Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

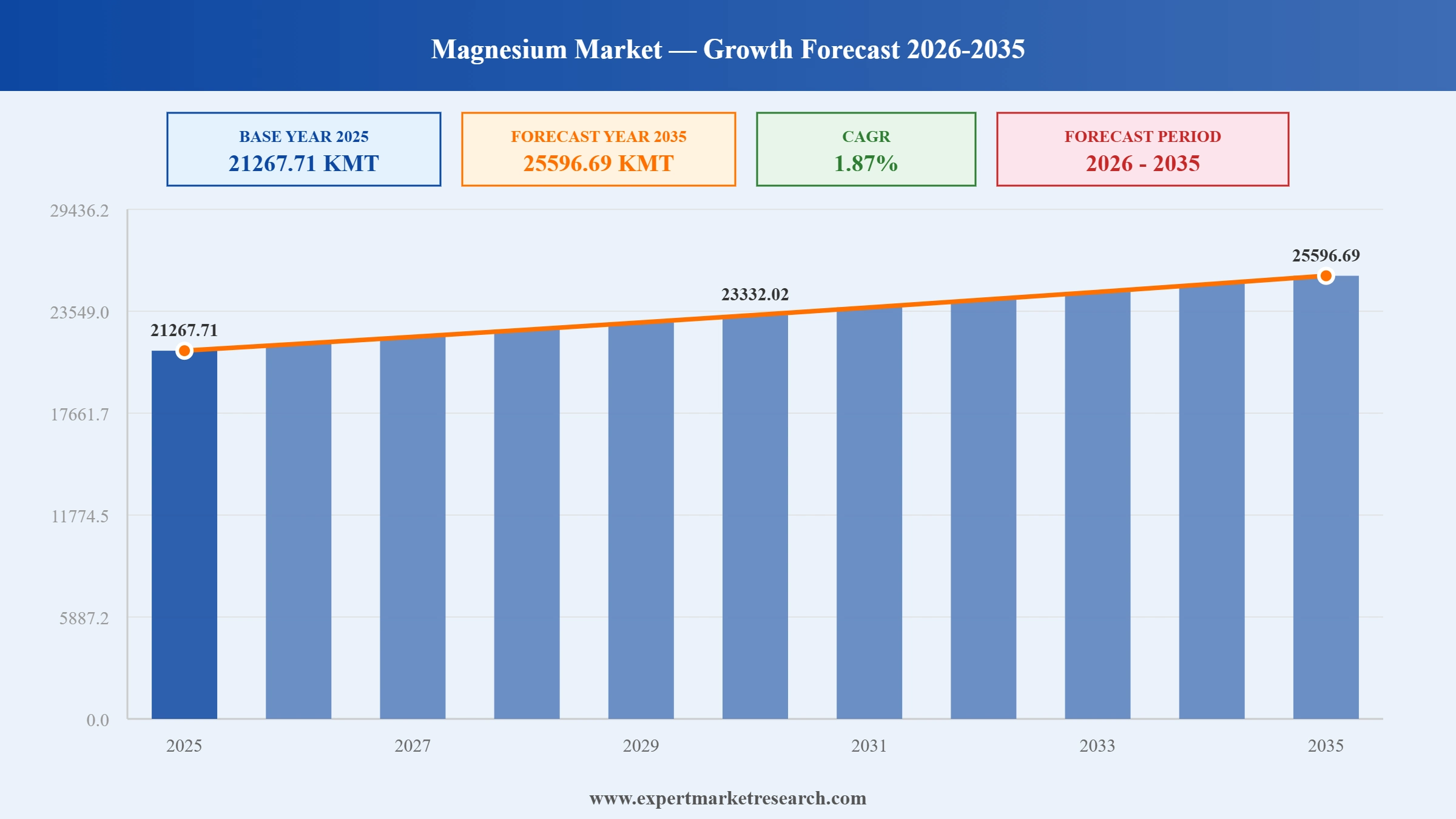

The global magnesium market size attained a volume of 21267.71 KMT in 2025. The industry is expected to grow at a CAGR of 1.87% during the forecast period of 2026-2035 to reach a volume of 25596.69 KMT by 2035. The market is witnessing a growing demand in the electric vehicle (EV) sector, a growing demand in the electric vehicle (EV) sector, driven by the increasing demand for lightweight materials that enhance vehicle efficiency and performance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Magnesium market is being shaped by EV-driven lightweighting demand, efforts to diversify supply chains away from China, expanding industrial applications for magnesium compounds, and growing adoption in emerging market steel and construction sectors.

