Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

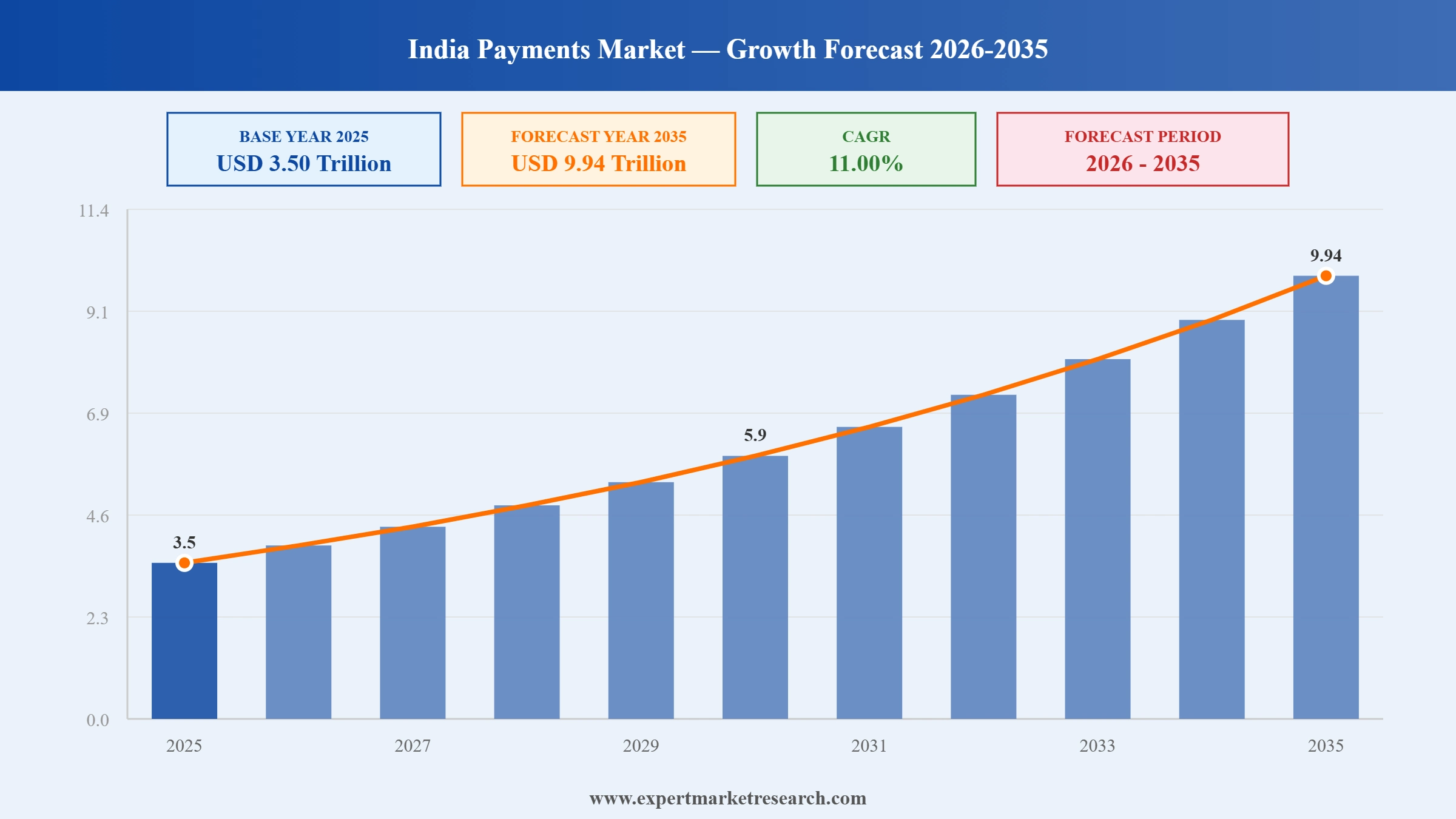

The India payments market reached a value of USD 3.50 Trillion at 2025 and is projected to expand at a CAGR of around 11.00% during the forecast period of 2026-2035. Driven by the rapid adoption of UPI-based digital payments, expanding mobile wallet penetration, government-led financial inclusion initiatives, and growing merchant digitisation across urban and rural India, the market is expected to reach USD 9.94 Trillion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India payments market is undergoing a structural transformation driven by the Unified Payments Interface's emergence as one of the world's most widely used real-time payment systems, regulatory maturation of the payment aggregator framework, and the entry of major Indian fintech companies into public capital markets. Ongoing innovations in offline, cross-border, and credit-linked payment services are broadening the market's revenue potential beyond pure transaction volume growth, attracting sustained investment and strategic consolidation among leading market participants.

The Reserve Bank of India cancelled the banking licence of Paytm Payments Bank Limited (PPBL) effective April 24, 2026, citing regulatory non-compliance and governance concerns that were detrimental to depositor interests. The cancellation followed a prolonged period of supervisory action against the Paytm Payments Bank subsidiary of One 97 Communications Limited, which began with restrictions on fresh deposits in early 2024. One 97 Communications clarified that the cancellation does not affect its core Paytm app, UPI services, payment gateway, QR, and Soundbox merchant operations, which continue to function independently of the payments bank entity.

Paytm Payments Services Limited (PPSL), a wholly owned subsidiary of One 97 Communications, received RBI authorisation to operate as a Payment Aggregator for physical (offline) payments and cross-border transactions in December 2025, following its online PA authorisation granted in November 2025. The dual licensing completes PPSL's coverage across all major payment aggregation segments, enabling it to offer merchants an end-to-end solution spanning online, in-store, and international payment acceptance. This regulatory milestone positions Paytm to rebuild its merchant ecosystem and expand its payment processing volumes across domestic and cross-border channels.

