Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

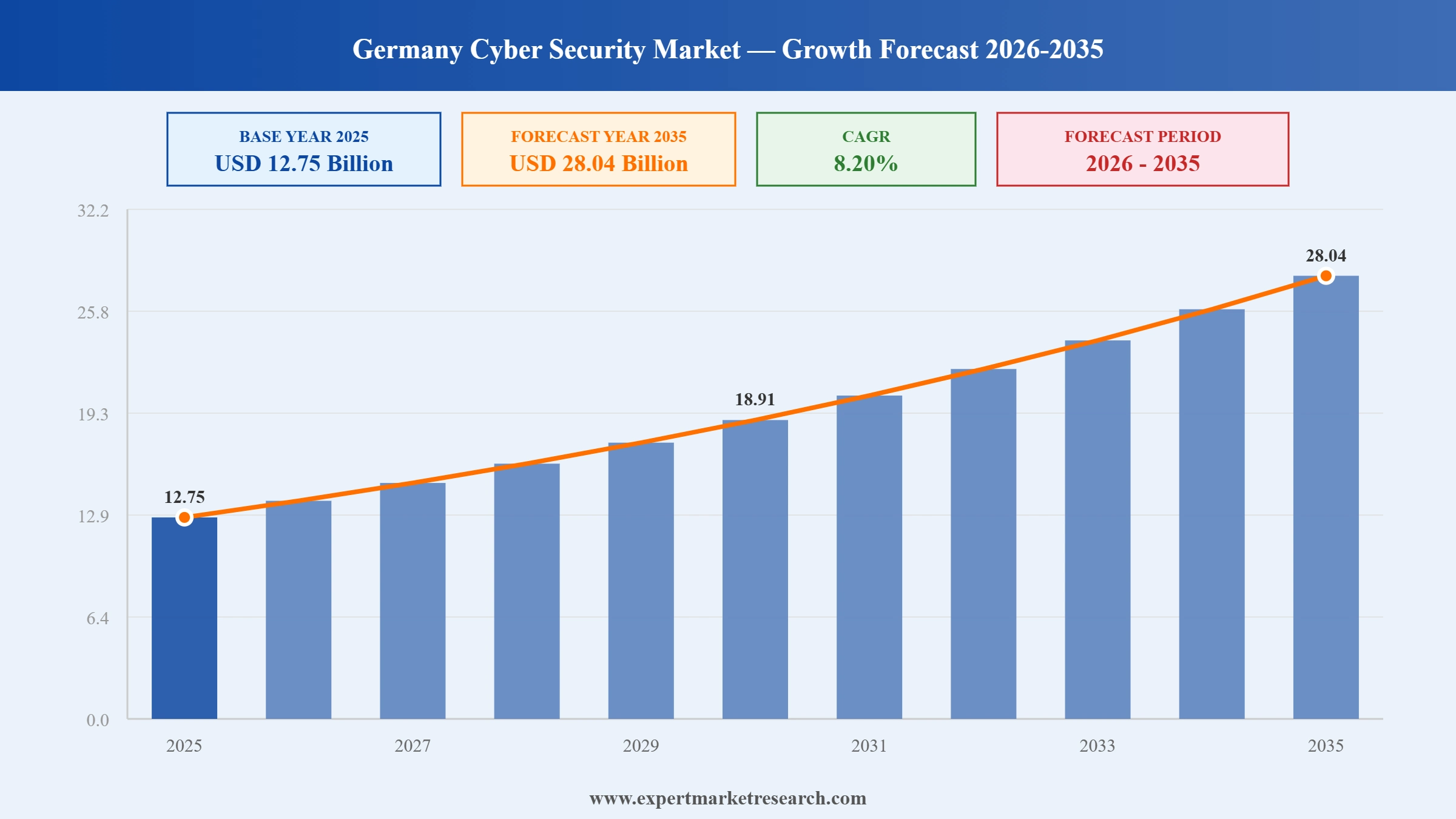

The Germany Cyber Security Market reached a value of USD 12.75 Billion at 2025 and is projected to expand at a CAGR of around 8.20% during the forecast period of 2026-2035. With rising cyber threats targeting critical infrastructure, expanding NIS2 and GDPR compliance requirements, surging cloud adoption across enterprise segments, and growing demand for AI-driven threat detection tools, the market is expected to reach USD 28.04 Billion by 2035.

