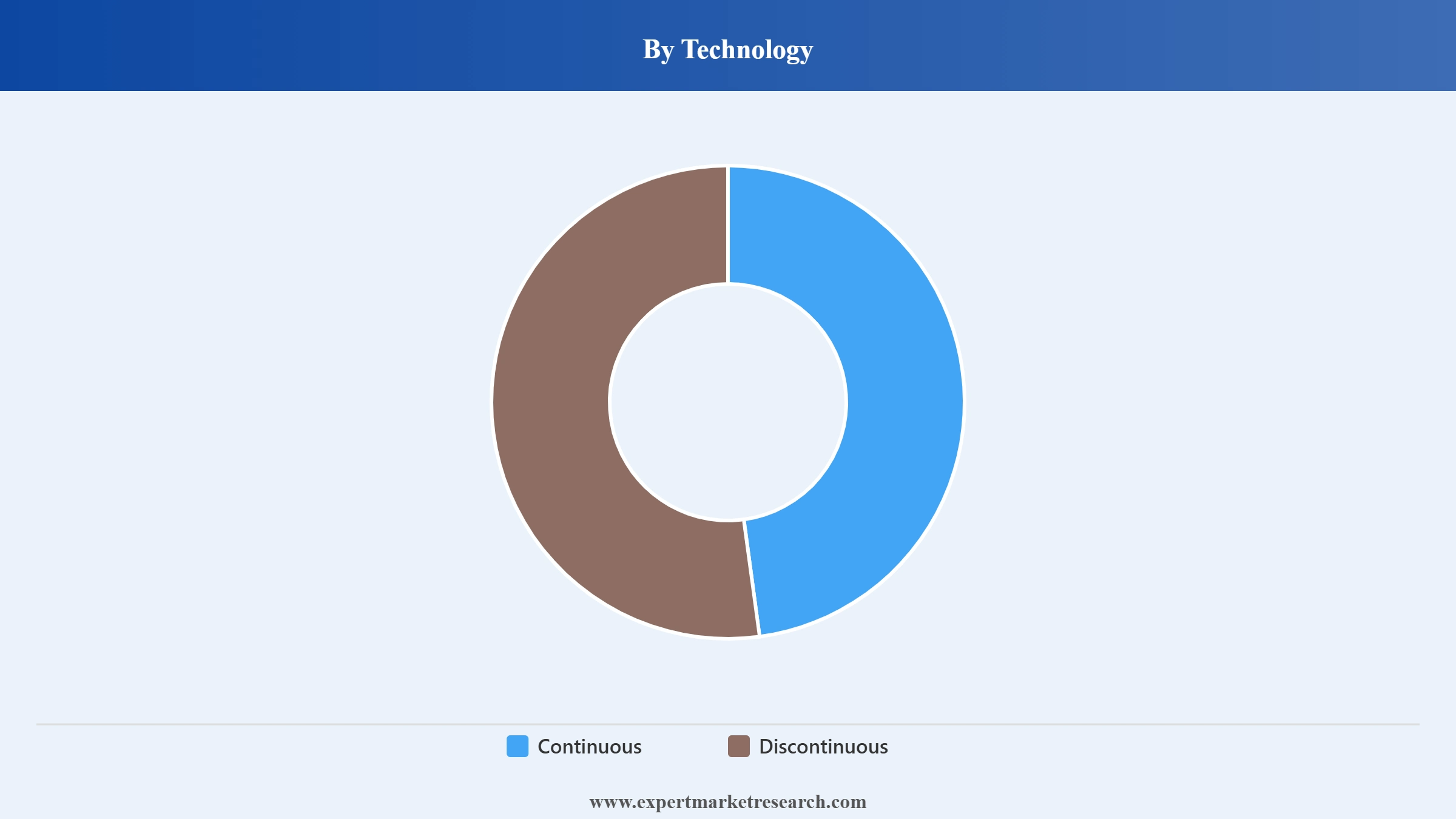

Market Breakup by Technology

Key Insight: Continuous lamination dominates, as automated continuous lines deliver consistent quality, high throughput, and lower unit cost for standardised wall and roof panels, suiting large-volume European production. Discontinuous, or press, technology remains valuable for shorter runs, bespoke dimensions, and certain mineral wool or specialty panels where flexibility matters more than scale. The balance lets manufacturers serve both high-volume commodity demand and customised project requirements within the sandwich panels market.

