Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

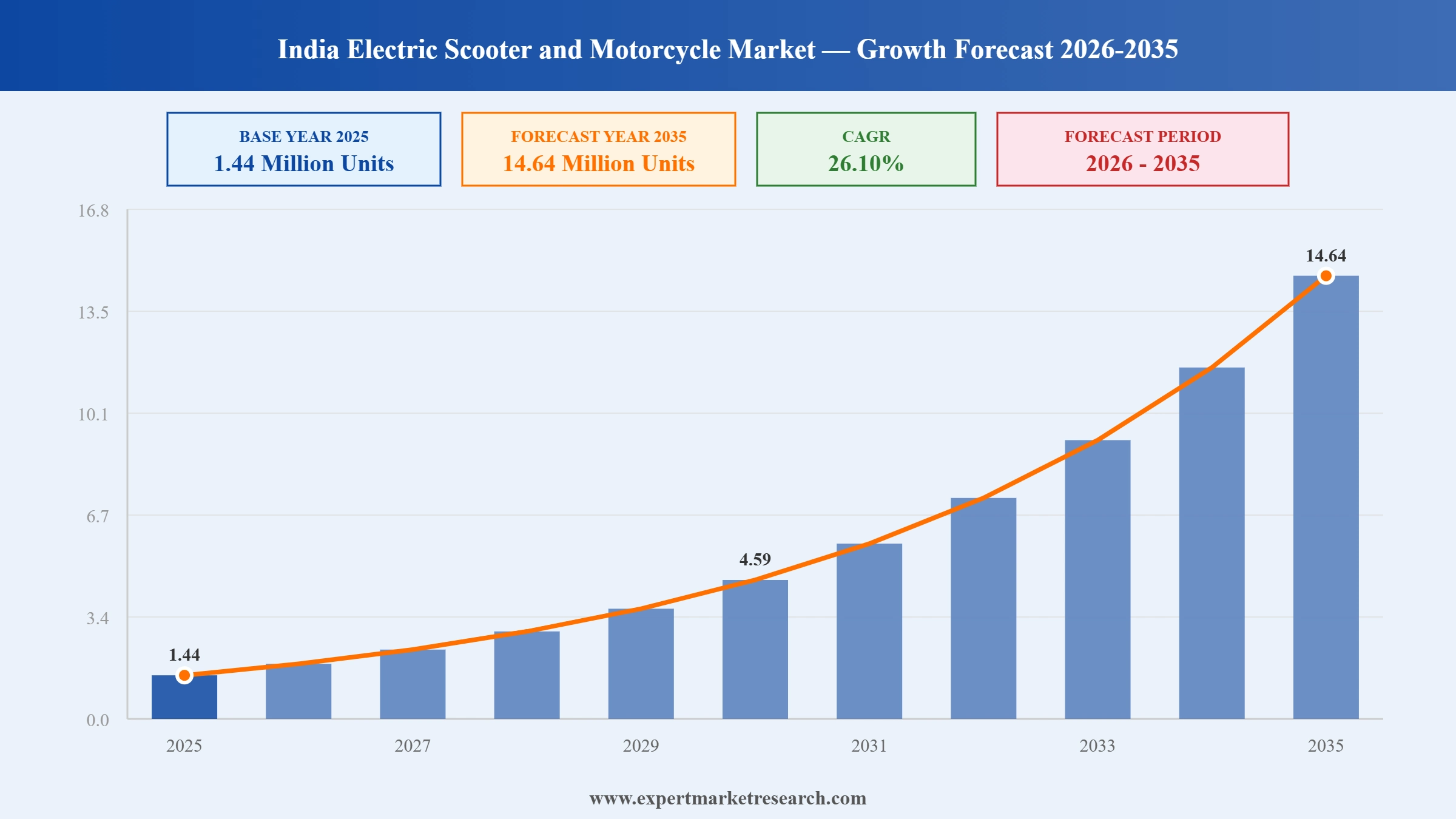

The India Electric Scooter and Motorcycle Market reached a volume of 1.44 Million Units at 2025 and is projected to expand at a CAGR of around 26.10% during the forecast period of 2026-2035. With growing adoption of lithium-ion battery technology, sustained government support through schemes like FAME-II and PM E-Drive, rising petrol prices driving consumer preference toward electric alternatives, and rapid geographic expansion into semi-urban markets across the country, the market is expected to reach 14.64 Million Units by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Electric Scooter and Motorcycle Market Report Summary |