Bavaria is expected to record a CAGR of 9.1% over the forecast period, underpinned by its concentration of technology companies, automotive OEMs, and defence contractors generating sustained demand for advanced cybersecurity solutions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Germany Cyber Security Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 12.75 |

| Market Size 2035 | USD Billion | 28.04 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 8.20% |

| CAGR 2026-2035 - Market by Region | North Rhine-Westphalia | 9.3% |

| CAGR 2026-2035 - Market by Region | Bavaria | 8.8% |

| CAGR 2026-2035 - Market by Offering | Services | 9.0% |

| CAGR 2026-2035 - Market by Industry Vertical | BFSI | 9.2% |

| 2025 Market Share by Region | Baden-Württemberg | 24.8% |

Germany's cyber security sector is being shaped by the convergence of tightening regulatory obligations, rapid AI integration, accelerating cloud migration, and a measurably worsening threat landscape. Each of these forces is translating into concrete procurement decisions and sustained investment across enterprise and public sector segments alike.

In February 2026, G DATA CyberDefense AG expanded its Security Awareness Training portfolio with four new modules covering AI-generated phishing images, voice phishing (vishing), CAPTCHA bypass attacks, and multi-factor authentication fatigue techniques. These additions reflect the growing sophistication of social engineering tactics targeting German businesses. The updated platform helps organisations build employee-level resilience against AI-assisted threats, a capability increasingly required by enterprises seeking to meet NIS2's provisions around human-layer security training across Germany's enterprise and public sector segments.

In December 2025, Deutsche Telekom made a strategic investment in Quantum Systems to accelerate Germany's transition towards lattice-based post-quantum encryption, ahead of approaching regulatory deadlines set by the German Federal Office for Information Security. The move reflects growing urgency within Germany's telecommunications and enterprise sectors to future-proof data protection frameworks against quantum-computing-enabled decryption threats. It positions Deutsche Telekom at the forefront of post-quantum cryptography adoption in Europe, aligning with BSI recommendations for quantum-safe security architectures across critical infrastructure sectors.

In November 2025, Munich-based Rohde and Schwarz entered a strategic partnership with Broadcom to validate its CMP180 radio communication tester for compatibility with Wi-Fi 8 chipsets. The collaboration is designed to accelerate time-to-market for next-generation wireless devices while ensuring end-to-end device security testing meets emerging standards. As Germany advances its 5G and next-generation wireless infrastructure rollout, this partnership strengthens Rohde and Schwarz's positioning at the intersection of wireless communications and cybersecurity testing for industrial and enterprise applications.

In May 2025, Unosecur, a Germany-based identity security specialist, introduced a native GitHub integration to its Cloud Infrastructure Entitlement Management platform. The agentless solution provides continuous visibility into developer access rights, enforces least-privilege access in real time, and identifies access sprawl and privilege risks without disrupting development workflows. This launch extended Unosecur's unified cloud-to-code security monitoring capability, directly targeting German enterprises facing heightened exposure to software supply chain attacks under increasingly stringent NIS2 obligations.

In March 2024, Airbus Defence and Space completed its acquisition of Infodas, a Cologne-based cybersecurity firm employing approximately 250 professionals and generating annual revenues of around EUR 50 million. With nearly five decades of experience delivering data diode and cross-domain security solutions to the German military and NATO, Infodas brought significant defence cybersecurity expertise to Airbus. The acquisition underscored Airbus's strategic intent to position cybersecurity as a core growth pillar as rising network connectivity in defence environments continues to expand the attack surface across mission-critical systems.

The EU NIS2 Directive, transposed into German law, dramatically expanded the scope of mandatory cybersecurity compliance, bringing an estimated 30,000 German entities under binding security obligations by 2025, up from approximately 2,000 previously. This shift compels organisations across critical infrastructure, manufacturing, healthcare, and financial services to deploy continuous monitoring, automated incident response, and third-party risk management platforms. In March 2024, the German Federal Parliament advanced NIS2 transposition legislation, reinforcing procurement urgency and driving substantial near-term investment in compliance technology and managed security services throughout the country.

Germany's Federal Office for Information Security published its State of Cybersecurity 2024 report in November 2024, revealing that malware variant counts had reached an average of 309,000 new variants per day, a 26% increase compared to 2022 levels. The findings prompted enterprises and government agencies to accelerate investment in AI-powered detection tools and real-time threat intelligence platforms. Germany Cyber Security Market growth is being directly fuelled by this intensifying threat environment, as perimeter-only defences are no longer sufficient to protect expanding and increasingly distributed digital asset bases.

In May 2024, Amazon Web Services announced a EUR 7.8 billion investment plan for cloud infrastructure development in Germany through 2040, targeting enterprise and public sector clients. This commitment accelerated cloud migration across industries and strengthened demand for cloud-native security solutions, particularly around data residency compliance, encryption, and identity management. German organisations facing data sovereignty obligations under GDPR and Schrems II rulings are prioritising sovereign cloud architectures backed by vetted security frameworks, making cloud security one of the fastest-growing segments in the German market.

