Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

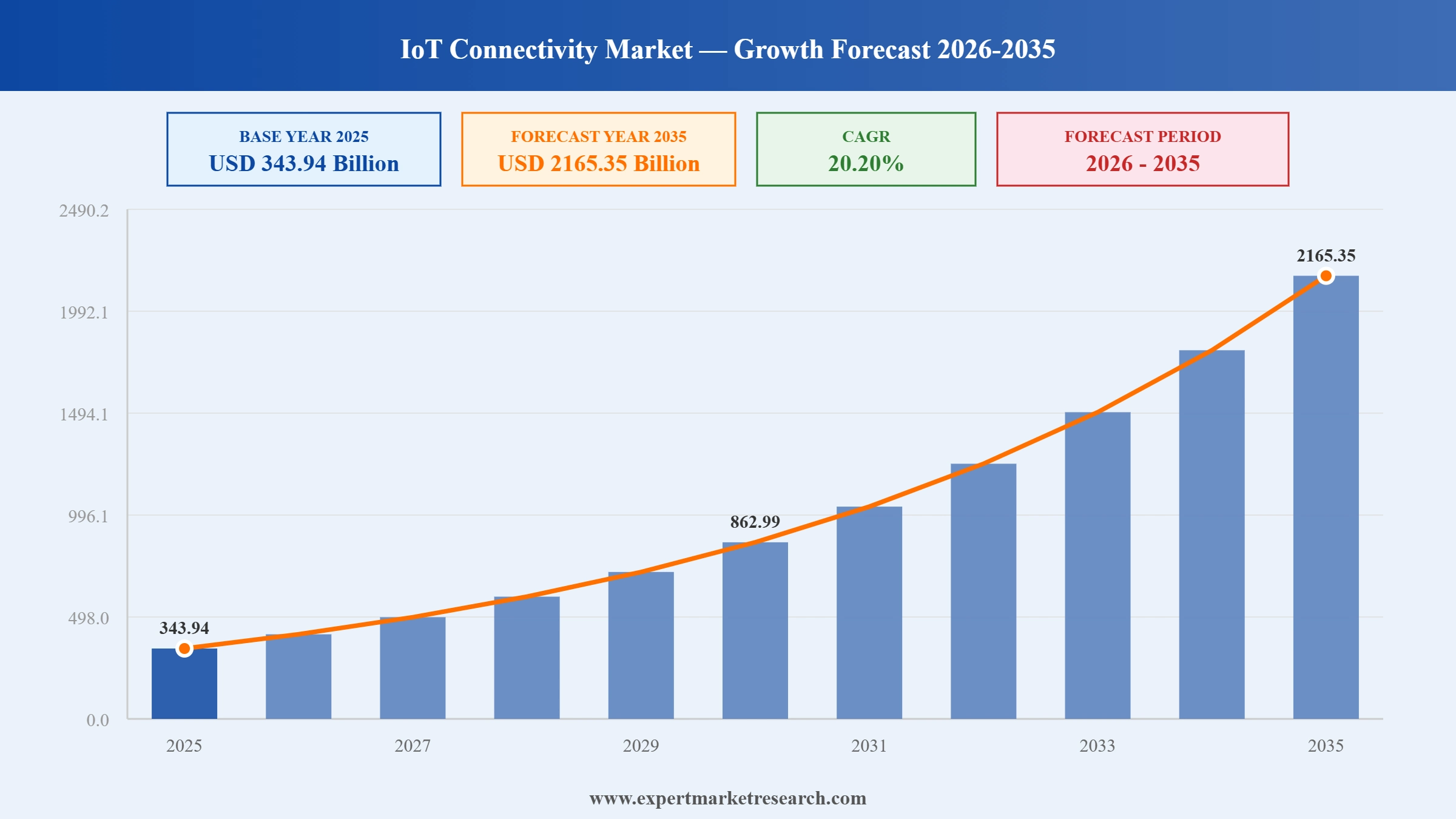

The Global IoT Connectivity Market reached a value of USD 343.94 Billion at 2025 and is projected to expand at a CAGR of around 20.20% during the forecast period of 2026-2035. With accelerating 5G rollouts, mainstreaming of eSIM and SGP.32 standards, expanding edge intelligence, and the convergence of AI with connected devices, the market is expected to reach USD 2165.35 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global IoT Connectivity Market is being reshaped by a wave of forward-looking shifts: the maturation of 5G Standalone networks and Critical IoT, the rise of multi-network and satellite-fallback architectures, the convergence of AI with edge devices for autonomous operations, and standardisation around SGP.32 eSIM that is finally simplifying cross-border device fleets at scale.

Aeris announced an inbound IoT connectivity-management collaboration with Verizon Business, integrating its IoT Accelerator (IoTA) platform with Verizon's ThingSpace and adopting the SGP.32 eSIM standard. The combination lets multinationals localise U.S.-shipped devices in weeks instead of months and orchestrate global SIM lifecycles through a single interface, materially reducing fragmentation for enterprises scaling automotive, asset-tracking, and industrial fleets across borders.

Vodafone IoT signed a multi-year agreement with Iridium to extend its NB-IoT customers onto Iridium NTN Direct, enabling messaging, tracking, and real-time monitoring beyond cellular footprints. The service, planned for commercial availability in 2026, targets automotive, industrial and asset-tracking customers requiring uninterrupted global coverage and complements Vodafone's earlier Skylo trials, broadening hybrid terrestrial-satellite IoT options for multinational deployments.

Tata Communications and Cisco unveiled a strategic collaboration that embeds Tata's MOVE eSIM orchestration platform-covering 200+ countries and 350+ million eSIM operating systems-into Cisco's IoT Control Center, used by 32,000+ enterprises managing 270+ million SIM-based devices including 100 million connected cars. The integration enables seamless multi-network device activation, faster time-to-market, and unified visibility across private and public networks for transport, logistics, and manufacturing customers.