Pine Labs Private Limited listed on the National Stock Exchange and Bombay Stock Exchange on November 14, 2025, following an INR 3,900 crore initial public offering at an issue price of INR 221 per share. The company opened at INR 242 on its listing day, representing a 9.5% premium, achieving a market capitalisation of approximately USD 3.3 billion at listing. Pine Labs serves over 988,000 merchants across India and 20 international markets with its POS payment solutions, BNPL services, merchant financing, and loyalty platforms. The IPO marks Pine Labs as the second-largest Indian fintech listing of 2025 and validates investor confidence in India's merchant payments infrastructure sector.

PayU India raised an equity funding round of USD 35.1 million from its parent company MIH Payments Holdings BV (a Prosus subsidiary) in July 2025, reinforcing its mission to advance India's digital payments ecosystem. The capital infusion, formalised through the issuance of 48.68 million equity shares, supports PayU's strategy to expand its merchant network, deepen partnerships, and invest in advanced payment technology infrastructure. PayU also raised its stake in Mindgate Solutions to 70.7% and rolled out UPINXT, an integrated UPI issuing and acquiring stack serving major Indian banks including SBI and HDFC Bank, collectively handling approximately 10 billion real-time transactions monthly.

UPI Transaction Volume Growth: India's Unified Payments Interface processed 228.3 billion transactions worth approximately USD 3.4 trillion establishing it as the world's single largest real-time payment network by transaction volume, accounting for approximately 50% of global real-time payment flows. The India payments market is benefiting from UPI's expansion beyond peer-to-peer transfers into merchant, corporate, credit-linked, and cross-border payments. UPI's interoperability now extends to 12 or more countries including Singapore, UAE, France, and Sri Lanka, enabling outward remittances and cross-border consumer payments for Indian travellers and diaspora.

Merchant Digitisation Drive: India's payments market growth is being driven by rapid expansion of digital payment acceptance infrastructure among small and micro-merchants through QR code deployments and audio-confirmation Soundbox devices from payment service providers including Paytm, PhonePe, and Pine Labs. The India payments market growth is particularly pronounced in tier-3 and tier-4 towns where first-time merchant digitisation is occurring at pace, supported by zero merchant discount rate policies on UPI and competitive device financing schemes from payment service providers targeting the unorganised retail sector.

