Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The Italy Retail Market reached a value of USD 10.79 Billion at 2025 and is projected to expand at a CAGR of around 2.70% during the forecast period of 2026-2035. With growing e-commerce adoption and omnichannel integration, expanding international brand presence across Italian retail centres, rising consumer preference for private-label and value products, and increasing convenience and discount format penetration, the market is expected to reach USD 14.08 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Italy Retail Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 10.79 |

| Market Size 2035 | USD Billion | 14.08 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 2.70% |

| CAGR 2026-2035 - Market by Region | North-West Region | 3.2% |

| CAGR 2026-2035 - Market by Region | South Region | 2.8% |

| CAGR 2026-2035 - Market by Type | Luxury Goods | 3.2% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 3.2% |

| 2025 Market Share by Region | Central Region | 18.4% |

Italy's retail market is navigating a careful balance between economic caution and genuine structural opportunity. International brands are flooding in, consumers are shopping smarter, and the digital and physical worlds are blending fast. Four trends are shaping how the market evolves from here.

In February 2026, Lidl Italia celebrated the opening of its 800th store in Viale Corsica, Milan, marking a significant milestone in the German discounter's Italian expansion. Lidl Italia reported turnover of EUR 7.5 billion in 2024, a growth of more than 4% year-on-year. Looking ahead, the retailer has committed to investing EUR 1.5 billion over the next three years to open 150 additional stores, with 2026 expansion focused on major metropolitan areas including Venice, Catania, Naples, Rome, Milan, and Turin. The expansion underscores the continued strength of the discount format in Italy as consumers remain price-conscious.

In December 2025, Carrefour Group completed the sale of its entire Italian retail operations to NewPrinces Group for approximately EUR 1 billion, in one of the most significant ownership transitions in Italian retail in recent years. The transaction included 1,188 stores comprising 41 hypermarkets, 315 supermarkets, and 820 convenience outlets, which together generated gross sales of EUR 4.2 billion in 2024. NewPrinces Group will continue operating under the Carrefour brand under a transitional licence. The exit reflects Carrefour's broader strategy of divesting from non-core markets and signals ongoing structural consolidation within Italy's competitive retail landscape.

In 2025, Italy's retail real estate sector attracted a record EUR 3.5 billion in investment, with retail leading all real estate sectors by transaction volume for the year. Q4 2025 alone recorded EUR 1.2 billion in retail investment, driven by strong activity in prime high-street locations in Milan and Rome as well as major shopping centre acquisitions. Cross-border capital accounted for approximately 58% of quarterly investment, reflecting sustained international investor confidence in Italian retail assets. The record inflows signal a positive structural reassessment of Italy's retail sector, with luxury and tourist-destination retail formats commanding particular investor interest.

In 2024, Spanish fashion retailer Mango opened its first flagship store in Rome and announced plans to establish 15 new stores across Italy within the same year, as part of the brand's broader ambition to open 500 new stores globally by 2026. The expansion reflects the continued attractiveness of Italy as a destination for international fashion brands, particularly in prime high-street locations in Rome and Milan. The move adds competitive pressure on domestic Italian apparel retailers and reinforces the apparel, footwear, and accessories category as one of the most actively contested segments within Italy's retail market.

In 2024, Japanese fast-fashion and lifestyle brand UNIQLO expanded its Italian footprint by launching two new stores in Milan and Rome, aiming to bring its LifeWear concept to Italian consumers and international visitors in both cities. UNIQLO's entry into Italy as part of its European growth strategy adds a globally recognised value-fashion brand to an already competitive apparel retail market. The openings formed part of a broader wave of international retail arrivals in Italy's prime urban centres, where vacancy rates in premium high-street locations have declined and consumer footfall has recovered significantly since 2022.