Description |

Value |

|

Base Year |

Million Units |

2025 |

|

Historical Period |

Million Units |

2019-2025 |

|

Forecast Period |

Million Units |

2026-2035 |

|

Market Size 2025 |

Million Units |

1.44 |

|

Market Size 2035 |

Million Units |

14.64 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

26.10% |

|

CAGR 2026-2035 - Market by Region |

East India |

27.9% |

|

CAGR 2026-2035 - Market by Region |

West India |

26.9% |

|

CAGR 2026-2035 - Market by Battery Type |

Li-ion |

32.5% |

|

CAGR 2026-2035 - Market by Technology |

Battery |

32.7% |

|

2025 Market Share by Region |

South India |

31.6% |

India's electric two-wheeler market is being reshaped by a combination of policy recalibration, accelerating OEM competition, technology cost curves, and new commercial demand dynamics, all of which are converging to shift the market from an incentive-driven phase toward more organic, consumer-led growth.

Ultraviolette Automotive signed a memorandum of understanding with the Government of Karnataka in March 2026 for a Phase 2 manufacturing facility expansion worth INR 2 billion. The new plant is designed to produce an additional 150,000 electric motorcycles per year, backed by state production-linked incentive support. The agreement reinforces Karnataka's status as the preferred destination for premium electric two-wheeler manufacturing in India, while positioning Ultraviolette to significantly increase its supply capacity ahead of anticipated demand growth in the performance segment. The expansion also creates downstream opportunities for local component manufacturers and engineering talent within the Bengaluru EV ecosystem.

Ather Energy and Infineon Technologies entered a strategic technology partnership in May 2025 focused on deploying advanced semiconductor solutions in electric scooters destined for the Indian market. The collaboration centers on integrating silicon carbide (SiC) and gallium nitride (GaN) semiconductor components into Ather's vehicle platforms, targeting improvements in energy efficiency, faster charging capability, and broader system reliability. The partnership represents a broader trend where Indian EV manufacturers are turning to component-level technology collaboration to build durable competitive advantages as hardware specifications converge and software-defined features become primary purchase motivators for urban consumers.

Honda Motorcycle and Scooter India introduced the Activa e, its inaugural electric scooter for the domestic market, bringing swappable battery architecture to one of India's most iconic two-wheeler nameplates. The vehicle features dual 1.5 kWh batteries and a 6 kW motor producing 22 Nm of torque across a 102 km operating range. Battery swap services were initially rolled out in Bengaluru in early 2025, before expanding to Delhi and Mumbai by April 2025. The product's success in early markets is expected to establish a template for how legacy two-wheeler brands with decades of dealership reach can accelerate EV adoption without requiring buyers to make significant behavioral changes around charging.

Suzuki Motorcycle India made its formal entry into the country's electric two-wheeler segment in January 2025 by unveiling the e-Access electric scooter at the Bharat Mobility Global Expo in New Delhi. The model was built on the widely recognised Access scooter platform, a deliberate decision to leverage existing consumer trust rather than introduce an unfamiliar brand identity. The launch signals a broader shift in India's two-wheeler industry as established ICE manufacturers commit to electrification, intensifying competition against EV-native players. Suzuki's market entry reinforces the view that brand reliability is now a critical differentiator as early-adopter dynamics give way to mass-market considerations in the Indian EV segment.

Hero MotoCorp announced a strategic collaboration with California-based Zero Motorcycles in November 2024, targeting the co-development of a performance electric motorcycle aimed at India's premium two-wheeler segment. The arrangement combines Zero Motorcycles' track record in high-performance EV engineering with Hero MotoCorp's unmatched manufacturing scale and a distribution footprint of more than 6,000 dealer touchpoints across India. The partnership signals India's largest two-wheeler company moving beyond volume leadership in the ICE segment to build credibility in the performance electric motorcycle category, where players like Ultraviolette Automotive currently hold a strong positioning advantage.

The Ministry of Heavy Industries halved the PM E-Drive electric two-wheeler incentive to INR 2,500 per kWh from April 2025, with the scheme's terminal date set for July 2026. This policy recalibration is compelling manufacturers to accelerate supply chain localisation, trim production costs, and rethink pricing models rather than relying on subsidy-bridged affordability. Brands with deeper manufacturing integration and stronger balance sheets are consolidating market share as subsidy dependency declines, marking a significant structural shift toward demand-led growth in India's electric scooter and motorcycle market growth cycle.

India's electric two-wheeler market entered a new competitive phase in 2025 as established ICE manufacturers accelerated their electrification timelines. Suzuki Motorcycle India debuted the e-Access in January 2025, and Honda launched the Activa e with battery swap capability in March 2025, bringing decades of brand trust and nationwide service infrastructure into direct competition with EV-native brands. This trend is narrowing the experiential gap that pure-play EV companies once held, forcing the entire market to compete more aggressively on product quality, after-sales service, and financing accessibility rather than novelty alone.

