Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

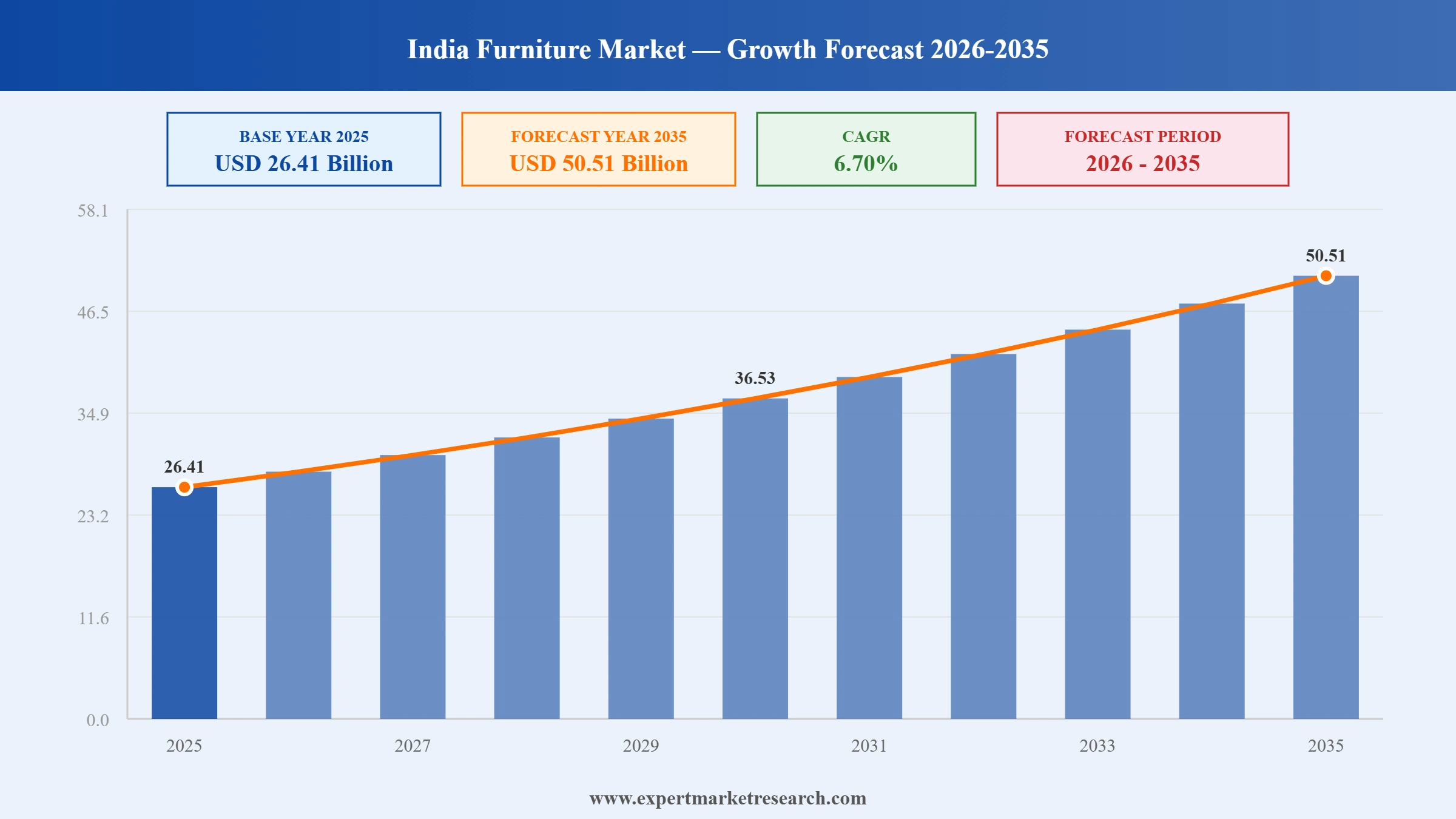

The India furniture market reached a value of USD 26.41 Billion at 2025 and is projected to expand at a CAGR of around 6.70% during the forecast period of 2026-2035. With rapid urbanisation driving demand for modern residential and commercial furniture, strong growth in India's real estate and hospitality sectors, rising penetration of organised retail and e-commerce platforms expanding market access, and increasing consumer preference for modular and customisable furniture designs, the market is expected to reach USD 50.51 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India furniture market is entering a phase of accelerated formalisation, driven by rising foreign direct investment, the scaling of organised retail networks, and growing consumer preference for branded, quality-assured products over unorganised local manufacturers. Global and domestic players are deepening their omnichannel strategies, combining physical showrooms with digital customisation tools, while government manufacturing incentives under Make in India are expanding domestic production capacity and supporting India's emergence as a furniture export hub.