Germany's enterprise and public sector organisations are rapidly integrating artificial intelligence and machine learning into cybersecurity operations, driven by the volume and complexity of modern attack vectors. In November 2023, the German Federal Office for Information Security confirmed that ransomware attacks remain exceptionally high risk for small and medium enterprises, triggering widespread deployment of AI-powered endpoint and network monitoring solutions. German cybersecurity vendors are embedding predictive analytics and behavioural analysis into their platforms to enable proactive threat identification rather than reactive incident response, significantly improving detection speed across enterprise environments.

"Germany Cyber Security Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

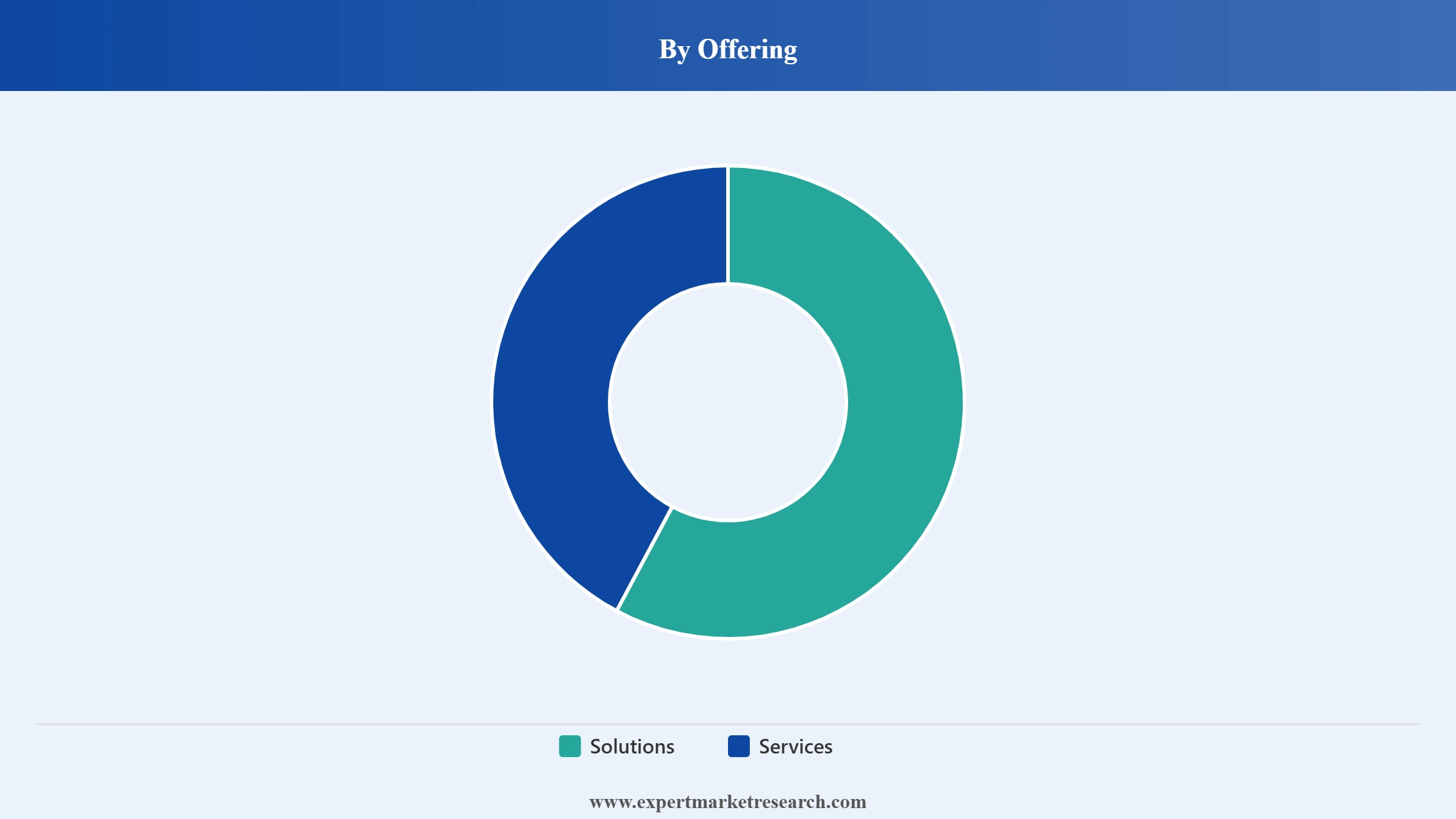

Market Breakup by Offering

Key Insight: The Solutions segment dominates the Germany cyber security market, accounting for approximately 66% of total market revenues in 2025. This reflects entrenched adoption of firewalls, identity management tools, and intrusion prevention systems across enterprise and critical infrastructure clients. Identity and Access Management is among the most prioritised sub-segments, with BaFin-regulated financial institutions mandated to enforce zero-trust network segmentation. The Services segment, while smaller in absolute share, is growing fastest at an estimated CAGR of 12.4%, driven by managed security service providers such as T-Systems and Atos Eviden offering bundled SOC monitoring and compliance advisory to organisations that lack sufficient in-house expertise for sustained round-the-clock security operations.