The cost of lithium-ion battery packs in India declined to approximately INR 10,000 per kWh in 2024 from roughly INR 20,000 per kWh in 2020, reducing the effective on-road price premium of electric scooters over comparable petrol models by INR 12,000 to INR 18,000 across typical 2 to 3 kWh configurations. This cost trajectory is one of the most important structural factors in the India electric scooter and motorcycle market outlook, as it enables manufacturers to offer competitive products across broader price bands, including the critical mass-market entry level below INR 80,000, where first-time buyers are most price-sensitive.

Commercial fleet electrification is emerging as a structural demand driver in the India electric scooter and motorcycle market forecast horizon, distinct from retail consumer cycles and largely insensitive to subsidy changes. Last-mile delivery operators from the e-commerce sector have begun deploying electric two-wheelers at scale, as demonstrated by Amazon India's partnership with TVS Motor Company to deploy 10,000 iQube electric scooters for delivery operations across India. Fleet buyers prioritise total cost of ownership over upfront price, making the operational cost advantages of electric two-wheelers particularly compelling as petrol prices remain elevated and urban emission restrictions tighten around major commercial zones.

The Expert Market Research's report titled "India Electric Scooter and Motorcycle Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

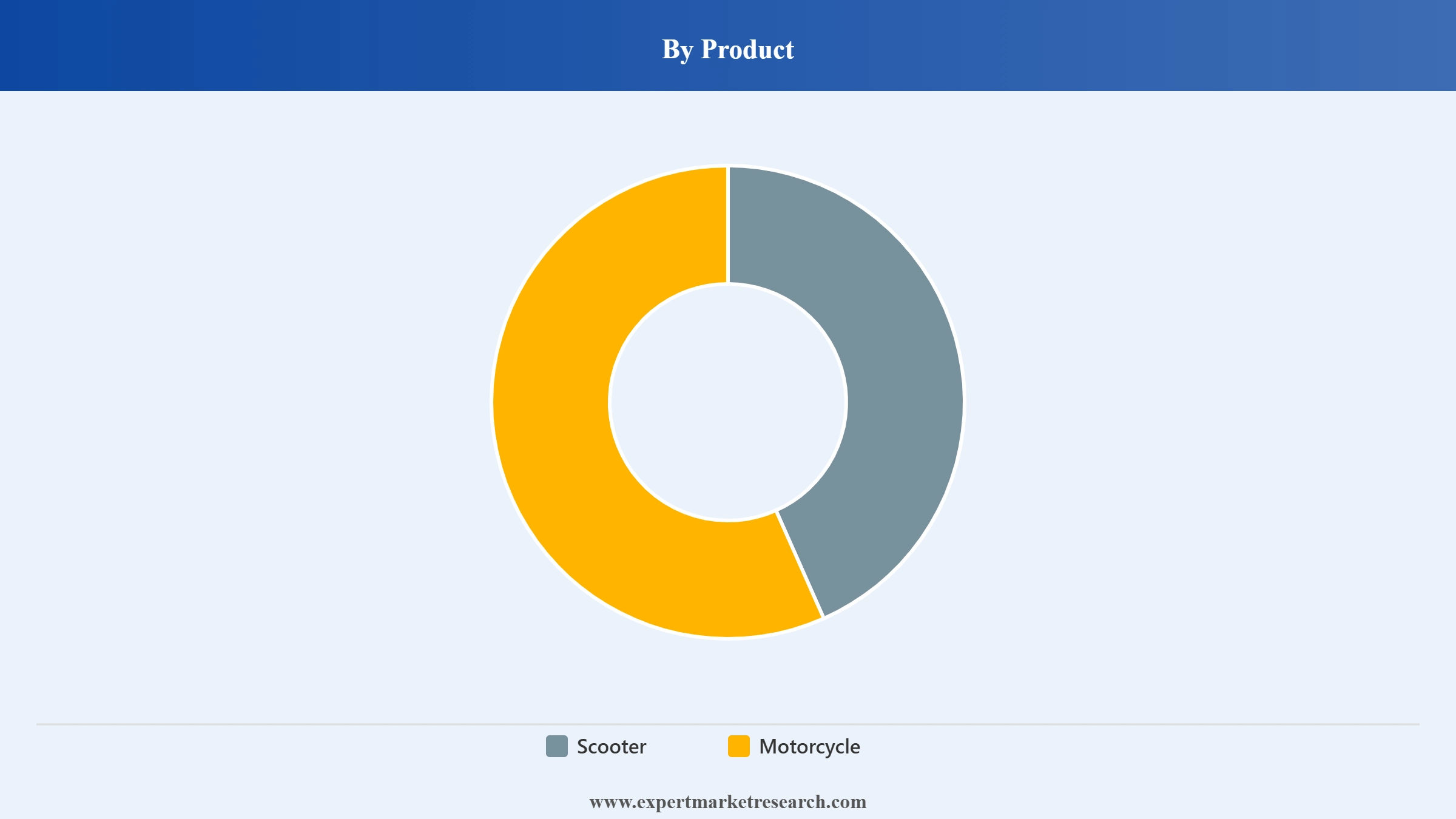

Market Breakup by Product

Key Insight: The Scooter sub-segment holds a commanding position within the India Electric Scooter and Motorcycle Market, accounting for more than 85% of total electric two-wheeler sales volume in FY 2025-26. Scooters benefit from lower average selling prices, simpler mechanical architecture, and inherent suitability for dense urban traffic conditions, making them the preferred choice for middle-class households and first-time EV buyers across Indian cities. TVS iQube, Bajaj Chetak, Ather Rizta, and Honda Activa e represent the key volume drivers in this sub-segment. Electric motorcycles, while a smaller share of current sales, are gaining momentum in the performance-conscious segment. Brands like Ultraviolette Automotive, Revolt Motors, and Hero MotoCorp's VIDA are targeting younger, range-focused riders seeking higher speeds and sportier designs. The motorcycle segment is also benefiting from increasing B2B demand, particularly from delivery platforms seeking extended-range vehicles for last-mile operations. Both sub-segments are set to grow significantly through the forecast period, though scooters are expected to maintain their dominant share.

