Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The GCC cement market reached a volume of 101.90 MMT in 2025. The market is expected to grow at a CAGR of 4.50% during the forecast period of 2026-2035 to reach a volume of 158.25 MMT by 2035. Rising adoption of low-carbon cement alternatives across GCC megaprojects is driving manufacturers to invest in clinker substitution technologies, enhancing sustainability compliance while securing long-term infrastructure supply contracts.

The GCC cement market is undergoing a significant transformation as companies ramp up their efforts to develop low carbon clinkers and expand capacity beyond their borders. For instance, in December 2023, thyssenkrupp Polysius announced plans to build new clinker line for GCC, increasing capacity, reducing emissions, and supporting infrastructure-driven cement demand growth. The company's decision was prompted by Saudi Arabia's industrial decarbonization framework. Such developments are aided by growing demand for green products in giga projects like NEOM, which consumes millions of tons of sustainable cement every year.

Most of the GCC cement market players are adjusting the composition of cement to suit its performance in harsh weather conditions. Companies like UltraTech Cement Ltd are increasing their exports via its subsidiaries due to high demand for marine cement in the UAE's coastal construction projects, whereas Qatar National Cement Company is deploying energy-efficient waste heat recovery technology. On the other hand, in December 2025, CHASM and Saudi Readymix demonstrated CNT-enhanced low-carbon concrete using local materials, improving durability, reducing emissions, and supporting scalable sustainable construction solutions.

With the rise of government-sponsored housing projects and transport networks, the overall demand in the GCC cement market is being heightened even further, although with procurement processes now being more dependent on Environmental, Social and Governance considerations for measuring compliance. This has led to firms relying on digital kiln monitoring and AI-based predictive maintenance technologies to reduce downtime and increase production stability. Strategic relationships with key construction companies as well as contractual commitments for supply are also becoming critical for stable revenue, with regional firms competing not only on sustainability but also in terms of efficiency.

