Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

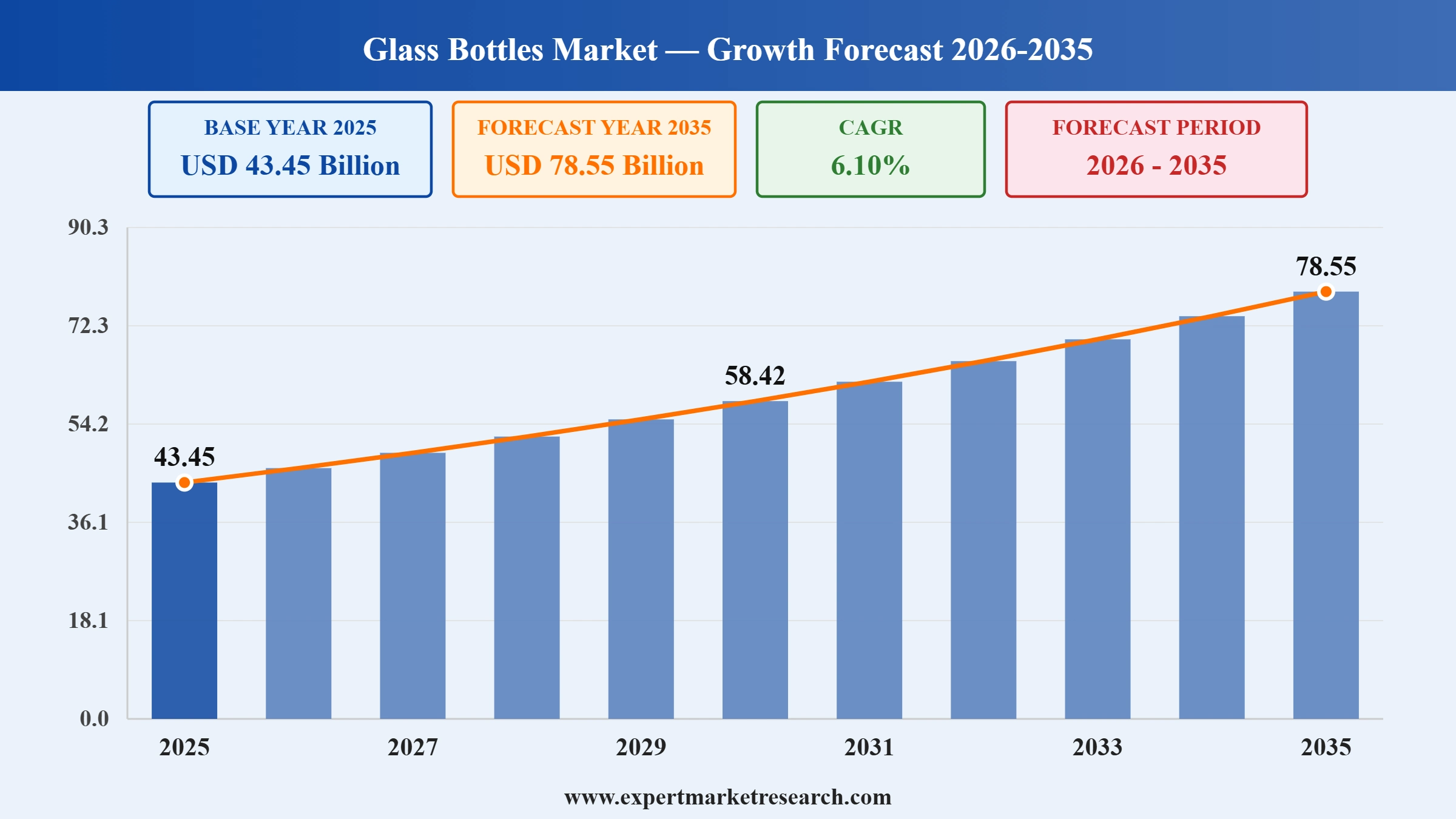

The global glass bottles market attained a value of approximately USD 43.45 Billion in 2025 The market is further expected to grow at a CAGR of 6.10% during the forecast period 2026-2035, to reach nearly USD 78.55 Billion by 2035. The glass bottles and containers market spans a wide range of packaging formats, including glass bottles, glass jars, glass vials, and ampoules, serving the beverage, food, pharmaceutical, cosmetics & personal care, and chemical industries. Key glass types include Type I borosilicate glass, Type II treated soda lime glass, and Type III regular soda lime glass, each suited to specific end-use performance requirements.

Owens-Illinois announced in April a major investment in modernizing U.S. glass bottle manufacturing operations, including new electric and hybrid furnaces aimed at reducing emissions. The upgrades support beverage customers including Anheuser-Busch and Constellation Brands seeking lower carbon packaging. The capital program also reflects rising preference for premium glass containers across spirits and craft beer segments, The Wall Street Journal reported.

The European Union finalized stricter recycled content rules for glass beverage bottles in March, requiring higher post consumer cullet thresholds across member states. The regulation aims to support circular economy goals and reduce furnace energy consumption. Manufacturers including Verallia and Vidrala are expanding cullet sourcing partnerships and investing in upgraded sorting infrastructure to meet the new requirements, The Guardian reported.