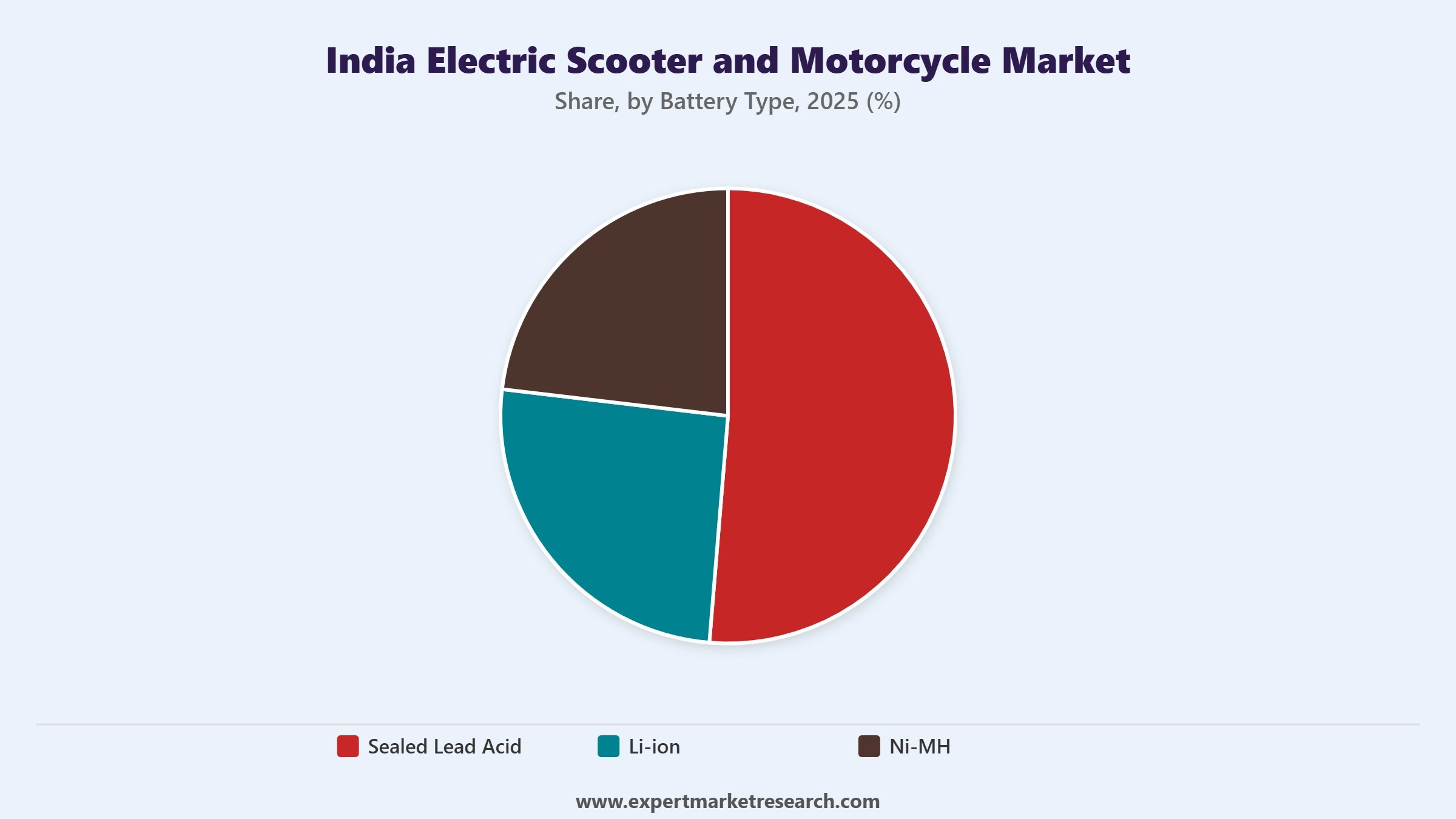

Market Breakup by Battery Type

Key Insight: Li-ion batteries account for more than 92% of new electric two-wheeler sales in India as of 2025, reflecting a decisive market transition from older battery chemistries. Li-ion pack costs fell from approximately INR 20,000 per kWh in 2020 to roughly INR 10,000 per kWh in 2024, making them not only superior in performance but also increasingly competitive on price. Within the Li-ion category, Lithium Iron Phosphate (LFP) chemistry dominates mass-market scooter volumes due to its thermal safety profile and long cycle life, while Nickel Manganese Cobalt (NMC) packs are used in premium electric motorcycles where energy density matters most. The PM E-Drive subsidy scheme, which is exclusively tied to advanced Li-ion cell types, is a powerful structural incentive reinforcing this shift. Sealed lead acid (SLA) batteries are now largely confined to low-speed, unregistered models below 25 km/h. Ni-MH batteries represent a negligible and declining share of new sales, remaining relevant only in niche applications. The Li-ion sub-segment's dominance is expected to deepen considerably through the forecast period.

Market Breakup by Technology

Key Insight: The Plug-in charging technology segment remains the backbone of the India electric two-wheeler market, covering the vast majority of retail consumer vehicles where home charging is the predominant behaviour, accounting for over 70% of electric two-wheeler owner interactions. However, battery-swappable vehicle technology is gaining significant traction, particularly within B2B fleet and last-mile delivery use cases where vehicle downtime is a