Compound Annual Growth Rate

4.5%

Value in MMT

2026-2035

|

GCC Cement Market Report Summary |

Description |

Value |

|

Base Year |

MMT |

2025 |

|

Historical Period |

MMT |

2019-2025 |

|

Forecast Period |

MMT |

2026-2035 |

|

Market Size 2025 |

MMT |

101.90 |

|

Market Size 2035 |

MMT |

158.25 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

4.50% |

|

CAGR 2026-2035 - Market by Country |

Saudi Arabia |

5.1% |

|

CAGR 2026-2035 - Market by Country |

UAE |

4.8% |

|

CAGR 2026-2035 - Market by Type |

Blended |

5.0% |

|

CAGR 2026-2035 - Market by End Use |

Infrastructural |

4.9% |

|

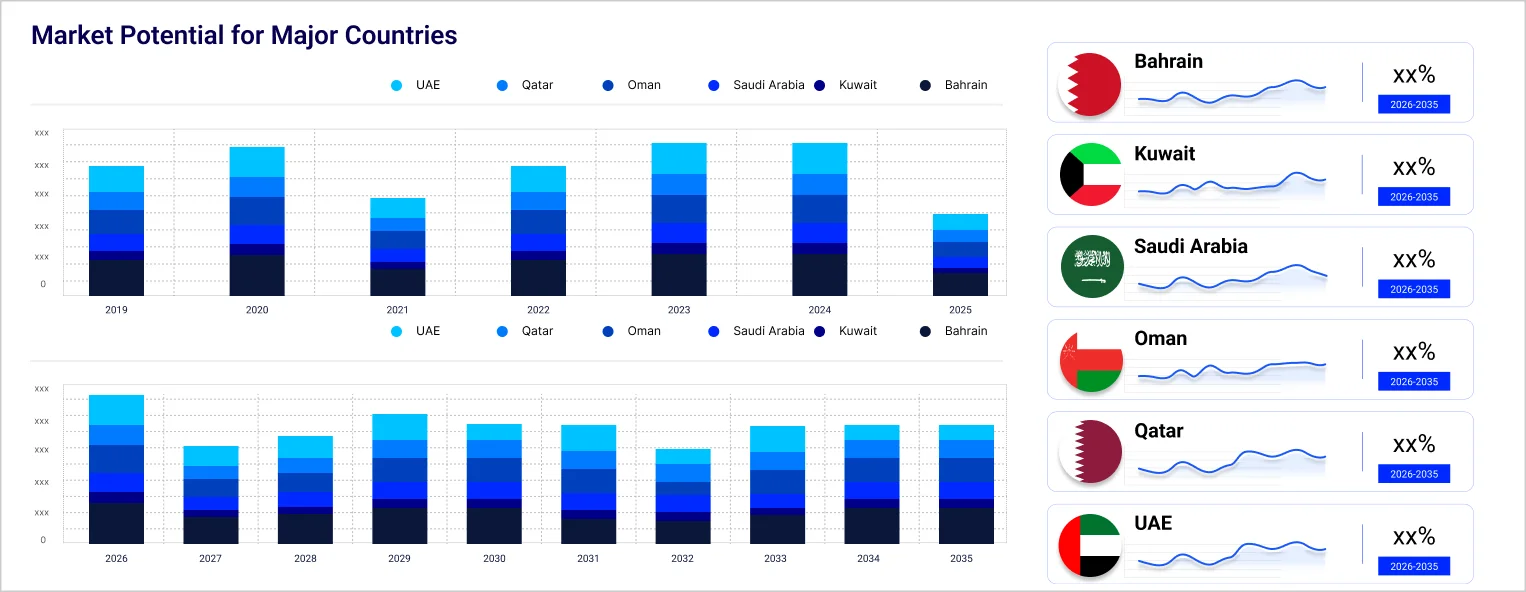

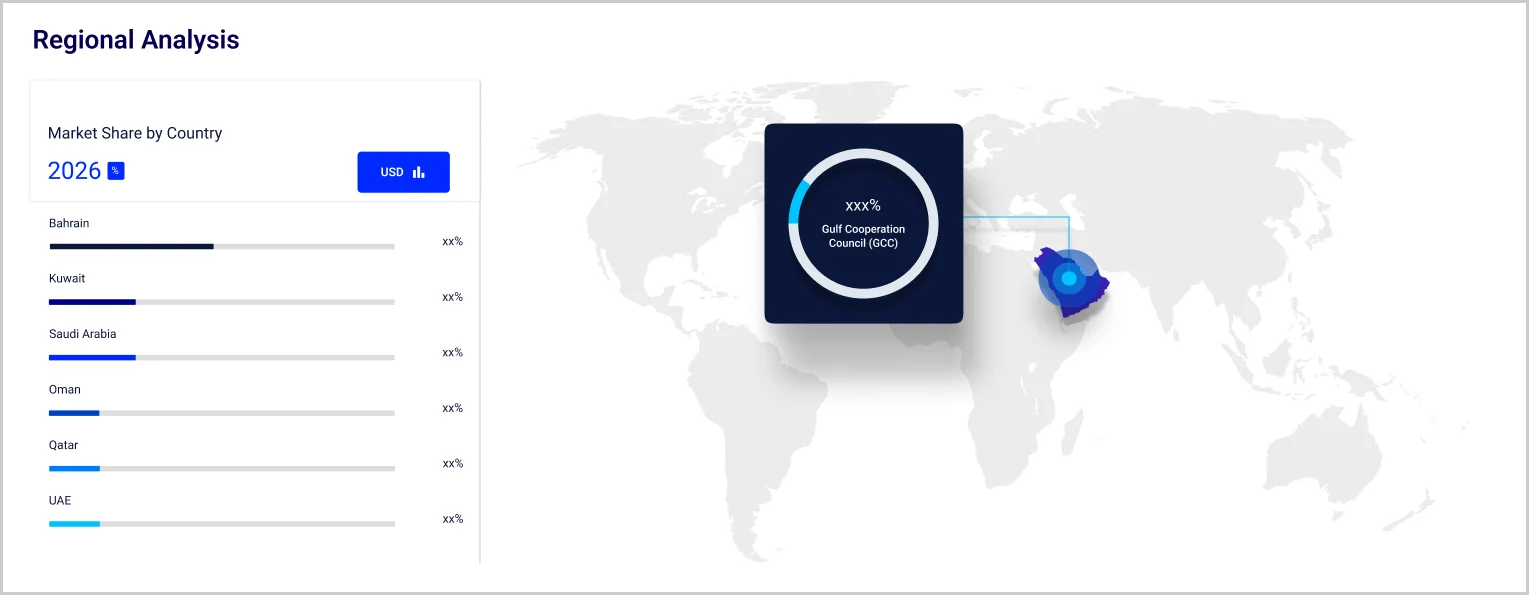

2025 Market Share by Country |

Saudi Arabia |

50.1% |

Southern Province Cement Company advanced its Jazan cement plant to the trial stage, boosting regional clinker production capacity, strengthening supply reliability, and supporting demand driven by infrastructure-led construction activity. Similarly, other firms can capitalize on rising construction demand in the GCC cement market by expanding capacity and bringing late-stage projects into operation.

Holcim collaborated with 44.01 to initiate CO₂ mineralization technology, which facilitates the capture of carbon permanently during the process of cement manufacturing. Firms can benefit by adopting carbon capture and mineralization technologies in line with the need for carbon emission reduction.

City Cement Company introduced low-carbon concrete by adopting state-of-the-art supplementary cementitious materials that decreased carbon footprints without compromising quality standards. Manufacturers can adopt innovative approaches to use different materials and low-carbon concrete mixes to adhere to sustainable practices and cater to environmentally-oriented construction projects.

Hoffmann Green Cement Technologies entered the Saudi Arabian market by offering clinker-free cement products to cut down carbon footprints and revolutionize cement manufacturing processes in the region. New firms can capitalize on clinker-free manufacturing methods and collaborations to disrupt conventional manufacturing processes, capitalizing on these developments in the GCC cement market.

