Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

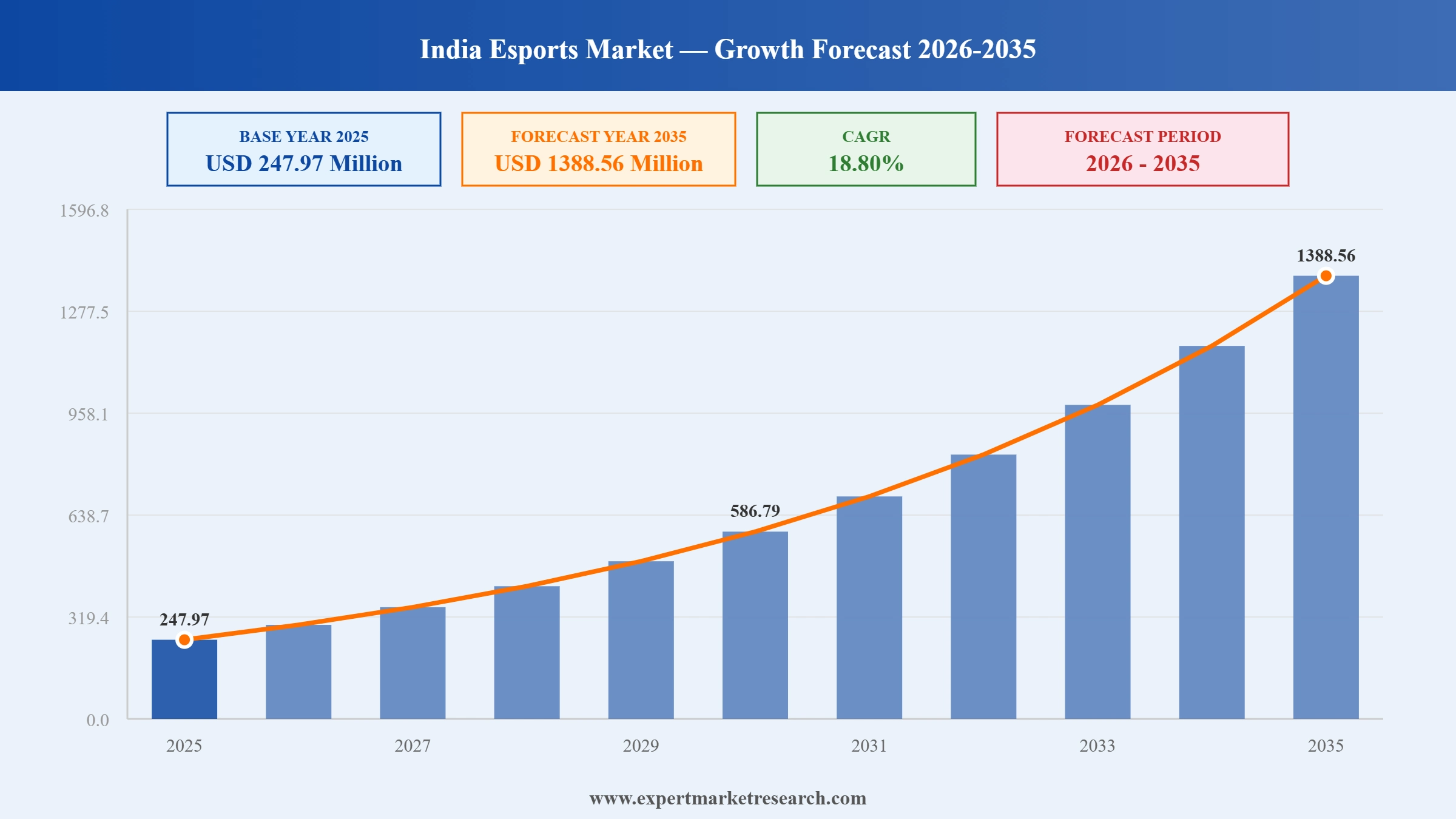

The India Esports Market reached a value of USD 247.97 Million at 2025 and is projected to expand at a CAGR of around 18.80% during the forecast period of 2026-2035. With a rapidly growing mobile-first gaming user base fuelled by affordable devices and low-cost data, expanding brand sponsorship revenue from non-endemic corporates seeking Gen Z engagement, government policy support formalizing esports as a recognized competitive discipline, and widening streaming platform audiences monetizing live and on-demand esports content, the market is expected to reach USD 1388.56 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Esports Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

