Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The India spices market reached a value of INR 94927.56 Crores at 2025 and is projected to expand at a CAGR of around 9.20% during the forecast period of 2026-2035. With the shift toward branded and packaged spices, the rise of organic and clean label sourcing, expanding food service consumption, and the surge in quick commerce repurchasing, the market is expected to reach INR 228885.72 Crores by 2035.

Compound Annual Growth Rate

9.2%

Value in INR Crores

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's spice market is moving from loose commodity sales to packaged, branded, and increasingly digital retail. FMCG giants are consolidating the organic tier, regional masala houses are upgrading processing lines, and D2C labels are competing on traceability and clean label claims. The runway sits on rising urban incomes, FSSAI driven standardisation, and a fast widening quick commerce shelf that is rewriting how households restock pantry staples.

Rising adulteration concerns, FSSAI tightening, and convenience packaging are accelerating the switch from open spice purchases to trusted brands like Everest, MDH, and Catch. This structural shift is the most durable growth lever in the India spices market today.

Organic and ayurvedic spices are pulling premium FMCG money. ITC's INR 472.5 crore Sresta deal in 2025, alongside Patanjali's expanded organic sourcing, signals how clean label is reshaping the India spices market growth trajectory across urban and export channels.

Blinkit, Zepto, and Instamart are turning ten minute deliveries into the default urban restocking habit for blended masalas and sprinkler packs. Native digital labels and incumbents alike are rebuilding distribution around quick commerce to capture rising Indian spices demand.

Cloud kitchens, QSR chains, and packaged food makers are driving consistent demand for institutional spice blends. Everest, MDH, and Aachi supply curated cuisine specific masalas to large kitchens, anchoring a steady B2B layer underneath retail volumes in the spices market.

Processing upgrades like cryogenic grinding retain flavour volatiles, while nitrogen flushed multi layered packs extend shelf life for exports. Leading players including MDH and Jayanti Herbs are using these techniques to defend quality led pricing in the spices market.

The Expert Market Research’s report titled “India Spices Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