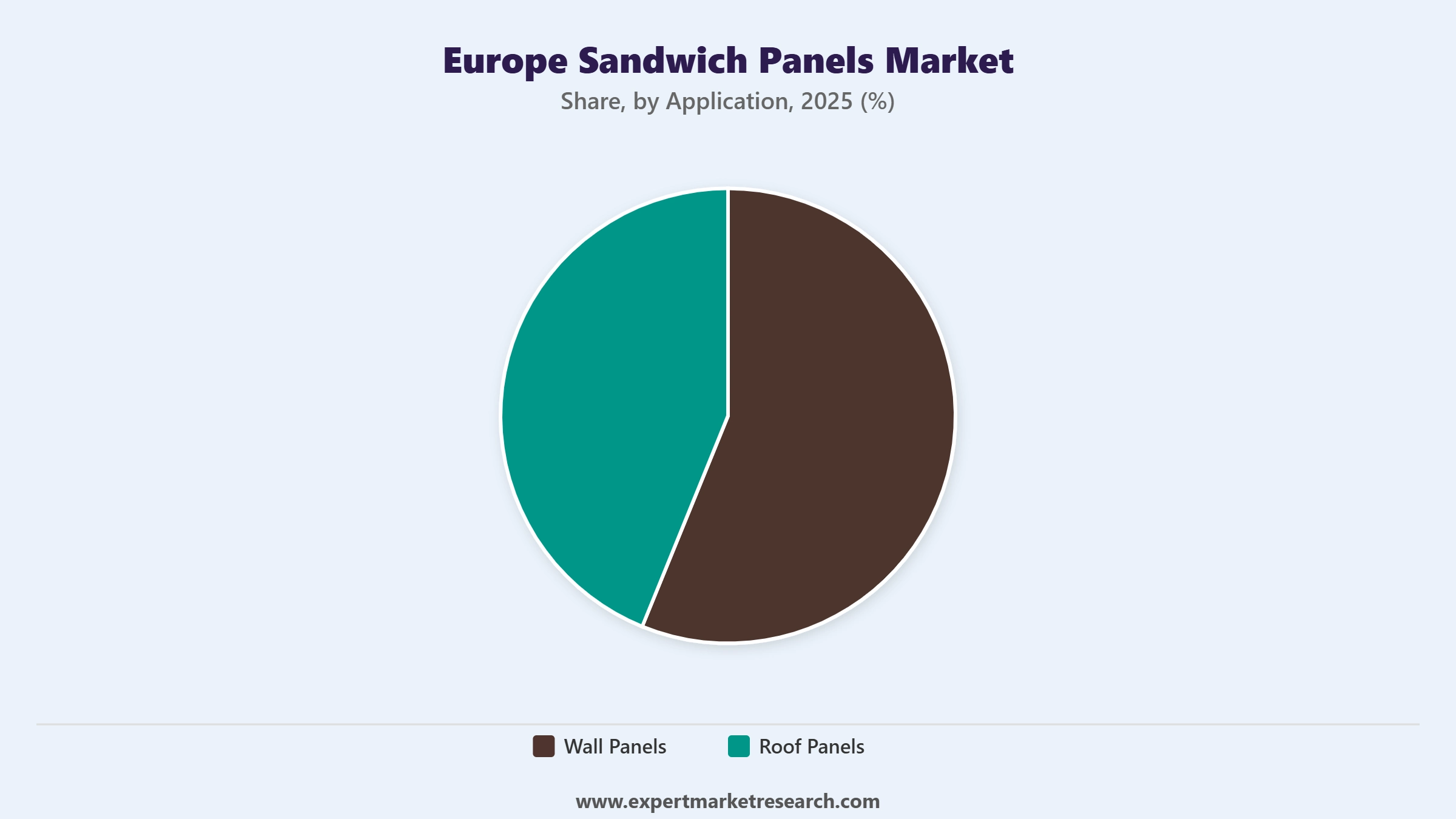

Market Breakup by Application

Key Insight: Wall panels hold the largest application share, used extensively across facades for industrial, commercial, and logistics buildings where thermal performance and fast installation matter. Roof panels grow steadily, essential for large-span warehouses, cold stores, and factories needing watertight, insulated coverage. Other applications, including partitions and cold-room systems, add niche demand. The dominance of wall and roof panels mirrors Europe's heavy pipeline of industrial and logistics construction within the sandwich panels market.