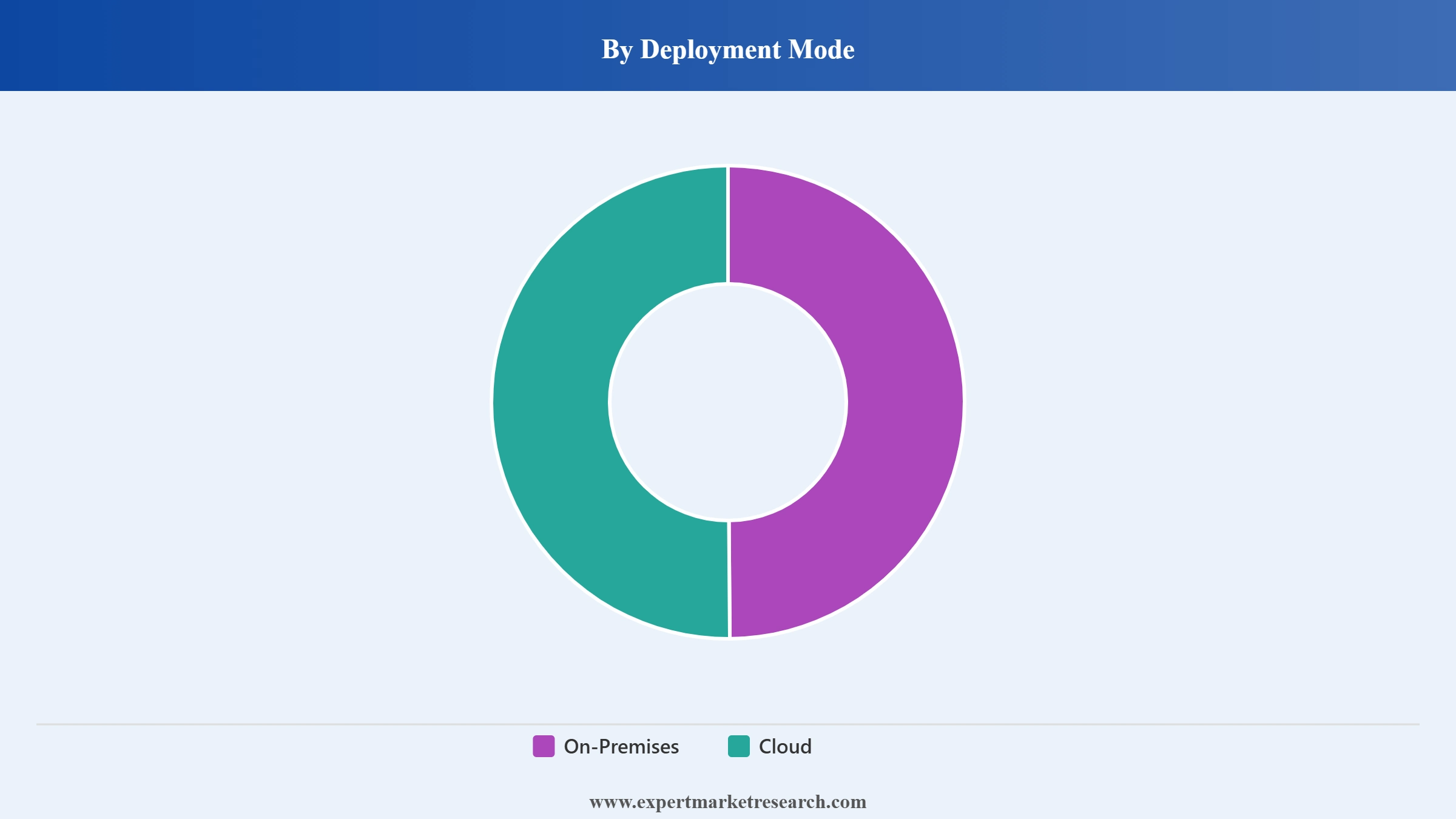

Market Breakup by Deployment Mode

Key Insight: On-Premises deployments hold the majority share of the Germany cyber security market at approximately 52.8% in 2025. The KRITIS regulatory framework requires critical infrastructure operators and defence contractors to maintain air-gapped environments for classified and sensitive workloads, reinforcing on-premises procurement preferences. Cloud deployment is gaining momentum rapidly at an estimated CAGR of 12.8%, as sovereign cloud platforms from Deutsche Telekom and IONOS increasingly satisfy German data residency requirements without exposing clients to US Cloud Act jurisdiction risk. Hybrid architectures combining plant-floor OT systems with cloud-based analytics are also gaining traction in automotive and industrial manufacturing environments.