Magmec and SMS Group signed a Memorandum of Understanding to develop a magnesium metal production facility in the United Arab Emirates. The planned facility aims to establish domestic magnesium supply infrastructure in the Middle East, a region that has historically relied on imports for its magnesium requirements. The collaboration between Magmec and the globally recognized SMS Group for metals and industrial plant engineering reflects the growing strategic interest in building regional magnesium production capacity to serve the Gulf's expanding aluminum, automotive, and industrial sectors while reducing dependence on Chinese supply.

Martin Marietta Materials closed its acquisition of Premier Magnesia, strengthening its position in the United States' natural and synthetic magnesia products market. The deal expands Martin Marietta's specialty materials portfolio with Premier Magnesia's established production assets and customer relationships in dead-burned and caustic calcined magnesia segments, which serve refractory, agricultural, and environmental treatment end markets. The acquisition reinforces Martin Marietta's strategic ambition to deepen its presence across multiple magnesium compound application categories within the North American market.

Verde Magnesium, backed by US investor Amerocap, was awarded a mining license in Romania and announced plans to invest USD 1 billion in a former magnesium mine near Oradea. The facility is expected to commence production by 2027, with the capacity to supply up to 90,000 tons of magnesium per year, potentially covering approximately 50% of the European Union's annual magnesium demand. The investment represents Europe's most significant attempt to restart domestic magnesium mining in over a decade, directly addressing the EU's critical raw materials dependency on Chinese imports and supporting regional supply chain resilience.

Great Wall Motor and Baowu Magnesium Technology Co., Ltd. established a strategic cooperation framework and a joint laboratory focused on advancing lightweight magnesium alloy applications in new energy vehicles (NEVs). The collaboration targets the development of high-performance magnesium alloy components for mass-produced NEV platforms, supporting China's automotive industry ambition to reduce vehicle weight and extend battery range. The partnership aligns with broader industry trends where Chinese automakers are actively integrating magnesium alloys into structural and non-structural components to improve energy efficiency in the rapidly growing NEV segment.

Tenova partnered with PT Tata Metal Lestari to install a hot-dip galvanizing line at its Sadang Plant in Indonesia, with a 250,000-ton annual production capacity for Zinc-Aluminum-Magnesium (Zn-Al-Mg) coated coils. This investment reflects the growing industrial adoption of ZAM-coated steel, which uses magnesium as a critical alloying element to deliver superior corrosion resistance and extended product lifespan compared to conventional galvanized coatings. The project underscores magnesium's expanding role as an essential alloying input in the Southeast Asian steel processing and construction materials sector.

The electric vehicle revolution is one of the most powerful structural demand drivers for magnesium, given the metal's exceptional strength-to-weight ratio, which is critical for extending battery range and improving vehicle energy efficiency. As OEMs shift production toward EVs, magnesium alloys are being increasingly specified for body panels, instrument panels, powertrain housings, and structural reinforcements. China's domestic NEV production scale is particularly significant, with leading automakers achieving up to 19 kg of magnesium alloy per vehicle in mass-produced models. The global magnesium market growth is directly tied to this electrification wave. In March 2025, Great Wall Motor formalized its partnership with Baowu Magnesium to accelerate lightweight magnesium alloy integration across its NEV platforms through a dedicated joint research laboratory.

China's dominance of global primary magnesium production, controlling an estimated 85-90% of output, has long posed supply chain vulnerability risks for consuming industries in Europe, North America, and Japan. The 2021 Chinese energy crisis, which triggered a sharp production curtailment and global price spike, exposed the fragility of this single-source dependency and accelerated policy-driven efforts to develop alternative production capacities. Governments and private investors are now funding projects in Romania, Canada, Australia, and the UAE to establish competitive magnesium supply outside China. In April 2024, Verde Magnesium's USD 1 billion investment in Romania, targeting 90,000 tons per year of output by 2027, marked a pivotal step toward rebuilding European magnesium production capability.