critical commercial constraint. Honda's Activa e launch in early 2025 with dual swappable 1.5 kWh packs demonstrated how even mainstream OEMs are adopting swap-ready designs. SUN Mobility's partnership with IndianOil, established in June 2024, resulted in the deployment of more than 10,000 battery-swapping stations across more than 40 Indian cities, building a growing physical network for the Battery-as-a-Service model. Both technology categories are expected to grow substantially through the forecast period, with battery swapping likely to expand its share within the commercial fleet segment.

Market Breakup by Volatge

Key Insight: The 48V configuration is the most widely adopted voltage specification in India's mass-market electric scooter segment, offering an effective balance between motor performance, charging speed, and component cost within the INR 70,000 to 1,00,000 price band. Higher voltage platforms at 60V and above are increasingly common in performance electric motorcycles, where they support faster acceleration and higher rated speeds demanded by urban performance riders. The 36V segment is primarily associated with legacy lead-acid low-speed scooters, a category that is actively shrinking as affordable high-speed Li-ion models expand their reach into smaller cities. Battery management system (BMS) improvements and falling cell costs are progressively enabling even mass-market manufacturers to shift toward higher-voltage architectures, which support better regenerative braking efficiency and reduce overall charging time. Voltage upgrading is expected to be a steady trend through the forecast period as product sophistication increases across price tiers.