Heightened regulatory pressure on single-use plastics, premiumization in the beauty and spirits sectors, and pharmaceutical fill-finish expansion are steering steady market gains. Government mandates such as California's SB 54 plastic-reduction law and France's polystyrene ban have accelerated the shift toward 100% recyclable glass packaging, reinforcing its competitive position against PET, aluminum, and other substrates. The growing adoption of returnable glass bottles and circular economy packaging models further supports long-term glass bottle market growth. In 2025, global glass container production volumes exceed 50 million tonnes annually, with soda lime glass accounting for approximately 90% of all glass container production.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Glass bottles are rigid, hollow containers manufactured primarily from silica sand, soda ash, limestone, and recycled glass (cullet), formed through high-temperature melting and precision molding processes. They are designed to store, preserve, and transport liquid and semi-liquid products across a broad range of industries, offering chemical inertness, impermeability, and infinite recyclability that no other packaging substrate can fully replicate.

For the purpose of this report, the glass bottles market encompasses all glass-based rigid containers including bottles, jars, vials, and ampoules used in commercial packaging applications. The market excludes flat glass, fiberglass, and specialty technical glass used in construction, electronics, or optical applications. Glass containers are produced from two primary material categories: borosilicate glass (Type I), prized for pharmaceutical and laboratory use due to its superior chemical resistance; and soda lime glass (Types II, III, and IV), which accounts for approximately 90% of all glass container production by volume and serves beverages, food, cosmetics, and general packaging.

Glass bottles are certified by the U.S. Food and Drug Administration (FDA) as "Generally Recognized as Safe" (GRAS) the only packaging material to hold this designation. This distinction, combined with glass's non-porous surface that preserves flavor, aroma, and product integrity without chemical interaction, makes it the preferred substrate for premium, pharmaceutical, and food-grade packaging globally.

Snapple announced the relaunch of its iconic glass bottle in New York City as part of their Snapsolutely Refreshing marketing campaign. The brand, through this short-time launch, is celebrating its heritage of Brooklyn and making it possible for the fans to have the original glass experience again with the unique “pop” when it is opened.

Saverglass, a member of the Orora Group, broadened its spirits portfolio with the addition of the GOLDEN RESERVE glass bottle collection, which features MALTY, BARLEY, and CASK bottles. The bottles are designed for use with premium spirits and rtd cocktails, and they provide the brands in North America with the possibility of customizing, sustaining, and 100% recycling their products.

Icelandic Glacial™ debuted their luxurious 750 ml capacity glass bottles of still and sparkling water on Gopuff in the glass bottles market across 30 cities in the United States. By this arrangement, customers get the opportunity to purchase water that is sourced in an environmentally friendly manner and is alkaline spring water and is at their service in a very short time without them doing it themselves. The 100% recyclable glass containers are in line with the brand’s promise of luxury, purity, and environmental stewardship.

SGD Pharma launched NOVA, a lightweight glass bottle innovation for cosmetic and beauty brands, at Cosmoprof Asia in Hong Kong. The new 200ml NOVA bottle can reduce CO₂ emissions by around 20% compared to the standard models, though it retains the same premium look and mechanical strength. This move is a gesture of SGD Pharma’s pledge to eco-friendly packaging and its larger plan for decarbonization.

Brands are highly focused on low-carbon glass packaging and the imposition of sustainability requirements on their suppliers, which is propelling the growth of the glass bottles market. Consequently, top producers are speeding up decarbonization roadmaps by operating furnaces in a cleaner way and reporting fewer emissions. In January 2025, O-I gave an account of the emissions-reduction program and the scalable furnace innovation done in the company, thereby pointing out that the increasing emphasis on sustainability as a driver for CAPEX rather than just a marketing claim. As consumers increasingly value third-party-verified sustainability, low-carbon glass capacity is gaining stronger preference and higher demand.

The beverage and cosmetics sectors are reaping the benefits of timely and well-targeted CAPEX on resource-efficient plants with a design for higher cullet usage, energy consumption reduction, and automated production. The achieved efficiencies thus make operating costs lower while output stability is higher, these two things are very important to beverage and cosmetics brands. In 2023, Vetropack put into operation its highly automated and resource-efficient plant in Boffalora, turning it into the company's sustainable glass production and performance improvement flagship. Advanced facilities like this increase premium-grade capacity and secure a good long-term outlook for glass bottles market.

Manufacturers are reducing the carbon content of their raw materials a lot and working with new innovative formulations that permit lower melting temperatures and higher recycled-glass compatibility. These improvements limit the average emissions per unit while also making the company more resistant to feedstock price fluctuations. In 2023, Verallia certified a low-carbon calcium source for implementation across its production network, thus marking an important turning point in the process of reducing the carbon footprint of glass. As the large companies implement these formulations, the brands will have eco-friendly packaging without losing the freedom of design or durability.

The establishment of closed-loop distribution and refill systems is leading to an increasing popularity of durable and returnable formats in the glass bottles market, which are compatible with such systems. The beverage companies are focusing their attention on those networks that not only lower packaging waste but also keep the premium brand presentation intact. For instance, in May 2024, Pernod Ricard entered a global licensing accord with ecoSPIRITS, aiming to expand the circular distribution for spirits, Thus, large-scale reuse of glass bottles is possible in numerous markets. Such partnerships facilitate the standardization of multi-cycle glass use and create a long-term increase in order volumes for refill-orientated bottling programs.