In January 2026, IKEA announced plans to more than double its cumulative investment in India to approximately USD 2.2 billion over the next five years, targeting accelerated store expansion, stronger digital commerce capabilities, and increased local sourcing. The commitment confirmed India's status as a priority growth market for the global furniture leader and reinforced competitive pressure on domestic players in the India furniture market.

In September 2025, Godrej Interio announced a INR 300 crore investment to accelerate its retail and manufacturing expansion, targeting INR 10,000 crore in revenue by FY2029 and a retail footprint of approximately 1,500 outlets. The commitment reinforced Godrej Interio's ambition to defend its domestic leadership position against both global entrants and fast-scaling DTC brands in the India furniture market.

In August 2025, IKEA India inaugurated its first Delhi-area store at Pacific Mall, Tagore Garden, spanning 15,000 square feet and offering over 2,000 home furnishing products. The Delhi entry opened access to one of India's highest-spending urban furniture markets and reinforced IKEA's multi-city physical retail strategy alongside its growing online presence.

In January 2025, Godrej Interio launched UPMODS, a unique furniture line designed for the evolving demands of modern Indian consumers with upgradability and customisation features. The range set a new benchmark in furniture ownership flexibility and addressed growing consumer preference for adaptive, long-lasting furniture in urban homes across the India furniture market.

Rapid urbanisation and India's expanding housing sector underpin the India furniture market's growth trajectory. Government programmes targeting affordable housing and the strong performance of Tier 1 and Tier 2 urban real estate markets are generating consistent demand for residential furniture, while office absorption forecasts of 65 to 70 million square feet for 2025 drive commercial furniture procurement.

Online retail is the fastest-growing distribution channel in the India furniture market, supported by platforms including Pepperfry, Urban Ladder, Amazon, and Flipkart. In June 2025, Pepperfry raised INR 430 million from existing investors for studio expansion, confirming the hybrid model combining digital discovery with physical touchpoints as the preferred growth strategy for furniture retailers.

India's furniture market is shifting steadily from unorganised local manufacturers toward branded and organised players as consumers in urban markets prioritise quality, warranties, and design consistency. The government's 51% FDI allowance in multi-brand retail has accelerated international entry, while domestic brands including Nilkamal and Wakefit are scaling their organised retail footprint across tier-2 cities.

India's furniture export potential is driving investment in manufacturing quality upgrades aligned with international standards. Jodhpur and Saharanpur craft clusters are increasingly supplying premium wooden furniture to the US, UK, and GCC markets. Growing environmental awareness is also pushing manufacturers toward sustainable wood sourcing and recycled material integration in the India furniture market.

India's hospitality sector expansion, driven by domestic tourism growth and international hotel brand entries into Tier 2 cities, is generating meaningful demand for commercial-grade furniture in the India furniture market. Hotel chains and co-working operators are procuring large volumes of modular, durable, and easily reconfigurable furniture from organised domestic suppliers and IKEA.

The report by Expert Market Research's titled "India Furniture Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

