Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

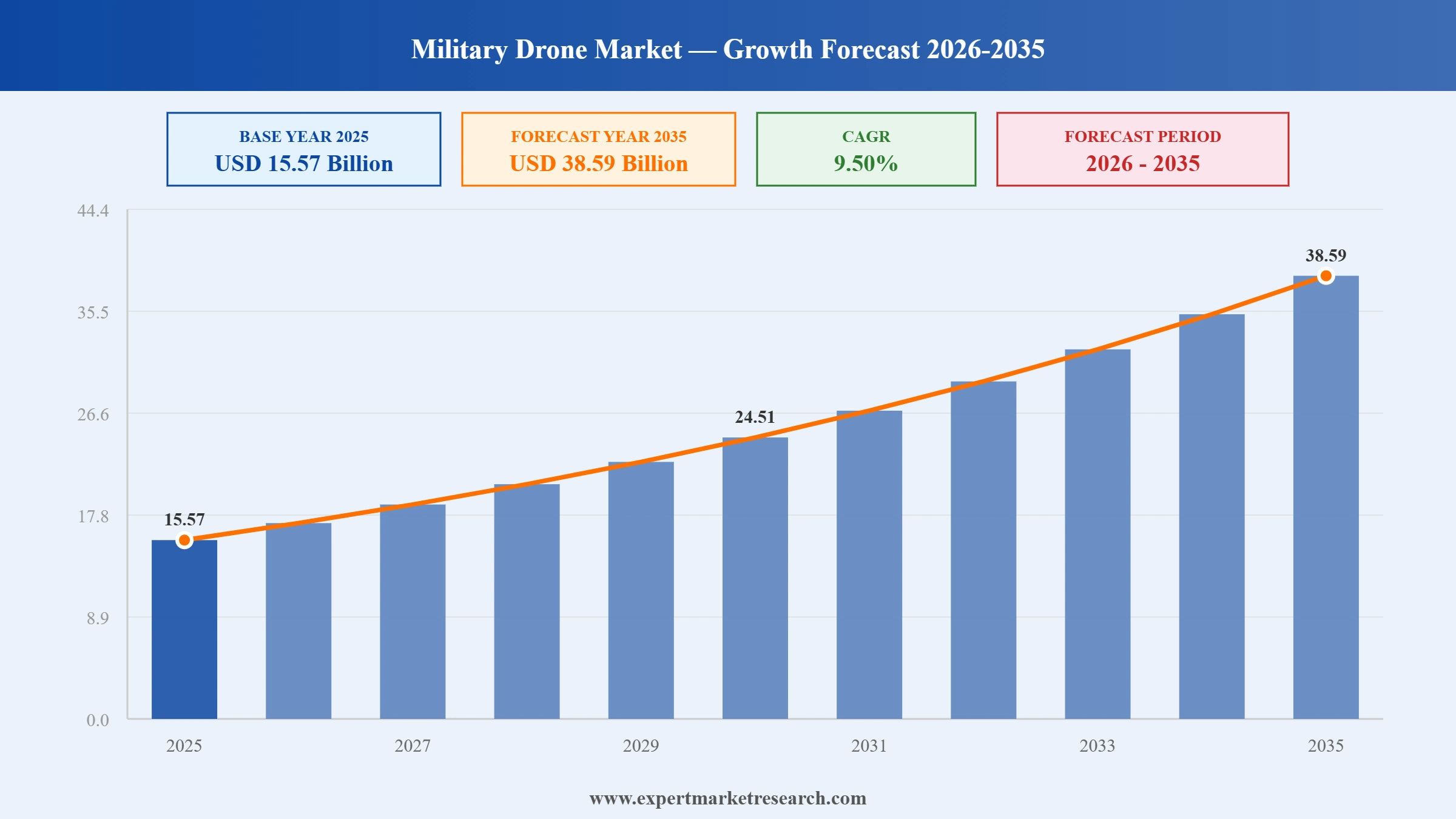

The global military drone market reached a value of USD 15.57 Billion at 2025 and is projected to expand at a CAGR of around 9.50% during the forecast period of 2026-2035 and expected to reach USD 38.59 Billion by 2035. With surging global defence budgets driving accelerated UAV procurement, the rapid integration of artificial intelligence and autonomous technologies into military platforms, expanding deployment of Beyond Visual Line of Sight drone systems for long-range operations, and intensifying geopolitical tensions reshaping national defence strategies.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global military drone market is being shaped by a convergence of escalating geopolitical pressures, rapid advances in autonomous and AI-enabled systems, and a generational shift in defence procurement toward unmanned platforms at scale. Major defence establishments are accelerating investment across fixed wing surveillance drones, loitering munitions, and collaborative combat aircraft, while strategic acquisitions and programme awards are concentrating capability development among established prime contractors and a new generation of defence technology companies.

The US Air Force officially designated Northrop Grumman's Talon drone as YFQ-48A in December 2025, making it the third Collaborative Combat Aircraft to receive formal designation, underscoring the programme's progress toward fielding semi-autonomous wingman systems alongside crewed fighter aircraft.

The US Army awarded AeroVironment an USD 874 million contract in December 2025 to support foreign military sales of unmanned aerial systems and counter-drone technology across allied and partner nations, covering platforms from Groups 1 to 3.

The US Navy awarded Collaborative Combat Aircraft drone contracts to five major defence companies including Boeing, General Atomics, Lockheed Martin, Northrop Grumman, and Anduril in September 2025, advancing carrier-based autonomous wingman capability development for maritime operations.