247.97 |

|

Market Size 2035 |

USD Million |

1388.56 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

18.80% |

|

CAGR 2026-2035 - Market by Region |

South India |

20.7% |

|

CAGR 2026-2035 - Market by Region |

West India |

19.9% |

|

CAGR 2026-2035 - Market by Streaming Type |

Live |

20.6% |

|

CAGR 2026-2035 - Market by Platform |

Mobile and Tablets |

22.1% |

|

2025 Market Share by Region |

South India |

31.2% |

The India esports market is being shaped by mobile-first gaming democratizing competitive participation across Tier 2 and Tier 3 cities, rising non-endemic brand sponsorship transforming revenue models, institutional government recognition formalizing career pathways, expanding live streaming audience monetization, and the emergence of regional esports leagues that bring competitive gaming to new geographies and languages.

NODWIN Gaming secured USD 10 million in funding from existing investors including South Korean gaming giant Krafton and digital entertainment company JetSynthesys in July 2025. The capital is earmarked for expanding NODWIN's esports tournament operations across India, scaling its live event production capabilities, and deepening its publisher partnerships across popular titles including BGMI and CS2. The funding round reflects continued institutional confidence in India's esports growth trajectory and reinforces NODWIN's position as one of the country's most influential tournament organizers and esports infrastructure builders.

Krafton expanded its Battlegrounds Mobile India (BGMI) competitive tournament circuit in 2025, backing events with a combined prize pool of USD 2 million. The investment reflects Krafton's strategic commitment to building a sustainable competitive ecosystem around BGMI following its return to the Indian market, and directly catalyses India's esports market growth by attracting elite grassroots players, increasing media coverage, and raising the overall production value of mobile esports events across the country. BGMI's rapid recovery to over 100 million downloads underscores the title's centrality to India's esports ecosystem.

S8UL, one of India's most prominent esports organizations and content creation teams, was selected as a Club Partner for the Esports World Cup 2025, one of the largest and most prestigious international esports events in the world. The partnership gave S8UL direct representation and branding rights at the tournament, elevating India's visibility on the global esports stage and creating a pathway for Indian gaming talent to compete at international levels. The selection validates India's growing stature as a competitive esports nation and strengthens the case for continued investment in domestic talent development.

CyberPowerPC partnered with Orangutan Esports to launch ApeCity in 2025, branded as India's first professional esports arena led by an esports organization, located in Navi Mumbai. The venue is equipped with high-performance gaming PCs, PlayStation consoles, and a Sim Racing setup, designed to serve competitive gamers, content streamers, and professional esports athletes. The development represents a step change in India's physical esports infrastructure, shifting from informal gaming cafes toward purpose-built professional competitive venues that can host live audience events, brand activations, and streaming productions.

The Skyesports Masters League attracted Hyundai and Intel as brand sponsors in early 2025, marking a significant expansion in non-endemic corporate participation in Indian esports. These partnerships go beyond basic event logos, encompassing branded content production, influencer integration, and regional audience targeting that brands use to reach India's 500 million-plus mobile gaming demographic. The involvement of automotive and semiconductor brands reflects how mainstream corporate India is now treating esports as a viable and credible platform for youth engagement, fundamentally strengthening the sponsorship revenue model across the domestic esports economy.

India's esports ecosystem is fundamentally mobile, with over 90% of esports participation occurring through smartphones rather than PCs or consoles. Titles like BGMI and Free Fire have created massive competitive communities in cities, towns, and even semi-rural areas where gaming café infrastructure is limited but smartphone ownership and 4G connectivity are widespread. The India esports market growth is structurally tied to this mobile accessibility: affordable devices costing under USD 150, sub-USD 0.20/GB data costs, and a population where over 65% are under 35 have created a competitive gaming ecosystem of unprecedented scale. In 2025, Krafton's expanded BGMI tournament circuit with USD 2 million in prize pools cemented mobile esports as the primary competitive format, attracting millions of grassroots participants and driving viewership on platforms including YouTube Gaming and Rooter.