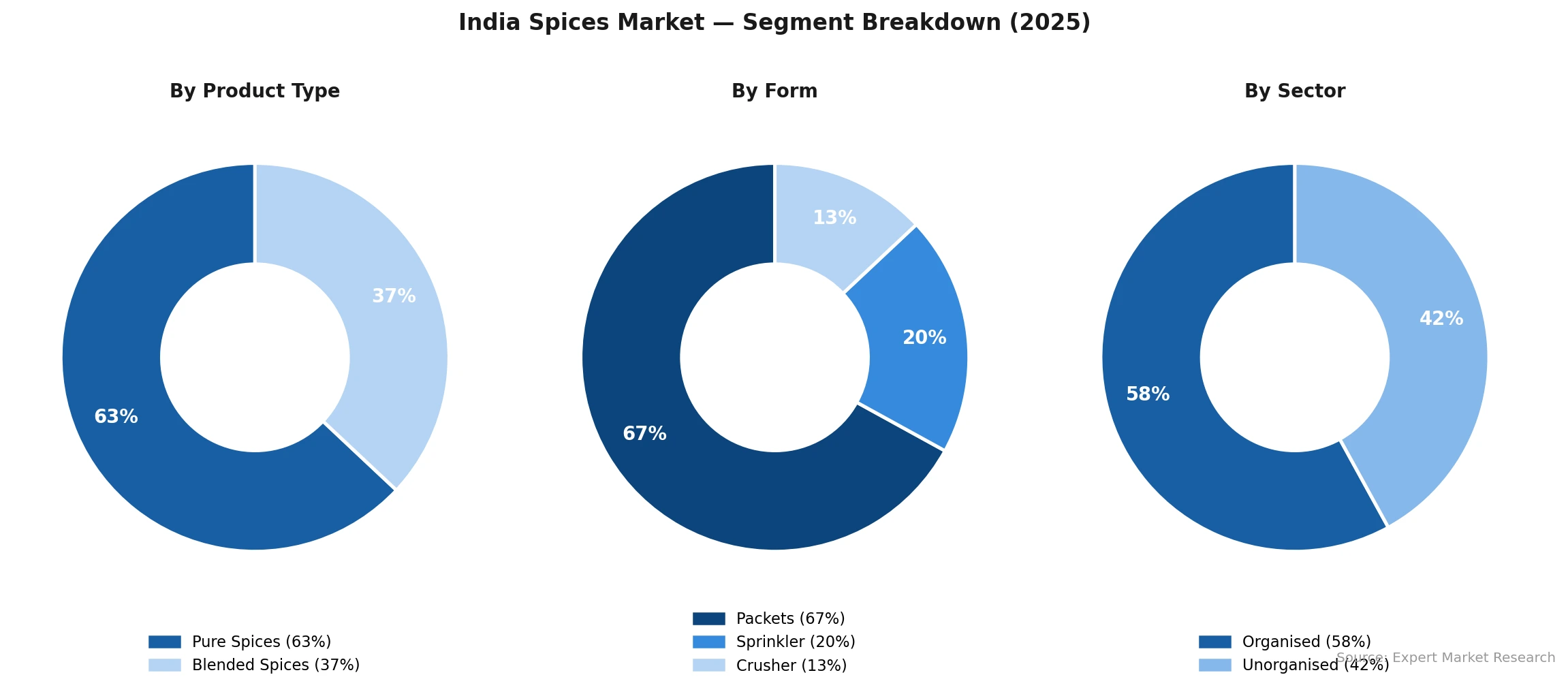

Market Breakup by Product Type

Key Insight: Pure spices like chilli, turmeric, and coriander hold the larger historical volume share because they are staple in nearly every Indian household. Blended spices are the faster growing tier, normalised by smaller urban kitchens, time pressed cooking, and standardised cuisine blends from Everest, MDH, and Catch. Convenience, recipe consistency, and rising quick commerce shelving are steadily lifting blended masala penetration across the India spices market.

Market Breakup by Form

Key Insight: Packets dominate the form mix thanks to wide retail availability, multiple price tiers, and easy stocking in kirana, supermarkets, and quick commerce dark stores. Sprinkler packs are gaining ground in urban kitchens for portion control and table top use, while crusher SKUs build a small premium niche. Leading brands like Everest, MDH, and Catch keep refreshing their pack architecture to defend shelf share.

Market Breakup by Sector

Key Insight: The unorganised sector still holds notable volumes through local chakkis and regional brands, but the organised tier is taking share quickly. FSSAI driven standardisation, adulteration concerns, and rising household income are pushing consumers toward branded packaged spices from ITC, Tata Consumer Products, and DS Group. ITC's 2025 Sresta acquisition shows how listed players are using M&A to formalise the India spices market.