AeroVironment completed its USD 4.1 billion acquisition of BlueHalo in May 2025, creating a diversified global defence technology company with expanded capabilities in directed energy, space, electronic warfare, and counter-unmanned aerial system technologies.

Surging global defence budgets are driving demand in the global military drone market. In March 2025, China announced a national defence budget of USD 249 billion, while NATO nations accelerate UAV procurement to modernise armed forces and expand unmanned capabilities.

Artificial intelligence is reshaping the global military drone market. In February 2025, Anduril's YFQ-44A demonstrated flying with two different AI pilots in a single flight, showcasing how software-centric autonomy is transforming military drone mission profiles and combat strike capability.

Beyond Visual Line of Sight capabilities are the fastest-growing range category in the global military drone market. Armed forces worldwide are investing in BVLOS platforms for persistent surveillance, long-range strike, and logistics support in contested and remote operational environments.

Intelligence, surveillance, reconnaissance, and targeting applications drive the dominant share of procurement across the global military drone market. Persistent ISR capability, enabled by long-endurance fixed-wing platforms, remains central to shaping defence procurement priorities across major military establishments worldwide.

Asia Pacific is the fastest-growing region in the global military drone market, driven by border tensions, military modernisation, and growing UAV procurement across China, India, and Southeast Asia as nations seek to expand unmanned surveillance and combat defence capabilities.

The report of Expert Market Research’s titled “Global Military Drone Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