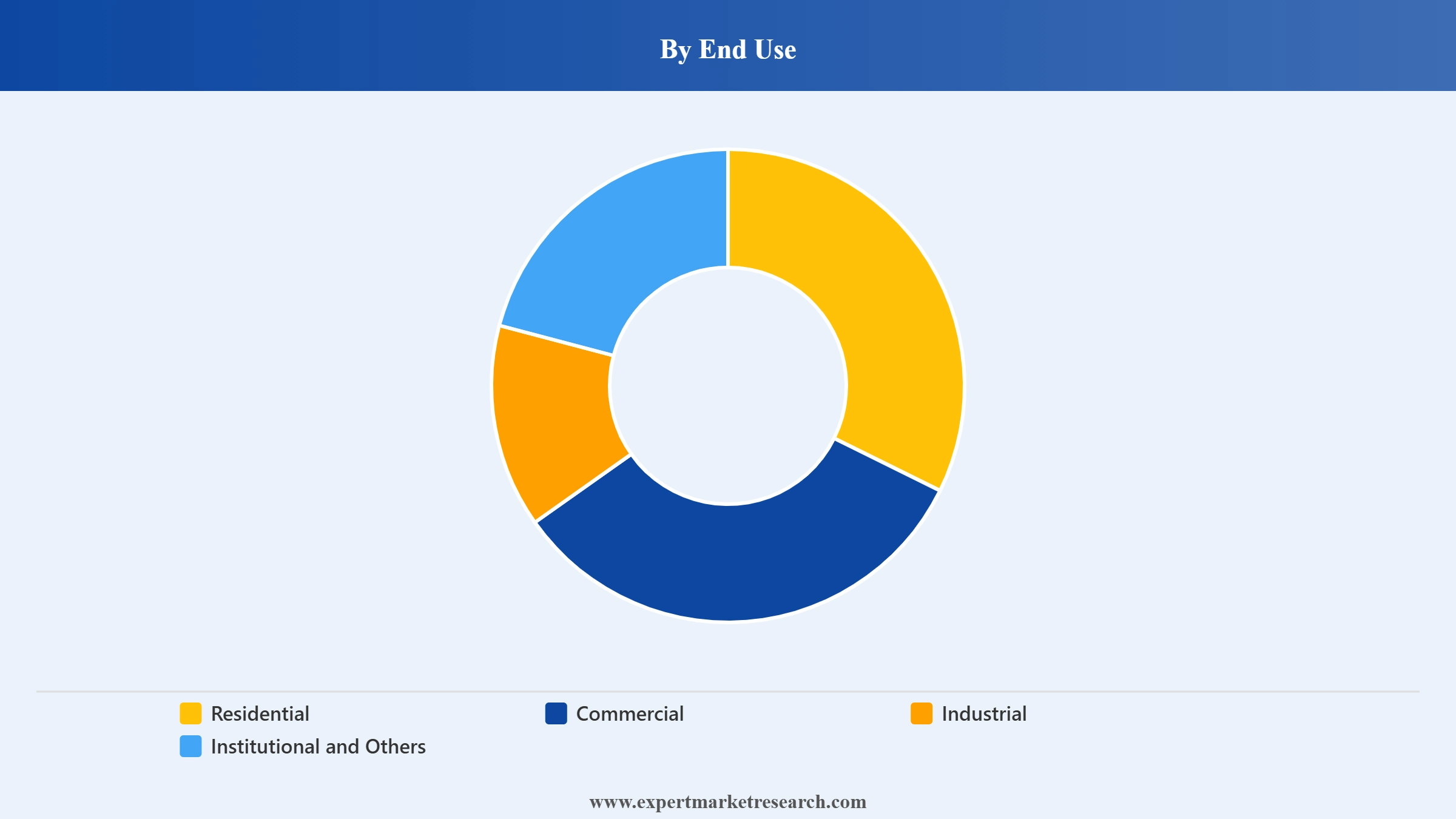

Market Breakup by End Use

Key Insight: Industrial end use leads the Europe sandwich panels market, driven by warehouses, factories, and cold-storage facilities that demand rapid, insulated, large-span envelopes. Commercial buildings, including retail and offices, form a strong second, while residential uptake grows as energy codes tighten. Institutional projects such as schools and hospitals add steady demand. The logistics and cold-chain boom keeps industrial firmly ahead, anchoring volume across the European panels market.