Lightweighting has been turned into a trend of strategic advantage, with which brands can reduce transport emissions and material usage while still maintaining the luxury of the product. Such a move is in harmony with both sustainability messaging and cost optimization. Exemplifying this trend, in September 2024, Johnnie Walker presented its lightest 70 cl whisky glass bottle, thereby accomplishing material reduction while at the same time not losing the product’s premium appeal. As more brands start to use lightweight premium bottles, the consumption of glass is expected to remain consistent in alcoholic and high-end beverage categories.

The glass bottles market demonstrates a well-established demand structure, with growth primarily driven by sector-wise consumption patterns and evolving packaging preferences. Instead of uniform expansion, the market shows strong concentration in specific high-demand segments, particularly within beverages and pharmaceuticals, where product integrity and premium packaging play a crucial role.

The beverage industry continues to account for the largest share of global demand, supported by increasing consumption of alcoholic drinks such as beer, wine, and spirits, alongside the steady rise in premium non-alcoholic beverages. Glass bottles remain a preferred choice in this segment due to their ability to preserve flavor, carbonation, and product quality without chemical interaction.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

From a regional perspective, mature markets such as North America and Europe maintain a stable share due to stringent sustainability regulations and well-developed recycling infrastructure. Meanwhile, Asia-Pacific is witnessing accelerated demand momentum, fueled by urbanization, rising disposable incomes, and expanding food and beverage industries. This shift indicates a gradual rebalancing of market share toward emerging economies.

In terms of product segmentation, flint (clear) glass holds a dominant position owing to its versatility and strong visual appeal, especially in premium packaging applications. Additionally, the increasing preference for recyclable and reusable packaging formats is influencing purchasing decisions, further strengthening the role of glass bottles in circular economy models.

The glass bottles market is undergoing significant transformation driven by sustainability mandates, premiumization trends, and technological advancements in lightweight glass manufacturing. Below are the key growth drivers shaping the market through 2035.

| Driver | CAGR Impact | Geographic Relevance | Timeline |

|---|---|---|---|

| Plastic bans driving shift to recyclable glass | +0.8% | California, France, EU | Medium term (2–4 yrs) |

| Premiumization in beauty & spirits ("glassification") | +0.6% | North America & Europe | Long term (4+ yrs) |

| Pharmaceutical fill-finish expansion & biologics demand | +0.5% | APAC, Global | Long term (4+ yrs) |

| Craft alcohol boom & custom container demand | +0.4% | North America & Europe | Medium term (2–4 yrs) |

| Smart packaging integration (NFC, QR codes in glass) | +0.3% | Global, led by Europe | Long term (4+ yrs) |

Plastic Bans & Sustainability Regulations

Global sustainability initiatives are accelerating the adoption of recyclable packaging materials, directly strengthening demand for glass containers. California's SB 54 mandates a 65% reduction in single-use plastic packaging by 2032, while France has banned expanded polystyrene food containers as of January 2025. The European Union's pending bisphenol-A restrictions further reinforce conversion in food-contact segments. Unlike plastic, glass can be recycled indefinitely without quality degradation, making it the preferred solution for brands targeting circular economy compliance.

Premiumization in Beauty & Spirits

The growing consumer preference for artisanal beverages and luxury cosmetics has significantly lifted demand for custom glass bottle designs. Premium spirits brands invest heavily in distinctive bottle silhouettes, embossed logos, and specialty closures to reinforce brand identity at the point of sale. In the beauty sector, the "glassification" trend shifting from plastic to glass for skincare and fragrance packaging is particularly pronounced in North America and Europe, where sustainability and perceived premium quality drive purchasing decisions.

Pharmaceutical & Biologics Packaging Demand

The pharmaceuticals segment is experiencing robust growth at a projected CAGR of over 4.6%, driven by rising demand for safe, non-reactive packaging solutions for liquid medications, vaccines, and injectable biologics. Glass vials and ampoules remain the gold standard for pharmaceutical packaging due to their superior chemical inertness and contamination resistance. The increasing production of biologics and mRNA-based therapeutics accelerated post-pandemic further boosts demand for borosilicate glass vials in particular.

Lightweighting & Technological Advancements

Manufacturers are investing heavily in lightweighting technologies that reduce the amount of glass per unit while maintaining structural integrity and durability. In October 2024, Ardagh Glass Packaging-Europe launched a new lightweight range of 750ml wine bottles reduced from 410g to 360g, incorporating up to 80% recycled glass cullet achieving a 12% reduction in carbon emissions per bottle. Similar initiatives across the industry are improving cost competitiveness versus plastic alternatives while supporting sustainability targets.

The glass bottles industry is poised for consistent and long-term growth, driven by a combination of regulatory, environmental, and consumer-led factors. The projected 6.10% CAGR from 2026 to 2035 reflects the increasing global shift away from plastic packaging toward recyclable and eco-friendly alternatives such as glass. Government regulations, including plastic bans and recycling mandates, are playing a crucial role in accelerating this transition.