Credit on UPI Expansion: The Reserve Bank of India's approval of credit line products linked to the UPI payment rails is creating new monetisation pathways for Indian fintech companies in the India payments market. Banks including HDFC, ICICI, and Axis Bank are offering UPI-linked credit facilities that enable pre-approved borrowers to make purchases through the UPI interface without upfront cash. PayU's UPINXT platform and MobiKwik's ZIP-EMI product are positioned to benefit from growing consumer credit adoption through digital payment channels, diversifying payment revenue beyond transaction processing fees.

Payment Aggregator Regulatory Framework: The Reserve Bank of India issued the Payment Aggregator Master Direction establishing a comprehensive compliance framework for companies operating as payment aggregators in India. The directive standardises merchant onboarding, escrow account management, cybersecurity standards, and grievance redressal requirements for PA licensees. Companies including Pine Labs, Razorpay, Cashfree, and PayU have received final PA authorisations under this framework, consolidating the India payments market around regulated, well-capitalised operators and raising the barriers to entry for smaller payment processing entities.

Fintech IPO Acceleration: India's payments sector is experiencing a significant wave of public market listings driven by investor appetite for India's digital economy growth story. The India payments market growth trajectory, combined with improving unit economics among leading fintech companies, is supporting IPO valuations for platform businesses including Pine Labs, which achieved a market capitalisation of approximately USD 3.3 billion at its listing, and Groww, which debuted at approximately USD 11 billion. PhonePe has filed its Draft Red Herring Prospectus targeting what would be India's largest technology IPO at a USD 15 billion valuation, signalling continued confidence in India's fintech public market narrative.

The Expert Market Research's report titled “India Payments Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