Italian retailers are accelerating their shift toward omnichannel models that blend physical store experience with the convenience of digital shopping, driven by changing consumer habits and mounting competitive pressure from international platforms. As of 2025, approximately 60% of purchases in food and grocery and fashion segments were made via smartphones, and e-commerce's contribution to total retail value continues to expand. Esselunga and Coop, two of Italy's leading supermarket chains, lead digital transformation through AI-powered mobile apps, personalised recommendations, and same-day delivery expansion in northern cities. This Italy retail market growth driver is compelling traditional store-only operators to invest heavily in digital capabilities or risk losing customers to more agile competitors.

Italy's prime retail corridors in Rome and Milan are experiencing a wave of international brand entries and expansions, particularly in the fashion, sportswear, and beauty categories. Spain's Mango opened its Rome flagship and announced 15 additional Italian stores in 2024, while UNIQLO entered the market with stores in both Milan and Rome the same year. Sportswear and sneaker brands, skincare, and beauty operators have also been among the most active entrants in prime high-street locations. The sustained international brand investment is lifting vacancy rates and boosting rental values in top locations while increasing competitive intensity for domestic Italian apparel and accessories retailers.

Private-label products have become one of the most significant structural trends in Italian retail, with consumers increasingly choosing own-brand alternatives that deliver comparable quality at lower prices. In 2023, private-label products captured 31.5% of total Italian retail revenues, and growth has continued into 2025 as inflation-cautious households seek value without sacrificing quality. Conad, Coop, and Esselunga all reported strong private-label performance in 2024, with Coop redesigning over a thousand existing private-label products and launching new categories including pet food. In 2024, Despar Italia's private-label products exceeded EUR 1 billion in sales for the first time, with expected growth of 5% in 2025.

The discount retail format has consolidated its position as one of Italy's most resilient and fast-growing retail channels, with Eurospin, Lidl, and MD gaining market share at the expense of traditional hypermarkets. Eurospin achieved approximately EUR 10 billion in revenue in 2024, while Lidl reached EUR 8 billion, both gaining 1-2 percentage points of market share amid inflation as consumers sought value. Simultaneously, many retailers are shifting toward smaller, proximity-focused formats in urban centres and residential zones, responding to consumer preference for frequent, convenient shopping trips. Esselunga's transition from hypermarkets to smaller premium urban LaEsse stores targeting metropolitan shoppers represents a clear adaptation to this evolving demand pattern.