Ericsson released the Cradlepoint X20 5G Router, an enterprise-class fixed-wireless-access device offering plug-and-play 5G connectivity with advanced network slicing and built-in security. Aimed at branch sites, pop-up locations, and primary-link applications, the X20 supports cloud-managed deployment via Cradlepoint NetCloud and was paired with the AT&T-Ericsson IoT Marketplace launched the same year to streamline device provisioning and billing for U.S. enterprises.

Telit Cinterion introduced its FE990D and FN990D modules and data cards-described as the industry's first AI-powered 5G connectivity products-featuring Qualcomm's X85/X82 5G Modem-RF and support for NB-IoT NTN satellite communication aligned with 3GPP Release 18. Targeted at automotive, industrial, and gateway applications, the launch positions on-device intelligence and non-terrestrial coverage as core requirements for next-generation IoT connectivity.

Operators and vendors are operationalising 5G Advanced features-ultra-reliable low-latency communication, network slicing and reduced-capability New Radio-to underwrite Critical IoT use cases such as remote surgery, autonomous vehicles, factory robotics, and synchronised power-grid telemetry. The trend is significant because it transitions IoT connectivity from best-effort cellular toward deterministic, mission-grade service tiers, opening higher-value enterprise contracts. Operator investments in standalone cores, dedicated network slices, and time-sensitive networking are converting connectivity from a commodity cost line into a differentiated SLA-bearing service, materially accelerating Global IoT Connectivity Market growth across regulated industries.

Carriers and IoT specialists are converging on multi-network service-management platforms that combine cellular, satellite NTN, LPWA, and Wi-Fi under a single orchestration layer. The Aeris-Verizon, Vodafone-Iridium, Vodafone-Skylo, and Tata-Cisco partnerships underline a decisive shift away from single-network SIMs toward unified, eSIM-orchestrated fleets. The pattern matters because multinational enterprises increasingly demand a single pane of glass to commission, monitor, and bill devices spanning continents, regulatory regimes, and connectivity bearers, while operators see it as the route to defending margins as legacy roaming and per-MB tariffs erode.