Sponsorship is the dominant revenue stream in India's esports market, and the fastest-evolving one. The shift in 2024-2025 has been the entry of non-endemic brands, companies with no direct gaming product, into tournament and team sponsorships. Hyundai and Intel co-sponsored the Skyesports Masters League in early 2025, while PepsiCo, Red Bull, and Flipkart have partnered with esports events for co-branded marketing campaigns targeting India's Gen Z consumer base. Ernst and Young projected tournament sponsorship and syndication revenue would reach approximately USD 47 million by 2025. These brand commitments are not one-off experiments; they reflect strategic decisions to allocate youth marketing budgets to esports as a premium channel for sustained engagement with a demographic that is largely unreachable through traditional advertising media.

India's government formally recognized esports as a multi-sport event discipline under the Ministry of Youth Affairs and Sports in December 2023, a landmark decision that allowed esports players to access Sports Authority of India infrastructure, Khelo India funding, and training support equivalent to Olympic athletes. In 2025, this policy foundation produced tangible institutional outcomes: the Association of Indian Universities (AIU) launched its inter-university esports championship, Rajasthan introduced the State Esports Championship (RSEC) 2025 with BGMI and CS2 competition tracks, and universities including Lovely Professional University established esports curriculum electives. These developments are building a generation of players and industry professionals through accredited pathways rather than informal routes, fundamentally strengthening the talent pipeline for teams, tournament organizers, and streaming platforms.

Live and on-demand streaming is becoming a significant and fast-growing monetization layer in India's esports economy. Platforms including YouTube Gaming, Rooter, and Loco are competing for esports content rights, investing in production quality, and developing subscription and virtual gifting revenue models that directly share income with tournament organizers and content creators. The live streaming segment benefits from India's extraordinary mobile viewing behavior, with millions of fans watching matches on phones during commutes and breaks. In July 2025, NODWIN Gaming's USD 10 million funding raise specifically targeted expanding its tournament production capabilities for both live and digital audiences, recognizing that broadcast quality and platform reach are now as commercially important as the competitive format itself in determining a tournament's sponsorship value and viewership numbers.

The Expert Market Research's report titled "India Esports Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