Moreover, growth is strongly supported by expanding demand in premium segments such as spirits, cosmetics, and pharmaceuticals, where glass packaging enhances product integrity and brand positioning. The increasing adoption of returnable glass systems and circular economy models is further strengthening market expansion. Technological advancements, particularly in lightweight glass production and higher recycled content (cullet usage), are improving cost efficiency and sustainability, enabling manufacturers to scale operations while meeting evolving environmental standards.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Despite favorable long-term growth dynamics, the glass bottles market faces several structural challenges that participants must navigate.

Energy-Intensive Glass Manufacturing & Cost Volatility

Glass container manufacturing requires glass furnace temperatures exceeding 1,500°C, making it one of the most energy-intensive packaging substrates. Energy costs represent approximately 15–25% of total glass manufacturing costs, making the sector highly sensitive to fuel price volatility. The annealing process where glass is slowly cooled to relieve internal stress also consumes significant energy. Extended periods of elevated energy prices, as experienced across Europe in 2022–2023, compress margins and may force producers to idle furnace capacity. Hybrid furnaces and oxy-fuel combustion technology are emerging as solutions that reduce energy intensity and NOx emissions, though they require substantial capital investment.

Weight & Transportation Costs

Despite lightweighting progress, glass remains significantly heavier than alternative packaging materials such as PET or aluminum cans. Higher transport costs increase the total cost of ownership for brand owners and distributors, particularly for long-distance shipping. This weight disadvantage limits glass adoption in categories where packaging cost per unit is highly sensitive.

Limited Cullet Availability & Recycled Glass Supply Chain Gaps

While glass is 100% recyclable, the availability of high-quality cullet (recycled glass) remains inconsistent across markets. Inadequate recycling infrastructure, color-sorting inefficiencies particularly separating flint glass, amber glass, and green glass streams and contamination reduce cullet quality and availability. Soda lime glass production relies heavily on cullet to lower melting points and reduce raw material costs (silica sand, soda ash, limestone). This supply variability limits manufacturers' ability to maximally substitute virgin raw materials, constraining both cost savings and sustainability benefits. The EU mandates at least 70% recycled content in glass packaging, making cullet supply a strategic priority for European producers.

Beyond near-term growth drivers, several structural opportunities are reshaping competitive dynamics in the glass bottles market and creating value for manufacturers, brands, and investors through 2035.

Customized & Premium Glass Packaging

Brand differentiation is emerging as one of the most powerful growth levers in the glass bottles industry. Beverage and cosmetics companies are seeking distinctive bottle shapes, color treatments, embossing, screen printing, and specialty closures to stand apart on increasingly crowded retail shelves. Limited-edition bottle designs and bespoke molds are particularly attractive to craft spirits producers and luxury beauty brands, where packaging cost is a small fraction of retail price making the economics of premium glass highly favorable. Manufacturers offering integrated design, prototyping, and short-run production capabilities are well-positioned to capture this high-margin opportunity.

Pharmaceutical Glass Packaging Expansion

The pharmaceutical industry represents the fastest-growing application segment for glass containers, with demand driven by an accelerating pipeline of biologics, GLP-1 therapies, mRNA vaccines, and injectable drugs all of which require chemically inert, contamination-resistant packaging. Glass vials and ampoules remain the regulatory gold standard for injectable pharmaceutical packaging globally. Manufacturers capable of producing high-purity borosilicate glass containers in ISO-certified cleanroom environments, meeting strict FDA and EMA specifications, are positioned to secure long-term supply agreements with pharmaceutical companies and contract manufacturing organizations (CMOs). This segment's high margins and specification-driven demand insulate producers from commodity pricing cycles.

Returnable & Refillable Glass Bottle Systems

Circular economy mandates and voluntary brand sustainability commitments are accelerating the adoption of returnable glass bottle systems across beverages. Coca-Cola has committed to selling 25% of its beverages in reusable or refillable packaging by 2030. Returnable glass bottles average 30–40 trips before recycling, dramatically reducing per-use carbon footprint relative to single-use formats. The returnable glass bottle market is expected to witness steady growth over the forecast period, expanding at a consistent pace driven by a moderate compound annual growth rate. Infrastructure investments in collection, washing, and redistribution logistics are critical enablers markets with established deposit-return systems (Germany, Scandinavia, Mexico) already operate at scale and serve as models for expansion into Asia-Pacific and North America.

Smart Glass Packaging & Digital Integration

The integration of NFC (Near Field Communication) chips and QR codes into glass bottles is an emerging opportunity that enhances consumer engagement, enables product authentication, and provides brands with real-time supply chain traceability. Premium spirits, wine, and cosmetics brands are piloting NFC-enabled bottles that unlock tasting notes, provenance stories, and personalized promotions via smartphone. As the cost of NFC tags falls below USD 0.10 per unit, mass-market adoption becomes economically viable. Glass's premium positioning makes it the natural substrate for smart packaging, differentiating it further from PET and aluminum alternatives.

The EMR’s report titled “Global Glass Bottles Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Capacity

Key Insights: The global glass bottles market quickly changes across different capacity segments: miniature (≤ 50 ml) units are rapidly spreading in luxury perfume and cosmetic samples as producers are implementing sustainable, lighter glass kinds. For example, cosmetics packaging producers are turning to eco-friendly, low-carbon, and reusable materials such as glass. Mid-size (51–200 ml) and 201–500 ml bottles are still very important for pharmaceutical syrups, nutraceuticals, and spirits, where a company like Diageo is very actively doing the lightweighting and increasing the recycled content of their liquor bottles. In addition, 500 ml+ bottles and refillable containers are getting more popular in bulk beverages and gourmet food packaging as sustainability-led reuse and circular-economy initiatives become increasingly popular.