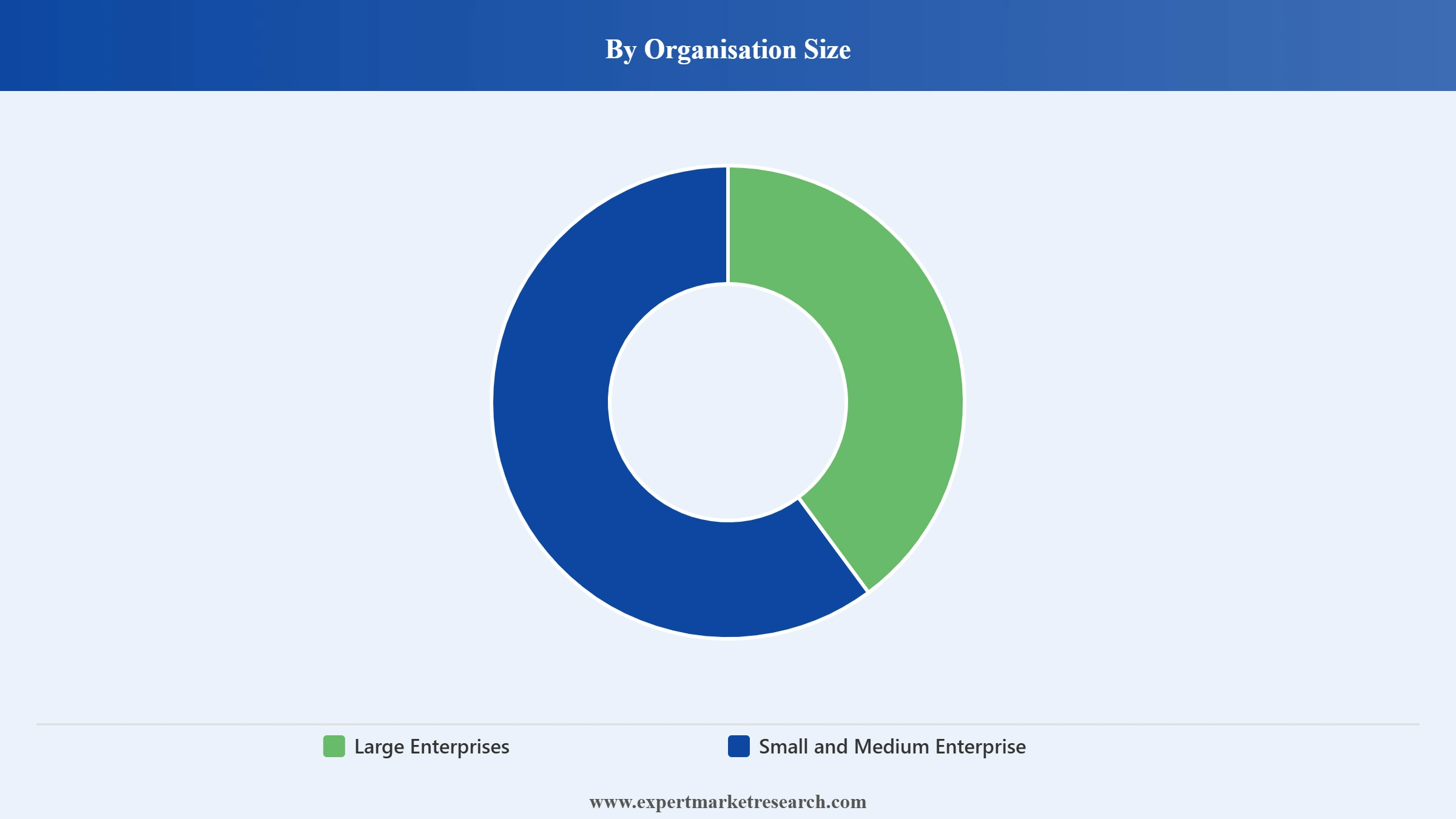

Market Breakup by Organisation Size

Key Insight: Large Enterprises hold approximately 71.3% of Germany's cyber security market share in 2025, driven by their complex multi-site operations, global regulatory exposure, and the scale of their managed detection, response, and compliance requirements. SMEs, however, are the faster-growing segment at an estimated CAGR of 12.6%. Cyber insurers have begun requiring baseline controls including multi-factor authentication and endpoint detection as underwriting preconditions, effectively converting optional tools into commercial necessities. Managed service providers have responded with turnkey monthly subscription bundles priced between EUR 500 and EUR 2,000, making enterprise-grade protection accessible to Mittelstand firms without dedicated security teams.