Module makers and platform providers are folding AI inference directly into IoT modules, routers, and gateways, rather than treating intelligence as a centralised cloud function. Telit Cinterion's deviceWISE Intelligence Suite and the FE990D and FN990D AI-enabled 5G modules exemplify a shift toward connected devices that not only transmit data but also see, decide, and act autonomously on factory floors and inside vehicles. The trend is reshaping value pools, with on-device intelligence-not raw bandwidth-becoming the chief differentiator and pulling enterprise spend decisively toward higher-margin software, models, and managed services.

The SGP.32 IoT eSIM specification is finally enabling remote provisioning and lifecycle management at fleet scale, removing the logistical and certification barriers that previously slowed cross-border IoT rollouts. Both Cisco's MOVE integration with Tata Communications and the Aeris-Verizon launch explicitly reference SGP.32, and module vendors are baking it into reference designs. The standard's adoption is significant because it lets enterprises ship a single SKU globally and switch operators over the air, slashing integration cost, accelerating connected-vehicle homologation, and unlocking sizeable transport, asset-tracking, and utilities deployments.

The Expert Market Research's report titled “Global IoT Connectivity Market Report and Forecast 2026–2035” provides a detailed analysis of the market based on the following segments:

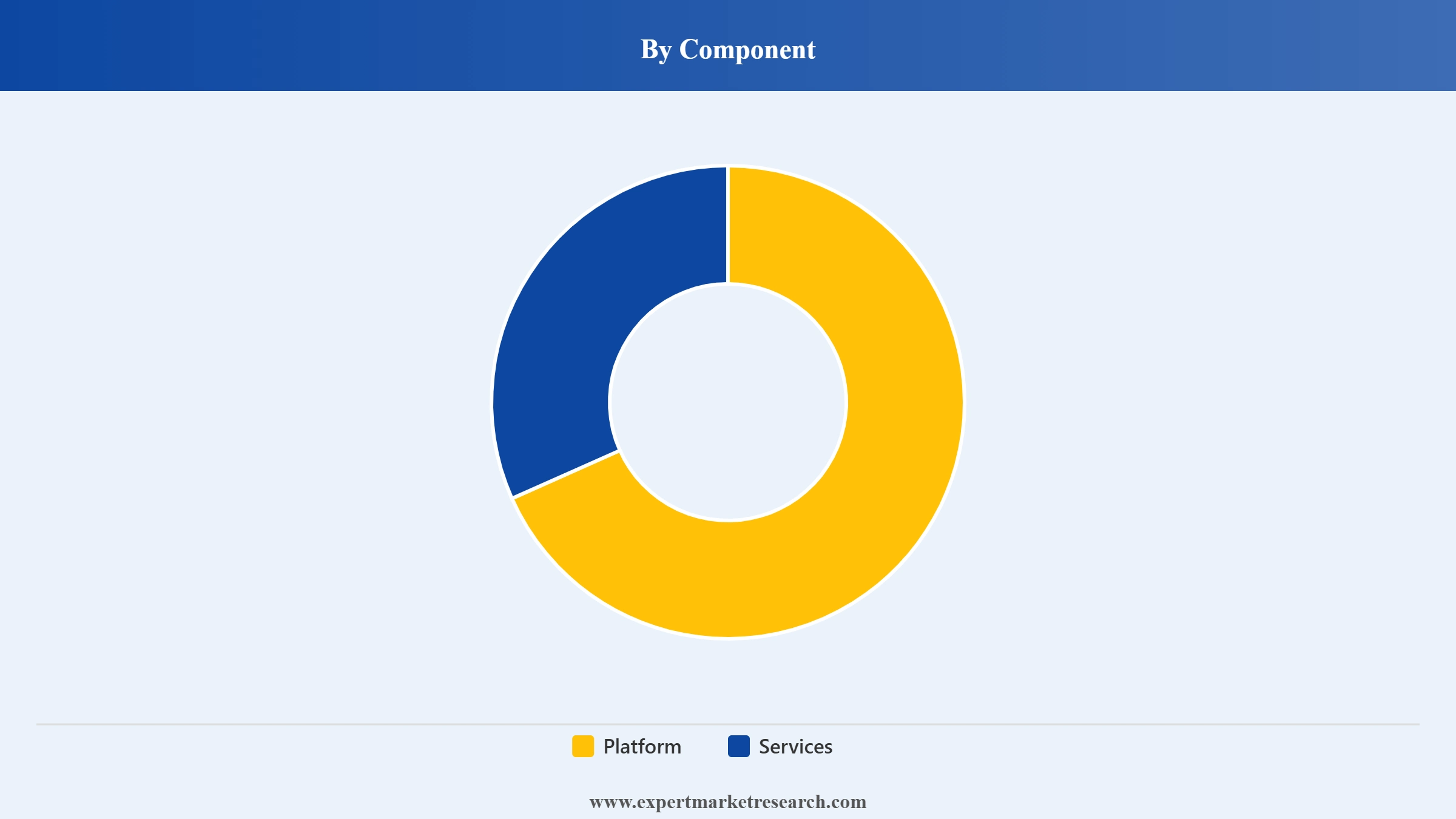

Based on component, the market is segmented into

Key Insight: The Services component is expected to dominate the global IoT connectivity market, supported by accelerating demand for managed connectivity, eSIM lifecycle orchestration, integration consulting, and platform implementation services. The hyperscaler-led platform layer (Microsoft, AWS, Huawei, Alibaba, Oracle) accounted for roughly 60% of the agnostic IoT platform market in 2024, but enterprises are increasingly outsourcing operations to specialists such as Aeris, Tata Communications, Vodafone IoT, and Telefonica. Services revenue is projected to expand at a CAGR of around 21.4% over 2026-2035 as multinational deployments require ongoing SIM management, monitoring, and security operations far beyond initial platform licensing.