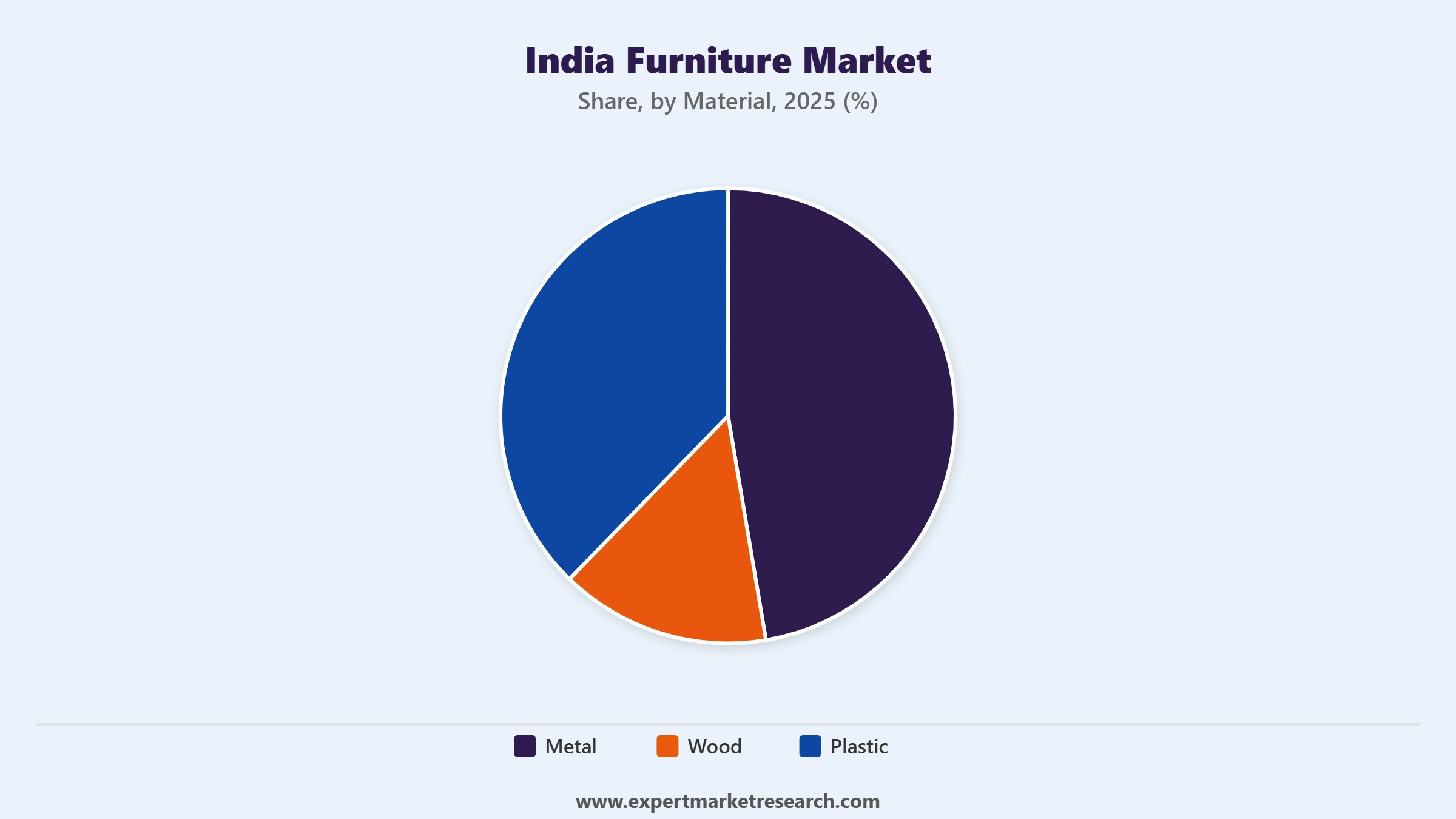

Market Breakup by Material

Key Insight: Wood dominates the India furniture market by material, accounting for approximately 62% of market revenue in 2025, driven by cultural preference for handcrafted wooden furniture, the legacy craft clusters of Saharanpur and Jodhpur, and the premium positioning of solid and engineered wood products. Metal furniture serves institutional and commercial segments, while plastic furniture from companies like Nilkamal and Supreme Industries addresses the mass-market, price-sensitive residential and commercial demand.