Market Breakup by Security

Key Insight: Network Security holds the largest segment share at approximately 36.2% of the Germany cyber security market in 2025. Its dominance reflects the foundational role network protection plays across BFSI, manufacturing, and government verticals as the first line of defence against ransomware and intrusion. Cloud Security and Identity Management are the fastest-growing solution families, each recording CAGRs above 13% as cloud migration accelerates and access control requirements tighten under NIS2. End Point and IOT Security is gaining significant traction as the proliferation of connected devices across Germany's Industrie 4.0 manufacturing environments expands the potential attack surface substantially.

Market Breakup by Industry Vertical

Key Insight: BFSI captured approximately 24.6% of Germany's cyber security market in 2025, propelled by MaRisk compliance requirements and DORA's four-hour incident reporting mandate, which has compelled banks to automate response playbooks and invest in continuous monitoring tools. Healthcare and Life Sciences is the fastest-growing vertical at approximately 13% CAGR, supported by the Hospital Future Act's EUR 4.3 billion in funding tied directly to encryption, role-based access control, and audit logging implementations. A ransomware incident that disrupted a Berlin hospital in 2024 further elevated cybersecurity as a patient safety and board-level governance priority across the sector.

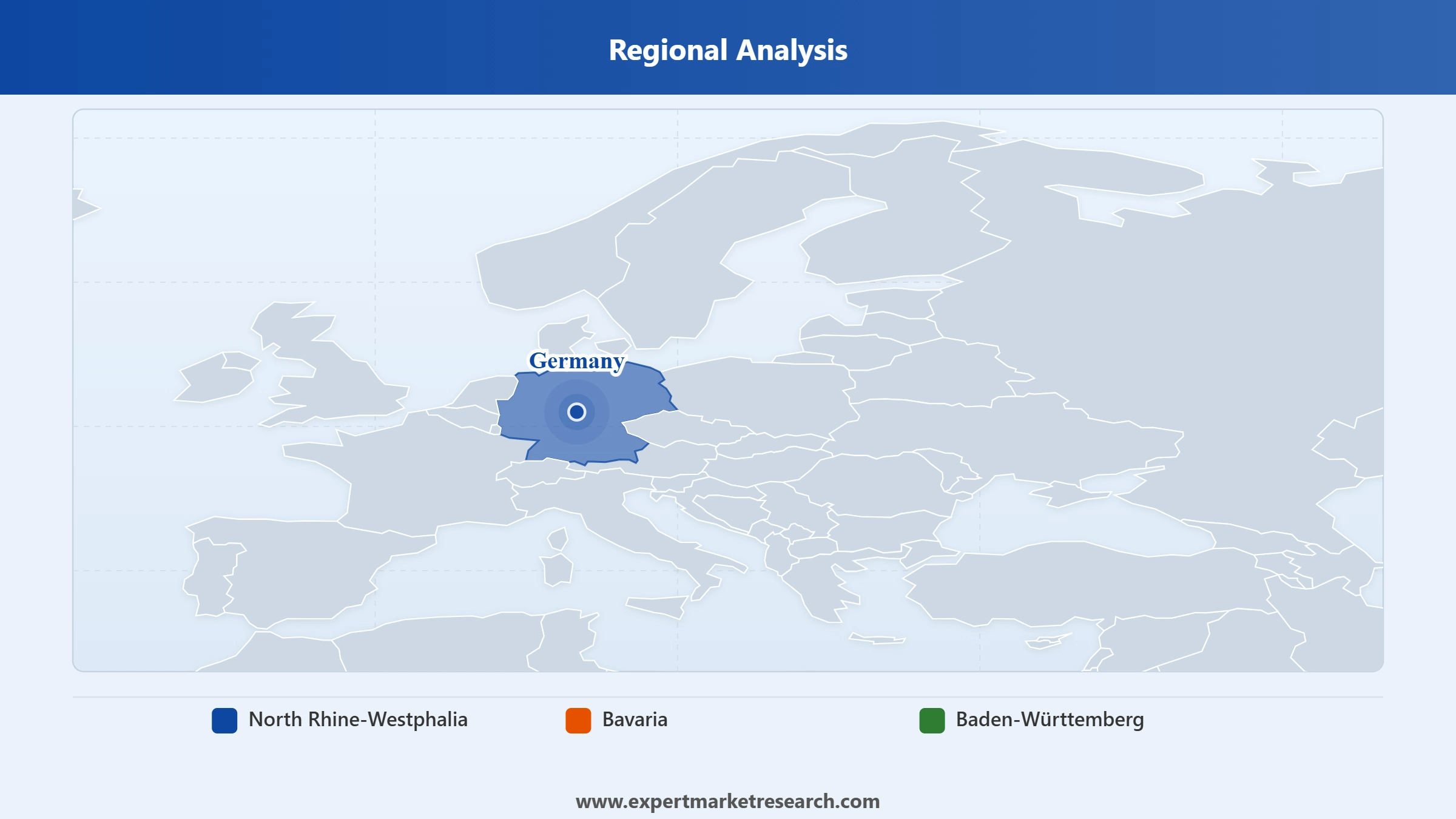

Market Breakup by Region

Key Insight: North Rhine-Westphalia leads Germany's cyber security market by revenue, anchored by its concentration of financial institutions, telecommunications companies, and large industrial manufacturers in Cologne and Dusseldorf. Bavaria is the fastest-growing regional market, driven by Munich's status as a hub for technology firms, automotive OEMs, and defence contractors. Strong demand from high-value asset-rich organisations in Bavaria is generating sustained requirements for advanced threat detection and OT security solutions. Baden-Wurttemberg, home to a dense base of precision engineering and automotive supply chain firms, is registering robust demand growth as Industrie 4.0 adoption broadens the OT and IoT security market within the state.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Solutions segment under the Offering dimension holds the dominant share of Germany's cyber security market, accounting for approximately 66% of total revenues in 2025. This supremacy reflects the foundational role solutions such as firewalls, identity management platforms, and encryption tools play in meeting statutory compliance obligations across large enterprises and critical infrastructure operators. Identity and Access Management and Antivirus/Antimalware are among the most widely deployed categories. German companies allocate an average of approximately 11% of IT budgets to security measures, with IAM increasingly treated as a baseline control requirement under BaFin and NIS2 frameworks. The Services segment, while smaller in share, is growing fastest as compliance outsourcing accelerates in response to four-hour NIS2 incident reporting obligations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