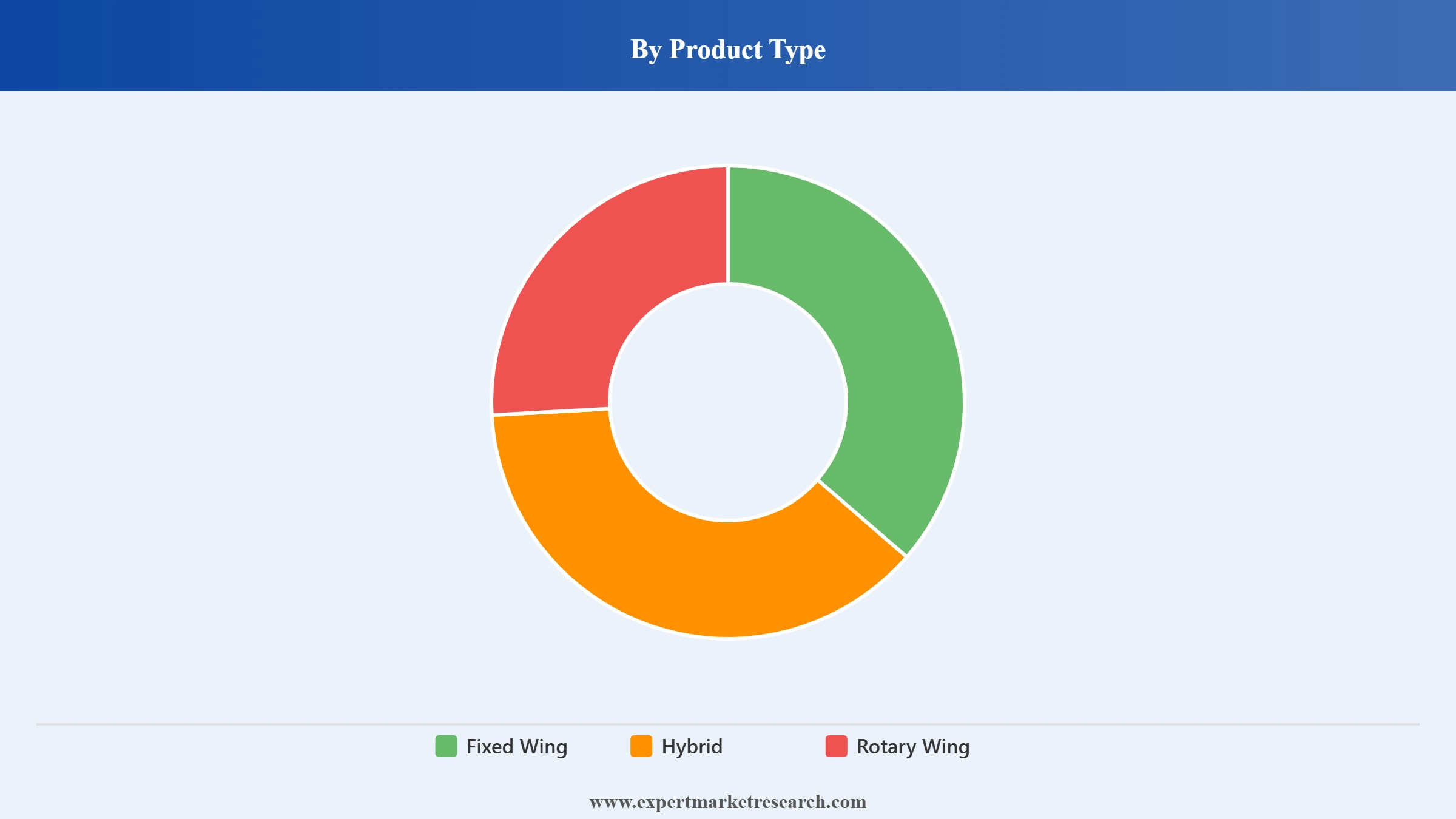

Market Breakup by Product Type

Key Insight: Fixed wing drones dominate the global military drone market, driven by their superior endurance, operational range, and payload capacity compared to other configurations. High-altitude and medium-altitude long-endurance platforms such as the MQ-9 Reaper are central to global ISR and strike operations. Rotary wing drones are gaining traction in tactical environments where vertical takeoff and landing, hover functionality, and close-range precision are essential. Hybrid configurations are an emerging category bridging endurance and flexibility across diverse military mission profiles.

