Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

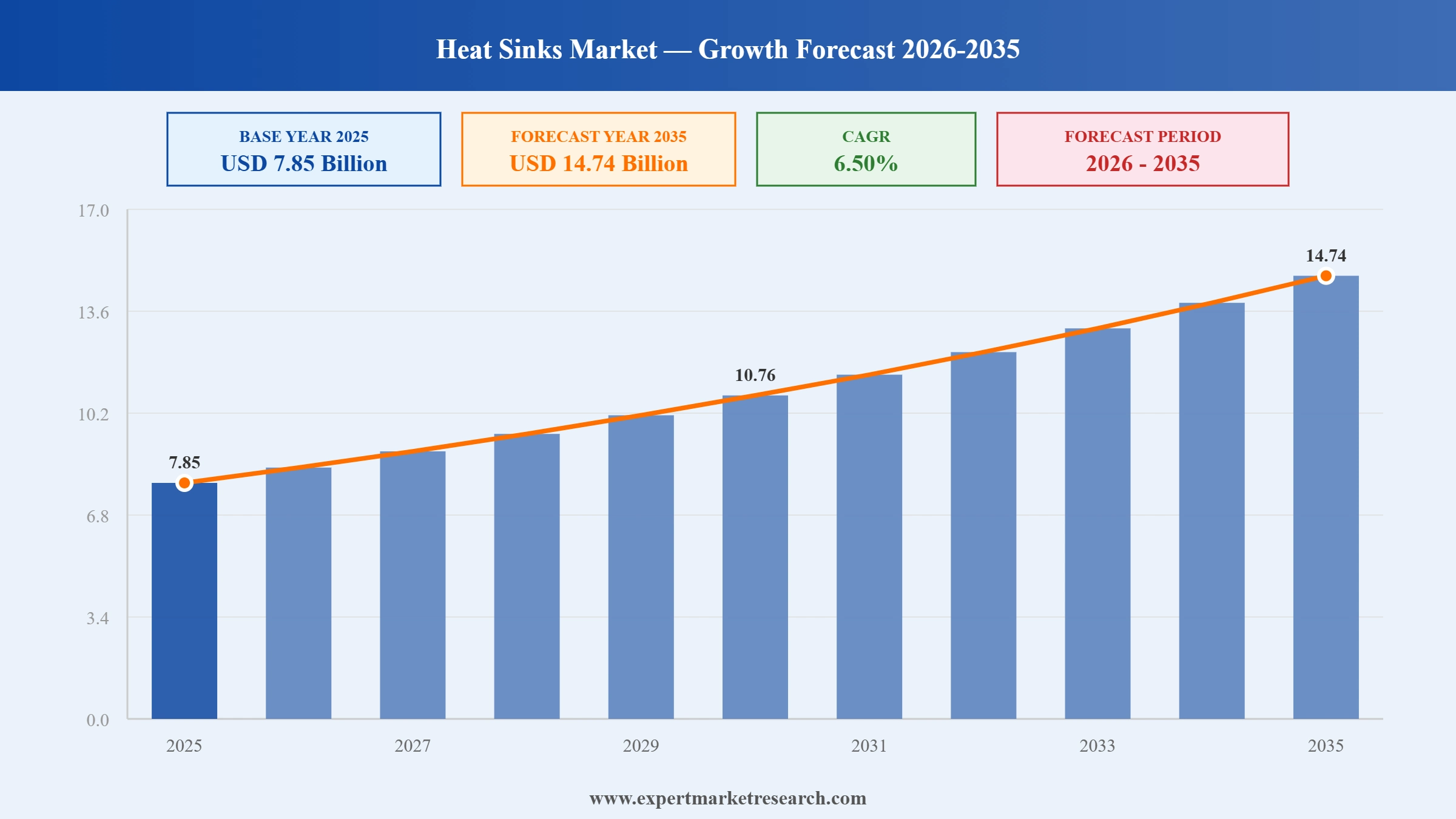

The heat sinks market reached a value of USD 7.85 Billion at 2025 and is projected to expand at a CAGR of around 6.50% during the forecast period of 2026-2035. With rapidly growing AI data centre thermal management requirements, surging electric vehicle battery cooling demand, miniaturisation of high-performance electronics, and expanding adoption of advanced copper and aluminium heat sink materials, the market is expected to reach USD 14.74 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global heat sinks market is being reshaped by the intersection of AI compute expansion, electric vehicle proliferation, and advanced electronics miniaturisation. Hyperscalers and cloud providers are moving away from traditional air-cooling toward liquid-based thermal management as GPU rack density increases, while automotive OEMs are demanding precision thermal solutions for battery packs, traction inverters, and onboard charging systems. Material science advances in copper-aluminium composites and 3D-printed heat sinks are opening new performance frontiers.

In January 2026, Eaton completed its $9.5 billion acquisition of Boyd Corporation, a leading thermal management and liquid cooling solutions provider. The acquisition provided Eaton with instant scale in the data centre cooling segment and strengthened its ability to supply advanced thermal management solutions to hyperscalers, semiconductor manufacturers, and EV OEMs within the growing heat sinks market.

In May 2026, analysis by Future Market Insights confirmed that the global AI data centre liquid cooling market was entering a high-growth phase as hyperscalers deployed GPU-intensive AI training environments. The trend directly supported the heat sinks market as thermal management requirements at the component level intensified with rising AI chip power densities.

In January 2025, advanced 3D printing technologies were integrated into commercial heat sink production for the first time at scale, enabling complex fin geometries previously unachievable through conventional extrusion or stamping. The innovation yielded improved thermal performance for high-performance computing, automotive electronics, and compact consumer device applications within the heat sinks market.