On-Premises deployment commands the majority of the German cyber security market at approximately 52.8% in 2025, driven by KRITIS-regulated operators, defence establishments, and financial entities requiring physical data sovereignty over classified and sensitive workloads. BSI IT-Grundschutz certification standards and GDPR data residency rules have historically reinforced on-premises procurement preferences in Germany. The Cloud segment is growing at an estimated CAGR of 12.8%. Sovereign cloud platforms from Deutsche Telekom and IONOS, which comply with German data residency obligations and reduce legal exposure from US Cloud Act provisions, are increasingly accepted alternatives for enterprises pursuing hybrid security architectures.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Large Enterprises account for approximately 71.3% of the Germany cyber security market in 2025. Their complex multi-site operations, stringent regulatory obligations, and global asset exposure require comprehensive security stacks covering managed detection, third-party risk management, and compliance auditing. SMEs represent the faster-growing segment, growing at an estimated CAGR of 12.6%, as insurers enforce baseline security controls as underwriting requirements and managed service providers deliver affordable subscription bundles that eliminate the need for full-time in-house security personnel across Germany's Mittelstand business community.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North Rhine-Westphalia holds the largest regional share of Germany's cyber security market and remains a primary growth engine for the sector. The state's concentration of financial services firms in Dusseldorf, telecommunications operators, and large industrial manufacturers generates sustained demand for network security, SIEM platforms, and managed security services. BaFin-regulated entities operating across Cologne and Dusseldorf drive compliance-linked investments in access management and incident response capabilities. Major global cybersecurity providers including IBM and Cisco maintain regional delivery teams in the state, supporting enterprise clients with round-the-clock monitoring and threat intelligence. The ongoing digitalisation of the Ruhr industrial corridor is also broadening OT and IoT security requirements within the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Bavaria is emerging as Germany's fastest-growing regional cyber security market, driven by the concentration of technology companies, automotive manufacturers, and aerospace and defence contractors headquartered in and around Munich. The state's high density of digitally advanced, asset-rich organisations makes it a primary target for advanced persistent threats and supply chain attacks. Munich's technology ecosystem has attracted meaningful investment in AI-powered security startups and specialist cybersecurity service providers. Major enterprises including BMW, Airbus, and Siemens have significantly expanded their internal security operations and vendor partnerships in response to rising OT security risks. Bavaria's Digital Strategy, which emphasises cloud infrastructure and smart manufacturing, further accelerates regional demand for cloud-native and endpoint security solutions.