Magnesium compounds, particularly magnesium oxide, magnesium chloride, and magnesium hydroxide, are seeing expanding industrial adoption across steel desulfurization, environmental waste treatment, agriculture, and construction materials. The increasing deployment of ZAM-coated steels incorporating magnesium as a corrosion-resistant alloying agent is creating new demand streams beyond traditional pure magnesium applications. In environmental applications, magnesium hydroxide is used for flue gas desulfurization and wastewater neutralization, while magnesium oxide plays a growing role in refractory materials for high-temperature industrial processes. The global magnesium market trends indicate that compound applications will account for a progressively larger share of total demand through 2035. In February 2025, Tenova and PT Tata Metal Lestari commissioned a 250,000-ton-per-year Zn-Al-Mg galvanizing line in Indonesia, illustrating this compound-driven demand expansion.

The global magnesium market is undergoing a period of strategic consolidation and capacity investment, as established players seek to broaden their product portfolios and new entrants attempt to challenge China's production dominance. Acquisitions, joint ventures, and greenfield investments are becoming increasingly prevalent as manufacturers respond to tightening supply conditions, rising demand from automotive and environmental sectors, and government incentives for critical mineral production outside China. The global magnesium market outlook indicates that companies with vertically integrated production capabilities and diversified geographic exposure will be best positioned to capture value through the forecast period. In July 2025, Martin Marietta Materials' acquisition of Premier Magnesia exemplified this consolidation trend, strengthening its specialty magnesia portfolio across natural and synthetic product lines in North America.

The Expert Market Research's report titled "Global Magnesium Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