GCC-based cement producers are expanding low-carbon cement ranges to meet national pledges regarding net-zero emission targets. Producers are including alternatives like calcined clay, slag-based, and alternative binder cements in order to minimize clinker content. Moreover, cement companies are getting involved in supply arrangements for future infrastructure projects, ensuring their market share in coming years. Additionally, the ongoing carbon pricing debate and rising green building certifications require companies to widen their product range to include more lucrative solutions. Demonstrating such trends in the GCC cement market, in November 2025, Cementir Group launched D-Carb white cement the Middle East, offering lower-carbon solutions, supporting sustainable construction demand and regional decarbonization strategies.

Energy efficiency is now becoming one of the primary competitive advantages for producers in the GCC cement market. They use waste heat recovery (WHR) systems to utilize waste heat and turn it into electric power, thereby minimizing dependence on other types of energy and lowering emissions. For example, in February 2026, Riyadh Cement initiated waste heat recovery project pilot operations, generating electricity from process heat, reducing energy costs and emissions significantly. In addition, regional governments are offering various incentives for energy-efficient operations within industries, thus allowing such projects to become economically feasible. These developments are enabling producers to stabilize production costs amid volatile fuel prices, while improving sustainability metrics critical for securing contracts tied to large-scale infrastructure developments.

The GCC cement market is witnessing transformations through digital technology adoption. Firms within the industry are integrating machine learning algorithms, sensors, and real-time analysis of their kilns to enhance plant efficiency and decrease unplanned shutdowns. Through predictive maintenance software, firms are being able to avoid major breakdowns by predicting them beforehand. The leading cement firms are also partnering with technology firms to introduce smart plants, thereby gaining increased control over the quality of their products and energy use in the manufacturing processes. In December 2025, Acciona launched DIGICONCRETE digital platform enabling real-time concrete monitoring, improving quality control, traceability, compliance, and efficiency across complex construction projects.

