Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

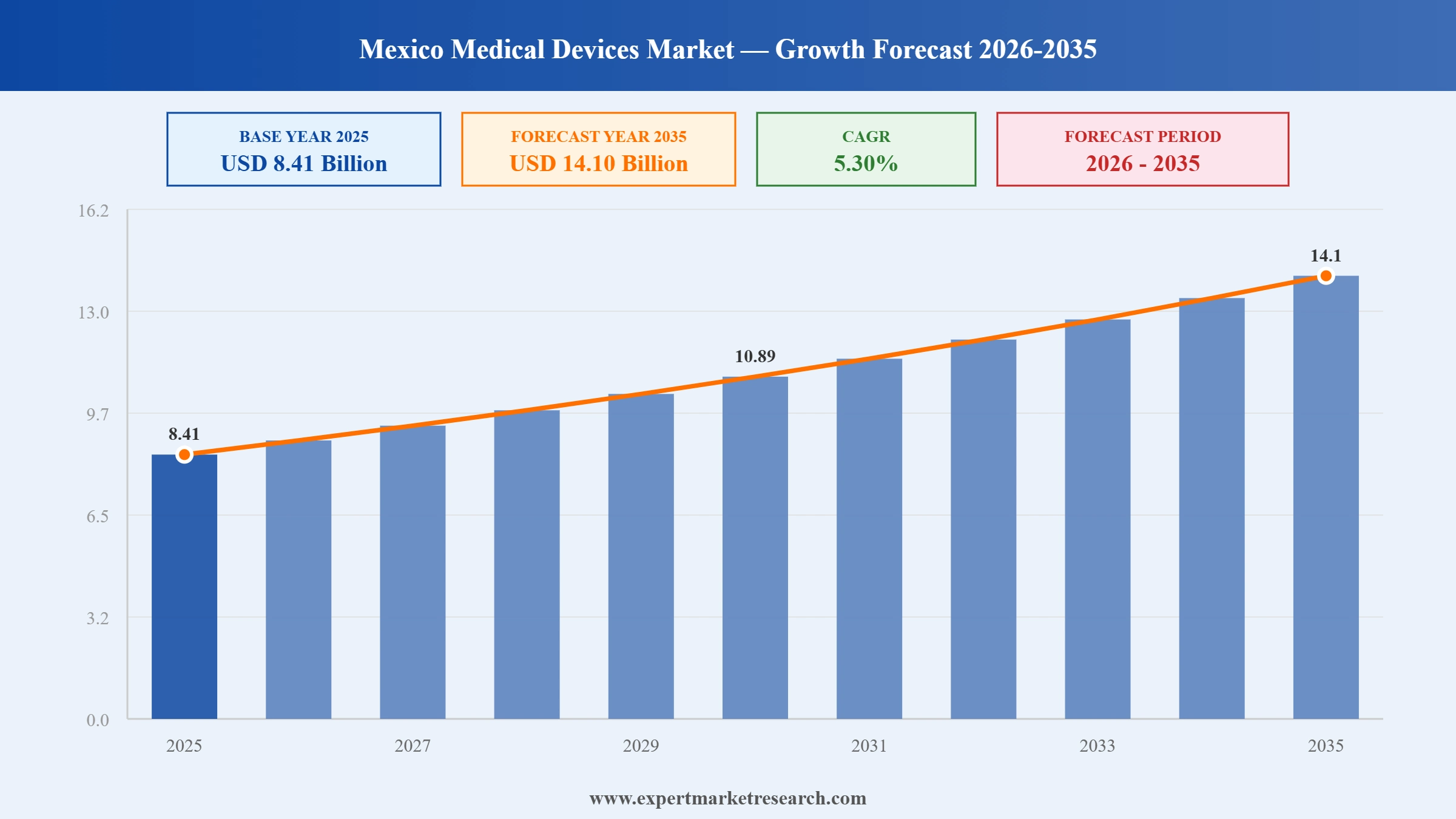

The Mexico medical devices market was valued at USD 8.41 Billion in 2025. It is poised to grow at a CAGR of 5.30% during the forecast period of 2026-2035, and reach USD 14.10 Billion by 2035. The market growth is driven by expanding healthcare infrastructure, rising chronic disease burden, increasing medical device manufacturing activities, growing demand for advanced diagnostics, technological innovation, and greater investment in healthcare modernization initiatives.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market reached a value of approximately USD 8.41 Billion in 2025. The market is supported by expanding healthcare infrastructure, rising healthcare expenditure, and increasing demand for advanced diagnostic and therapeutic technologies. Growth in chronic disease prevalence, an aging population, and greater access to healthcare services are driving device adoption across hospitals and clinics. Mexico also serves as a major manufacturing hub for medical devices, benefiting from strong export capabilities and international investment. Technological advancements, increasing private healthcare participation, and supportive regulatory developments are further encouraging market expansion. Additionally, growing demand for minimally invasive procedures continues to stimulate innovation and product innovation across the country.