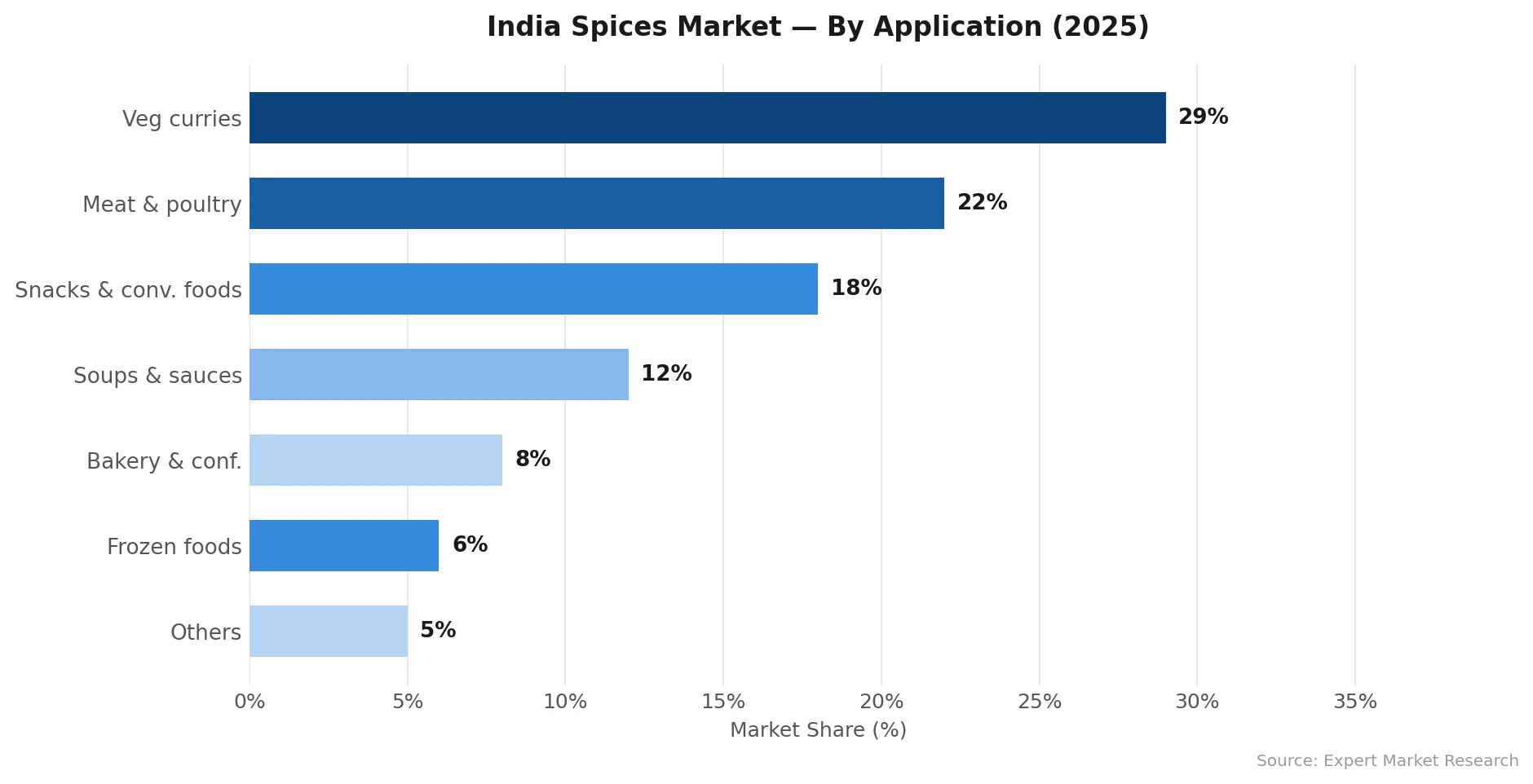

Market Breakup by Application

Key Insight: Veg curries are the largest application bucket, given the everyday central role of dal, sabzi, and rice in Indian meals. Snacks and convenience foods are growing fast, driven by branded namkeen, ready to fry, and frozen snacks from ITC, Haldiram's, and Bikaji. QSR chains and cloud kitchens are also lifting masala demand for meat, poultry, and frozen prepared foods across the India spices market.

Market Breakup by End Use

Key Insight: Retail is the dominant end use, anchored by household pantry purchases through kirana, modern trade, and quick commerce. Food service is the faster growing tier, lifted by QSR chains, cloud kitchens, and HORECA operators that need consistent, large pack institutional blends. Everest and MDH are deepening dedicated food service portfolios with cuisine specific masalas, expanding their share inside the India spices market.

Market Breakup by Region

Key Insight: South India leads spice cultivation thanks to Kerala's pepper and cardamom belts, Tamil Nadu's Erode turmeric, and Andhra's Guntur chilli; this anchors both domestic supply and exports. North India is the largest consumption pole for blended garam masala style blends, with Everest, MDH, and Catch leading the shelves. West India, especially Gujarat's Mehsana belt, contributes significantly to cumin and fennel output, while East and Central India is the fastest growing consumption zone as branded penetration climbs in tier two towns.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, pure spices dominate the market due to deep household and culinary anchoring

Pure spices lead the India spices market by volume because they sit at the base of nearly every Indian household kitchen. Chilli, turmeric, coriander, cumin, and pepper are non discretionary staples used daily across cuisines and income bands. Brands like Everest, MDH, and Aashirvaad have built broad SKU shelves for single spices to ride this everyday demand, while regional producers in Guntur, Erode, and Kerala supply the underlying raw material base.

Blended spices are the faster growing tier, normalised by smaller urban kitchens, time pressed cooking, and the rise of cuisine specific blends like Pav Bhaji, Chole, Sabzi, and Biryani masala. In December 2025, ITC's INR 472.5 crore Sresta acquisition expanded its organic and ayurvedic blended portfolio, while D2C labels such as Zoff Foods and ZESTA push transparency claims, reshaping how new shoppers enter the Indian spices market.