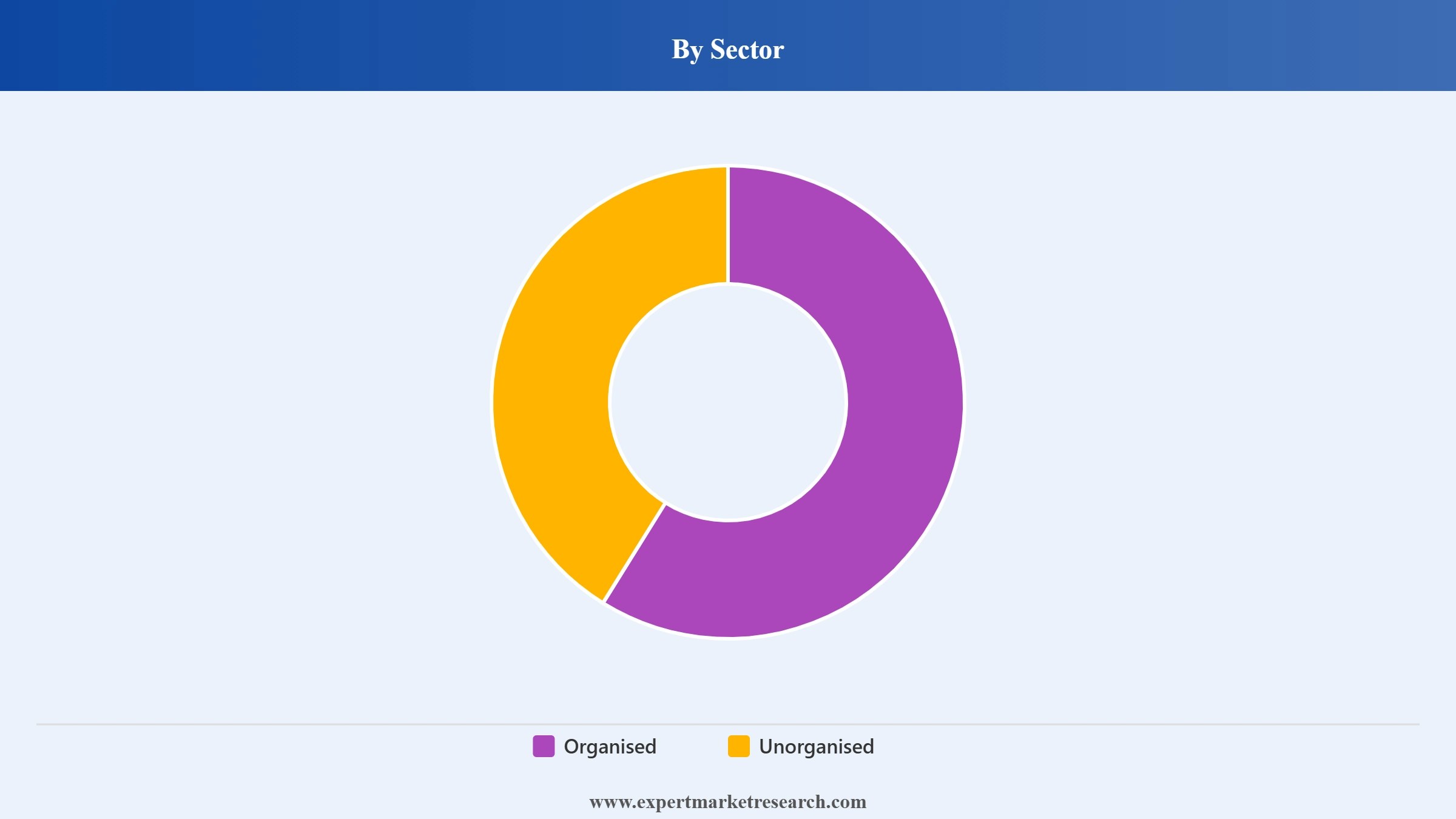

Market Breakup by Sector

Key Insight: The unorganised sector still commands a larger share of the India furniture market by unit volume, serviced by millions of small local carpentry and furniture-making units. However, the organised sector is the faster-growing segment, scaling through branded retail chains, e-commerce platforms, and factory-made ready-to-assemble products. FDI liberalisation and growing consumer preference for quality assurance and after-sales service are accelerating the structural shift from unorganised to organised supply.