Market Breakup by Manufacturing Process

Key Insights: The global glass bottles market is largely influenced by blown and tubing processes. Beverages, food, and premium packaging rely on the blown process, which is the focus of companies like Arglass and Owens-Illinois, to be done via automation, lightweighting, and energy-efficient furnaces. On the other side, the tubing process is for the pharmaceutical and nutraceutical industries only, and some of the great SCHOTT and Gerresheimer initiatives in this industry include capacity expansion, quality control improvement, and sterile manufacturing adoption. Moreover, both methods are still open for reforms regarding efficiency and sustainability.

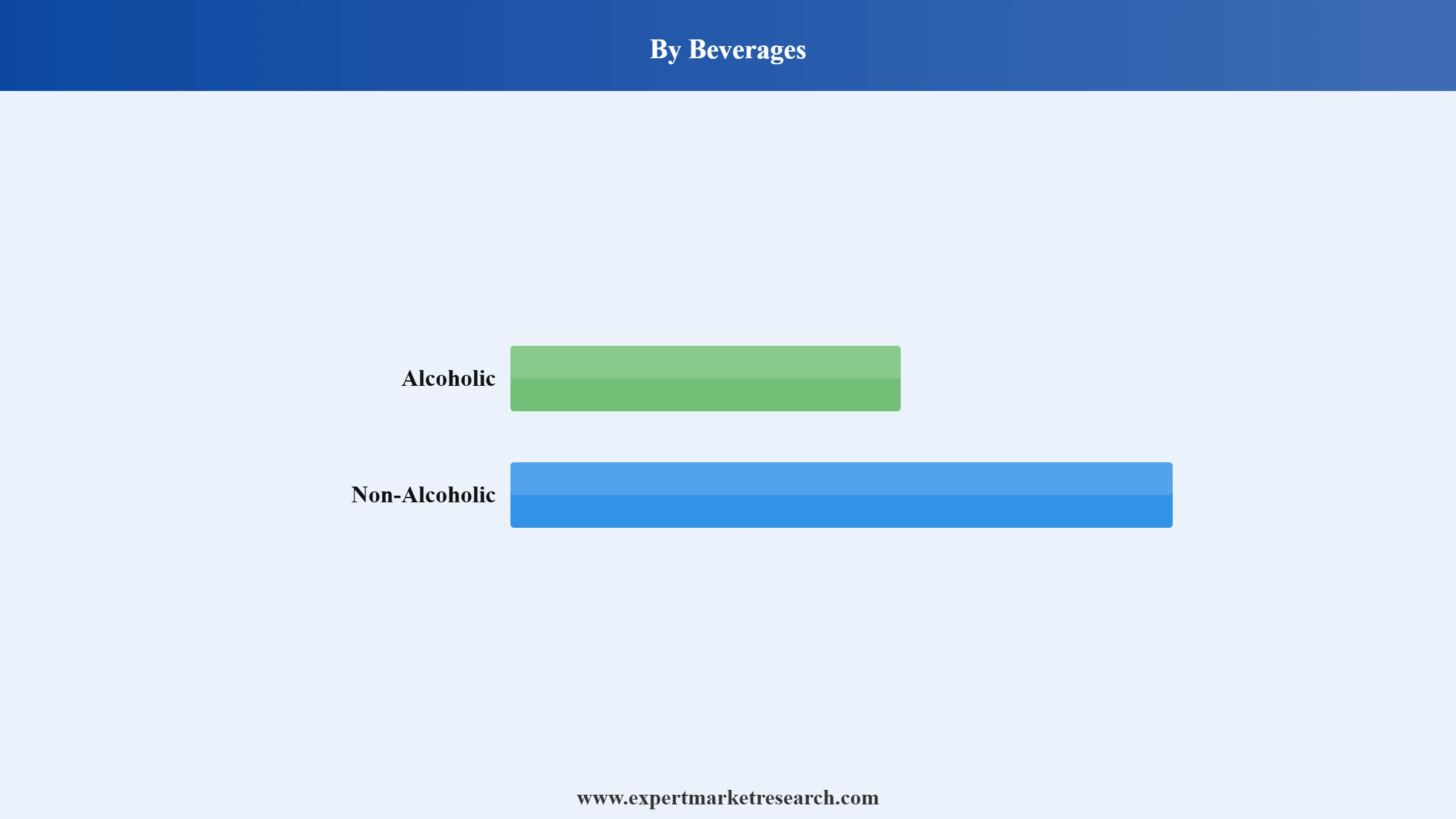

Market Breakup by Beverages

Key Insights: One of the factors that the global glass bottles market is highly dependent on is the segment of alcoholic and non-alcoholic beverages. As one of the most intensive users of glass containers, alcohol beverages, such as spirits, wine, and beer, are trying to surface their sustainability efforts by a company like Diageo using lightweight, returnable bottles. Furthermore, in the field of non-alcoholic beverages, such as juices, soft drinks, and energy drinks, there is a steady growth in glass usage for the reasons of its premium perception and product safety, and one of the major brands, like Coca-Cola, is taking the lead to adopt eco-friendly packaging designs.