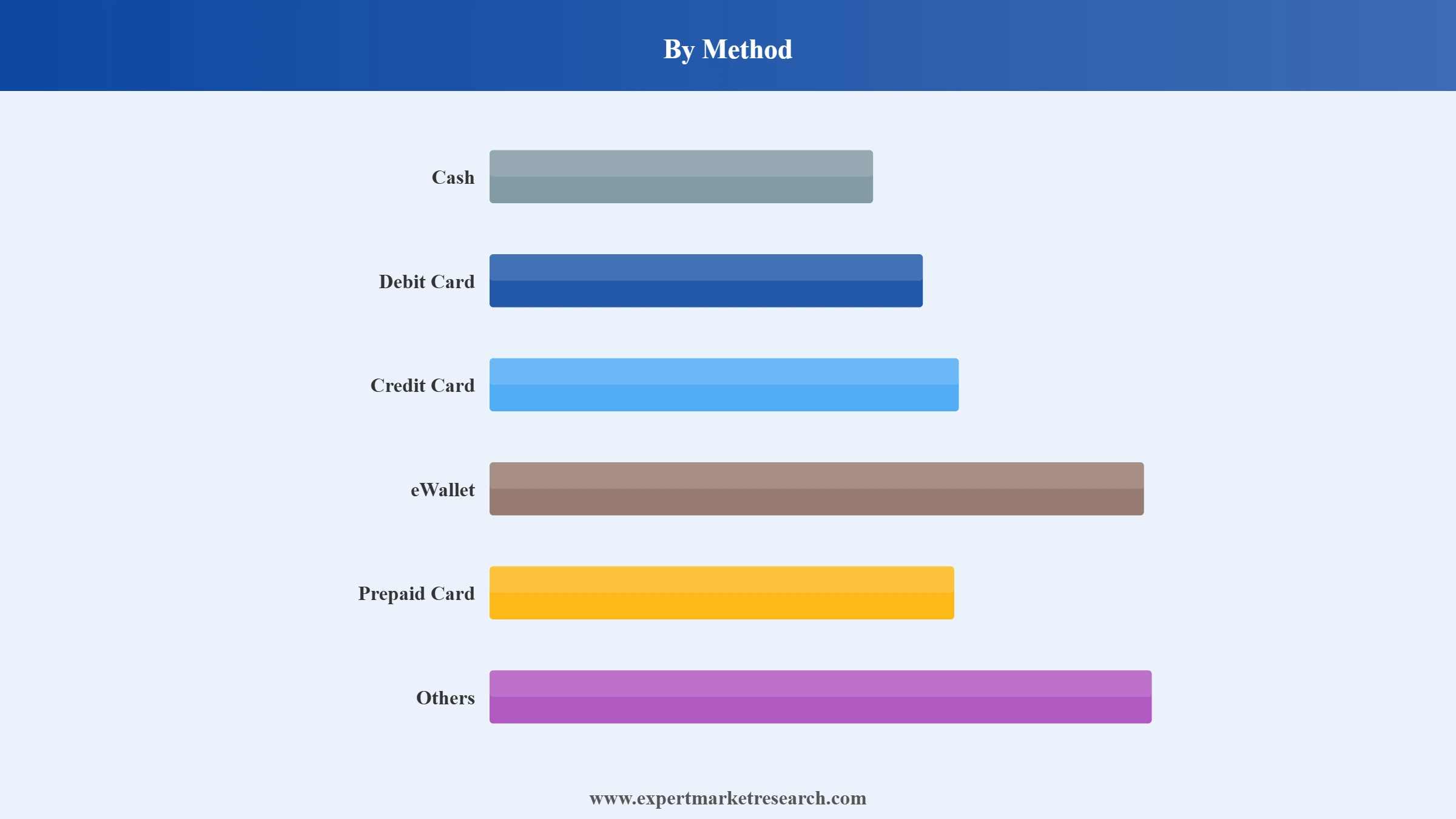

Market Breakup by Method

Key Insight: eWallet is the dominant and fastest-growing payment method in India, accounting for the largest share of digital transaction volume driven by UPI-linked applications including PhonePe, Google Pay, and Paytm. The eWallet segment's dominance reflects India's unique position as the world's largest real-time payments market, with UPI processing record monthly transaction volumes and expanding into credit-linked, cross-border, and offline near-field communication use cases. Cash remains significant in rural and semi-urban markets but is declining structurally as merchant digitisation programmes expand digital acceptance infrastructure across underserved geographies.