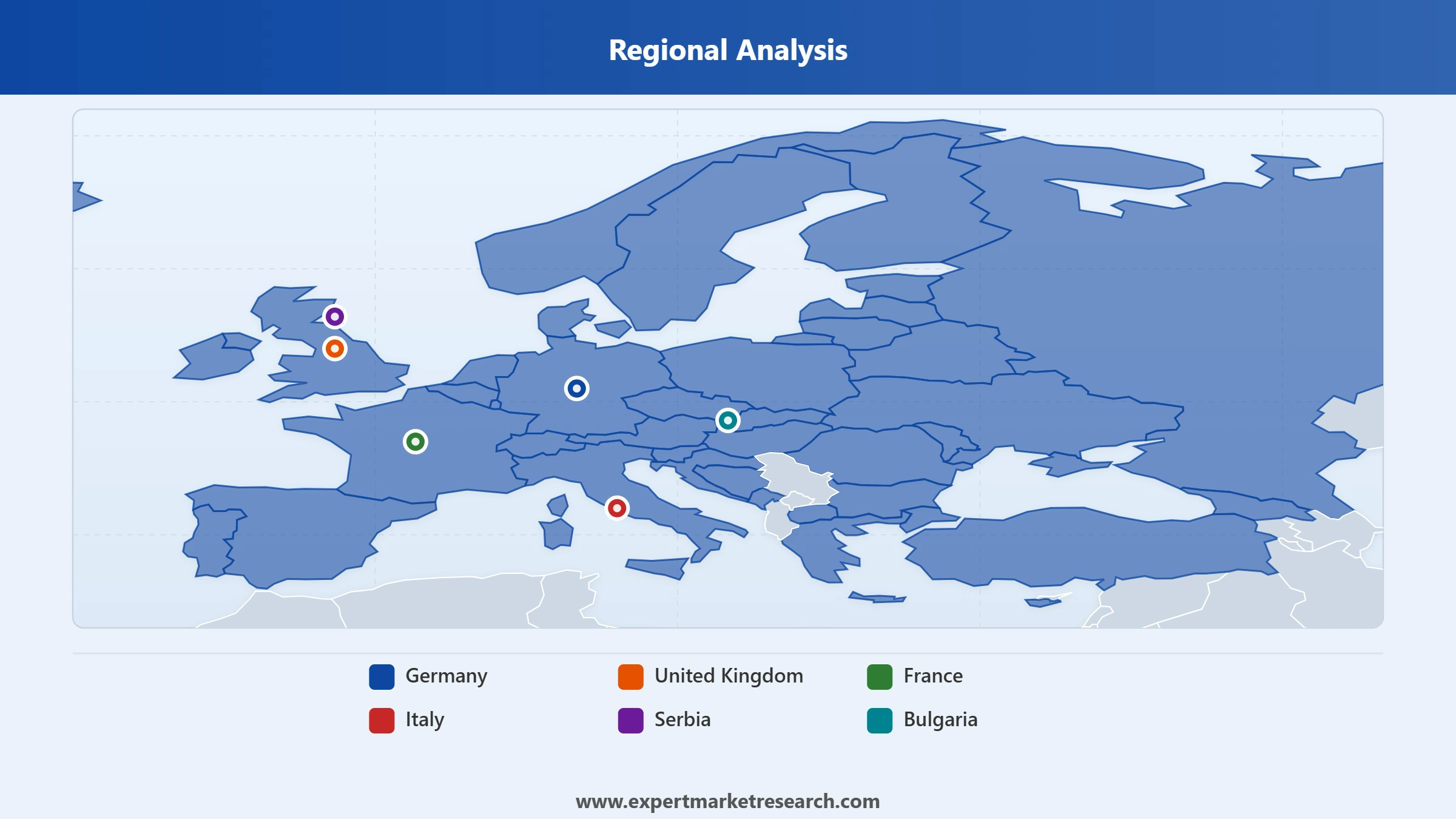

Market Breakup by Country

Key Insight: Germany leads the Europe sandwich panels market on the strength of its large industrial base, advanced construction sector, and strict energy standards. The United Kingdom and France follow with substantial commercial and logistics demand, while Italy combines strong manufacturing with major domestic producers. Serbia and Bulgaria are faster-growing emerging markets, benefiting from new industrial investment and lower-cost production. This spread reflects both mature western demand and rising central and southeastern European activity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, PUR/PIR panels dominate the market due to superior thermal performance and competitive cost

PUR/PIR panels hold the dominant share of the Europe sandwich panels market because their cores deliver outstanding thermal insulation for a given thickness, keeping buildings energy-efficient while remaining light and affordable. As EU energy-savings obligations tighten through 2030, specifiers continue to favour PUR/PIR for walls and roofs across industrial, commercial, and logistics projects. That blend of performance, weight, and cost keeps these panels the default insulated-envelope choice region-wide.