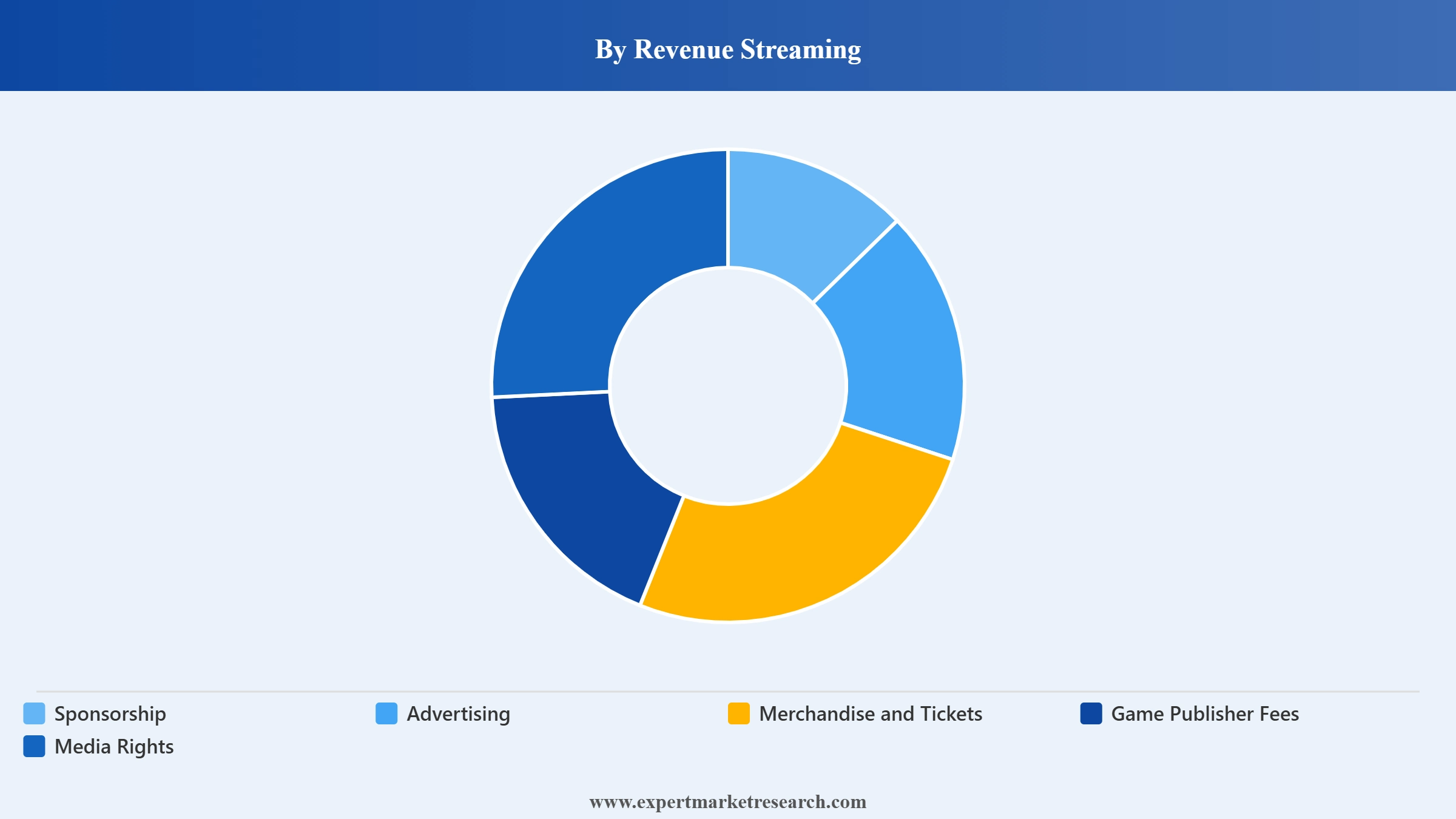

Market Breakup by Revenue Streaming

Key Insight: Sponsorship is the dominant revenue stream in India's esports market, driven by surging non-endemic brand participation and a competitive brand landscape where companies from automotive, food and beverage, technology, and FMCG sectors are allocating dedicated youth engagement budgets to esports events and team partnerships. Advertising revenue is closely linked to streaming growth, with in-stream brand placements on YouTube Gaming, Rooter, and Loco generating views-based revenue that scales with viewer numbers. Media rights is the fastest-growing revenue stream as tournament organizers and streaming platforms negotiate exclusive broadcast deals, a trend expected to accelerate as esports audience figures approach mainstream sports viewership benchmarks in India.