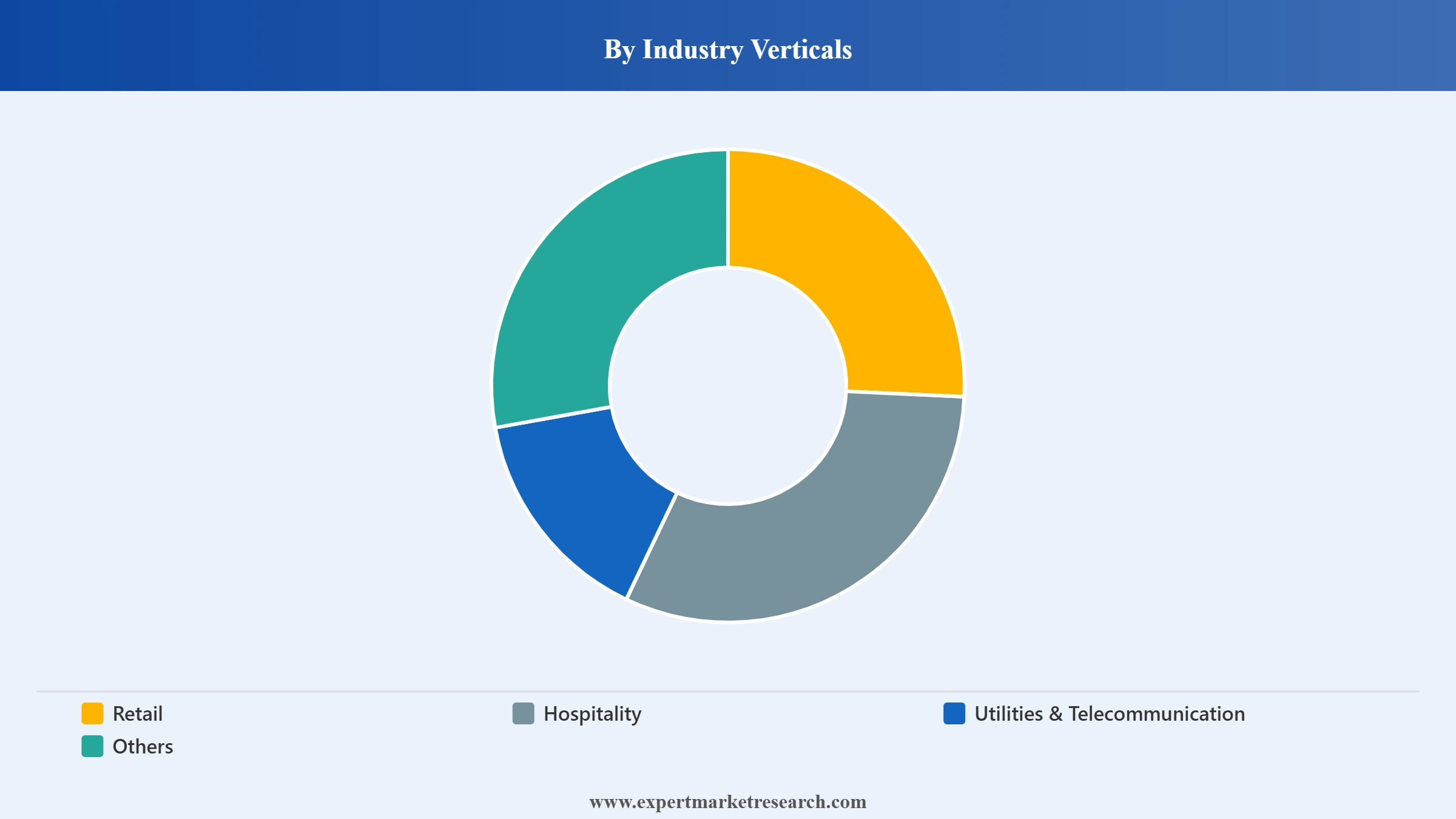

Market Breakup by Industry Verticals

Key Insight: Retail is the dominant industry vertical for India payments, accounting for the largest share of digital transaction value driven by the mass adoption of UPI QR codes at kirana stores, supermarkets, food delivery platforms, and e-commerce. The expansion of India's retail sector, combined with zero merchant discount rate policy on UPI and competitive merchant acquisition strategies by Pine Labs, Paytm, and other POS solution providers, ensures retail's structural dominance in the payments volume mix. Hospitality is one of the fastest-growing verticals, supported by the recovery of travel and tourism and the adoption of digital payment acceptance at hotels, restaurants, and travel booking platforms.