Italy Retail Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

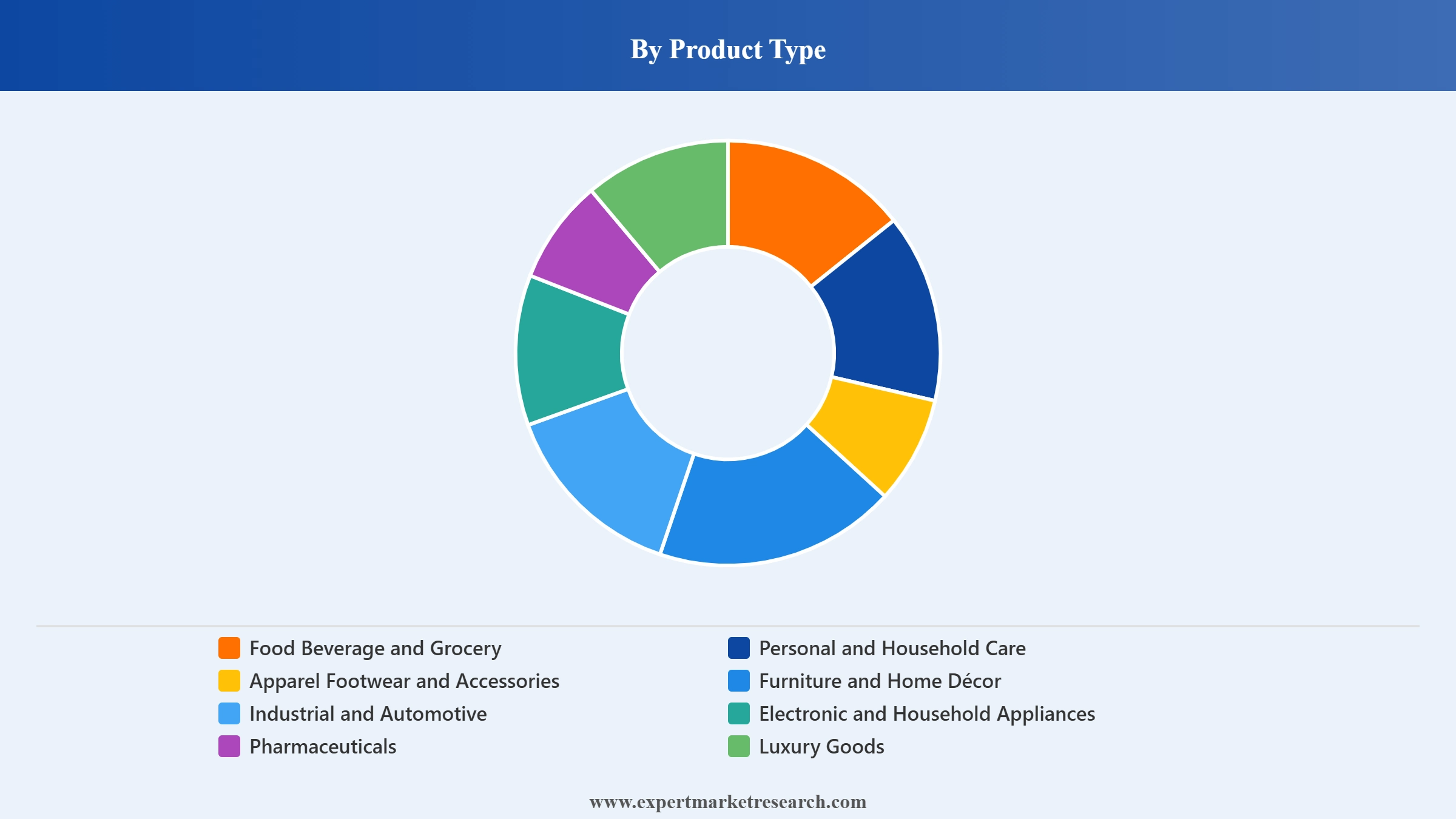

Market Breakup by Product Type

Key Insight: Food, beverage, and grocery is the largest product type segment in Italy's retail market, anchored by a dense network of hypermarkets, supermarkets, and discount outlets that serve Italy's 60 million-plus population. The segment is supported by consistently high household spending on food, with average consumer spending recovering to EUR 25.4 from 2019 levels and restaurants and personal care goods recording significant growth. Luxury goods represent one of Italy's most internationally distinctive segments, with Milan and Rome serving as global luxury retail hubs that attract sustained investment from premium brands. The apparel, footwear, and accessories segment is experiencing dynamic activity driven by international brand entries and consumer spending on fashion, which increased by approximately 19% year-on-year in recent periods. Pharmaceuticals and electronic and household appliances are stable segments with consistent consumer demand.