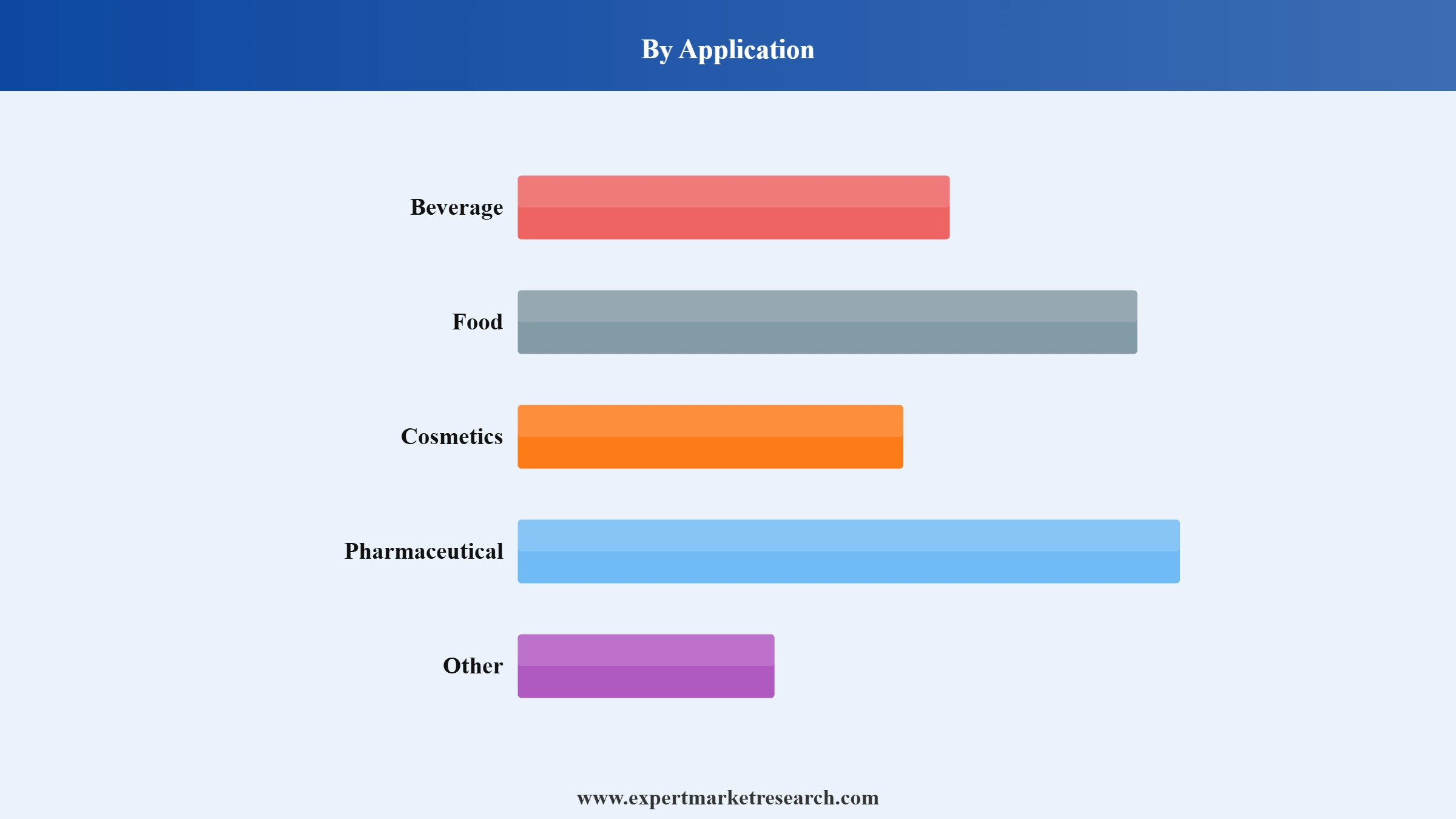

Market Breakup by Application

Key Insights: By serving a variety of industries like beverages, food, cosmetics, and pharmaceuticals, the global glass bottles market is mostly influenced by the need for safe, premium, and sustainable packaging. Brands in the beverage and food industries are concentrating on using lightweight and recyclable glass, while cosmetics and pharma are more inclined towards luxury packaging and chemical resistance. For example, SGD Pharma unveiled post-consumer recycled (PCR) glass bottles in 2024, clearly indicating the transition to eco-friendly glass in cosmetics and pharmaceuticals.

Market Breakup by Filament Type

Key Insights: Moulded glass is mainly used in beverages, food, and cosmetics because of its ability to produce high volumes, the flexibility of the design, and the attractive finish. So, a couple of the most significant players in this market, like Ardagh Glass and Owens-Illinois, are heavily investing in automation and lightweighting. Whereas tubular glass is more often used in pharmaceuticals and nutraceuticals because of its accuracy, chemical resistance, and sterilization. Several production expansion projects by SCHOTT and Gerresheimer aiming at meeting both regulatory requirements and market demands are now underway in this sector.