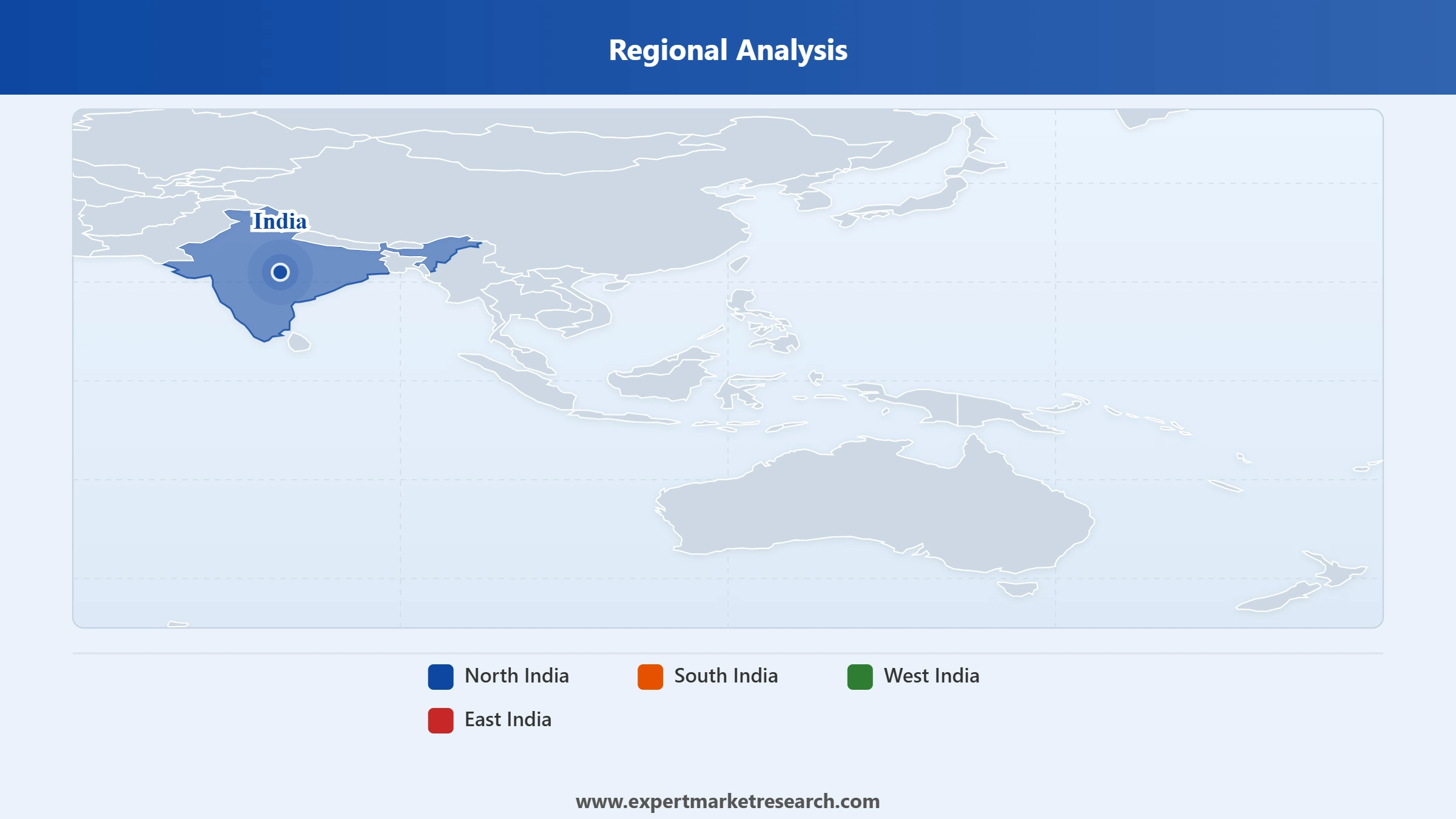

Market Breakup by Region

Key Insight: West India leads the India payments market by transaction value, driven by Maharashtra's position as India's largest financial centre and Gujarat's rapidly expanding industrial and commercial economy. Mumbai's concentration of financial services firms, corporate headquarters, and high-income consumers generates the largest per-capita digital payment volumes. West India is also home to significant fintech infrastructure, with major payment companies including PayU and Pine Labs operating large merchant networks across Mumbai, Pune, Ahmedabad, and Surat. South India is the fastest-growing region, supported by Bangalore and Hyderabad's technology sector, high smartphone penetration, and digital-first consumer demographics that are accelerating payments adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Method, eWallet accounts for the dominant share due to UPI's near-universal adoption as India's preferred real-time payment interface