By form, packets dominate the market due to broad retail visibility and quick commerce friendliness

Packets capture the largest form share in the India spices market because they fit every retail format, from kirana counters to hypermarket aisles to ten minute quick commerce baskets. Multiple grammage tiers and price points let brands like Everest, MDH, and Catch serve sachet buyers in small towns and bulk household stockers in metros. Pack innovation, including nitrogen flushed and zip lock variants, is also helping protect shelf life and pricing premium.

Sprinkler packs are the fastest growing form, particularly in urban kitchens that want portion control, on the table dispensing, and cleaner storage. In May 2025, Everest expanded its sprinkler SKUs on Blinkit and Zepto, capturing higher repeat order velocity from urban repeat buyers. Crusher units remain a smaller premium niche, but they signal a clear upgrade pathway for the India spices market.

By sector, the organised tier leads on trust, standardisation, and modern retail reach

The organised sector is steadily overtaking the unorganised tier in the India spices market on the back of FSSAI standardisation, packaged hygiene, and growing distrust of loose mandi spices after past adulteration scares. Listed FMCG players such as ITC, Tata Consumer Products, and DS Group are scaling automated grinding, traceable sourcing, and pan India distribution networks, anchored by flagship brands like Aashirvaad, Sampann, and Catch.

The unorganised sector still serves price sensitive small towns and rural households through local chakkis, regional masala houses, and weekly mandi purchases, holding meaningful share by volume. However, regulatory tightening and rising consumer demand for traceable, clean label spices are slowly pulling that demand into organised channels, accelerating consolidation across the Indian spices market.

By application, veg curries dominate the market on the strength of daily Indian meal patterns

Veg curries lead application demand in the India spices market because dal, sabzi, paneer, chole, and rice based meals are an everyday default across most Indian homes. Brands like Everest and MDH offer dedicated Sabzi, Chole, and Paneer masalas to standardise these everyday recipes. Steady wheat, rice, and pulse consumption combined with rising packaged staple food penetration translate into a deep, predictable run rate of curry masala usage.

Snacks and convenience foods are the fastest growing application bucket, lifted by branded namkeen, frozen snacks, and ready to fry products from ITC, Haldiram's, and Bikaji. QSR chains and cloud kitchens are also lifting masala demand for meat, poultry, and frozen prepared foods, while soups, sauces, dressings, bakery, and confectionery uses add a smaller but rising layer of B2B demand across the Indian spices market.

By end-use, retail dominates the market on the back of deep household penetration

Retail is the dominant end use channel in the India spices market because spices are an unavoidable household staple. Kirana stores still anchor reach in tier two and tier three India, modern trade like Reliance, DMart, and Big Bazaar drives discovery in metros, and quick commerce platforms such as Blinkit, Zepto, and Instamart are now becoming the default urban restocking shelf, lifting repeat orders for Everest, MDH, and Catch packs.

Food service is the faster growing end use bucket, lifted by QSR chains, cloud kitchens, hotels, and packaged food makers that need consistent institutional spice blends. Everest and MDH are deepening dedicated food service portfolios, while Aachi and Eastern Condiments are pushing standardised cuisine specific masalas to large kitchens, building a steady B2B layer underneath the consumer facing spices market in India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India dominates the market due to dense urban demand, strong distribution, and household masala heritage

North India leads the India spices market on the back of dense urban consumption, deep distribution networks, and a strong culinary tradition of blended masalas like garam, chole, and paneer masala. Cities such as Delhi NCR, Lucknow, Jaipur, and Chandigarh are core demand hubs for Everest, MDH, and Catch. Khari Baoli in Delhi remains India's largest spice trading hub, while modern trade and quick commerce in metros continue to lift branded blended spices demand.

South India is the fastest growing region, anchored by Kerala's pepper and cardamom belts, Tamil Nadu's Erode turmeric, and Andhra's Guntur chilli cluster. Strong cultivation, deep exports, and growing branded consumption combine to lift the Indian spices market. In March 2026, DS Group's distribution push into tier two and three south Indian towns, alongside Aachi and Sakthi's local strength, is driving organised channel penetration and stronger food service demand.

The India spices market is moderately fragmented, with a few large branded FMCG players holding meaningful share alongside a long tail of regional masala houses, D2C labels, and unorganised local chakkis. Everest, MDH, DS Group's Catch, and ITC's Aashirvaad and Sunrise Pure brands anchor the organised tier, while Tata Sampann, Patanjali, Eastern Condiments, and Aachi dominate specific regional belts.