Market Breakup by Product

The product segment categorizes medical devices based on clinical functions and therapeutic applications across healthcare settings. It encompasses diagnostic, monitoring, imaging, surgical, and treatment technologies supporting diverse patient care requirements.

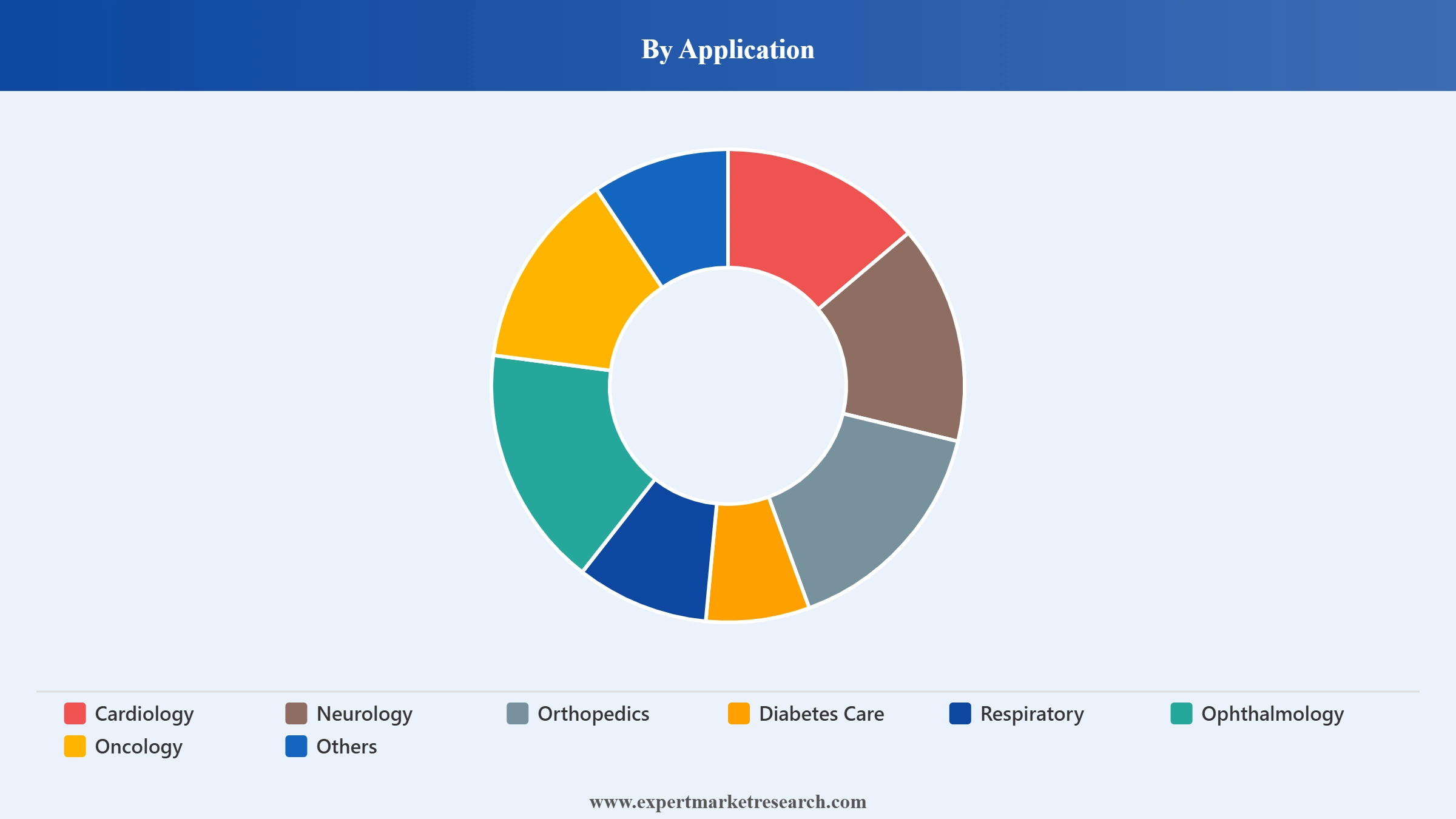

Market Breakup by Application

The application segment classifies medical devices according to disease areas and clinical specialties driving utilization. Demand patterns are influenced by treatment requirements, diagnostic needs, disease prevalence, and healthcare service expansion.