Mineral wool is the fastest-growing type, propelled by stricter fire-safety regulation in the wake of high-profile facade fires. Its non-combustible core and acoustic benefits make it the preferred option for tall, public, and sensitive buildings. Expanded polystyrene serves cost-sensitive and cold-storage uses. This regulatory-led rebalancing is gradually lifting mineral wool's role within the Europe sandwich panels market, even as PUR/PIR retains overall leadership.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By skin material, steel-faced panels dominate the market due to strength, durability, and cost efficiency

Steel-faced panels hold the dominant skin-material share of the Europe sandwich panels market, prized for structural strength, fire performance, durability, and competitive cost. Coil-coated steel skins bonded to insulated cores suit warehouses, cold stores, and industrial halls where speed and span matter. Wide availability of coated steel and integrated coil-coating capacity among leading producers keeps steel the default facing across most commercial and industrial projects.

Aluminium, fibreglass-reinforced panels, and composite skins occupy higher-value niches where corrosion resistance, weight, or architectural finish is critical. Demand for low-carbon and recycled-content steel skins is rising as decarbonisation targets tighten. Producers using recycled-steel facings show how sustainability is reshaping skin-material choices, though steel's balance of cost and performance keeps it the leading facing across the Europe sandwich panels market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By technology, continuously produced panels lead the market due to scale, consistency, and lower unit cost

Continuous production technology dominates the Europe sandwich panels market because it delivers high volumes, consistent quality, and lower unit costs for standardised wall and roof panels. Automated continuous lines bond facings and insulation in a single pass, suiting the large, repeatable orders that warehouses, logistics parks, and cold-storage projects demand. Major producers concentrate investment in continuous capacity to serve high-throughput construction across the region.

Discontinuous production retains an important role for bespoke, short-run, and specialised panels, including complex shapes, niche cores, and custom architectural facings. It offers flexibility where volumes are low or specifications unusual. As prefabrication and modular construction expand, both technologies grow, yet continuous manufacturing remains the leading and most cost-efficient route across the Europe sandwich panels market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By application, wall panels hold the dominant share due to widespread facade use and fast installation

Wall panels account for the dominant application share of the Europe sandwich panels market, used extensively across facades of industrial units, warehouses, retail parks, and commercial buildings. Their combination of thermal performance, structural strength, and rapid installation makes them ideal for the prefabricated, fast-track construction favoured across Europe. The sheer volume of industrial and logistics buildings under development keeps wall panels at the centre of regional demand.

Roof panels form the fastest-growing application, indispensable for large-span warehouses, cold stores, and factories requiring watertight, insulated coverage. The logistics and cold-chain construction boom is a key driver here. Other applications, including internal partitions and modular cold-room systems, add specialised demand. Together, wall and roof panels mirror Europe's heavy pipeline of energy-efficient industrial construction shaping the sandwich panels market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By end use, the industrial segment holds the dominant share due to warehouse and cold-storage construction

The industrial segment dominates the Europe sandwich panels market, fuelled by a wave of warehouse, factory, and cold-storage construction that demands large-span, insulated, quickly erected envelopes. Sandwich panels meet these needs precisely, offering thermal control, structural performance, and speed of build. The continued expansion of e-commerce logistics and cold-chain capacity across Europe sustains a deep order book, keeping industrial firmly ahead of other end uses.

Commercial buildings such as retail outlets and offices form a strong second segment, while residential uptake grows as energy-performance codes tighten for new homes and refurbishments. Institutional projects, including schools, hospitals, and public facilities, add steady, regulation-driven demand. This balanced end-use profile, anchored by industrial construction, supports resilient growth across the Europe sandwich panels market through building cycles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Germany dominates the market due to its large industrial base, advanced construction sector, and strict energy standards

Germany leads the Europe sandwich panels market, supported by Europe's largest manufacturing economy, a sophisticated construction sector, and some of the region's strictest energy-efficiency standards. Heavy investment in logistics, automotive, and industrial facilities drives sustained demand for insulated wall and roof panels. The presence of major producers and stringent building codes also push adoption of high-performance and low-carbon panels, reinforcing Germany's position as the region's anchor market for sandwich panels.