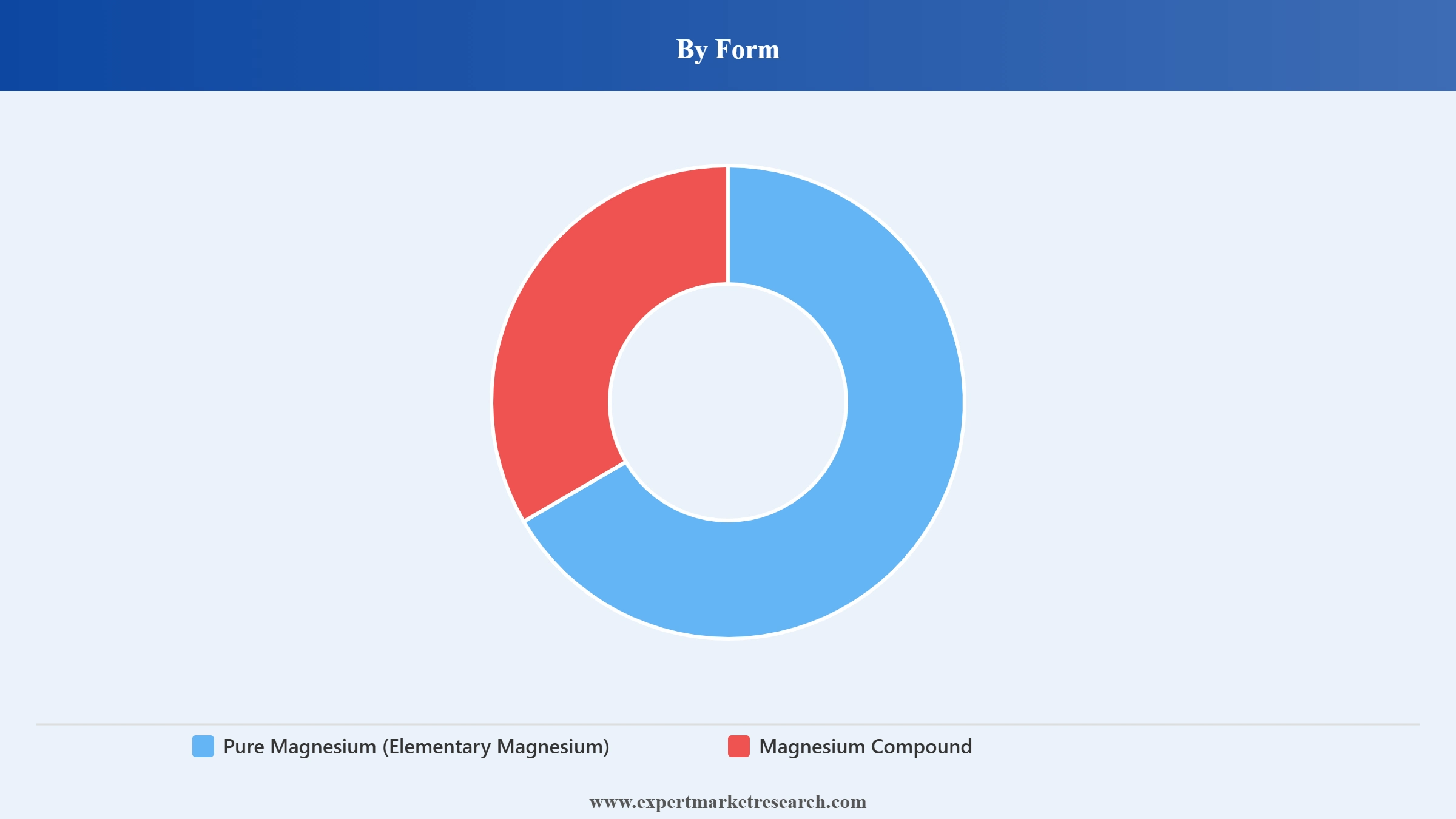

Market Breakup by Form

Key Insight: Magnesium compound holds the dominant revenue share in the global magnesium market, supported by its diverse industrial applications spanning agriculture, steel production, cement manufacturing, environmental treatment, and glass making. Magnesium oxide is the largest compound sub-type, accounting for significant volumes in refractory production and agricultural soil conditioning. Pure magnesium (elementary magnesium) is the critical segment for automotive, aerospace, and electronics manufacturing, where its lightweight and high-strength properties are essential. Primary magnesium, produced through thermal or electrolytic refining, commands the dominant share of elementary magnesium production, while secondary magnesium from recycling is growing at a higher CAGR of 3.96%, reflecting increasing circularity in metals manufacturing and lower carbon footprint compared to primary production.