The GCC cement market is experiencing integration within regional trade. Firms are adopting cross-border trading strategies that allow them to match capacity utilization and cope with demand fluctuations among neighboring countries. For instance, Oman is expanding its export routes to Bahrain and the UAE through improved ports. These efforts are allowing firms in the industry to streamline their logistics to facilitate fast-paced project delivery. In October 2025, NEOM unveiled USD 187 million green concrete factory, enabling high-capacity production, integrating carbon capture technologies, and supporting large-scale sustainable urban construction projects.

Cement companies are forming relationships with the constructors of mega projects through signing agreements that ensure a steady flow of business and income for them. In some instances, firms align their products based on the demands set forth by the projects. These include cement designed for high strength and resistance to harsh environmental conditions. The need for such materials is brought about by new projects like NEOM and other smart cities being created. Aligning this shift in the GCC cement market, in July 2025, Fayhaa Cement launched white cement plant in Adra Industrial City, boosting local production, reducing imports, and supporting Syria’s reconstruction-driven construction demand.

The EMR’s report titled “GCC Cement Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: The segmentation of the GCC cement market by type shows an ideal combination of innovation for sustainability with performance-based needs. Blended cement is mostly used because of its cost-effectiveness and environmental compatibility, whereas Portland cement is increasing in use due to strength and fast construction. Othe specialized types of cements are used in niche applications such as oil wells and marine constructions. In December 2024, Al Jouf Cement launched green cement for NEOM projects, reducing emissions, enhancing durability, and supporting sustainable large-scale construction applications. In the GCC, manufacturers have started using their manufacturing process strategically depending upon the need for the project.

Market Breakup by End Use

Key Insight: The GCC cement market report reveals that infrastructure serves as the pillar for demand generation through extensive government investment. Stable residential development continues to be sustained as a result of urban residential needs and demographic factors. On the other hand, growth in commercial and industrial uses of cement is becoming increasingly rapid as a result of economic diversification and increased investments by the private sector. Different cement grades are required for different segments. For example, durability and volume are required in the case of infrastructure, cost effectiveness in the case of residential use, and accuracy and consistency in the case of commercial and industrial uses.

Market Breakup by Country

Key Insight: Segmentation based on different countries highlights that the leading consumer country is Saudi Arabia because of massive governmental projects and industrial activities. Rapid growth in the UAE takes place owing to diversification in real estate and exporting policies. Qatar continues to record a stable demand base, while Oman capitalizes on its geographical positioning for exporting clinkers. In June 2023, Qatar National Cement adopted SAP S/4HANA and Google Cloud, enhancing operational visibility, automation, scalability, and enabling data-driven decision-making for future-ready cement operations. Growth in Bahrain and Kuwait is primarily driven by ongoing urbanization and industrial expansion. Each country’s growth is driven by distinct factors, including government policies, regulatory frameworks, and varying levels of private sector participation, accelerating the overall GCC cement market penetration.

By type, blended cement accounts for the dominant share of the market due to sustainability compliance and cost optimization

Blended cement remains prevalent in the GCC cement market as manufacturers seek ways to substitute clinkers and maintain sustainable benchmarks while reducing production costs. Organizations such as Saudi Cement Company are including fly ash and slag products to develop an optimal mixture for extensive urban projects. The blended category features enhanced resistance against high temperatures and sulfate content, thus increasing its compatibility with GCC construction requirements. On the other hand, construction companies prefer this category owing to the enhanced workability associated with the product. In January 2024, Unique Cement launched Dhalai Special blended cement, offering faster strength development, 25% higher durability, and improved construction efficiency for structural applications.

On the other hand, Portland cement emerges as one of the fastest-growing segments due to its widespread usage in high-strength and fast-paced construction activities throughout the region. Construction firms working on transportation networks, commercial skyscrapers, and manufacturing facilities are using Portland cements to speed up their project delivery. Firms such as CEMEX S.A.B. de C.V. are developing specialized products of Portland cement for applications within harsh marine environments and heavy loads, boosting demand in the GCC cement market.