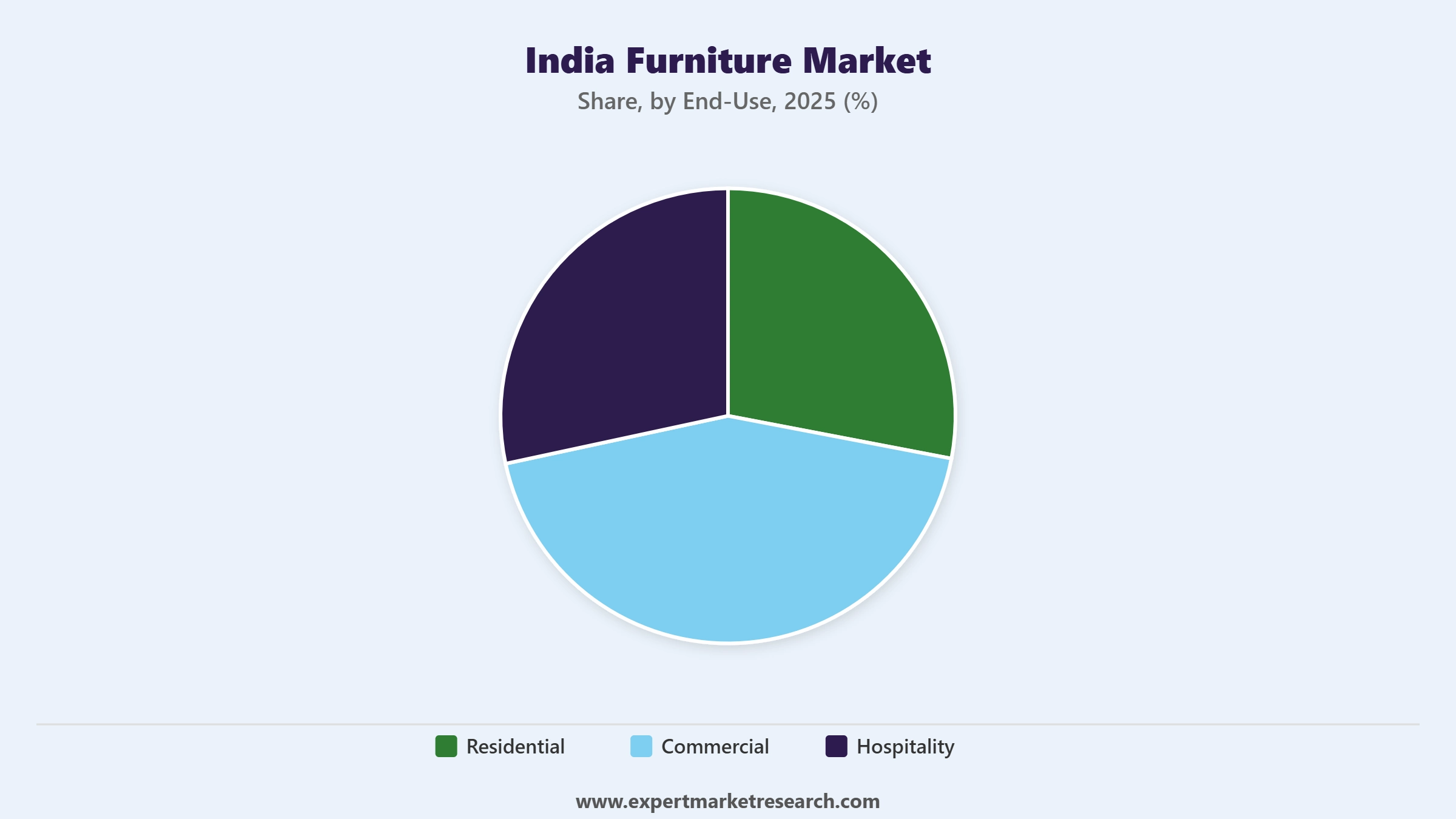

Market Breakup by End-Use

Key Insight: Residential end-use dominates the India furniture market, driven by housing construction growth, rising home improvement spending, and the cultural emphasis on home aesthetics among India's expanding middle class. Commercial furniture is the fastest-growing segment, propelled by office absorption activity in technology hubs including Bengaluru, Hyderabad, and Pune. Hospitality is a growing niche driven by hotel brand expansion and co-working space proliferation.