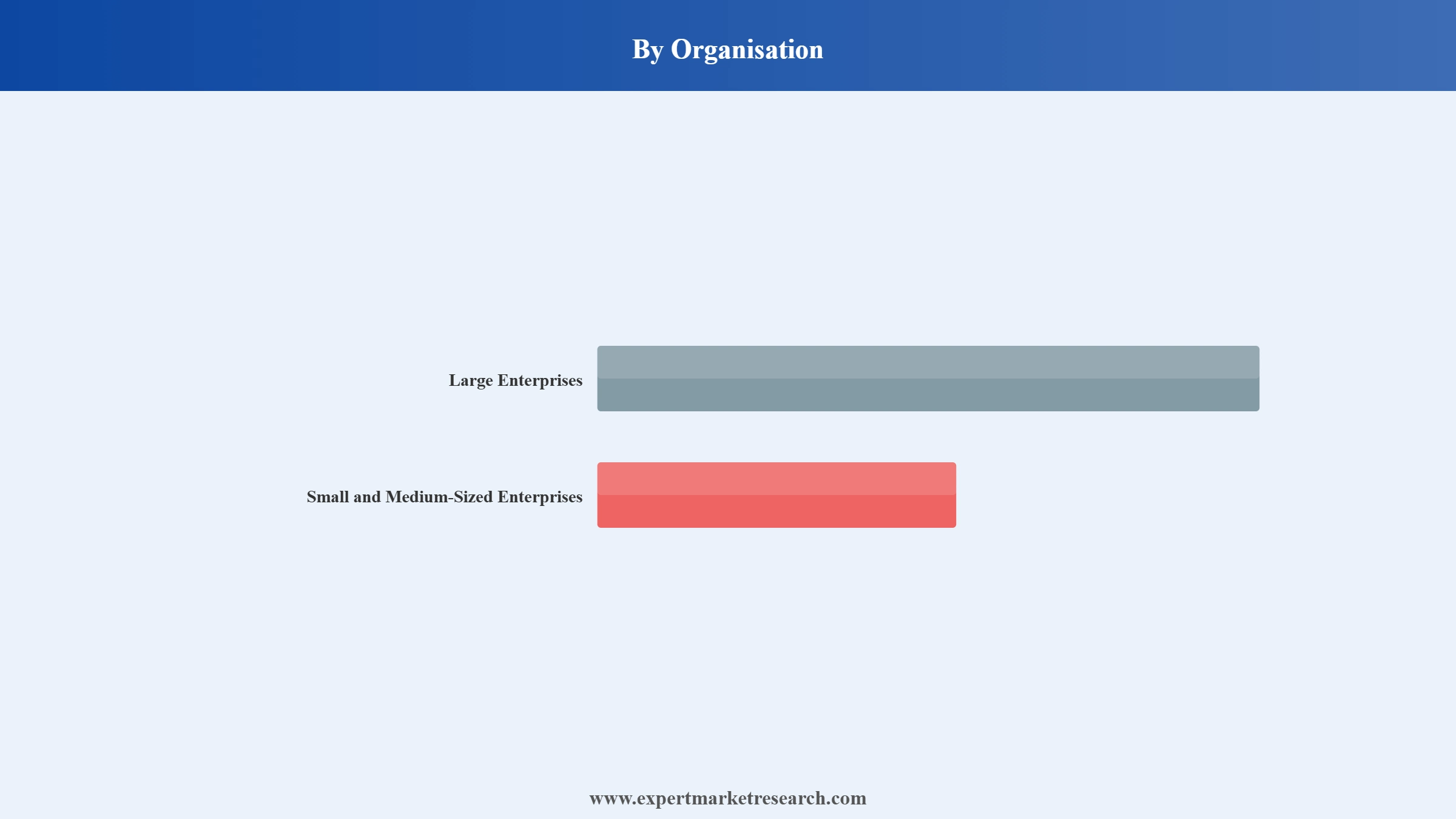

On the basis of organisation, the market can be divided into

Key Insight: Large Enterprises continue to anchor revenue, accounting for the majority of IoT connectivity spend through automotive, manufacturing, energy, and logistics deployments at scale. However, the Small and Medium-Sized Enterprises segment is forecast to register the highest growth, with industry analysts citing CAGRs in the 23-27% range during 2026-2035 as cost-effective, plug-and-play kits, cellular LPWA pricing, and pre-integrated AWS/Azure stacks lower the entry bar. SME use cases are concentrated in remote equipment monitoring, energy optimisation, and workflow visibility.