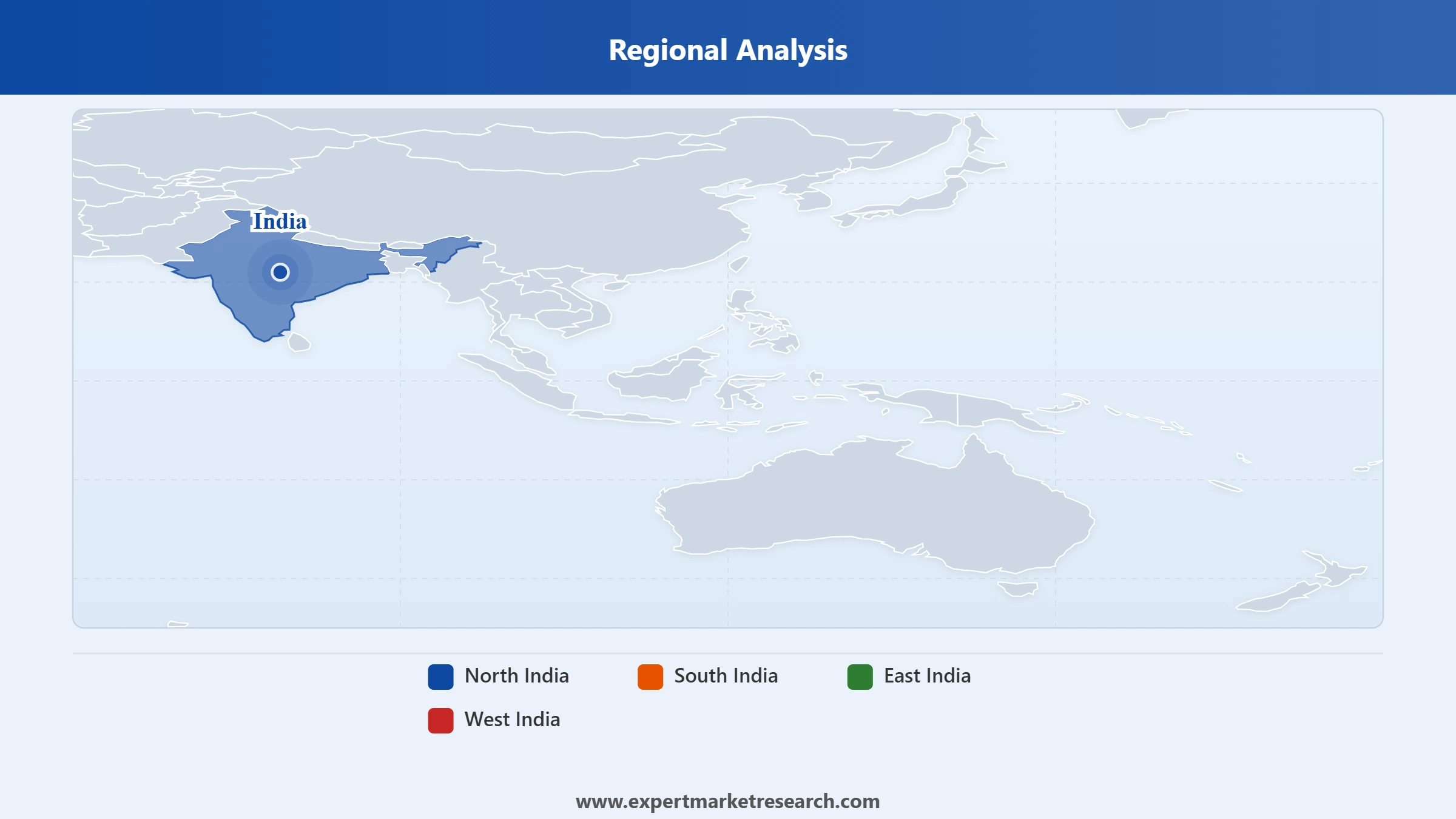

Market Breakup by Region

Key Insight: South India leads the India Electric Scooter and Motorcycle Market, accounting for approximately 36% of FY 2025-26 retail volumes, underpinned by Karnataka, Tamil Nadu, and Kerala as the three primary demand centres. Karnataka houses the production and headquarters operations of Ather Energy and Ultraviolette Automotive, while TVS Motor Company's Hosur facility in Tamil Nadu operates as the single-largest electric two-wheeler production site in India. Tamil Nadu's state EV policy, which provides 100% road tax and registration fee waivers for electric vehicles, has been a meaningful consumer demand catalyst. North India is the second-largest market, driven by Delhi's progressive EV mandate that will require electric-only two-wheeler registrations from April 2028, alongside strong demand across Uttar Pradesh, Rajasthan, and Punjab. West India, anchored by Maharashtra's INR 1,993 crore EV incentive commitment, forms a strong third regional market. East India is in an earlier growth phase but is witnessing steadily improving penetration through expanding dealer networks across states like West Bengal and Odisha.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Scooter sub-segment holds the dominant position in the Product segmentation of the India Electric Scooter and Motorcycle Market, representing more than 85% of total electric two-wheeler sales volume in FY 2025-26. Scooters have consolidated this leadership position through a combination of structural advantages: their lower price positioning makes them accessible to first-time EV buyers, while their compact and lightweight design allows riders to navigate India's congested urban traffic with greater ease compared to motorcycles. Lower maintenance requirements, thanks to simplified drivetrains, have further reinforced this preference among middle-class buyers. TVS iQube, Bajaj Chetak, and Honda Activa e are among the strongest volume contributors in this sub-segment. The Motorcycle sub-segment, while significantly smaller in volume terms, is attracting a growing cohort of performance-oriented younger riders through brands like Ultraviolette Automotive and the Hero-Zero Motorcycles joint development initiative, with further growth anticipated from expanding delivery fleet deployments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Battery Type segmentation, the Li-ion sub-segment is the clear and overwhelming market leader, accounting for over 92% of new India electric two-wheeler sales as of 2025. This dominance is driven by a multi-factor advantage: Li-ion batteries deliver higher energy density, longer operational life, faster charge acceptance, and lower total cost per kilometre compared to both SLA and Ni-MH alternatives. Critically, the government's PM E-Drive subsidy is exclusively tied to advanced Li-ion chemistry, making it both an economic and regulatory imperative for manufacturers to adopt this technology. Cost declines from INR 20,000 per kWh in 2020 to INR 10,000 per kWh in 2024 have accelerated adoption across price segments. Within the Technology segmentation, Plug-in technology remains the dominant configuration for retail consumers, while the Battery segment (swappable) is rapidly gaining share in fleet and commercial applications. In the Voltage segmentation, the 48V platform commands the mass-market segment, while 60V configurations are establishing themselves in the premium and performance motorcycle sub-segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the most dynamic and best-developed regional market within the India Electric Scooter and Motorcycle Market, commanding around 36% of total retail volumes in FY 2025-26. The region benefits from a rare