In November 2024, Microsoft deployed its proprietary Sidekick direct-to-chip liquid cooling system for Azure Maia AI Accelerator chips, incorporating cold plates and precision thermal management to handle next-generation GPU heat loads. The move set a benchmark for hyperscaler thermal architecture and accelerated demand for high-performance heat sink and cold plate assemblies across the heat sinks market.

AI chip power densities are growing at a rate that traditional air-cooled heat sinks cannot address cost-effectively. As rack-level power rises above 100 kW in AI data centres, the heat sinks market is shifting toward liquid-cooled cold plates and vapour chamber solutions that can handle ultra-dense thermal loads efficiently.

EV battery pack thermal management, power inverter cooling, and onboard charger heat dissipation are creating high-growth demand within the heat sinks market. Each battery electric vehicle requires multiple precision thermal management components, and the rapid global expansion of EV production is generating a structural, high-volume demand increase for automotive-grade aluminium and copper heat sinks.

Aluminium heat sinks maintain market leadership because they balance thermal performance, weight, machinability, and unit cost better than pure copper alternatives for the vast majority of consumer electronics and standard industrial applications. The growing electronics manufacturing base in Asia Pacific reinforces heat sinks market growth for aluminium components across compute, networking, and consumer device sectors.

Silicon carbide and graphite-based thermal interface materials and heat sink substrates are gaining traction in the heat sinks market for high-frequency power electronics and aerospace applications. These materials offer superior thermal conductivity and stability at elevated temperatures, enabling compact, high-performance thermal management solutions for next-generation power semiconductor devices.

Rising energy costs and ESG commitments are making heat sink thermal efficiency a design priority across industries. Manufacturers including Aavid Thermalloy and Delta Electronics are developing eco-friendly heat sink solutions that reduce the cooling energy burden on system-level power supplies, supporting heat sinks market growth as sustainability criteria enter procurement decisions.