By end use, the infrastructure segment records notable growth in the market due to large-scale government-led construction programs

Infrastructural projects continue dominating the GCC cement market revenue due to the significant government investments in building roads, railways, and other construction activities. The implementation of mega projects such as NEOM and railway networks creates a continuous demand for advanced forms of cement that can withstand harsh environmental conditions, for instance, high salt content and temperature variations. Therefore, the companies are currently focusing on improving their products to provide greater durability and structural stability. In December 2025, KAUST launched Future Cement Initiative, accelerating low-carbon technologies, research collaborations, and innovation to transform Saudi Arabia’s sustainable cement industry.

The commercial and industrial sectors are experiencing the highest rate of growth in the GCC cement market due to economic diversification in the region. The fast-paced growth of logistics centers, manufacturing plants, and tourism facilities creates a demand for advanced cement solutions. There has been a recent trend of prefabricated buildings, which calls for advanced cement products with consistent properties. In addition, manufacturers are increasingly developing specialized cement variants to meet specific requirements, such as those needed for industrial flooring and large-span construction projects.

|

CAGR 2026-2035 - Market by |

Country |

|

Saudi Arabia |

5.1% |

|

UAE |

4.8% |

|

Qatar |

4.6% |

|

Oman |

XX% |

|

Bahrain |

XX% |

|

Kuwait |

XX% |

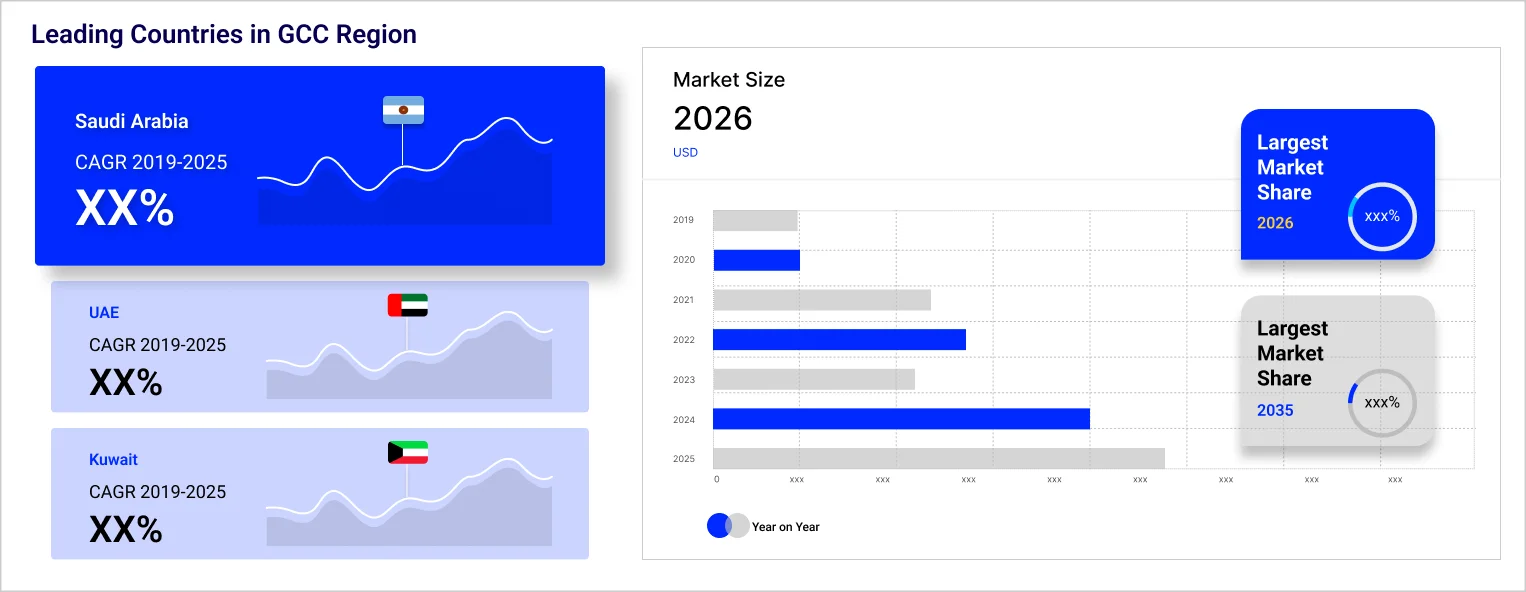

By country, Saudi Arabia accelerates the overall growth in the market due to giga projects and industrial expansion initiatives