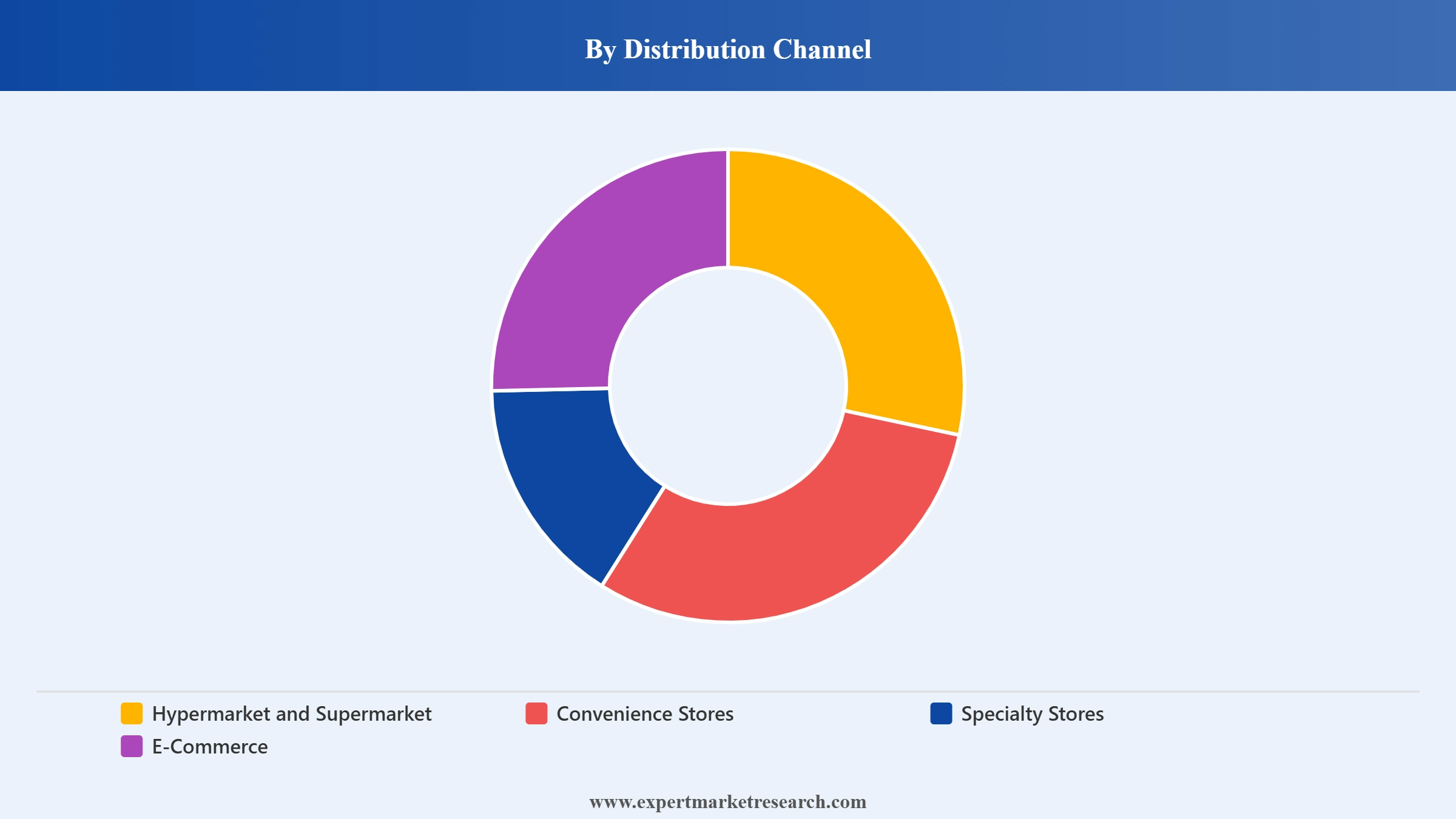

Market Breakup by Distribution Channel

Key Insight: Hypermarkets and supermarkets remain the dominant distribution channel in Italy's retail market, with cooperative-led chains including Conad (approximately 15% food retail market share), SELEX Gruppo Commerciale (approximately 15%), and Coop (approximately 11%) collectively accounting for a significant majority of grocery retail. E-commerce is the fastest-growing channel, with approximately 60% of fashion and grocery purchases made via smartphone as of 2025. International platforms including Amazon and Zalando have expanded their Italian market presence, while domestic grocery chains including Esselunga and Coop have invested in digital delivery infrastructure. Convenience stores are gaining traction in urban areas as consumers shift to smaller, more frequent shopping formats.