eWallet's dominance in the India payments market is fundamentally anchored in the Unified Payments Interface's structural advantages of zero transaction fees, interoperability across all bank accounts, and instant settlement that has made digital payments accessible to all income segments. PhonePe and Google Pay command over 85% of UPI transaction volume, while Paytm maintains a significant merchant acquiring and offline payments presence. The eWallet segment is expanding its use cases through UPI Lite for low-value offline transactions, UPI Circle for delegated payments, and RuPay credit card on UPI integration, ensuring continued share growth at the expense of cash and debit card transactions in the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Debit cards represent the second-largest payment method by transaction value, with India's large banked population using cards for e-commerce, ATM withdrawals, and retail purchases at POS terminals. However, debit card transaction volumes are declining relative to eWallet as UPI displaces card payments at merchant acceptance points. Credit card transaction volumes are growing at a higher rate than debit cards, driven by rising consumer credit adoption, premium card rewards programmes, and the integration of RuPay credit cards into the UPI payment rails. In November 2025, Pine Labs' IPO listing highlighted the investment community's confidence in India's card and multi-payment POS terminal infrastructure business model.

By Industry Verticals, retail dominates the India payments market due to mass merchant digitisation and high-frequency consumer transaction volumes

Retail's dominance in the India payments market reflects the fundamental role of daily consumer spending on food, groceries, apparel, and consumer electronics in driving payment transaction volumes. The expansion of India's formal retail sector, supported by the proliferation of digital payment acceptance through UPI QR codes at micro-merchants and POS terminals at organised retailers, has made retail the structural foundation of India's digital payments ecosystem. Mswipe Technologies and Pine Labs provide critical merchant payment infrastructure supporting retail transaction processing at the national scale, with Pine Labs alone serving over 988,000 merchants across India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Utilities and Telecommunication represent a growing application for India's digital payments infrastructure, with government Direct Benefit Transfer schemes, electricity bill payments, and mobile recharges generating high-frequency, consistent transaction flows through digital channels. The PayU India platform, which raised USD 35.1 million in July 2025, specifically targets utility payments as a high-volume application that drives platform stickiness and merchant retention. Cross-selling of digital credit and insurance products through utility payment touchpoints is a growing strategy among Indian payments companies seeking to monetise their customer base beyond fee-based transaction processing.

West India leads the market due to its concentration of financial services, corporate headquarters, and high-income consumers driving premium payment volumes

West India's leadership in the India payments market is anchored by Maharashtra's dominant position as India's largest state economy and commercial capital, with Mumbai serving as the national headquarters for most major payment companies and financial institutions. Gujarat's rapidly growing industrial economy, driven by manufacturing, chemicals, and diamond trading in Surat and Ahmedabad, contributes high-value B2B payment flows alongside consumer digital transactions. West India's concentration of payment industry talent and infrastructure makes it both the largest market by transaction value and a key driver of innovation in the India fintech ecosystem.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the fastest-growing regional market in India's payments landscape, driven by the technology sector concentration in Bangalore and Hyderabad, high digital literacy among the working population, and strong merchant acceptance of contactless and QR-based payment methods. Bangalore functions as India's primary fintech innovation hub, hosting the headquarters of major payment companies and their engineering and product development teams. Chennai and Coimbatore's manufacturing and textile industries are also generating growing digital payment adoption as employer salary digitisation and vendor payment automation expand corporate digital payments penetration.

The India payments market is highly competitive and evolving rapidly, shaped by UPI's emergence as the dominant payment rail and a maturing regulatory framework for payment aggregators, wallets, and fintech platforms. Market structure is fragmented across multiple segments including POS hardware and acquiring, payment gateway and online aggregation, mobile wallet and UPI apps, and banking-as-a-service, with different competitive dynamics in each layer. Leading participants compete on merchant acquisition capabilities, acceptance infrastructure coverage, transaction reliability, value-added services breadth, and increasingly on regulated payment aggregator credentials under the RBI's PA Master Direction.