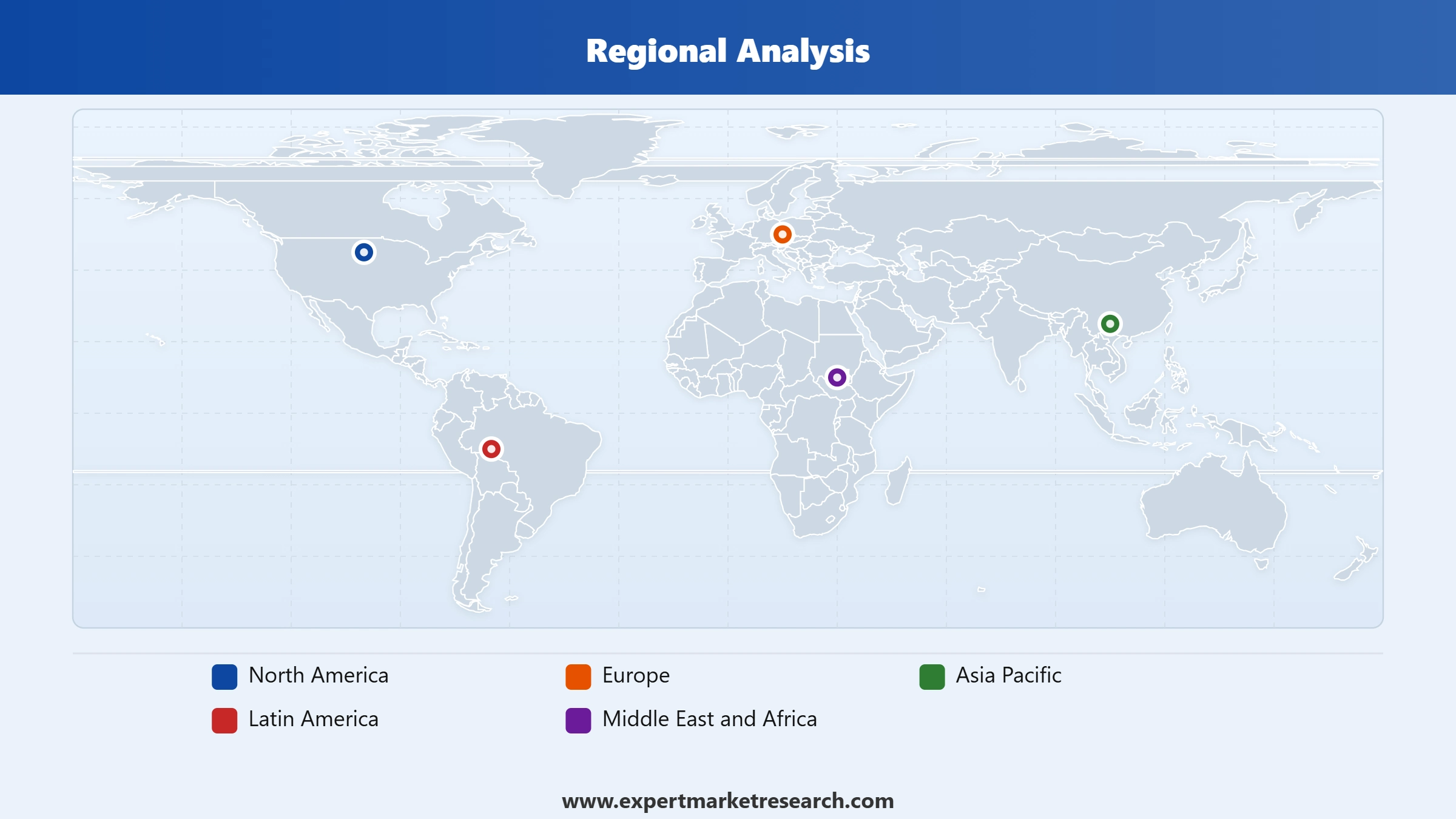

Market Breakup by Region

Key Insights: North America demonstrates notable growth in the global glass bottles market attributed to the presence of companies like Owens-Illinois and Ardagh Group which are increasing their production capacity and introducing lighter bottles for beverages. In Europe, the market growth is influenced by the prominent activities of firms such as Vetropack and Heinz Glas, which are implementing eco-friendly production and hybrid furnace technologies. Asia Pacific boasts of companies such as Toyo Seikan and Vitro SAB, who are broadening their operations to fulfil the demands for beverage and cosmetic products. Meanwhile, Latin America and MEA are gradually growing as their local players are providing recyclable and premium glass solutions for food, pharma, and personal care sectors.

Access Detailed Forecasts & Data-Driven Insights – Download Free PDF

The glass bottles market is analyzed across five key geographic regions, each with distinct demand dynamics, regulatory environments, and growth trajectories.

North America - Market Leader (~55% share)

North America holds the largest share of the global glass bottles market, supported by strong beverage consumption, premium spirits demand, and a well-established glass manufacturing infrastructure. The United States is the dominant market, with California's SB 54 mandate driving accelerated brand conversion from plastic to glass. Canada similarly benefits from stringent single-use plastic regulations. Major container manufacturers including Owens-Illinois (O-I) and Ardagh operate extensive furnace capacity across the region.