The Expert Market Research's report titled “Heat Sinks Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

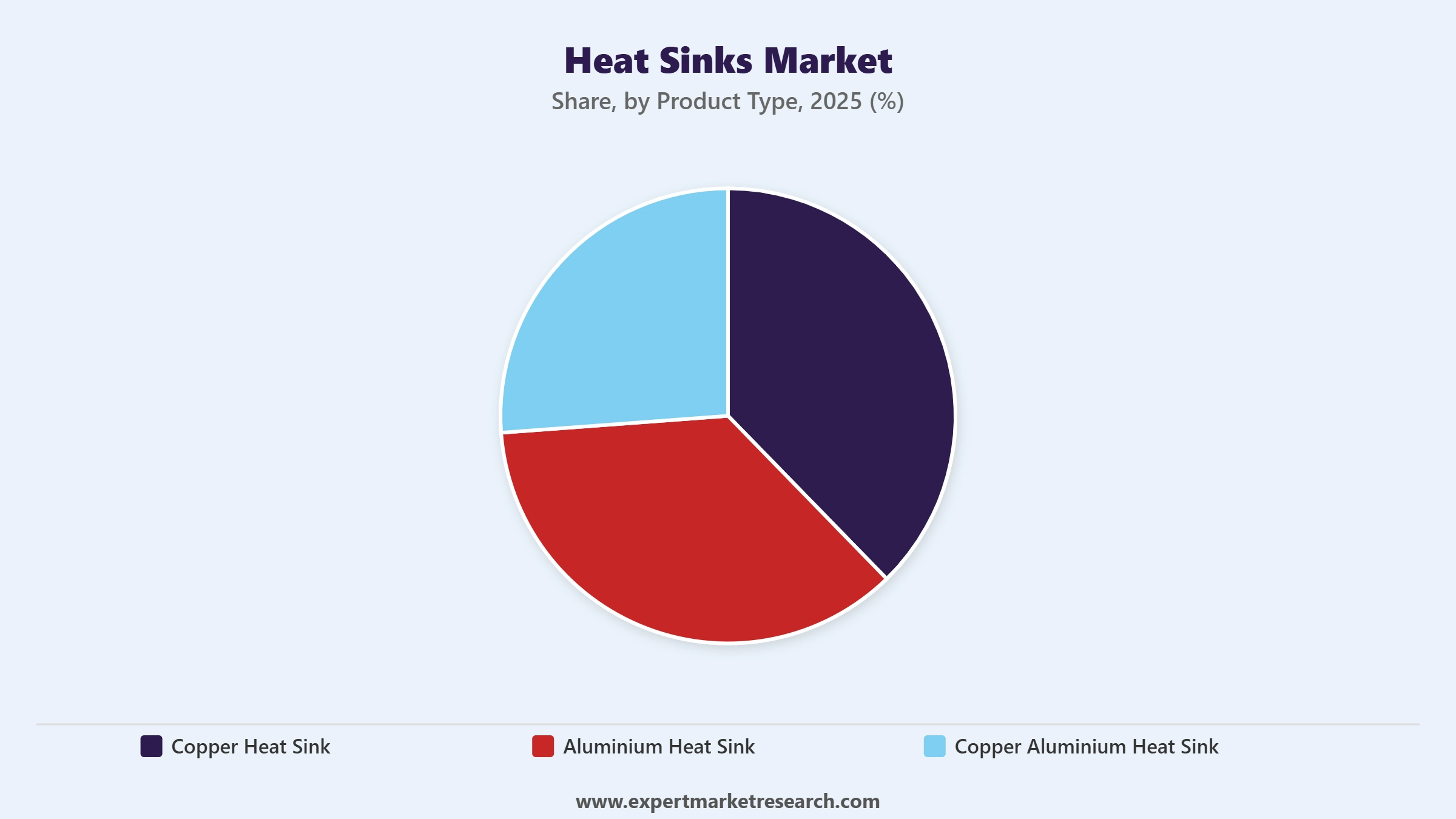

Market Breakup by Product Type

Key Insight: Aluminium heat sinks dominate the heat sinks market by volume because they offer an optimal balance of thermal conductivity, weight, machinability, and cost that suits the broadest range of consumer electronics, telecommunications, and industrial applications. Copper heat sinks serve the premium performance segment, where superior thermal conductivity justifies higher material cost for high-power processors, power amplifiers, and dense server components. Copper-aluminium composite heat sinks represent an emerging category that combines the thermal performance of copper with the weight and cost advantages of aluminium for next-generation power electronics applications.