Competition is increasingly defined by processing technology, traceable sourcing, and quick commerce shelf access rather than price alone. M&A activity, including ITC's INR 472.5 crore Sresta deal, automation upgrades at MDH, and Everest's e-commerce push, all show how the India spices market is rapidly formalising while staying fiercely contested across product, form, and cuisine specific blends.

Founded in 1967 and headquartered in Mumbai, Everest is a leading branded spices player in India with over 52 blended masala variants, including Tikhalal, Kitchen King, and Garam Masala. The company runs automated grinding plants and a deep pan India distribution network, with strong leadership in west and north India and growing quick commerce shelf share.

Founded in 1919 and headquartered in Delhi, MDH is among India's most iconic spice brands with deep household penetration. Its portfolio spans flagship blends like Deggi Mirch, Chunky Chat Masala, and Kitchen King. The company has invested in automated grinding and nitrogen flushed packaging to strengthen export compliance and protect its premium north Indian masala positioning.

Founded in 1958 and headquartered in Mumbai, Badshah Masala is a prominent blended spices maker with strong distribution across west and north India. Its portfolio includes Garam Masala, Chana Masala, Pav Bhaji Masala, and a growing range of cuisine specific blends, marketed through traditional retail, modern trade, and increasingly through quick commerce platforms.

DS Group, founded in 1929 and headquartered in Noida, operates the Catch Spices brand, known for its tableware sprinklers and a broad range of pure and blended spices. In March 2026, the group outlined a distribution led plan to double Catch sales, deepening its tier two and tier three footprint and lifting modern trade and HORECA presence.

Other key players in the market are Eastern Condiments Pvt. Ltd., Aachi Spices & Foods Pvt Ltd, MTR Foods Pvt. Ltd., Patanjali Ayurved Limited, Sakthi Masala Private Limited, ITC Limited (Sunrise Pure), Ushodaya Enterprises Pvt. Ltd. (Priya), Tata Consumer Products Limited, Zoff Foods Private Limited, Goldiee Group, Ashok Masale, LIFESTYLE FOODS PVT LTD., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the full intelligence on the India spices market 2026 with our latest report. See how branded packaged spices, organic and clean label tiers, food service growth, and quick commerce are reshaping demand across pure and blended categories. Whether you build a spice brand, run an ingredient supply chain, operate a food service kitchen, or invest in Indian FMCG, this report gives you the clarity to act. Download your free sample today and explore the key opportunities across India spices.

Spices and Seasonings Market

Organic Spices Market

India Spice Production Agricultural Value Chain

India Ayurvedic Herbal Ingredients Spice Usage

India Packaged Food Ingredients Spice Demand

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India spices market reached an approximate value of INR 94927.56 Crores.

The market is projected to grow at a CAGR of 9.20% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of INR 228885.72 Crores by 2035.

Key strategies driving the market include building regional hubs, digitizing farmer networks, introducing subscription models for foodservice, and leveraging AR for virtual sampling.

The growing utilisation of spices in processed and ready-to-eat food products and the increasing demand for authentic cuisines are the key trends propelling the growth of the market.

India is the largest producer of spices in the world. India is also the world's largest exporter and consumer of spices.

The use of cinnamon in cooking goes back much further in history than any other spice. As a result, it has earned the title ‘world's oldest spice’.

Kozhikode was known as the ‘City of Spices’ during classical antiquity and the Middle Ages due to its significance as the main commercial hub for trading Eastern spices.

The major players in the Indian market for spices are Everest Food Products Pvt. Ltd., Mahashian Di Hatti Pvt. Ltd., Badshah Masala Private Limited, DS Group (Catch), Eastern Condiments Pvt. Ltd., Aachi Masala Foods (P) Ltd, MTR Foods Pvt Ltd, Patanjali Ayurved Limited, Sakthi Masala Private Limited, ITC Limited, Ushodaya Enterprises Pvt. Ltd. (Priya), Tata Consumer Products Limited, Zoff Foods Private Limited, Goldiee Group, Ashok Masale, and LIFESTYLE FOODS PVT LTD., among others.

The key challenges are regulatory compliance across states, inconsistent raw spice quality, adulteration risks, and lack of cold chain in Tier-2 regions.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Form |

|

| Breakup by Sector |

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.