Market Breakup by Region

Key Insight: The North-West Region, which encompasses Milan, Turin, and Genoa, leads Italy's retail market and is projected to grow at the fastest CAGR of 3.2% through the forecast period. The region benefits from Italy's highest per-capita income levels, a dense concentration of premium and luxury retail, and active retailer expansion activity. The North-East Region, including Venice and Bologna, is a commercially significant market with a strong food retail culture and growing e-commerce adoption. The Central Region, anchored by Rome and Florence, attracts substantial luxury and international brand investment. The South Region, while lagging economically, is a growing market for discount retail expansion, with Eurospin, Lidl, and Conad all pursuing network growth in southern Italian cities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type

Food, beverage, and grocery holds the dominant position in Italy's retail market by product type, reflecting the centrality of food shopping in Italian household expenditure patterns. Conad leads the national food retail market with approximately 15% market share across its 3,300-plus stores, closely followed by SELEX Gruppo Commerciale at approximately 15% and Coop at approximately 11%. The combined market leadership of cooperative-model retailers - a format that is distinctly prevalent in Italy relative to other European markets - gives the food retail segment considerable structural stability. Private-label products have become a significant competitive lever across this segment, with Esselunga, Coop, and Conad all reporting private-label revenue growth in 2024. Luxury goods, while smaller in overall value, carry disproportionate brand significance and investment interest, with Italy's luxury retail segment attracting sustained capital from global luxury groups focused on Milan and Rome prime high-street locations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Hypermarkets and supermarkets account for the largest share of Italy's retail market by distribution channel, anchored by the cooperative networks of Conad, SELEX, and Coop. However, the competitive dynamics of this channel are shifting as discount formats led by Eurospin and Lidl gain market share, and as the broader trend toward smaller urban formats continues. E-commerce is the most rapidly expanding channel, with Italy's digital grocery and fashion retail platforms attracting strong investment. Amazon has solidified its position as Italy's dominant e-commerce operator, while Zalando leads in fashion e-commerce. Italian retailers including Esselunga have invested significantly in their own digital platforms to compete with pure-play online operators. Italy's total retail real estate investment reached a record EUR 3.5 billion in 2025, signalling strong institutional confidence in the sector's trajectory.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North-West Region

The North-West Region is Italy's most economically powerful retail zone, encompassing Milan, Turin, and Genoa, and is projected to expand at a CAGR of 3.2% through the forecast period - the fastest among Italy's four retail regions. Milan functions as Italy's retail capital, hosting the highest concentration of international luxury brands, flagship stores, and premium retail real estate. In 2025, Italian retail real estate hit record investment levels of EUR 3.5 billion nationally, with prime high-street locations in Milan attracting the majority of cross-border capital. The North-West accounts for approximately 58% of foreign retail investment in Italy, according to Expert Market Research data. The region is also at the forefront of Italy's omnichannel transformation, with Esselunga - headquartered in Milan - operating same-day delivery and leading digital grocery adoption. International entries including Mango and UNIQLO targeted Milan as their primary Italian retail launch location in 2024, underscoring the city's status as Italy's gateway retail market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Region

The South Region represents Italy's most price-sensitive but fastest-developing retail frontier, characterised by lower per-capita incomes, strong local food culture, and accelerating discount retail expansion. Eurospin, Lidl, and Conad have all prioritised southern Italian cities in their store opening programmes, recognising a consumer base that is increasingly open to discount and convenience formats as household budgets remain under pressure. Lidl's 2026 expansion plan specifically targets Naples, Catania, and other major southern cities. The South also presents growing opportunities in modern trade retail, with large shopping centres serving as anchor destinations in regions that have historically had limited access to organised retail infrastructure. Government-backed investment in southern Italy's infrastructure and logistics under EU cohesion fund programmes is expected to improve retail supply chain economics and support gradual market formalisation through the forecast period.

Italy's retail market is characterised by a distinctive cooperative ownership model that sets it apart from most Western European peers. Conad and SELEX Gruppo Commerciale together account for approximately 30% of food retail market share, operating through networks of independent regional cooperatives that benefit from national purchasing power and shared branding. This cooperative structure has proven resilient to international competition, enabling domestic chains to maintain local relevance and pricing discipline in a market where consumer trust in regional operators runs deep.

International retailers are reshaping the competitive landscape through e-commerce dominance (Amazon, Zalando) and physical expansion (Lidl, UNIQLO, Mango). The December 2025 sale of Carrefour Italy to NewPrinces Group marks the most significant competitive landscape shift of recent years, removing a major French multinational from direct Italian operations and potentially triggering further store network redistribution among Conad, Esselunga, and other domestic operators. Sustainability, private-label expansion, and digital investment are the dominant competitive priorities across both grocery and non-food segments.