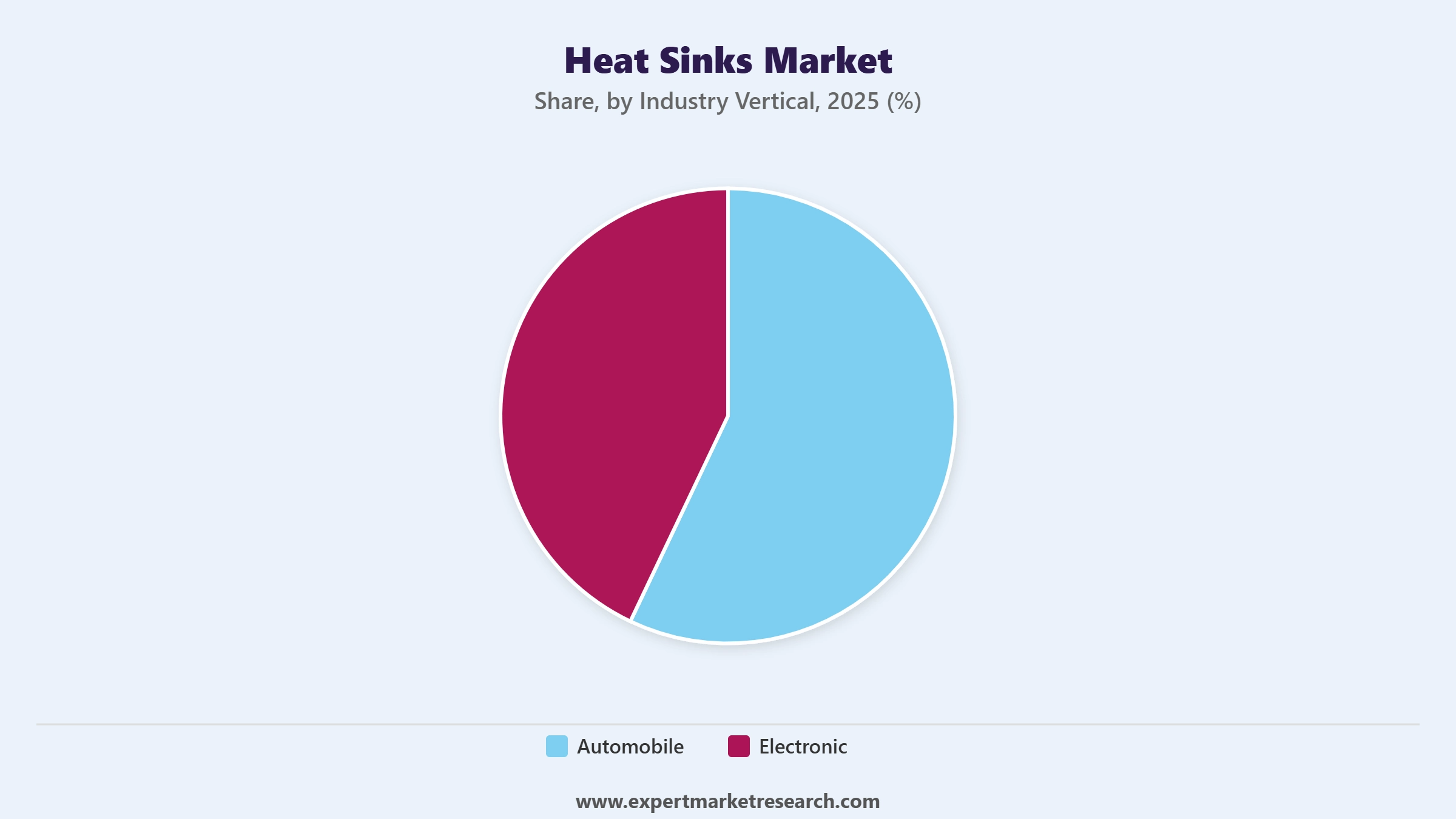

Market Breakup by Industry Vertical

Key Insight: The electronic industry vertical holds the dominant share of the heat sinks market, encompassing data centre servers, networking equipment, consumer electronics, and power management systems that collectively generate the highest aggregate thermal management demand globally. The automobile vertical is the fastest-growing segment, driven by the rapid proliferation of battery electric vehicles requiring thermal management for battery packs, traction inverters, onboard chargers, and ADAS processing modules. The convergence of automotive electrification and electronics content per vehicle is creating a sustained, high-growth demand horizon for automotive-grade heat sinks.