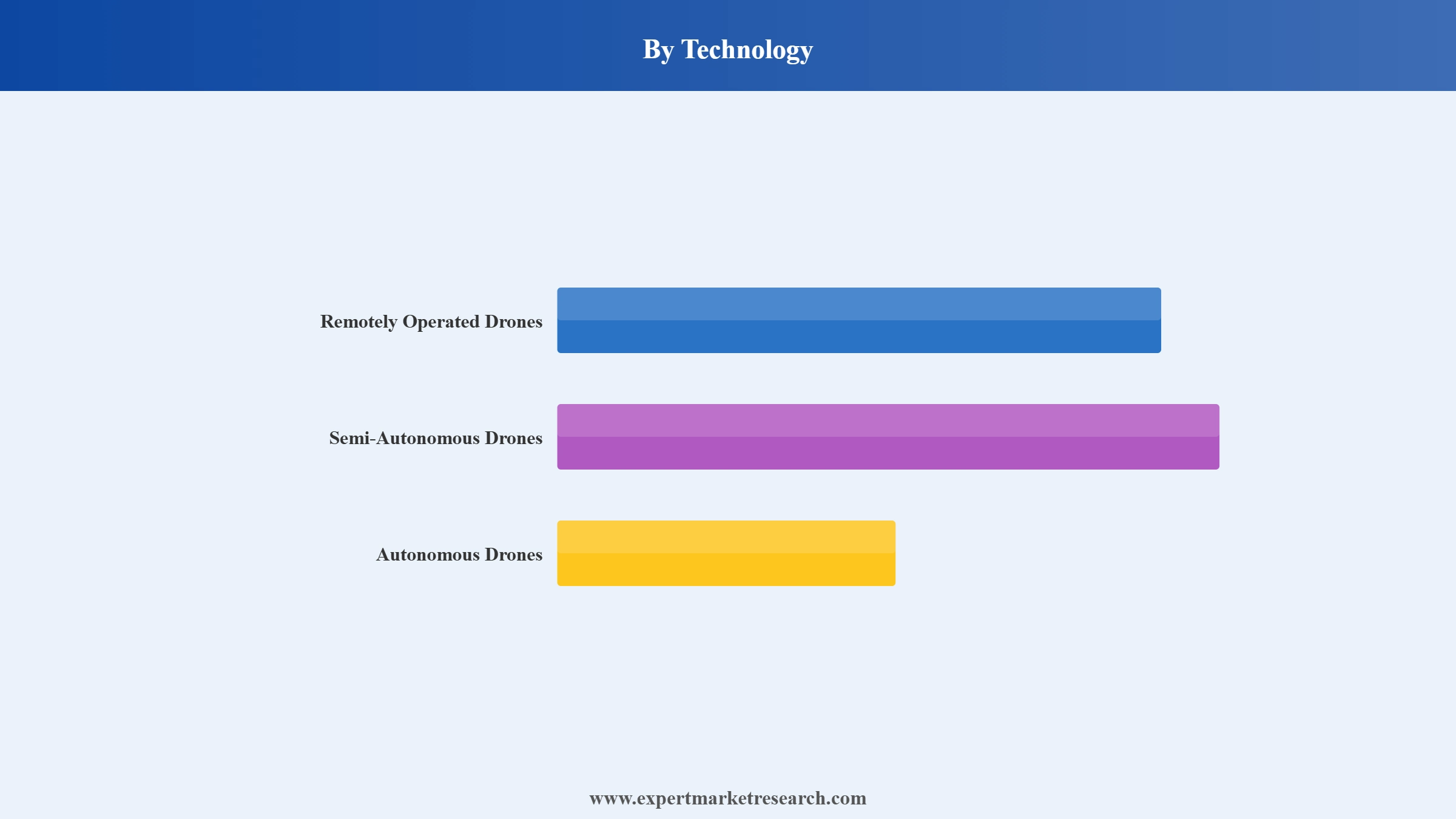

Market Breakup by Technology

Key Insight: Remotely operated drones represent the largest technology segment in the global military drone market, supported by decades of operational experience and established ground control station infrastructure. Semi-autonomous and fully autonomous drones are the fastest-growing sub-categories, powered by advances in AI, machine learning, and onboard processing. The US Air Force's Collaborative Combat Aircraft programme illustrates the growing investment in autonomous systems designed to extend the reach of crewed fighters in contested environments.