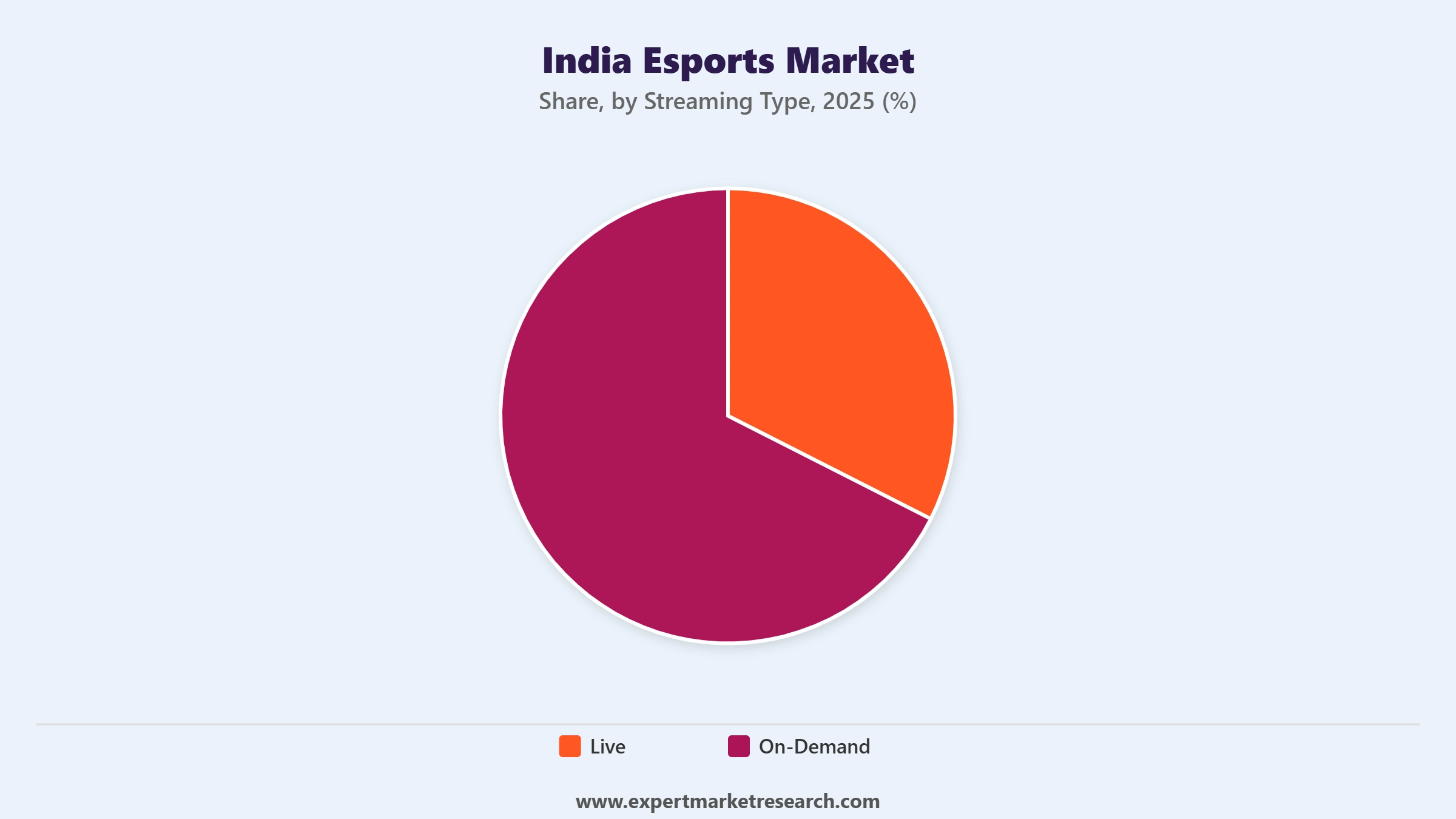

Market Breakup by Streaming Type

Key Insight: Live streaming is the dominant format in India's esports market, capturing the highest engagement from fans who follow real-time tournament matches on mobile devices and value the communal, event-driven experience of watching competitive play unfold. Live events drive peak advertising rates and virtual gifting revenue, making them the primary monetization anchor for platforms. On-demand streaming is growing strongly as short-form highlight content and full match replays attract casual viewers who cannot commit to full live broadcasts, extending the content lifecycle of tournament events and creating new discovery pathways for brands and teams seeking to build audience relationships beyond live event windows.