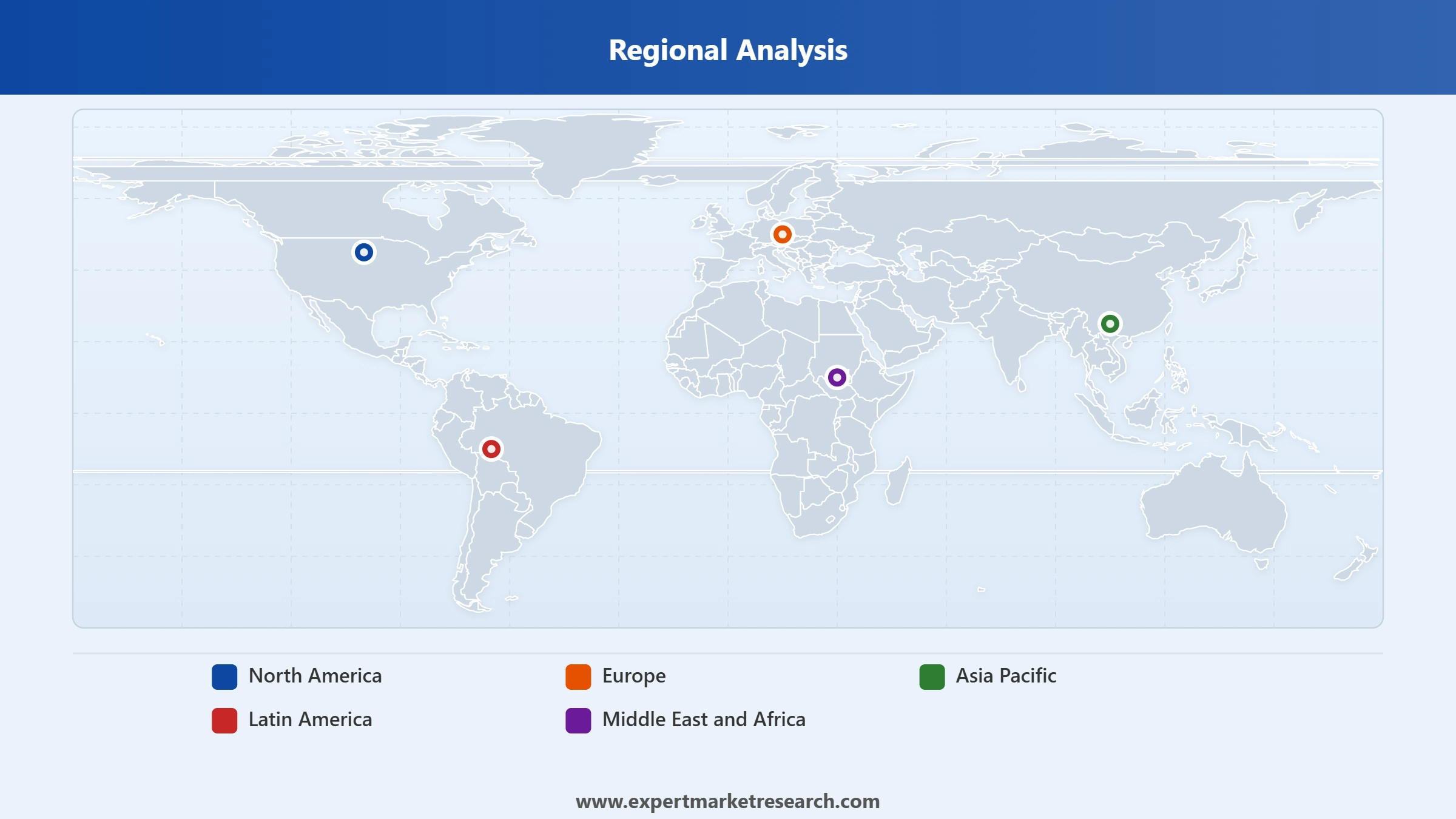

Market Breakup by Region

Key Insight: Asia Pacific leads the global magnesium market, accounting for approximately 45-48% of global production and consumption, dominated by China's vertically integrated thermal reduction supply chain. China's production of both primary magnesium metal and magnesium compounds for domestic and export markets underpins Asia Pacific's leadership position. Europe represents a significant consuming region, particularly for automotive and aerospace magnesium alloys, though it remains heavily import-dependent following the decline of its domestic magnesium production capacity. Middle East and Africa is the fastest-growing region in the global magnesium market, registering an estimated CAGR of 3.03%, driven by industrial expansion in Gulf states, growing steel production in Africa, and new investment in regional magnesium production infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Magnesium compound holds the dominant market share by form in the global magnesium market, reflecting its extensive industrial footprint across agricultural fertilizers, steel refractory materials, environmental treatment chemicals, cement additives, and specialty industrial applications. Magnesium oxide, the most widely produced compound type, leads within the compound segment due to its irreplaceable role in steel furnace lining and its broad applications across agriculture and environmental sectors. The pure magnesium (elementary magnesium) segment, while representing a smaller share of total volume, commands premium pricing for high-purity alloy and die-casting grades used in automotive and aerospace manufacturing, making it the critical value driver for premium-grade producers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In terms of application, alloy production accounts for the largest share of pure magnesium consumption globally, driven by the deep integration of magnesium-aluminum alloys into automotive manufacturing. Die casting is the application registering the strongest growth trajectory at a CAGR of 3.83%, as precision magnesium die-cast components become increasingly standard in vehicle lightweighting and consumer electronics. For magnesium compounds, the agricultural and steel industry applications together command the largest combined share, supported by the structural and non-substitutable nature of magnesia in steelmaking refractories and the growing global demand for secondary nutrient crop nutrition programs addressing soil magnesium deficiencies in intensively farmed regions.

Asia Pacific dominates the global magnesium market, with China accounting for the overwhelming majority of primary magnesium metal production through the thermal Pidgeon reduction process, which is concentrated in Shaanxi, Shanxi, and Xinjiang provinces. China's cost-competitive production, abundant dolomite and magnesite mineral resources, and integrated supply chains supporting its automotive, electronics, and construction sectors have cemented its market leadership. However, China's dominance also creates supply concentration risks that importing regions are actively addressing through supply diversification investments. Japan, South Korea, and India represent additional Asia Pacific consumption centers, with Japan and Korea in particular driving premium alloy demand from their automotive and electronics manufacturing industries.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe is the world's second-largest consuming region for magnesium, particularly for automotive-grade alloys and specialty magnesium compounds used in refractories, cement, and environmental applications. European demand is primarily satisfied through imports, making it the most import-dependent major region and a key driver of supply diversification investments such as Verde Magnesium's planned Romanian production facility. Germany, the UK, France, Italy, and Poland are the leading European markets, driven by automotive manufacturing, specialty chemicals, and steel production. The EU's Critical Raw Materials Act has formally recognized magnesium as a strategic raw material, prompting policy support for domestic production investments and strategic stockpiling.

The global magnesium market is highly concentrated at the primary production level, with Chinese manufacturers controlling the dominant share of global primary magnesium output. Outside China, a small number of specialized producers in North America, Europe, Latin America, and Australia serve regional and niche markets. The magnesium compound segment is more geographically diversified, with significant producers in Greece, Canada, Netherlands, China, and the United States competing across magnesia, magnesium chloride, and magnesium sulfate product lines. Key competitive strategies include capacity expansion, supply chain integration, product grade diversification, and partnerships with major end-use industries in automotive, steel, and agriculture.