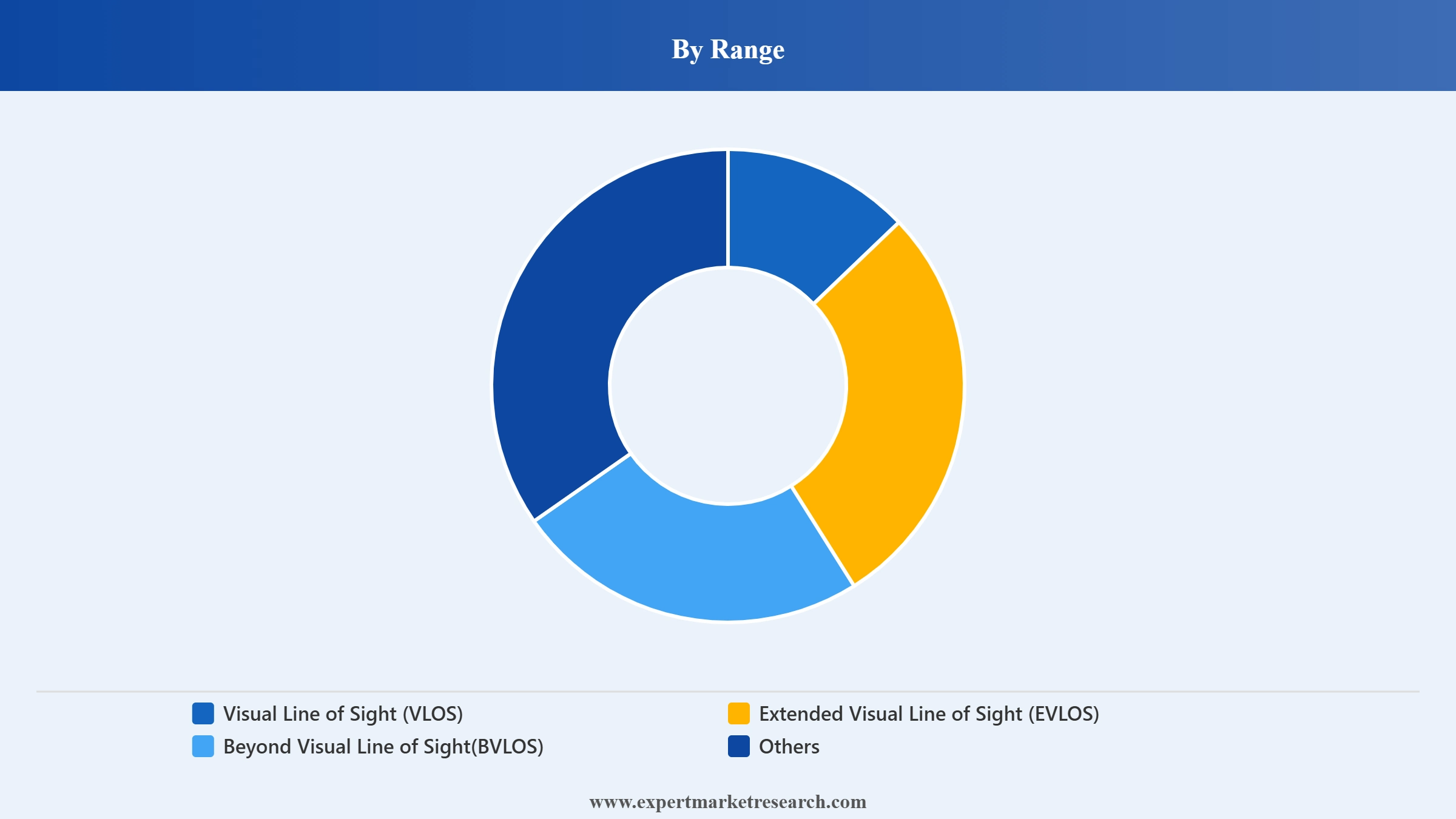

Market Breakup by Range

Key Insight: Beyond Visual Line of Sight operations represent the fastest-growing range category in the global military drone market, enabling persistent surveillance, long-range precision strike, and logistics operations at distances far exceeding operator sightlines. BVLOS capability is essential for theatre-level operations, driving investment in satellite communications and encrypted datalinks. Visual Line of Sight platforms retain relevance for short-range tactical operations, training, and counter-drone applications in confined or urban operational environments.