Europe - Sustainability & Regulatory Driver

Europe is a mature but innovation-driven market, propelled by some of the world's most stringent packaging sustainability regulations. France's polystyrene ban, the EU's bisphenol-A restrictions, and Extended Producer Responsibility (EPR) frameworks are steering brand owners toward glass. The premium wine and spirits industries in France, Italy, and Spain provide a strong structural demand base. Vidrala, Verallia, and Ardagh are key regional producers investing in furnace modernization and lightweighting.

Asia-Pacific - Fastest Growing Region

Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, urbanization, and expanding beverage consumption in China, India, Japan, and Southeast Asia. India's expanding pharmaceutical manufacturing base bolstered by government initiatives such as Production-Linked Incentive (PLI) schemes is generating significant new demand for pharmaceutical glass. China's premium liquor (baijiu) segment and growing wine culture are supporting glass bottle adoption. The region is expected to post the highest growth rates through 2035.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Latin America - Emerging Opportunity

Latin America represents a growing market, with Brazil and Mexico as primary demand centers. The beer packaging segment drives the majority of demand in the Latin America glass bottles market, supported by a strong regional brewing culture. Increasing middle-class consumption and growing awareness of packaging sustainability are supporting gradual market expansion. Local producers and global players are investing in regional capacity to serve growing demand.

Middle East & Africa - Nascent Growth

The Middle East & Africa market remains nascent but presents long-term growth opportunities, driven by pharmaceutical sector expansion and the growing non-alcoholic beverages market (carbonated drinks, juices, specialty water). Government infrastructure investments and rising urbanization rates across Sub-Saharan Africa are gradually expanding the addressable market for packaged goods.

The global glass bottles and containers market is characterized by low market concentration, with a mix of large multinational manufacturers and regional producers competing across segments and geographies. Key players are investing in furnace modernization, lightweighting technologies, and higher recycled-content production to improve sustainability credentials and cost competitiveness.

O-I Glass was founded in 1903 by Michael J. Owens in Toledo, Ohio, and took its current form after the 1929 merger between Owens Bottle Company and Illinois Glass Company. Headquartered in Perrysburg, Ohio, USA, the company is the world's largest manufacturer of glass containers, serving the food, beverage, pharmaceutical, and cosmetics sectors with a focus on MAGMA furnace technology.

Ardagh Group originated in 1932 as the Irish Glass Bottle Company in Dublin and is now headquartered in Luxembourg. The company specializes in sustainable metal and glass packaging for food, beverage, and personal care brands. Following major acquisitions including Anchor Glass and Verallia North America, Ardagh operates around 60 production facilities across 16 countries on four continents.

Verallia traces its origins to the Vauxrot glassworks established in France in 1827, with its packaging division formalized in 1972 and the Verallia brand launched globally in 2010. Headquartered in Courbevoie, France, the company is the European leader and the world's third-largest glass packaging producer for beverages and food, focusing on sustainability and circularity.

Vidrala was founded in 1965 in Llodio, Álava, Spain, by the Delclaux family, with operations starting in 1966. Headquartered in Llodio, Spain, the company is a leading European glass packaging manufacturer specializing in bottles for wine, spirits, beer, soft drinks, and olive oil. Vidrala is recognized for its lightweighting innovation and operates plants across Spain, Portugal, Italy, and the UK.

Gerresheimer was founded in 1864 by Ferdinand Heye in Gerresheim, near Düsseldorf, Germany. Headquartered in Düsseldorf, Germany, the company specializes in primary pharmaceutical packaging vials, ampoules, syringes, and drug delivery devices made of special-purpose glass and plastics. Listed on the German MDAX, Gerresheimer is a key beneficiary of biologics and injectable drug packaging growth globally.

SCHOTT AG was founded in 1884 by Otto Schott — credited with inventing borosilicate glass in Jena, Germany. Headquartered in Mainz, Germany, the company is a specialty glass manufacturer with strong focus on pharmaceutical packaging, particularly borosilicate glass vials, cartridges, ampoules, and syringes. SCHOTT serves global biopharma, vaccine, and medical device clients across more than 30 countries.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other players in the market include Vitro SAB, Heinz Glas, Koa Glass, and, Nihon Yamamura, among others.

Explore the latest trends shaping the Global Glass Bottles Market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on global glass bottles market trends 2026.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global glass bottles market reached an approximate value of USD 43.45 Billion.

The market is projected to grow at a CAGR of 6.10% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach USD 78.55 Billion by 2035.

Key strategies driving the market include product innovation, premium packaging development, partnerships with beverage and beauty brands, global capacity expansion, and sustainability-focused manufacturing upgrades.

Innovations in packaging industry, growing focus on minimising plastic consumption, and increasing demand for flavoured beverages are the key trends propelling the growth of the market.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The primary applications of glass bottles are beverage, food, cosmetics, and pharmaceutical, among others.

The key players in the market include Ardagh Group, Toyo Seikan, O-I Glass, AptarGroup, Vitro SAB, Gerresheimer, Heinz Glas, Koa Glass, Nihon Yamamura, Owens-Illinois, and several other regional and local manufacturers.

The major challenges that the global glass bottles market faces are high energy and production costs, raw material and logistics volatility, competition from alternative packaging, and rising regulatory pressure for circular and low-carbon packaging.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Capacity |

|

| Breakup by Manufacturing Process |

|

| Breakup by Beverages |

|

| Breakup by Application |

|

| Breakup by Filament Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.