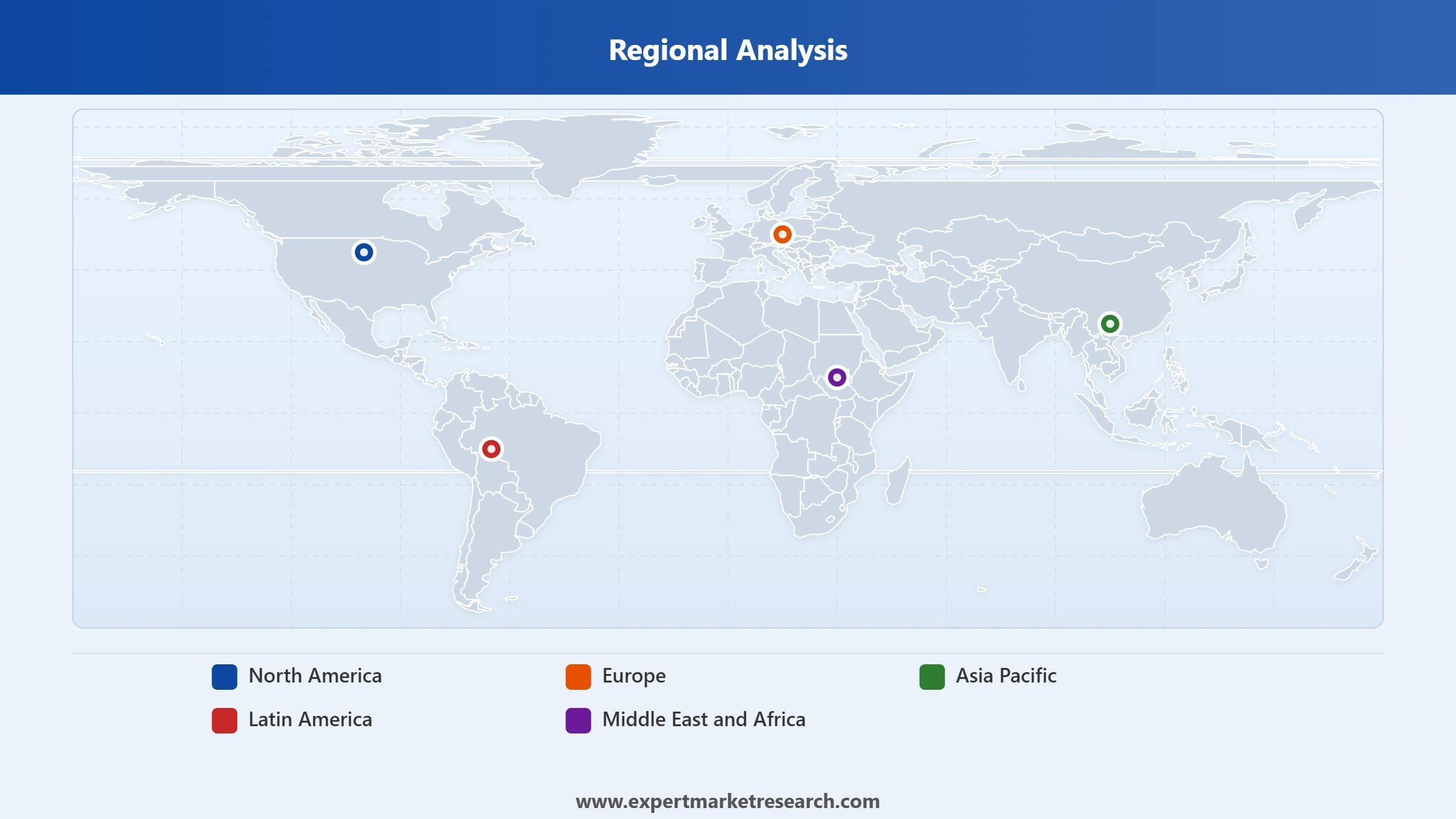

Market Breakup by Region

Key Insight: Asia Pacific dominates the heat sinks market by production volume and consumption value, anchored by China, Taiwan, Japan, and South Korea's dominant positions in electronics manufacturing, semiconductor packaging, and automotive component production. North America is a fast-growing innovation market, driven by AI data centre buildout by hyperscalers and the expansion of advanced semiconductor packaging for high-performance computing. Europe's market growth is tied to automotive electrification and industrial electronics demand, particularly in Germany, France, and the Nordic countries where EV production and industrial automation are accelerating.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, aluminium heat sinks dominate the market due to cost-effectiveness and broad application suitability

Aluminium heat sinks lead the global heat sinks market by unit volume because they meet the thermal performance requirements of the broadest range of commercial applications at the lowest total material and manufacturing cost. In consumer electronics, personal computers, networking equipment, and standard industrial power electronics, aluminium's thermal conductivity is sufficient, and its light weight is a valued attribute. The extensive electronics manufacturing ecosystems in China, Taiwan, and South Korea generate consistent, high-volume demand for aluminium heat sink extrusions and die-cast components.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Copper heat sinks are the premium performance choice for applications where aluminium's thermal conductivity is insufficient, including high-power server CPUs, power amplifiers, and dense GPU modules operating at elevated thermal design power ratings. As AI chips push thermal design power above 700 watts per chip in 2025-2026, copper cold plates and heat spreaders are increasingly specified alongside aluminium fin arrays. In January 2026, Eaton's Boyd Corporation acquisition provided scale in precisely these high-end thermal management solutions for the heat sinks market.

By industry vertical, electronic industry accounts for the dominant share due to pervasive thermal management needs across devices