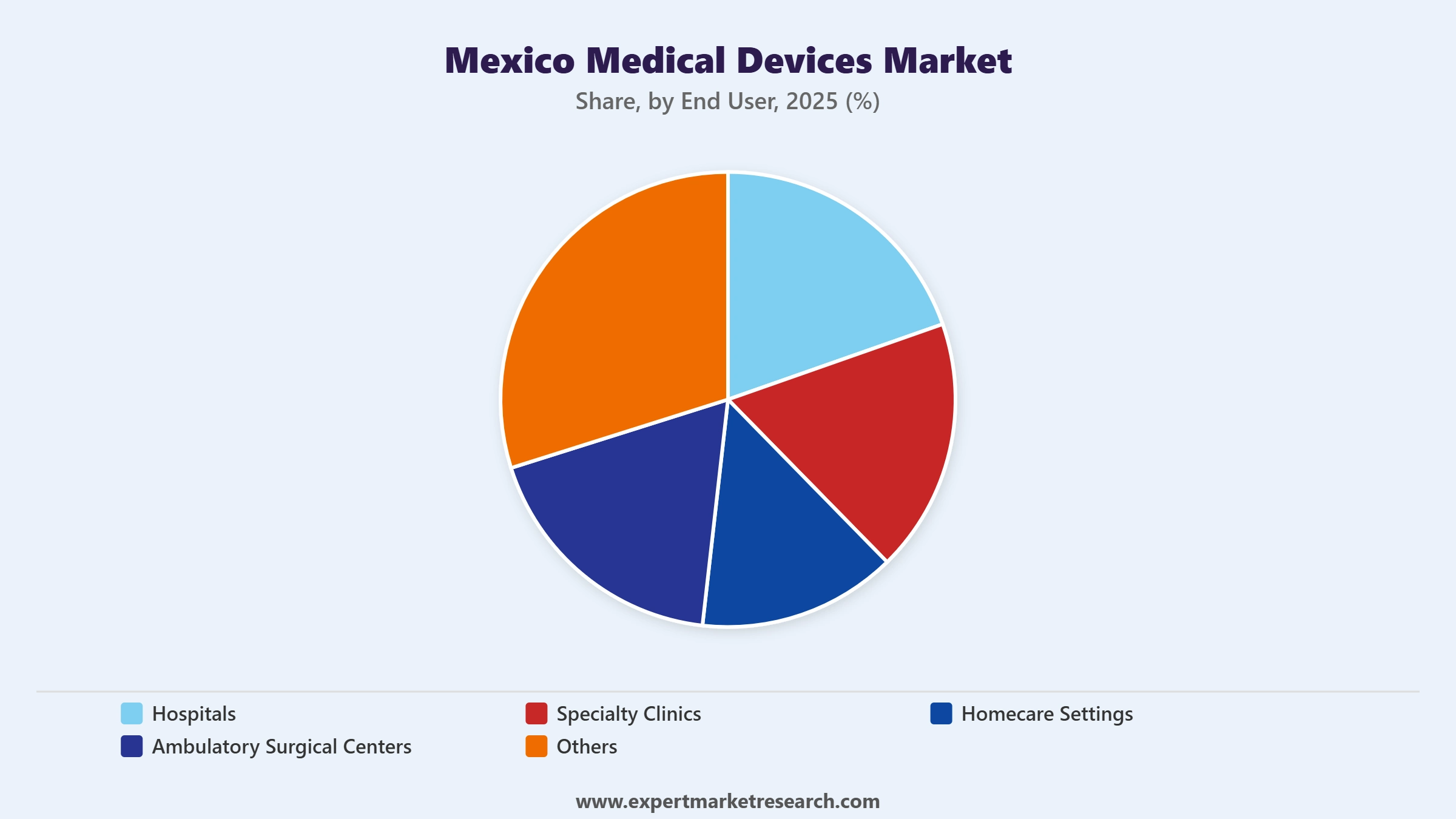

Market Breakup by End User

The end-user segment evaluates medical device adoption across healthcare delivery settings. Purchasing decisions, utilization rates, and technology investments vary according to care intensity, patient volume, treatment complexity, and service capabilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Analysis Type | Factors | Example |

| Market Drivers | Rising chronic disease screening, expansion of public healthcare coverage, modernization of diagnostic infrastructure, and higher demand for advanced imaging and treatment equipment. | For instance, in June 2026, Mexico announced a 21 billion peso IMSS-Bienestar investment plan through 2027, covering medical equipment, hospitals, and healthcare workforce expansion. |

| Market Restraints | Public procurement delays, tender cancellations, regulatory scrutiny, supplier verification issues, and compliance-related cost pressure for device manufacturers. | For instance, in May 2025, Mexico annulled the 2025-2026 consolidated purchase of drugs and medical devices after legal and procedural irregularities were identified in the procurement process. |

| Market Opportunities | Nearshoring growth, faster device authorizations, demand for local manufacturing, digital health adoption, and rising need for safer, connected, and better-monitored medical technologies. | For instance, in April 2026, COFEPRIS reported 608 new health input authorizations during the first quarter, including approvals linked to clinical trials, medicines, and medical devices. |