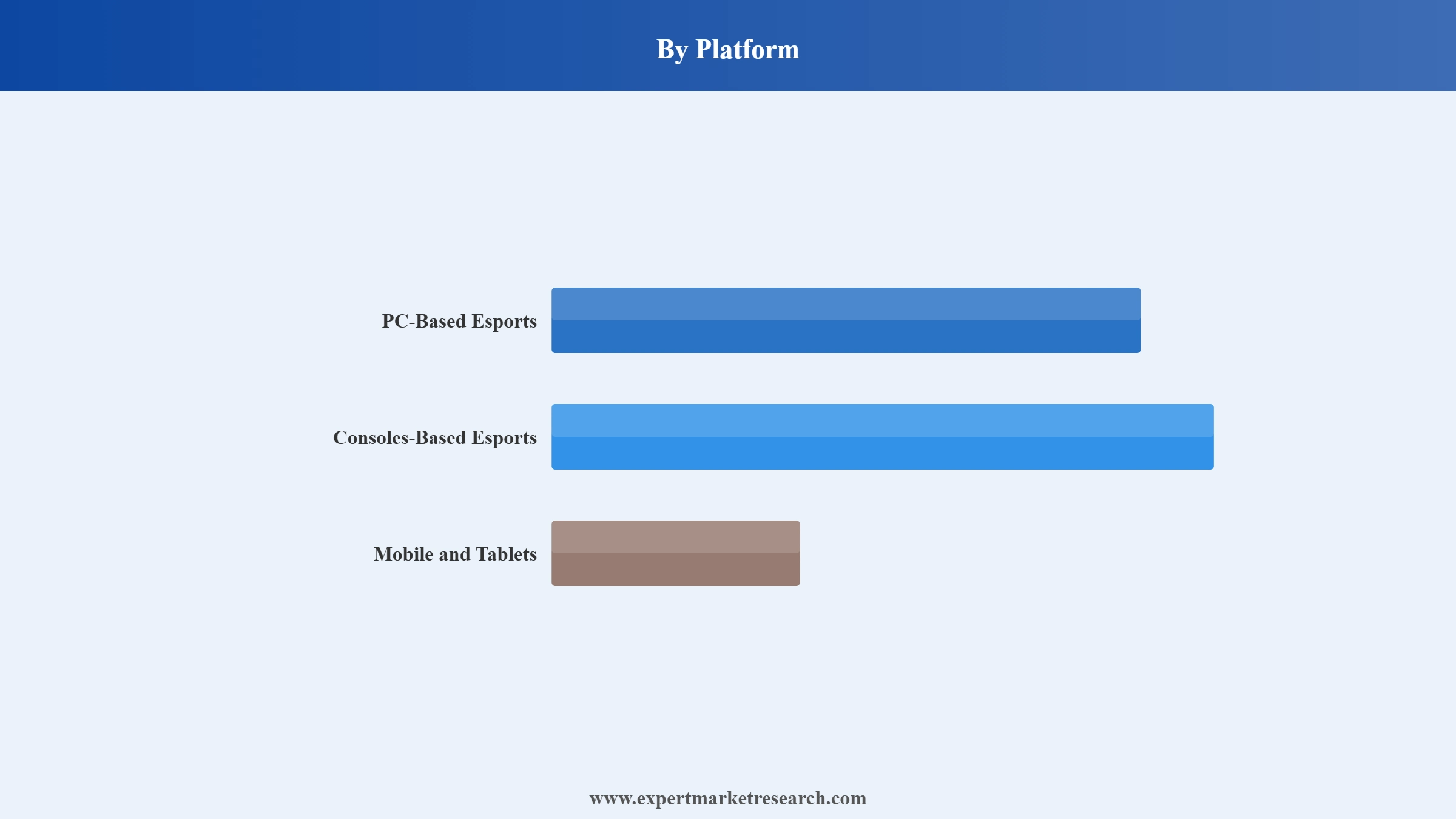

Market Breakup by Platform

Key Insight: Mobile and tablets dominate India's esports platform landscape with approximately 62% market share, underpinned by the country's mobile-first internet culture, mass smartphone ownership, and the competitive ecosystem around titles including BGMI and Free Fire that operate at high levels with relatively modest hardware requirements. The Mobile and Tablets segment is projected at a CAGR of 22.1%, the fastest among all platforms. PC-based esports caters primarily to the urban market through gaming cafes and college setups, with titles including Valorant and CS2 gaining ground. Console-based esports is the fastest-growing niche segment by growth rate, benefiting from declining console prices and urban café integration, particularly around FIFA and Call of Duty competitive formats.