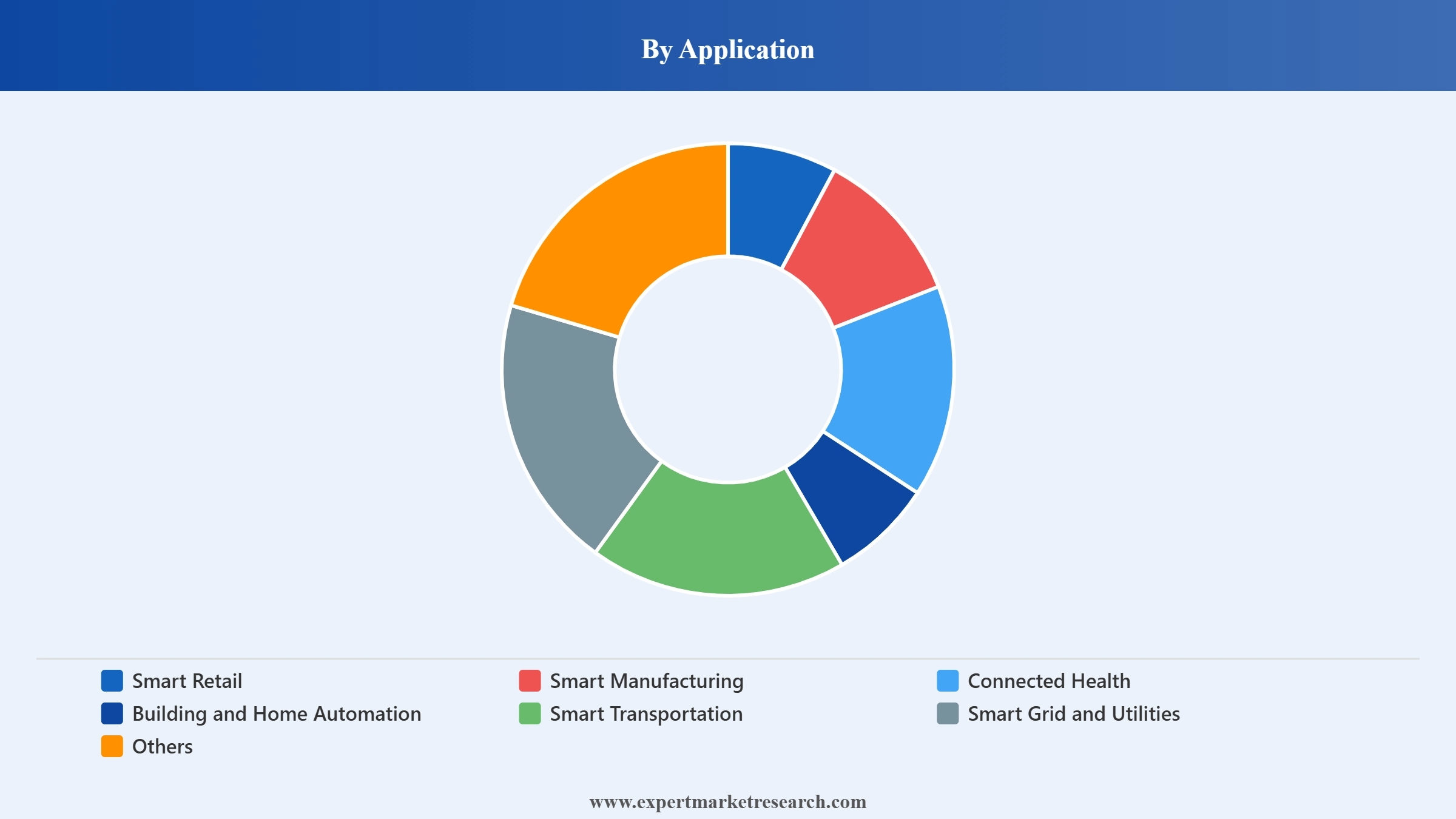

By application, the IoT connectivity market segmentation includes

Key Insight: Smart Manufacturing leads application demand, propelled by Industry 4.0 modernisation, predictive-maintenance deployments, and the rise of private 5G in factory environments-where private 5G manufacturing revenue is projected to climb from roughly USD 1 Billion in 2025 to USD 8.7 Billion by 2030. Connected Health is the fastest accelerator within applications, with the broader IoT-in-healthcare market forecast to grow above 23% CAGR, supported by chronic-disease prevalence, ageing populations, and home-care monitoring. Smart Transportation, Smart Grid and Utilities, and Building and Home Automation also benefit from 5G slicing and eSIM standardisation.