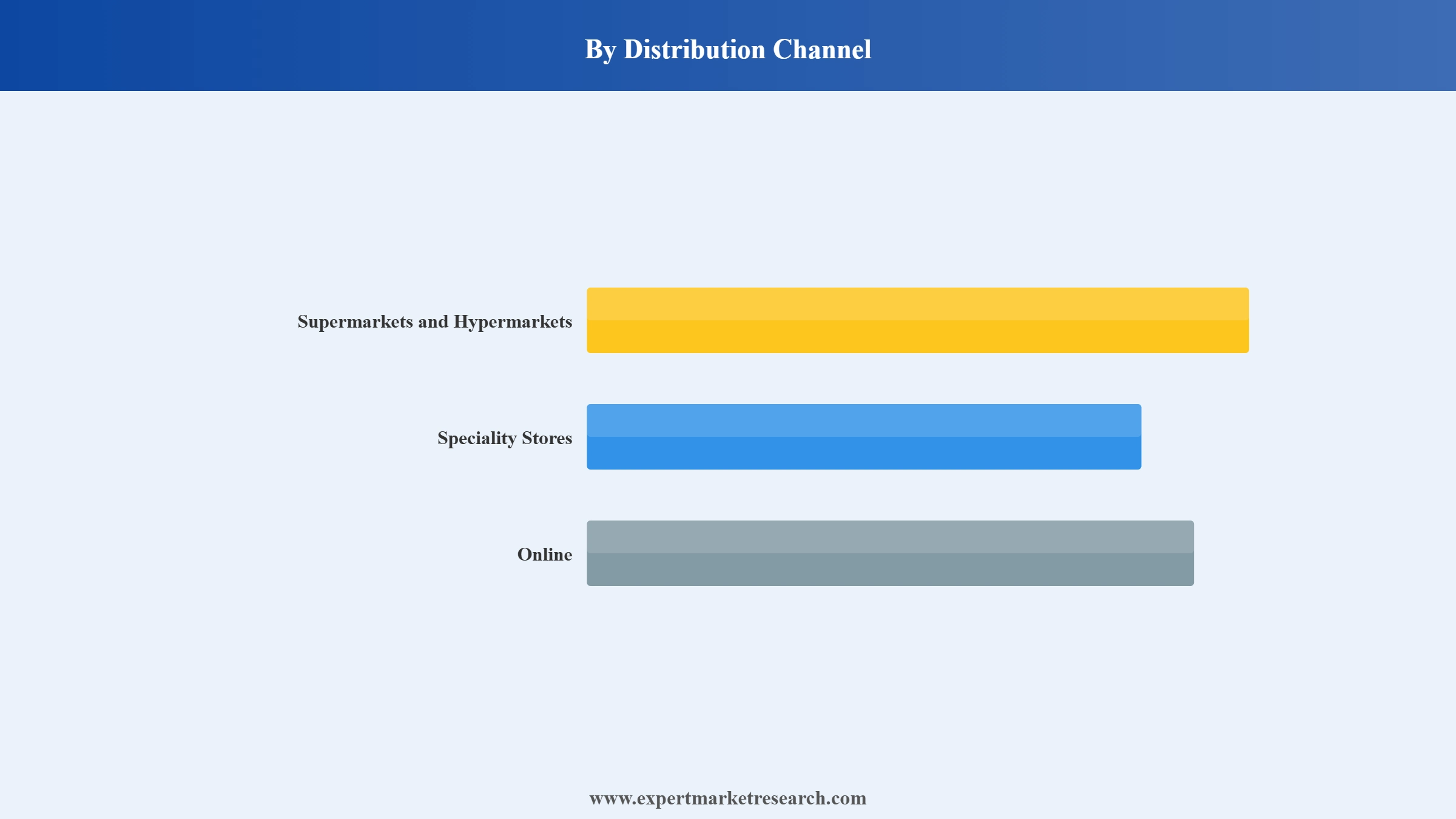

Market Breakup by Distribution Channel

Key Insight: Speciality stores hold the largest share of the India furniture market distribution landscape, as dedicated furniture showrooms from Godrej Interio, IKEA, Durian, and Zuari provide the experiential purchasing environment consumers prefer for high-value furniture decisions. Online is the fastest-growing channel, with platforms like Pepperfry and Urban Ladder combining curated product assortments with home delivery and EMI financing. The hybrid physical-plus-digital model is becoming the competitive standard for organised players.