Founded in 2011 and headquartered in Mumbai, India, Mswipe Technologies Pvt. Ltd. is a leading mobile payments and POS solutions provider serving merchants across India with card acceptance, UPI, and digital payment solutions. Mswipe operates a large network of payment terminals including mobile POS devices, Android POS, and QR-based acceptance solutions, with a focus on small and medium merchants in tier-2 and tier-3 cities. The company offers merchants real-time analytics, payment gateway integration, and EMI processing capabilities through its merchant-facing technology platform.

Founded in 1998 and headquartered in Gurugram, India, Pine Labs Private Limited is a leading Indian merchant commerce platform listed on the NSE and BSE following its November 2025 IPO. Pine Labs provides smart POS devices, BNPL solutions, merchant financing, loyalty and gift card platforms, and payment gateway services to over 988,000 merchants across India and 20 international markets. Backed by PayPal, Mastercard, and Sequoia Capital, Pine Labs serves major retail brands, financial institutions, and consumer goods companies with integrated payment and commerce technology infrastructure.

Founded in 2012 and headquartered in Mumbai, India, ePaisa Services Private Limited is a fintech company providing tablet-based and mobile POS solutions, payment gateway services, and inventory management tools for small and medium businesses across India. ePaisa's platform integrates multiple payment acceptance methods including cards, UPI, and wallets with billing, inventory, and customer loyalty management capabilities, serving retail, hospitality, and service sector merchants seeking affordable and comprehensive digital payment and business management solutions.

Founded in 2013 and headquartered in India, Mosambee Payment Solutions Private Limited is a mobile payment solutions company providing mPOS terminals, payment gateway services, and merchant management tools to businesses across India. The company's solutions enable merchants to accept all major payment types including cards, UPI, and digital wallets through mobile-connected card reader devices and cloud-based payment management systems, serving SME clients in retail, hospitality, and service industries across Indian tier-1 and tier-2 markets.

Other key players in the market are MobiSwipe Technologies Private Limited, ICICI Merchant Services Pvt. Ltd., One 97 Communications Ltd. (PayTM), Ezetap Mobile Solutions Private Limited, One MobiKwik Systems Limited, PayU Payments Private Limited, Freecharge Payment Technologies Pvt. Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Navigate India's transformative payments landscape with our comprehensive India payments market report for 2026. Whether you are a financial institution assessing digital payments strategy, a fintech company planning market entry, an investor evaluating the India payments sector opportunity, or a merchant solutions provider developing go-to-market plans, our research delivers the intelligence you need. Access detailed forecasts by payment method, industry vertical, and region, alongside competitive profiles of key market participants. Download your free sample today and gain a strategic advantage in India's high-growth payments market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 3.50 Trillion.

The market is projected to grow at a CAGR of 11.00% between 2026 and 2035.

Key strategies driving the market include government-led digital initiatives, fintech innovation, expansion of mobile wallets, increased merchant acceptance, and financial inclusion efforts. Collaborations between banks and tech firms, along with improved cybersecurity and real-time payment infrastructure, further accelerate growth and user adoption.

Rapid digitalisation in the country and the introduction of m-wallets are the key trends driving the market.

The major regions in the industry are North India, South India, West India, and East India.

Cash, debit card, credit card, e-wallet, and prepaid card, among others are the various methods of payments in the industry.

The significant industry verticals are retail, hospitality, and utilities and telecommunication, among others.

The key players in the market report include Mswipe Technologies Pvt. Ltd., Pine Labs Private Limited, ePaisa Services Private Limited., Mosambee Payment Solutions Private Limited., MobiSwipe Technologies Private Limited, ICICI Merchant Services Pvt. Ltd., One97 Communications Ltd. (PayTM), Ezetap Mobile Solutions Private Limited., One MobiKwik Systems Limited, PayU Payments Private Limited, and Freecharge Payment Technologies Pvt. Ltd., among others.

Retail is the most dominant segment in the market, driven by rapid digitalization of offline and online commerce.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Method |

|

| Breakup by Industry Verticals |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.