convergence of manufacturing infrastructure, state government incentives, and consumer readiness. Karnataka's capital, Bengaluru, functions as the electric two-wheeler innovation capital of India, housing Ather Energy, Ultraviolette Automotive, and a growing ecosystem of component and software suppliers. In March 2026, Ultraviolette Automotive formalised a INR 2 billion manufacturing expansion with the Government of Karnataka, adding an additional 150,000 units of annual production capacity under state PLI support. Tamil Nadu hosts TVS Motor Company's Hosur plant, the single-largest electric two-wheeler manufacturing facility in India, while the state's EV policy provides full road tax and registration waivers. Consumer demand in Bengaluru, Chennai, Hyderabad, and Coimbatore remains robust, driven by high urbanisation rates, above-average household incomes, and strong awareness of environmental considerations. Kerala is also emerging as a strong retail market, supported by high literacy and environmental consciousness among its population.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India is the second-largest regional market in the India Electric Scooter and Motorcycle Market, with growth increasingly driven by regulatory imperatives and rising consumer awareness across both urban and semi-urban pockets. Delhi's Draft EV Policy 2026 to 2030 stands out as the most decisive regulatory catalyst in the region, mandating electric-only two-wheeler registrations from April 1, 2028, and offering consumer purchase subsidies of up to INR 30,000 per vehicle. This policy has significantly boosted pre-adoption interest among Delhi commuters. Uttar Pradesh, India's most populous state, is contributing substantial volume as major OEMs including Bajaj Auto, Hero MotoCorp, and TVS Motor expand their distribution networks into Tier-2 cities including Lucknow, Kanpur, Agra, and Varanasi. Rajasthan and Punjab are also growing markets, with brands like KLB Komaki and BGauss Auto building retail footprints across these states. Punjab in particular has seen accelerating adoption among young professional commuters, and brands have responded with localised financing partnerships and extended warranty programmes to reduce purchase friction.

The India Electric Scooter and Motorcycle Market is moderately concentrated at the top, with the five largest manufacturers collectively accounting for over 90% of total sales volume in FY 2025-26. Legacy ICE-origin OEMs have reclaimed market leadership from earlier EV-native challengers, a shift underpinned by their advantages in manufacturing scale, nationwide service infrastructure, and established brand trust. TVS Motor Company leads with approximately 24.4% market share driven by the iQube family, while Bajaj Auto holds second position at approximately 20.6% through the Chetak range. Ather Energy, the leading pure-play EV manufacturer, holds third at approximately 17.1% with the Ather 450 and Rizta product families.

The competitive landscape has undergone a significant shift in recent years. Ola Electric, which once commanded a dominant 35% share as recently as CY2024, saw its position weaken to approximately 15.6% in CY2025 due to competitive and operational pressures. International brands such as Honda and Suzuki have entered with electric products backed by decades of brand credibility, further intensifying competition across price tiers. Performance-focused specialists including Ultraviolette Automotive and Revolt Motors are carving defensible premium niches. As subsidy dependence declines post-2026, manufacturers with stronger technology pipelines, localised supply chains, and multi-segment product portfolios are expected to consolidate their positions as long-term market leaders.