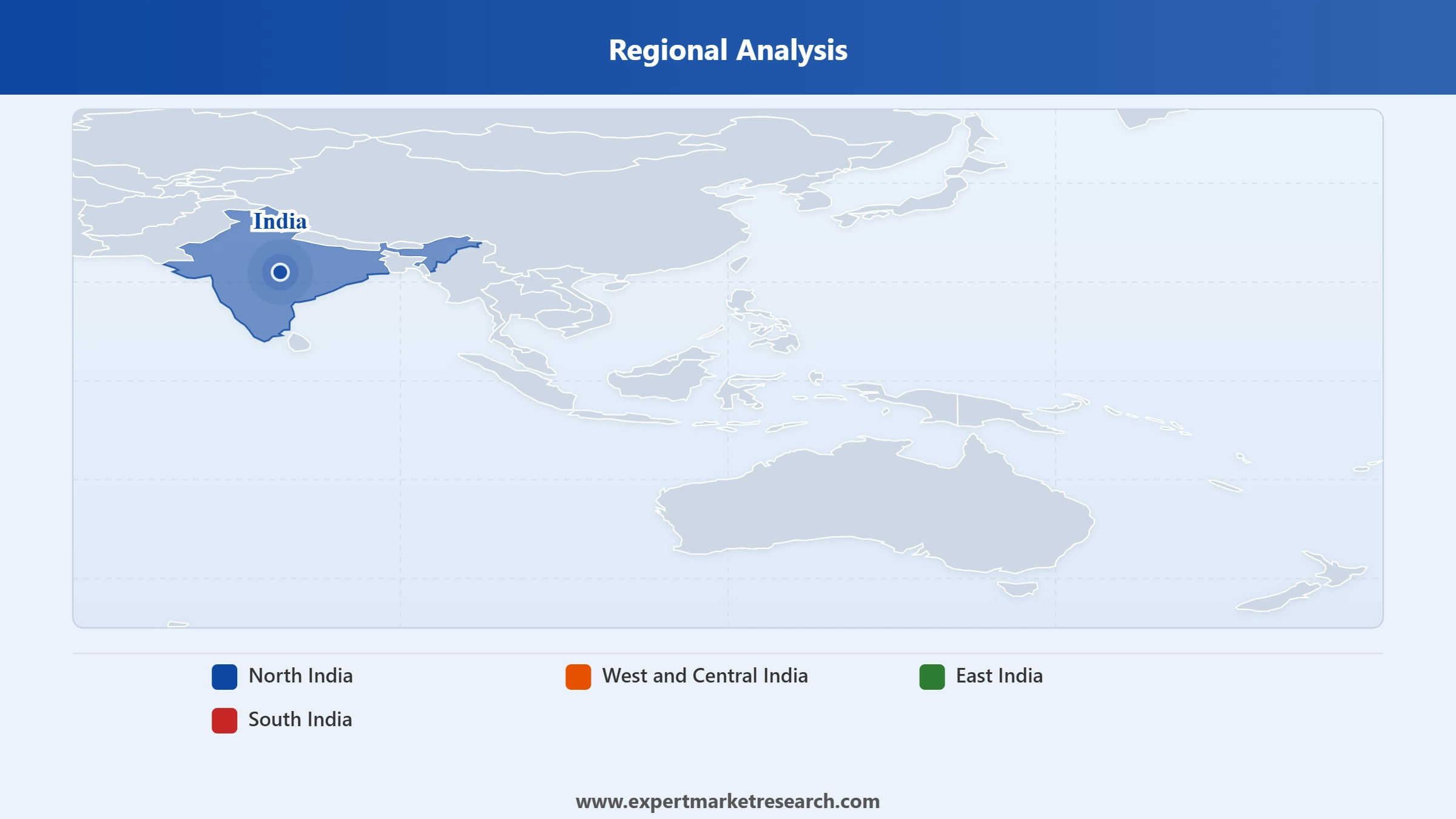

Market Breakup by Region

Key Insight: North India is the largest regional market for furniture in India, led by Delhi NCR's high-density urban population, strong consumer spending, and proximity to the Saharanpur and Jodhpur craft manufacturing clusters. West and Central India holds a strong secondary position driven by Mumbai's premium residential market and Pune and Ahmedabad's corporate demand. South India is the fastest-growing region, fuelled by Bengaluru's technology sector activity and Chennai's export-manufacturing base.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By material, wood accounts for the dominant share of the market due to cultural preference and established craft manufacturing heritage

Wood dominates the India furniture market by material, holding approximately 62% of revenues in 2025. Consumer preference for handcrafted and aesthetically superior wooden furniture is deeply rooted in India's design culture, and the established craft manufacturing clusters of Saharanpur, Jodhpur, and Jaipur provide a scalable supply base. Both solid wood and engineered wood variants serve different price tiers, ensuring wood-based furniture spans mass-market, mid-tier, and premium segments.

Metal furniture is growing steadily in commercial and institutional applications, particularly in the office, hospitality, and industrial sectors where durability and easy maintenance are priorities. Plastic furniture, manufactured at scale by Nilkamal and Supreme Industries, holds a stable share in price-sensitive residential and outdoor segments. In January 2025, Godrej Interio launched the UPMODS line with flexible material combinations, reflecting the growing trend toward composite and modular furniture in the India market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By sector, the unorganised sector accounts for the dominant share of the market by volume while the organised sector grows fastest

The unorganised sector commands the majority of unit volume in the India furniture market, served by a large network of local carpenters and small-scale manufacturers that have historically met the needs of price-sensitive rural and semi-urban consumers. These producers offer highly customised, site-fabricated furniture at competitive prices, and their informal distribution model has been entrenched across non-metropolitan India for decades.

The organised sector is growing faster, driven by branded retailers including IKEA, Godrej Interio, and Wakefit that offer standardised quality, design variety, and after-sales support. In January 2026, IKEA's USD 2.2 billion India investment commitment accelerated the organised sector's geographic and channel expansion. Government FDI liberalisation and growing consumer quality consciousness are steadily shifting share from unorganised to branded organised players in the India furniture market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By end-use, residential accounts for the dominant share of the market due to housing construction growth and rising home improvement spending

Residential end-use leads the India furniture market, driven by a growing housing stock supported by government affordable housing programmes, rising urban household income, and a cultural emphasis on home aesthetics. The expanding Indian middle class, projected to reach 583 million people, is investing more in stylish, functional home furniture as a reflection of lifestyle aspirations. Ready-to-assemble and modular furniture formats are gaining share among urban apartment dwellers seeking efficient space utilisation.

Commercial end-use is the fastest-growing segment, fuelled by office absorption of 65 to 70 million square feet forecast in 2025, coworking operator growth, and IT park expansion across Bengaluru, Hyderabad, and Pune. Ergonomic workstations, modular collaboration spaces, and smart furniture with embedded sensors are gaining traction among corporate buyers. In September 2025, Godrej Interio's INR 300 crore expansion commitment included targeted investment in commercial segment capabilities across the India furniture market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By distribution channel, speciality stores account for the dominant share of the market due to the experiential value of in-store furniture purchasing

Speciality stores are the dominant distribution channel in the India furniture market, as consumers prefer to assess furniture quality, dimensions, and aesthetics in person before committing to large purchases. Godrej Interio's network targeting 1,500 outlets by 2029, IKEA's growing store footprint, and Durian's multi-city showroom model all reinforce the speciality store channel's importance. The format enables upsell, cross-sell, and personalisation that online platforms replicate less effectively.

Online is the fastest-growing channel, transforming how younger and tech-savvy consumers discover and purchase furniture. Pepperfry and Urban Ladder lead the digital-first approach, combining online catalogues with physical studios for touch-and-feel validation. In August 2025, IKEA India's new Delhi store at Pacific Mall complemented its robust online presence, illustrating how hybrid omnichannel strategies are becoming the competitive default for organised players in the India furniture market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India dominates the market due to high population density, strong consumer spending, and proximity to craft manufacturing clusters

North India leads the India furniture market, commanding the largest regional share driven by Delhi NCR's high-density urban population and strong consumer spending power. Proximity to India's two largest furniture craft manufacturing clusters in Saharanpur, Uttar Pradesh, and Jodhpur, Rajasthan, provides North Indian retailers with cost and supply chain advantages. The region's dense residential and commercial construction pipeline sustains consistent furniture demand across residential, institutional, and hospitality segments.