Saudi Arabia emerges to be the largest producer of cement within the GCC region owing to its extensive pipeline of construction and infrastructure projects. There is an increasing demand for cement from the government owing to various Vision 2030 initiatives. Some companies producing cement in Saudi Arabia are increasing their production capacities to support the current project requirements. The construction and development of smart cities and transport networks in the Kingdom are contributing to the continuous demand in the GCC cement market.

The United Arab Emirates is becoming a fast-growing cement market in the GCC region owing to its vibrant real estate market and regional gateway positioning. The market observes a growing focus on sustainable construction which helps encourage the development of advanced cement solutions. The well-developed logistics ecosystem within the region supports continued cement demand. In October 2025, Asian Paints launched white cement facility in the UAE, diversifying portfolio, expanding global footprint, and targeting premium construction materials demand across Middle East markets.

Leading GCC cement market players are developing innovative sustainable technologies, optimizing efficiency, and forming strategic alliances. Companies are adopting technologies to produce low clinker cement, implementing waste heat recovery systems, and digitalizing their plants to cut costs and satisfy the ESG criteria. Exporting capacities have become a crucial aspect for firms, especially those operating in the UAE and Oman.

Furthermore, GCC cement players are now engaging in supply contracts for extended periods with the builders of massive infrastructure projects to guarantee regular demand for their products. Moreover, there is an increasing pressure on firms to introduce specialized cement grades to differentiate their offerings. The growth prospects include increasing the range of green cement types, improving logistics networks, and utilizing digital technology to enhance manufacturing processes.

Gulf Cement Company was formed in 1977 and is located in Ras Al Khaimah, United Arab Emirates. The company is committed to sustainable production methods and efficient operations. The company supplies cement products for construction projects and industries, while regularly improving its kiln technology and using alternative fuels in order to increase operational efficiency.

Sharjah Cement & Industrial Development Co. was established in 1977 and is based in Sharjah, United Arab Emirates. The company offers a diverse range of cement products tailored to meet the region’s specific construction needs and requirements. The company has invested in advanced manufacturing systems to increase production efficiency.

Since its foundation in 1906, CEMEX S.A.B. de C.V., based in Mexico, has operated internationally with a significant footprint in the GCC region. The firm concentrates on developing innovative cement products, integrating its digital logistics network, and providing sustainable construction materials to satisfy infrastructure and commercial demands.

Fujairah Cement Industries, founded in 1979, is based in Fujairah Emirate, United Arab Emirates. Fujairah Cement Industries focuses on producing high-quality cement for both regional consumption and export markets. Through its state-of-the-art manufacturing and logistics, the firm delivers construction materials to meet the demands of infrastructure and industry projects.

Other key players in the market include Lafarge Emirates Cement LLC, Union Cement Company (UCC), Pioneer Cement Industries, Ras Al Khaimah Cement Company LLC, and Najran Cement Company, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest trends shaping the GCC cement market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on GCC cement market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the GCC cement market reached an approximate volume of 101.90 MMT.

The market is projected to grow at a CAGR of 4.50% between 2026 and 2035.

The key players in the market include Gulf Cement Company, Sharjah Cement & Industrial Development Co., CEMEX S.A.B. de C.V., Fujairah Cement Industries, Lafarge Emirates Cement LLC, Union Cement Company (UCC), Pioneer Cement Industries, Ras Al Khaimah Cement Company LLC, and Najran Cement Company, among others.

Investing in low-carbon technologies, expanding export networks, forming long-term project partnerships, optimizing digital operations, and diversifying product portfolios are enabling stakeholders to strengthen competitiveness and capture emerging regional opportunities.

Volatile energy costs, tightening environmental regulations, clinker overcapacity, pricing pressures, and supply chain disruptions are challenging profitability, compelling companies to balance cost efficiency with sustainability investments and operational resilience.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.