Market Breakup by Region

Key Insight: South India leads the India esports market, with Bengaluru and Hyderabad functioning as key esports hubs due to their concentration of technology professionals, gaming café infrastructure, and active college esports communities. The region also benefits from strong state-level government interest in digital sports and the presence of major game development studios and esports organizations. North India is a significant and fast-growing market, with Delhi-NCR driving viewership and tournament participation through dense urban populations and a rising college esports culture. West India, particularly Mumbai and Pune, is emerging as the country's esports infrastructure capital, housing new venues like ApeCity in Navi Mumbai and attracting brand partnerships through proximity to India's marketing and media industry headquarters.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Sponsorship holds the commanding share of India's esports revenue, a position that reflects the market's current commercial maturity stage where brands are the primary monetization engine rather than consumer direct spending. Non-endemic brand involvement is particularly notable: automotive brands, food and beverage companies, and technology hardware makers are all committing multi-year sponsorship agreements that include event naming rights, team jerseys, digital content co-creation, and product placements within esports broadcast environments. The Ernst and Young estimate of approximately USD 47 million in tournament sponsorship and syndication revenue by 2025 indicates the scale of commercial investment flowing into India's esports event calendar annually.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Mobile and tablets holds the dominant platform share, and the gap between mobile esports and PC/console esports is wider in India than virtually any other significant global market. The 2025 return of Free Fire to the Indian market alongside BGMI's continued growth have reinforced this dominance, collectively providing two flagship mobile esports titles that serve different competitive skill thresholds and regional player demographics. For brands, mobile platforms offer the most scalable reach, connecting sponsors to potential audiences that number in the hundreds of millions. For tournament organizers like NODWIN Gaming and Skyesports, mobile titles offer the broadest grassroots participation base, enabling qualifying pathways from rural Tier 3 towns all the way to national championship finals in major metros.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By streaming type, live viewing drives the highest commercial value per viewer through real-time engagement metrics that brands prize for brand recall and community sentiment building. South India's regional leadership in the market is reinforced by Bengaluru's role as India's technology capital, which creates natural density for both gaming talent and corporate sponsors who can activate locally. North India's growth is creating new sponsorship inventory as regional leagues expand into Delhi-NCR, Lucknow, and Chandigarh, giving brands geographic diversification across India's esports audience.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India's leadership in the India esports market stems from the region's concentration of technology professionals, digital-native youth populations, and established gaming infrastructure in Bengaluru and Hyderabad. These cities function as commercial esports hubs where brands, studios, and tournament organizers cluster, creating a density of activity that drives sponsorship deals, production investments, and talent development at a scale not yet replicated elsewhere. Tamil Nadu and Andhra Pradesh also contribute significant participation volumes from their large youth populations, with regional language esports content in Tamil generating strong platform engagement and creating brand activation opportunities for sponsors reaching non-English speaking gaming communities. State government interest in esports as a digital economy pillar is increasingly visible, with infrastructure support and championship programs formalizing South India's leading position.

North India is the market's most commercially dynamic growth region, with Delhi-NCR functioning as the convergence point of India's marketing industry and its highest urban gaming density. Brands that want to activate esports sponsorships work through agencies and event organizers headquartered in the capital, making the north the natural commercial hub for deal-making. The AIU inter-university esports championship, which drew participation from colleges across North India in 2025, reflects the deepening institutional roots of competitive gaming in the region. Beyond Delhi, cities including Lucknow, Chandigarh, and Jaipur are seeing rapid expansion of gaming cafe infrastructure and organized esports participation, driven by rising youth disposable income and the rollout of affordable 5G connectivity that reduces mobile gaming latency and opens new competitive play formats.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's esports market is moderately fragmented, with a small number of large, established tournament organizers and esports management companies competing alongside a growing ecosystem of regional teams, streaming-focused organizations, and technology platform players. NODWIN Gaming and Skyesports are the two most prominent tournament organizers by scale and geographic reach, while team organizations including Revenant Esports and S8UL have built significant fan bases through both competitive performance and content creation. Global technology companies including NVIDIA and international esports holding groups like Modern Times Group are also active in India's market, either through hardware partnerships or investment in local organizations.