Serbia and Bulgaria are among the fastest-growing markets, benefiting from new industrial investment, expanding logistics corridors, and competitive local production costs. Western markets such as the United Kingdom and France also grow steadily, lifted by warehouse construction and fire-safety-led demand for mineral wool cores. In September 2025, ArcelorMittal Building Solutions reinforced its European footprint, reflecting how producers are positioning for both mature and emerging demand across the sandwich panels market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Europe sandwich panels market is moderately consolidated, led by large vertically integrated producers alongside strong regional specialists. Major players combine steelmaking, coil coating, and panel manufacturing to control quality and cost, while focused producers compete on service, customisation, and local proximity. Scale, energy performance, and fire-safety credentials are the primary battlegrounds, and cross-border acquisitions continue to reshape the competitive map.

Strategy increasingly centres on decarbonisation, with leaders cutting embodied carbon through recycled steel and greener insulation cores, and on consolidation through mergers, acquisitions, and joint ventures. Producers also differentiate via fire-rated mineral wool ranges, fast-track installation systems, and full building-envelope offerings. Those able to pair sustainability with production scale and reliable delivery are best placed to defend and grow share across the European panels market.

Founded in 1972 and headquartered in Kingscourt, Ireland, Kingspan is a global leader in insulation and building-envelope solutions. Its insulated and sandwich panels span walls and roofs, and through 2025 it expanded low-embodied-carbon ranges and acquired complementary businesses, including Mercor's daylighting operations in Poland, strengthening its European platform.

Headquartered in Luxembourg and formed in 2006, ArcelorMittal is the world's leading steel and mining group. Its construction arm, renamed ArcelorMittal Building Solutions in September 2025, manages the full coil-coating process in-house and produces insulated and sandwich panels, profiles, and turnkey steel building systems across Europe.

Part of Turkey's Kibar Holding and headquartered near Istanbul, Assan Panel is a leading manufacturer of insulated sandwich panels for roofs and facades. Serving European and Middle Eastern markets, it offers PUR, PIR, mineral wool, and EPS panels, competing on capacity, breadth, and competitive production economics.

Founded in 1960 and based in Finland, Rautaruukki, known by the Ruukki brand and part of SSAB, supplies steel building components including energy-efficient sandwich panels and roofing. Its Nordic engineering heritage and focus on durable, high-performance envelopes give it a strong position across northern and central European construction.

Other key players in the market are Adamietz Sp. z o.o., PaNELTECH Sp. z o.o., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the full intelligence on the Europe sandwich panels market with our latest report. See how tightening energy rules, low-carbon construction, fire-safety regulation, and the logistics boom are reshaping demand, and where the next opportunities are opening across types and countries. Whether you manufacture panels, make steel, build, develop, or invest in construction, this report gives you the clarity to act. Download your free sample today and explore the key opportunities across sandwich panels.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 15.24 Billion.

The market is projected to grow at a CAGR of 4.20% between 2026 and 2035.

The Europe sandwich panels market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 23.00 Billion by 2035.

Key strategies driving the market include investments in sustainable materials, adoption of energy-efficient building standards, expansion of production capacity, and strategic partnerships or acquisitions. Manufacturers are focusing on circular economy principles, fire and thermal performance, and meeting EU Green Deal targets to cater to growing demand in construction and infrastructure.

The key market trends guiding the growth of the market include the rising investments by the market players in the development of eco-friendly sandwich panels.

The major European countries in the market are United Kingdom, Germany, France, Italy, Serbia, Bulgaria and others.

The significant types include PUR/PIR, mineral wool, expanded polystyrene (EPS), and others.

Based on skin material, the market covers continuous fibre reinforced thermoplastics (CFRT), fibreglass reinforced panel (FRP), aluminium, steel, and others.

The major market segments, based on technology include continuous and discontinuous.

The major applications include wall panels, roof panels, and others.

The significant end uses of the product include residential, commercial, industrial, and institutional and others.

The key players in the market include Kingspan Group, ArcelorMittal Construction, Isopan (Manni Group), Metecno Group, Assan Panel, Romakowski GmbH & Co. KG, Balex Metal, Tata Steel Europe, Fischer Profil and Hoesch Bausysteme GmbH.

Key challenges for market players include volatile raw material prices, strict environmental and fire safety regulations, and supply chain disruptions. Intense competition and the need for continuous innovation in sustainable materials increase pressure. Additionally, adapting to diverse regional building codes and labor shortages complicate expansion and operational efficiency across markets.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Skin Material |

|

| Breakup by Technology |

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.