The competitive landscape is evolving as new entrants invest in primary production outside China to capitalize on supply diversification demand from European and North American industries. Companies with established relationships with automotive OEMs and strategic investments in high-purity magnesium alloy grades are particularly well-positioned. Environmental and sustainability credentials, including low-carbon production processes and recycled magnesium capabilities, are becoming increasingly important differentiators in premium industrial and automotive markets.

US Magnesium LLC is the largest primary magnesium producer in the United States, extracting magnesium from the brine of the Great Salt Lake in Utah using an electrolytic production process. The company serves domestic automotive, steel, and aerospace industries with primary magnesium metal, providing a critical domestic supply source in a market otherwise heavily reliant on Chinese imports. US Magnesium's position as the sole significant US primary magnesium producer gives it strategic importance in the context of North American supply chain security for critical materials.

NikoMag is a Russian magnesium company engaged in the production of magnesium metal and magnesium-based compounds, serving industrial and chemical sectors. The company operates within Russia's magnesium production sector, utilizing the country's mineral resources for both domestic consumption and export. NikoMag's product portfolio serves applications in the automotive, aerospace, and chemical industries, and the company is positioned within the competitive landscape of non-Chinese magnesium suppliers serving global markets.

Martin Marietta Materials, Inc. is a US-based publicly listed aggregates and specialty materials company headquartered in Raleigh, North Carolina. Following its July 2025 acquisition of Premier Magnesia, the company strengthened its presence in the natural and synthetic magnesia products market, adding dead-burned and caustic calcined magnesia to its specialty products portfolio. Martin Marietta serves refractory, agricultural, and environmental end markets with its expanded magnesia product line, reinforcing its position as a leading North American magnesia supplier.

Nedmag B.V. is a Netherlands-based magnesium compound producer specializing in magnesium chloride and related products extracted from subsurface brine deposits in Groningen, the Netherlands. The company is one of Europe's primary sources of high-purity magnesium chloride, serving the chemical, de-icing, dust suppression, and food-grade markets. Nedmag's integrated extraction-to-product supply chain and European market proximity give it a competitive advantage in serving the EU's chemical and industrial sectors with locally sourced magnesium chloride formulations.

Other key players in the market are Grecian Magnesite S.A., Hebei Meishen Technology Co. Ltd., Yingkou Magnesite Chemical Ind Group Co. Ltd. (Sinomagchem), Baymag Inc., Rima Industrial S.A., Shaanxi Yulin Magnesium Industry (Group) Co. LTD., Baowu Magnesium Technology Co. Ltd., Shanxi Yinguang Huasheng Magnesium Industry Co. Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the dynamic Global Magnesium Market with our comprehensive 2026 to 2035 forecast report. Whether you are navigating supply chain risk from China dependency, assessing investment opportunities in non-Chinese magnesium production, evaluating demand from EV lightweighting and environmental sectors, or benchmarking against the competitive landscape, this report delivers the data-driven intelligence you need. Download your free sample today and explore the opportunities shaping the future of the global magnesium industry.

Upto 15% Off

USD

$3499 $3149

$5599 $5039

$6999 $5949

$8459 $7190

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate volume of 21267.71 KMT.

The market is projected to grow at a CAGR of 1.87% between 2026 and 2035.

The key players in the market report include US Magnesium LLC, NikoMag, Martin Marietta Materials, Inc., Nedmag B.V., Grecian Magnesite S.A., Hebei Meishen Technology Co., Ltd., Yingkou Magnesite Chemical Ind Group Co., Ltd. (Sinomagchem), Baymag Inc., Rima Industrial S.A., Shaanxi Yulin Magnesium Industry (Group) Co., LTD., Baowu Magnesium Technology Co., Ltd., and, Shanxi Yinguang Huasheng Magnesium Industry Co., Ltd., among others..

Magnesium compound is a dominant form of the market due to its wide applications in agriculture, construction, environmental treatment, and industrial manufacturing.

Key strategies driving the magnesium market include technological innovation, capacity expansion, vertical integration, recycling initiatives, and sustainability-focused practices aimed at reducing emissions, lowering costs, and strengthening supply chain resilience.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Form |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,499

USD 3,149

tax inclusive*

Single User License

One User

USD 5,599

USD 5,039

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,459

USD 7,190

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.