South India is the fastest-growing regional market, propelled by Bengaluru's position as India's technology capital generating strong commercial furniture demand and Chennai's manufacturing-sector growth. In August 2025, IKEA India's Delhi store opening signalled expanding physical retail activity across major regional hubs, while Bengaluru remained the most active market for D2C furniture brands targeting young professionals. South India's office absorption rate and rising middle-class incomes are key structural drivers of the India furniture market in the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India furniture market is moderately fragmented, combining legacy domestic conglomerates such as Godrej Interio and Nilkamal with global entrants including IKEA and fast-scaling digital-native brands like Wakefit. Competition is shifting from pure price rivalry toward quality, design, brand experience, and omnichannel accessibility as consumers in urban India become more sophisticated.

Organised players are investing heavily in retail network expansion, manufacturing capacity, and digital commerce capabilities. International brands leverage global supply chains and design heritage to compete at the premium end, while Indian players such as Godrej Interio and Durian compete on heritage trust, local customisation, and after-sales service depth. The market's ongoing formalisation is raising competitive stakes across all segments.

Headquartered in Mumbai and a flagship of the Godrej Group, Godrej and Boyce manufactures furniture, appliances, and security solutions under the Godrej Interio brand. In September 2025, Godrej Interio announced a INR 300 crore investment targeting INR 10,000 crore revenue by FY2029 and 1,500 retail outlets, cementing its ambition to lead the organised India furniture market through network scale and product innovation.

Founded in 1943 and headquartered in Delft, Netherlands, IKEA is the world's largest furniture retailer operating in India through Inter IKEA Systems B.V. In January 2026, IKEA committed to more than doubling its India investment to USD 2.2 billion, targeting accelerated store expansion, digital capability strengthening, and local sourcing. Its August 2025 Delhi store opening marked a major milestone in reaching India's largest urban furniture market.

Founded in 2016 and headquartered in Bengaluru, Wakefit is a direct-to-consumer home solutions brand offering mattresses, furniture, and home furnishings online and through physical studios. Its data-driven inventory model, competitive pricing, and rapid fulfilment capabilities have made it one of India's fastest-scaling organised furniture brands, particularly among urban millennials seeking affordable quality in the India furniture market.

Founded in 1981 and headquartered in Mumbai, Nilkamal is one of India's largest plastic furniture manufacturers and a leading organised retail operator under its at-home format. With over 20,000 dealer outlets, Nilkamal commands unmatched distribution reach across urban and semi-urban India, competing on affordability, product range, and supply chain scale in the mass-market India furniture segment.

Other key players in the market are Cello World Private Limited, Zuari Furniture, Durian Industries Limited, Usha Shriram Enterprises Pvt. Ltd., Damro Furnitures Pvt. Ltd., Supreme Industries Ltd., Wipro Furniture Private Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock comprehensive intelligence on the India furniture market with our latest research report. Understand how urbanisation, IKEA's investment commitment, organised sector growth, and regional expansion are reshaping competitive dynamics from North to South India. Whether you are a furniture manufacturer, retailer, e-commerce platform, material supplier, or investor, this report provides the data and strategic insight to drive your decisions. Download your free sample today and explore the key opportunities in India's furniture industry.

Mexico Office Furniture Market

Brazil Furniture Market

United States Furniture Market

Vietnam Home Furniture Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The furniture market in India reached an approximate value of USD 26.41 Billion in 2025

The market is estimated to grow at a CAGR of 6.70% between 2026 and 2035.

The major drivers of the industry, such as the increased investments in the infrastructure development activities, rising population, increased demand for home-office set up essentials, rising disposable incomes, and improved living standards of consumers, are expected to aid the market growth.

The key trends aiding the market include the growing demand for sustainable furniture materials, the rising trend of minimalism, the growing popularity of vintage and antique furniture, and the increased integration of smart technology into furniture.

The major regions in the industry are North India, East India, West India, and South India.

The significant raw materials include metal, wood, plastic, and others.

The major sectors include organised and unorganised.

The different end uses include residentials, commercial offices, hotels/restaurants, and others.

The major distribution channels include supermarkets and hypermarkets, speciality stores, online, and others.

The major players in the market are Godrej & Boyce Manufacturing Company Limited, Inter IKEA Systems B.V., Wakefit Innovations Pvt. Ltd, Nilkamal Limited, Cello World Private Limited, Zuari Furniture, Durian Industries Limited, Usha Shriram Enterprises Pvt. Ltd., Damro Furnitures Pvt. Ltd., Supreme Industries Ltd., and Wipro Furniture Private Limited, among others.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 50.51 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material |

|

| Breakup by Sector |

|

| Breakup by End-Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.