Germany's cyber security market operates within a moderately fragmented competitive landscape, where global technology giants coexist with specialised regional and national vendors. The market's competitive intensity has risen sharply in response to NIS2 and DORA compliance timelines, prompting organisations to seek vendors with demonstrated regulatory expertise and local delivery capabilities. Large multinationals such as IBM, Cisco, Fortinet, and Palo Alto Networks compete on the strength of their broad solution portfolios and global threat intelligence networks, while regional specialists including Secunet Security Networks, G DATA CyberDefense, and Rohde and Schwarz hold competitive advantages through BSI-certified products and long-standing relationships with German government and defence clients.

Competitive differentiation increasingly centres on managed services breadth, AI-driven threat detection capability, and the ability to offer sovereign cloud-compatible security architectures. Vendors capable of demonstrating alignment with German regulatory frameworks while providing scalable, cost-effective solutions for Mittelstand SMEs are gaining meaningful market share in a segment growing at more than double the pace of the large enterprise segment, reshaping how cybersecurity is sold and delivered across Germany.

Founded in 1911 and headquartered in Armonk, New York, IBM Corporation is a global technology and consulting leader. IBM Security's QRadar SIEM platform and X-Force threat intelligence network anchor its presence in Germany's enterprise and government segments. IBM delivers identity management, endpoint protection, cloud security, and managed security operations to major clients across BFSI, manufacturing, and public sector verticals in Germany, supported by local delivery teams and strategic partnerships.

Founded in 2000 and headquartered in Sunnyvale, California, Fortinet is a global network security leader. Its Security Fabric architecture integrates firewall, endpoint, cloud security, and OT protection within a unified management framework. Fortinet's FortiGate next-generation firewalls and strong channel partner network make it a preferred solution provider for German enterprises navigating NIS2 compliance across manufacturing, energy, and critical infrastructure environments.

Founded in 1984 and headquartered in San Jose, California, Cisco Systems is a leading global networking and security provider. Its portfolio spans Secure Firewall, Duo multi-factor authentication, Umbrella DNS security, and Extended Detection and Response capabilities. In Germany, Cisco holds strong positions across telecommunications, BFSI, and government sectors, delivering scalable, integrated security architectures aligned with BSI standards and EU regulatory requirements.

Founded in 2005 and headquartered in Santa Clara, California, Palo Alto Networks is a leading AI-driven cybersecurity provider. Its Cortex platform, Prisma Cloud suite, and next-generation firewalls are widely adopted across Germany's enterprise market. In October 2025, the company announced a strategic cloud security partnership with a major German telecommunications provider, strengthening its managed detection and response footprint across the region.

Other key players in the market are Intel Corp., Oracle Corp., Fujitsu Ltd., Dell Inc., Trend Micro Inc., F5 Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a clear competitive advantage in the Germany Cyber Security Market 2026 with our comprehensive market intelligence report. Access the latest analysis on solution innovations, regional demand dynamics, enterprise spending patterns, and the regulatory shifts redefining cybersecurity across the country. Whether you are evaluating market entry, expanding your security portfolio, or benchmarking competitors, our research gives you the clarity to move with conviction. Download your complimentary sample today and uncover the growth opportunities shaping Germany's cybersecurity landscape through 2035.

Asia Pacific Cyber Security Market

Automotive Cyber Security Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 12.75 Billion.

The market is assessed to grow at a CAGR of 8.20% between 2026 and 2035.

The market is estimated to reach around USD 28.04 Billion by 2035.

The market is being driven by increasing cyber threat cases and swift digital transformation in the economy.

The key trends aiding the market expansion include the growing adoption of automation, swift financial inclusion, and strict data protection regulations.

The different types of enterprise sizes in the market are large enterprises and small and medium enterprise (SMEs).

The major regions considered in the market are North Rhine-Westphalia, Bavaria, and Baden-Württemberg.

The major players in the market are IBM Corporation, Cisco Systems Inc., Intel Corp., Dell Inc., Fortinet Inc., Trend Micro Inc., Oracle Corporation, Fujitsu Ltd., Palo Alto Networks Inc., and F5 Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment

|

| Breakup by Offering |

|

| Breakup by Deployment Mode |

|

| Breakup by Organisation Size |

|

| Breakup by Security |

|

| Breakup by Industry Vertical |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.