This section analyzes key factors influencing market growth, including healthcare infrastructure expansion, rising chronic disease prevalence, medical technology advancements, manufacturing investments, regulatory developments, healthcare spending trends, and increasing demand for diagnostic and therapeutic devices.

Public Healthcare Investments Strengthening Market Outlook

Rising chronic disease screening, expanding public hospital capacity, and demand for advanced diagnostics are supporting market growth. For instance, in June 2026, the federal government announced a 21 billion peso IMSS-Bienestar plan running through 2027, covering medical equipment, hospitals, and health workforce expansion. The measure should lift procurement volumes during the forecast period, strengthen access to diagnostic and treatment technologies, and support suppliers serving public healthcare modernization across underserved regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Procurement Uncertainty to Restrain Market Expansion

Rising demand for hospital supplies, expanding public healthcare coverage, and stronger device localization are supporting Mexico’s medical technology ecosystem, but procurement uncertainty remains a major market restraint. For instance, in May 2025, authorities annulled the 2025-2026 consolidated purchase of drugs and medical devices after finding legal and procedural irregularities in the Birmex process. During the forecast period, delayed tenders and stricter supplier verification may slow public-sector orders, affect delivery timelines, and raise compliance costs for manufacturers serving public healthcare facilities.

Public Healthcare Investments Strengthen Market Growth

Public-sector modernization, oncology demand, and replacement of aging diagnostic assets are raising market value. For instance, in February 2026, the presidency announced the purchase of 816 high-technology medical devices, including CT scanners, mammography systems, MRI units, linear accelerators, PET-CT equipment, and gamma cameras, with an investment of 11.257 billion pesos. The program should expand installed capacity during the forecast period, improve specialized care access, and create stronger demand for maintenance, training, and consumables.

Nationwide Regulatory Authorizations Accelerate Market Development

Regulatory simplification, digital health adoption, and cross-border supply-chain integration are shaping Mexico’s market trends. For instance, in January 2026, Mexico amended the General Health Law, covering digital health, sanitary regulation, infrastructure, medical devices, technovigilance, and public procurement. The reform should support clearer compliance planning during the forecast period, improve monitoring of connected technologies, and help domestic and foreign companies bring safer, better-documented products into clinical use across public and private healthcare channels.

Cardiology Likely to Dominate the Market Segment by Application

The cardiology segment held around 27% share in the historical period. The rising prevalence of cardiovascular diseases, increasing demand for early diagnosis, and expanding use of advanced cardiac monitoring technologies are driving strong clinical adoption. Healthcare providers are increasingly investing in precision diagnostic and therapeutic solutions to improve patient outcomes and reduce mortality risks. Continuous innovation in minimally invasive cardiac procedures and remote monitoring systems is further strengthening utilization patterns. Growing focus on preventive healthcare and hospital-based cardiac care services supports sustained demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Founded in 1949 and headquartered in Galway, Ireland, Medtronic is a global medical technology company. Its portfolio in the medical devices market includes cardiovascular, neuroscience, surgical, diabetes management, patient monitoring, and respiratory care solutions.

Established in 1886 and headquartered in New Brunswick, New Jersey, United States, Johnson & Johnson MedTech develops advanced healthcare technologies. Its portfolio includes surgical systems, orthopedic implants, cardiovascular devices, electrophysiology solutions, and vision care products.

Founded in 1996 and headquartered in Bad Homburg, Germany, Fresenius Medical Care specializes in kidney care technologies. Its medical devices portfolio includes dialysis machines, dialysis consumables, renal therapies, and related patient care solutions.

Established in 1888 and headquartered in Abbott Park, Illinois, United States, Abbott is a diversified healthcare company. Its medical devices portfolio includes cardiovascular products, diabetes care systems, diagnostic equipment, neuromodulation technologies, and structural heart devices.

Other key players in the market include GE Healthcare, Koninklijke Philips N.V., Siemens Healthcare GmbH, and 3M Company.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

This report is developed through a robust mixed-methods research design combining:

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Application |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.