Founded in 1962 and headquartered in Bologna, Italy, CONAD is Italy's leading food retailer by market share, operating through a national cooperative network of over 3,300 stores across all 20 Italian regions. With approximately 15% food retail market share and revenue exceeding EUR 21.1 billion in 2024, CONAD's cooperative model enables strong regional adaptation while maintaining national scale. The company has grown through strategic acquisitions, including stores formerly owned by Auchan Italia, and operates formats including Margherita and Spazio CONAD. Its private-label range, particularly fresh food, pasta, and wine, commands strong consumer trust, and its sustainability investments in solar energy and low-emission logistics reinforce brand appeal among environmentally conscious Italian shoppers.

Unieuro SpA is Italy's leading specialist retailer for electronics and household appliances, headquartered in Forli, Italy. The company operates an extensive network of physical stores as well as a growing e-commerce platform, serving Italian consumers across consumer electronics, household appliances, IT products, and telephony. Unieuro's dual channel strategy positions it to capture both the in-store browsing behaviour typical of Italian electronics purchasing and the growing online demand from digitally active consumers. The company competes directly with both domestic retailers and international platforms including Amazon in the electronics and household appliances segment.

Founded in 1994 and headquartered in Seattle, Washington, USA, Amazon operates one of Italy's most significant e-commerce retail platforms, serving Italian consumers across virtually all product categories including food, electronics, fashion, home goods, and pharmaceuticals. Amazon's competitive advantage in Italy lies in its logistics infrastructure, Prime membership ecosystem, and ability to aggregate a vast third-party seller marketplace. The platform's growth in Italy has been a defining force in the development of e-commerce as a structural retail channel, contributing to the acceleration of omnichannel investment among traditional Italian retailers. Amazon continues to expand its last-mile delivery infrastructure in Italian cities to compete with the growing same-day delivery capabilities of domestic supermarket chains.

Euronics International is a European consumer electronics retail cooperative with a strong presence in Italy operating through a franchise network model. The cooperative brings together independent retailers across Europe under the Euronics brand, offering a competitive range of electronics, household appliances, and multimedia products. In Italy, Euronics is one of the key competitors to Unieuro in the consumer electronics specialty retail segment, operating through franchise stores across the country. The network model allows local operators to benefit from group purchasing power and shared marketing while maintaining regional business ownership, a structure that resonates with Italy's historically cooperative and locally-rooted retail culture.

Other key players in the market are Amplifon SpA, Zalando SE, SELEX Gruppo Commerciale Srl, Coop, Carrefour Group, Esselunga SpA, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead in Italy's evolving retail market with our comprehensive report for 2026. From the discount channel's continued rise to the record investment inflows into luxury and high-street retail, the report provides a clear, evidence-based picture of where the market is heading. Whether you are a retailer planning your Italian market entry, a brand assessing channel strategy, or an investor evaluating retail asset opportunities, this report delivers the clarity you need to act with confidence. Download your free sample today and explore what is driving growth in Italy's retail landscape.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 10.79 Billion.

The market is assessed to grow at a CAGR of 2.70% between 2026 and 2035.

The market is estimated to reach around USD 14.08 Billion by 2035.

The different products in the market are food, beverage, and grocery, personal and household care, apparel, footwear, and accessories, furniture and home décor, industrial and automotive, electronic and household appliances, pharmaceuticals, and luxury goods, among others.

The different distribution channels in the market are hypermarket and supermarket, convenience stores, speciality stores, and e-commerce, among others.

The different regions covered in the market report are the north-west region, the north-east region, the central region, and the south region.

The key market players are CONAD, Unieuro SPA, Amazon.com, Inc., Euronics International, Amplifon SpA, Zalando SE, SELEX Gruppo Commerciale Srl, Coop, Carrefour Group, and Esselunga SpA, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.