The major regional markets for IoT connectivity include

Key Insight: North America retains revenue leadership in IoT connectivity, anchored by deep enterprise IT budgets, mature carrier ecosystems (AT&T, Verizon, T-Mobile), and aggressive ThingSpace, AT&T-Ericsson Marketplace, and private-5G rollouts. Asia Pacific is the fastest-growing region, projected to log a CAGR meaningfully above the global average over 2026-2035, fuelled by 5G Standalone rollouts in China, Japan, and South Korea, "Made in China 2025," "Digital India," and Japan's "Society 5.0," with cellular M2M/IoT connections in the region projected to reach 1.3 billion by 2030. Europe benefits from a strong telco IoT base (Vodafone, Telefónica, Orange, Deutsche Telekom), while Latin America and the Middle East and Africa are emerging hot-spots tied to smart-city programmes and utility digitisation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Component, Services dominates the market with the larger share, supported by enterprises increasingly outsourcing connectivity orchestration, security, and lifecycle management to specialists. Platform revenue is concentrated among five hyperscalers-Microsoft, AWS, Huawei, Alibaba, and Oracle-which collectively held about 60% of the agnostic platform market in 2024. Services dominance reflects the operational reality that platform spend is one-time, while services such as eSIM provisioning, monitoring, and SOC operations recur. Aeris-Verizon's February 2026 launch of unified inbound services and Tata-Cisco's eSIM-powered MOVE integration are direct evidence of services becoming the higher-margin growth engine.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Organisation, Large Enterprises dominate the market with a substantial share of total IoT connectivity revenue. Their lead reflects multi-year, multi-country contracts in automotive (connected cars), industrial manufacturing, oil and gas, and global logistics-segments that demand SLAs, private networks, and integration with enterprise IT. Hyperscaler tie-ups, regulatory complexity, and the cost of certifying global SIMs all favour incumbents. Even so, SMEs are growing fastest, with adoption of cost-effective LPWA, off-the-shelf cellular routers, and managed-connectivity bundles broadening the customer base. Vodafone IoT's hyperscale partnerships and AT&T-Ericsson's IoT Marketplace are designed to bring SMEs into the same platform as Fortune 500 customers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Smart Manufacturing dominates application share, reflecting Industry 4.0 capex, automotive manufacturing's appetite for IoT-enabled smart factories (the largest end-user share in 2025), and the maturation of private 5G. Coherent industry data places IoT-in-manufacturing revenue at USD 278.69 Billion in 2025, growing toward USD 909 Billion by 2032 at an 18.4% CAGR. Connected Health is the second pillar by share, supported by remote patient monitoring, wearable-device adoption, and post-pandemic home-care models. an industry research firm's April 2026 update flagged home-care IoT growing at an 18.32% CAGR through 2031, pulling demand for cellular and Wi-Fi connectivity bundles into clinics, pharmacies, and homes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America remains the largest revenue contributor to the Global IoT Connectivity Market, supported by mature 5G coverage, deep enterprise IT spending, and a dense ecosystem of connectivity specialists, hyperscalers, and module makers. Verizon's 2026 partnership with Aeris, AT&T's IoT Marketplace built with Ericsson, and the rollout of network APIs through Aduna (AT&T, T-Mobile, Verizon) underscore aggressive carrier-led innovation. Connected vehicles, healthcare, manufacturing, and oil and gas account for the bulk of demand, with Verizon's ThingSpace platform managing tens of millions of cellular IoT lines. The U.S. continues to anchor regional spend, with Canada's adoption growing through digital-utility, smart-city, and connected-fleet programmes that ride on the same carrier infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing region, with major economies channelling national strategies-China's "Made in China 2025," "Digital India," and Japan's "Society 5.0"-into IoT-enabled industrial, smart-city, and connected-vehicle ecosystems. Cellular M2M/IoT connections in the region are projected to climb to 1.3 billion by 2030, supported by 5G Standalone rollouts in China, Japan, and South Korea and large-scale smart-city programmes in India and ASEAN economies. Major regional players such as Huawei Technologies, Soracom, and Tata Communications are expanding cross-border platforms, while Indian and ASEAN governments are subsidising private-5G and IoT-platform pilots in manufacturing, agriculture, and logistics, with India alone projected as the fastest-growing IoT country at 13.8% CAGR through 2030.

The Global IoT Connectivity Market is moderately consolidated yet competitively intense, with telco-grade specialists, hyperscalers, module makers, satellite operators, and pure-play IoT MVNOs all vying for enterprise wallets. Differentiation increasingly hinges on multi-network orchestration, eSIM and SGP.32 readiness, satellite NTN tie-ups, and AI-enabled module portfolios rather than simple per-MB tariffs, with carriers using IoT as a strategic margin defence against legacy roaming erosion.