The electronic vertical leads the heat sinks market because thermal management is a fundamental requirement across every category of electronic system, from mobile handsets and laptops to enterprise servers, base station radios, and power inverters. The continued trend toward higher computing performance in smaller form factors increases power density and generates escalating thermal loads, ensuring sustained, volume-driven demand for heat sinks across the electronic segment regardless of specific end-device category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The automobile vertical is the fastest-growing segment, with each battery electric vehicle incorporating thermal management across battery packs, traction inverters, DC-DC converters, and ADAS processing units. In January 2025, the integration of 3D-printed heat sink production expanded the design possibilities for automotive thermal management components, enabling complex geometries optimised for tight vehicle packaging constraints. The global BEV production ramp-up is converting automotive into the highest-growth demand vector within the heat sinks market.

Asia Pacific dominates the market due to the world's largest electronics manufacturing and EV production base

Asia Pacific leads the heat sinks market by value and volume because the region is home to the world's largest electronics manufacturing ecosystems and the fastest-growing electric vehicle production base. China's electronics assembly scale and EV ramp-up, Taiwan's advanced chip packaging industry, Japan's precision manufacturing base, and South Korea's consumer electronics dominance collectively generate unmatched aggregate demand for aluminium, copper, and composite heat sink components.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the fastest-growing regional market for premium heat sink solutions, driven by the unprecedented build-out of AI and high-performance computing data centres. As hyperscalers including Microsoft, Google, and Amazon invest tens of billions in AI infrastructure, rack-level power densities are rising rapidly, requiring direct-to-chip cooling solutions and high-performance vapour chambers that go beyond conventional air-cooled aluminium heat sinks. In January 2026, Eaton's Boyd acquisition created a scaled North American capability in precisely these advanced thermal management segments of the heat sinks market.