Founded in 2007 and headquartered in New Delhi, Hero Electric Vehicles is among India's oldest and most experienced electric two-wheeler manufacturers. The company offers a wide portfolio of electric scooters covering both low-speed and high-speed categories, positioned at value-conscious price points suited to first-time EV buyers in Tier-2 and Tier-3 cities. With a distribution network spanning more than 700 dealer touchpoints across India, Hero Electric has prioritised geographic breadth and subsidy eligibility as core competitive pillars. The company faces increasing pressure from better-capitalised rivals offering technologically superior products at comparable price points.

Founded in 2013 and headquartered in Bengaluru, Ather Energy is India's most prominent pure-play electric scooter manufacturer, widely regarded as the technology benchmark in the premium urban commuter segment. Ather produces the 450 family of scooters and the Rizta, a family-oriented product launched in 2024 to broaden its demographic appeal. The company operates its own manufacturing facility at Hosur, Tamil Nadu, and has built a proprietary fast-charging network, Ather Grid, across major Indian cities. In May 2025, Ather announced a technology partnership with Infineon Technologies to integrate SiC and GaN semiconductors into its platforms, enhancing energy efficiency and charging performance.

Founded in 2015 and headquartered in Bengaluru, Ultraviolette Automotive is a technology-forward electric motorcycle company known for the F77, one of India's most advanced and high-performance electric two-wheelers. The company competes in the premium segment with an engineering-first identity, differentiating through battery management technology, aerodynamic design, and software-defined performance tuning. In March 2026, Ultraviolette signed an INR 2 billion expansion MoU with the Karnataka government, committing to a Phase 2 manufacturing facility capable of producing an additional 150,000 units per year, reflecting strong confidence in future demand growth in the performance electric motorcycle category.

Founded in 2020 and headquartered in Mumbai, BGauss Auto is a mid-segment electric scooter manufacturer backed by RR Global, a well-established consumer electronics company with a broad distribution presence across India. The company produces electric scooters in the INR 70,000 to 1,10,000 price range, targeting value-conscious urban buyers who prioritise design quality and reliable after-sales support. BGauss has been actively expanding its dealer footprint across West India and North India, particularly in Maharashtra, Gujarat, Rajasthan, and Punjab, competing on design differentiation and service accessibility as its primary brand levers.

Other key players in the market are Vmoto Limited, Avon Cycles Limited, KLB Komaki Pvt Ltd, BATTREELECTRIC Mobility Private Limited, Joy e-bike Ltd, Ujaas Energy Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead of the curve in one of Asia's most dynamic clean mobility markets. Our comprehensive analysis of the India Electric Scooter and Motorcycle Market 2026 delivers the clarity you need on product innovation pipelines, battery technology shifts, government policy developments, and the fastest-growing regional corridors. Whether you are a manufacturer planning a product launch, an investor evaluating sector positioning, or a strategic planner assessing competitive dynamics, this report gives you the evidence base to act decisively. Download your free sample now and start exploring the opportunities driving India's electric two-wheeler revolution.

Electric Scooter and Motorcycle Market

Three-Wheeled Motorcycle Market

Germany Adventure Motorcycle Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India electric scooter and motorcycle market reached an approximate volume of 1.44 Million Units.

The market is projected to grow at a CAGR of 26.10% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a volume of around 14.64 Million Units by 2035.

Key strategies include aggressive pricing, battery-swapping infrastructure, localized manufacturing, feature-rich smart models, and partnerships with delivery platforms and financing firms to boost accessibility, consumer adoption, and operational efficiency across urban and tier-II markets.

Some of the key trends involve smart connectivity, advanced battery technology, lightweight materials, and performance-driven models.

The major regions in the market are North India, South India, East India and West India.

The various products considered in the market report are scooter and motorcycle.

The various voltages mentioned in the report are 36V, 48V, 60V and others.

The various technologies considered in the market report are battery and plug-in.

The major players in the market are Hero Electric Vehicles Pvt. Ltd, Vmoto Limited, Ather Energy Private Limited, Ultraviolette Automotive Private Limited, Avon Cycles Limited, KLB Komaki Pvt Ltd, BATTREELECTRIC Mobility Private Limited, Joy e-bike Ltd, BGauss Auto Private Limited, Ujaas Energy Limited., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Battery Type |

|

| Breakup by Technology |

|

| Breakup by Volatge |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.