Top players are investing heavily in partnerships and platforms-Cisco and Tata Communications, Aeris and Verizon, Vodafone with Iridium and Skylo, and AT&T with Ericsson-because connectivity is now sold alongside lifecycle management, cybersecurity, and analytics. Strategic priorities revolve around globalising eSIM management, embedding AI at the edge, and bundling connectivity with vertical IoT solutions for manufacturing, transportation, healthcare, energy, and connected-vehicle customers, while regional players defend home turf with regulatory know-how.

Founded in 2004 and acquired by Cisco in 2016, Jasper Technologies is headquartered in Santa Clara, California. Its IoT Control Center underpins one of the world's largest connectivity-management deployments, supporting 32,000+ enterprises and 270+ million SIM-based devices, including 100 million connected cars. Strengths include carrier-grade scale, deep automotive penetration, and the 2025 MOVE integration with Tata Communications.

Founded in 1991 and headquartered in Newbury, United Kingdom, Vodafone is one of the world's largest IoT MNOs, managing more than 200 million IoT connections globally. The group has invested heavily in NTN NB-IoT through partnerships with Iridium and Skylo and is hyperscale-ready for global automotive, logistics, and utilities customers. Vodafone's strength lies in cross-border SIM management and operator alliances.

Founded in 2000 and headquartered in New York, U.S., Verizon operates one of the world's largest 5G and IoT networks. Its ThingSpace platform anchors enterprise IoT in North America, and the February 2026 Aeris partnership extended its reach to multinationals localising in the U.S. Verizon's strengths include private 5G, satellite tie-ups with AST SpaceMobile, and a deep automotive-and-utilities customer base.

Founded in 1876 and headquartered in Stockholm, Sweden, Ericsson is a leading 5G and IoT infrastructure vendor. Through its Cradlepoint subsidiary it offers enterprise FWA and IoT routers (the X20 launched in 2025) and runs joint platforms such as the AT&T IoT Marketplace and the Aduna network-API venture with U.S. carriers. Ericsson's strengths span Critical IoT, 5G Advanced, and global telco partnerships.

Other key players in the market are Huawei Technologies Co., Ltd., AT&T Inc., Orange S.A., Hologram Inc., Telit, Telefónica S.A., Sierra Wireless, Particle Industries, Inc., Aeris Communications, Inc., UnaBiz Pte., Ltd, EMnify GmbH, Velos IoT Group, Microsoft Corporation, Tata Communications Limited, Soracom, Inc., Pelion IoT Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global IoT Connectivity Market 2026 with our comprehensive report. Stay ahead of the curve with detailed data on platform innovation, eSIM standardisation, satellite-NTN integration, and the regions powering connected-device growth. Whether you are launching a new connectivity platform, scaling a global IoT fleet, or sizing an investment, this report provides the clarity you need. Download your free sample now and unlock the key opportunities in the thriving Global IoT Connectivity industry.

IoT Device Management Market

IoT Medical Devices Market

IoT in Smart Cities Market

IoT Cloud Platform Market

IoT in Healthcare Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 343.94 Billion.

The market is assessed to grow at a CAGR of 20.20% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 2165.35 Billion by 2035.

The major market drivers are the growing deployment of edge computing by businesses and the surging accessibility to the 5G network.

The key trends aiding the market growth are the growing focus by organisations to improve their efficiency and the rising adoption of digital twin technology by businesses.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The major components of IoT connectivity are platform and services.

The major players in the market are Jasper Technologies, Inc., Huawei Technologies Co., Ltd., AT&T Inc., Vodafone Group Plc, Orange S.A., Hologram Inc., Telit, Telefónica Global Solutions, S.L.U., Telefonaktiebolaget LM Ericsson, Sierra Wireless, Verizon Communications Inc., Particle Industries, Inc., Aeris Communications, Inc., UnaBiz Pte., Ltd, EMnify GmbH, Velos IoT Group, Microsoft Corporation, Tata Communications Limited, Soracom, INC., and Pelion IOT Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Organisation |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.