The global heat sinks market is fragmented across thousands of manufacturers, with a small number of vertically integrated specialists holding leading positions in premium thermal management segments. Aavid Thermalloy (Boyd Corporation), Delta Electronics, Advanced Thermal Solutions, and Sunonwealth Electric Machine Industry compete on design engineering capability, material science expertise, manufacturing precision, and customisation for specific OEM thermal management requirements.

Competition is shifting toward liquid cooling capability, AI and data centre thermal solutions, and automotive-grade product qualification as the most valuable growth segments of the market. Eaton's acquisition of Boyd Corporation and the broad market trend toward liquid cold plates reflect how leading players are repositioning for the highest-growth demand categories.

Taiwanese thermal management and cooling solutions manufacturer founded in 1970, headquartered in Kaohsiung. Sunonwealth, operating under the Sunon brand, specialises in heat dissipation products including heat sinks, thermal modules, and cooling fans for consumer electronics, industrial equipment, and networking applications. Its Asia Pacific manufacturing base supports cost-competitive supply to global OEM customers.

US-based thermal management specialist headquartered in Norwood, Massachusetts. Advanced Thermal Solutions provides engineering consultancy, heat sink design, and thermal testing services primarily for the electronics and telecommunications industries. Its ATS-Coldplate and ATSink product lines serve demanding applications including power electronics, telecommunications, and RF systems requiring precision thermal performance.

US-based thermal management company now operating as Boyd Corporation following its acquisition by Boyd. Aavid Thermalloy is one of the most established heat sink and thermal management solution providers globally, serving data centres, telecommunications, power conversion, and automotive markets with extruded aluminium, stamped copper, and liquid-cooled heat sink products across its global manufacturing network.

US-based manufacturer founded in 1969 and headquartered in Tucson, Arizona, specialising in high-power precision linear amplifiers and associated thermal management components. Apex Microtechnology's heat sink products are designed for demanding signal processing and power amplification applications where temperature stability is critical to linear amplifier performance and reliability across industrial and defence markets.

Other key players in the market are CUI Inc., Comair Rotron, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full picture of the global heat sinks market with our comprehensive report for 2026. Understand where AI data centres, electric vehicles, and consumer electronics are driving the highest thermal management demand, and which product types and regions are set for the most rapid growth. Whether you manufacture thermal components, supply electronics OEMs, operate data centres, or invest in electronics supply chains, this report gives you the intelligence to act. Download your free sample today and explore the key opportunities in heat sinks.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the heat sinks market reached an approximate value of USD 7.85 Billion.

The market is expected to grow at a CAGR of 6.50% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to USD 14.74 Billion by 2035.

The major drivers of the market include the increasing applications of heat sinks in high-power semiconductors, rising sales of automobiles, and increasing demand for consumer electronics.

Key trends aiding market expansion include the growing popularity of electric vehicles, enhancements in thermal management systems of various electronics, and growing research and development activities to enhance the efficiency of heat sinks.

Regions considered in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

Copper heat sink, aluminium heat sink, and copper aluminium heat sink are the different product types in the market.

Automobile and electronic are the significant industry verticals in the market.

The major components of heat sink include metal such as aluminium or copper, fan, and conductive thick plate, among others.

Key players in the market are Sunonwealth Electric Machine Industry Co. Ltd., Advanced Thermal Solutions, Inc., Aavid Thermalloy, LLC, Apex Microtechnology, CUI Inc., and Comair Rotron, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Industry Vertical |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.