The competitive differentiation axes in India's esports market are shifting. Raw tournament hosting capability was previously the primary measure of market position; increasingly, the ability to drive viewership, monetize streaming audiences, execute brand partnership activations at scale, and develop grassroots talent pipelines are becoming equally critical. Organizations with strong creator economies alongside competitive team operations, like S8UL, have discovered that content monetization can rival or exceed tournament prize pool-related revenues, reshaping how esports organizations think about their commercial models.

Skyesports is one of India's leading independent esports tournament organizers, known for running regionally focused competitions in local languages including Tamil, Hindi, and Bengali with relatively accessible entry requirements that broaden grassroots participation beyond metro markets. The organization has operated national leagues including the Skyesports Masters League and has attracted brand sponsors including Hyundai and Intel. Skyesports' strategy of combining accessible grassroots pathways with professional production quality for top-tier events has made it a key talent discovery and brand activation platform in India's esports ecosystem.

NODWIN Gaming is among the most influential esports companies in India, operating as a tournament organizer, content producer, and esports infrastructure developer. The company secured USD 10 million from Krafton and JetSynthesys in July 2025 to expand its operations, and has established partnerships with publishers, streaming platforms, and hardware brands for major events including the iQOO Battleground Series. NODWIN's role as the esports partner for the India Gaming Show 2025 and its participation in WAVES 2025 in Mumbai reflect its positioning at the intersection of India's gaming industry, entertainment sector, and digital economy.

Revenant Esports is a professionally managed Indian esports team organization competing across multiple game titles including BGMI, Free Fire, and Valorant. The organization competes at national and regional championship levels and has built a social media following among India's competitive gaming community. Revenant focuses on talent identification, player development, and building team brand equity through both competitive results and digital content creation, positioning itself as a team brand rather than purely a competitive entity in India's increasingly monetization-focused esports landscape.

Founded in 1993 and headquartered in Santa Clara, California, NVIDIA is the world's leading GPU manufacturer and a significant technology partner in India's esports ecosystem. NVIDIA's GeForce hardware powers the majority of PC-based esports setups in India, from casual gaming cafes to professional tournament infrastructure. The company actively sponsors esports events and gaming competitions in India, using the market to drive awareness of its consumer gaming products among India's young demographic. NVIDIA's partnerships with tournament organizers and its GeForce gaming platform give it direct influence over India's PC and console esports segments.

Other key players in the market are G Esports Holding GmbH, MODERN TIMES GROUP, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Capture India's explosive esports opportunity with our detailed India Esports Market report for 2026 to 2035. With the market projected to exceed USD 1 billion within the decade, backed by a mobile-first gaming population of hundreds of millions, rising brand sponsorship budgets, and formal government support for competitive esports as a career, the window to establish strategic positions is open right now. Whether you are a brand planning audience engagement, a technology company seeking hardware partnerships, a streaming platform building content rights, or an investor evaluating the sector, this report delivers the intelligence you need. Download your free sample today and explore what is driving India's thriving esports industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India esports market reached an approximate value of USD 247.97 Million.

The market is projected to grow at a CAGR of 18.80% between 2026 and 2035.

The key players in the market include Jet Skyesports Gaming Private Limited, NODWIN Gaming Pvt. Ltd., Revenant Esports Private Limited, G Esports Holding GmbH, NVIDIA Corporation,and MODERN TIMES GROUP, among others.

The mobile and tablets platform is gaining traction and anticipated to expand with a 22.1% CAGR through 2035.

Key strategies include localization of content, mobile-first gaming ecosystems, grassroots tournament development, influencer-led marketing, publisher partnerships, and investments in streaming infrastructure to tap into India’s rapidly growing digital-native gaming audience.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Revenue Streaming |

|

| Breakup by Streaming Type |

|

| Breakup by Platform |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.