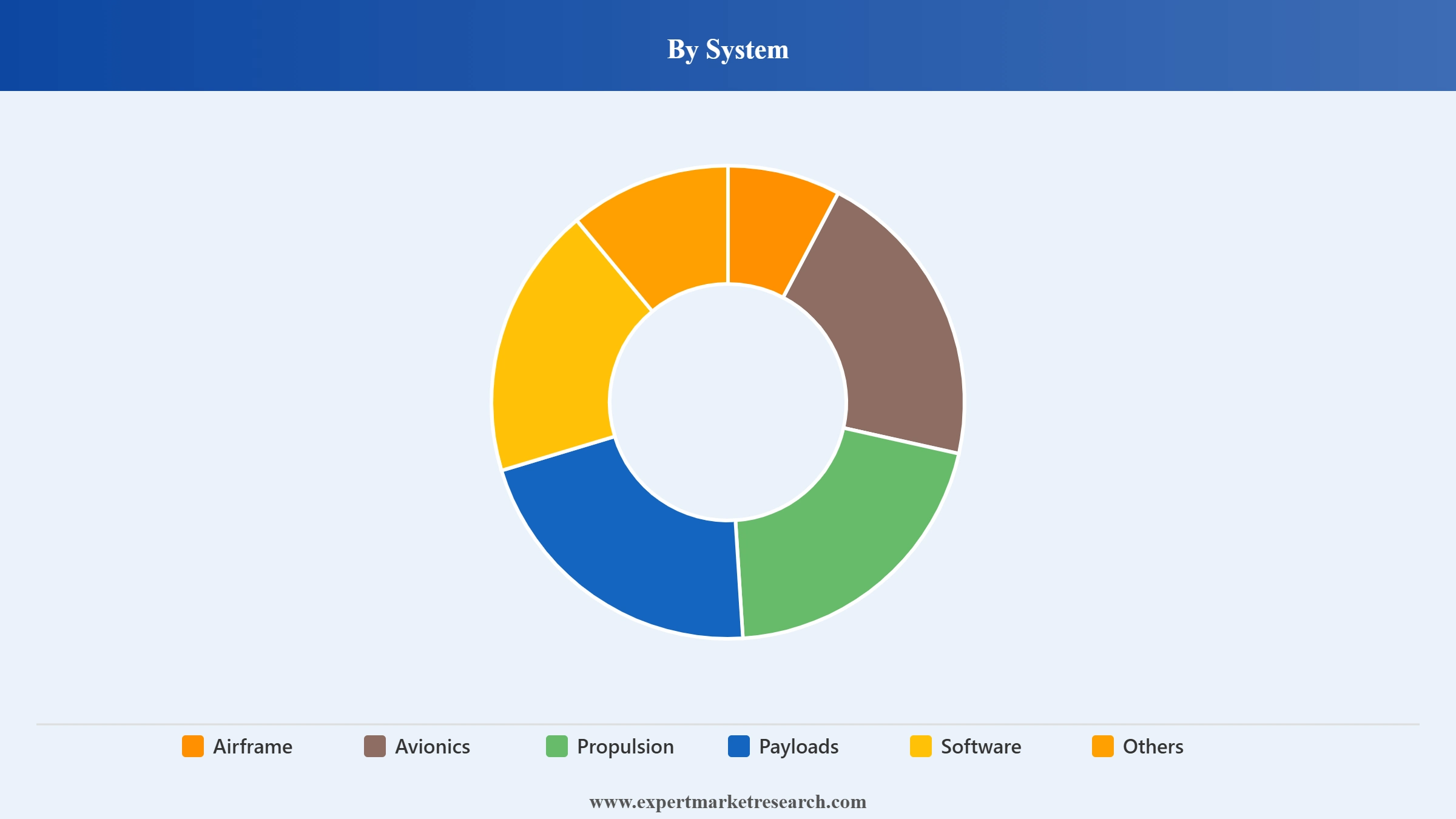

Market Breakup by System

Key Insight: Payloads represent one of the highest-value system components in the global military drone market, encompassing electro-optical and infrared sensors, radar, LiDAR, CBRN sensors, and electronic warfare equipment that determine a platform's mission versatility. Airframe and propulsion are foundational structural segments, while avionics and software are growing rapidly as digital architecture and AI-driven flight management become central to next-generation drone design. Integrated payload systems increasingly command a significant share of total platform value.

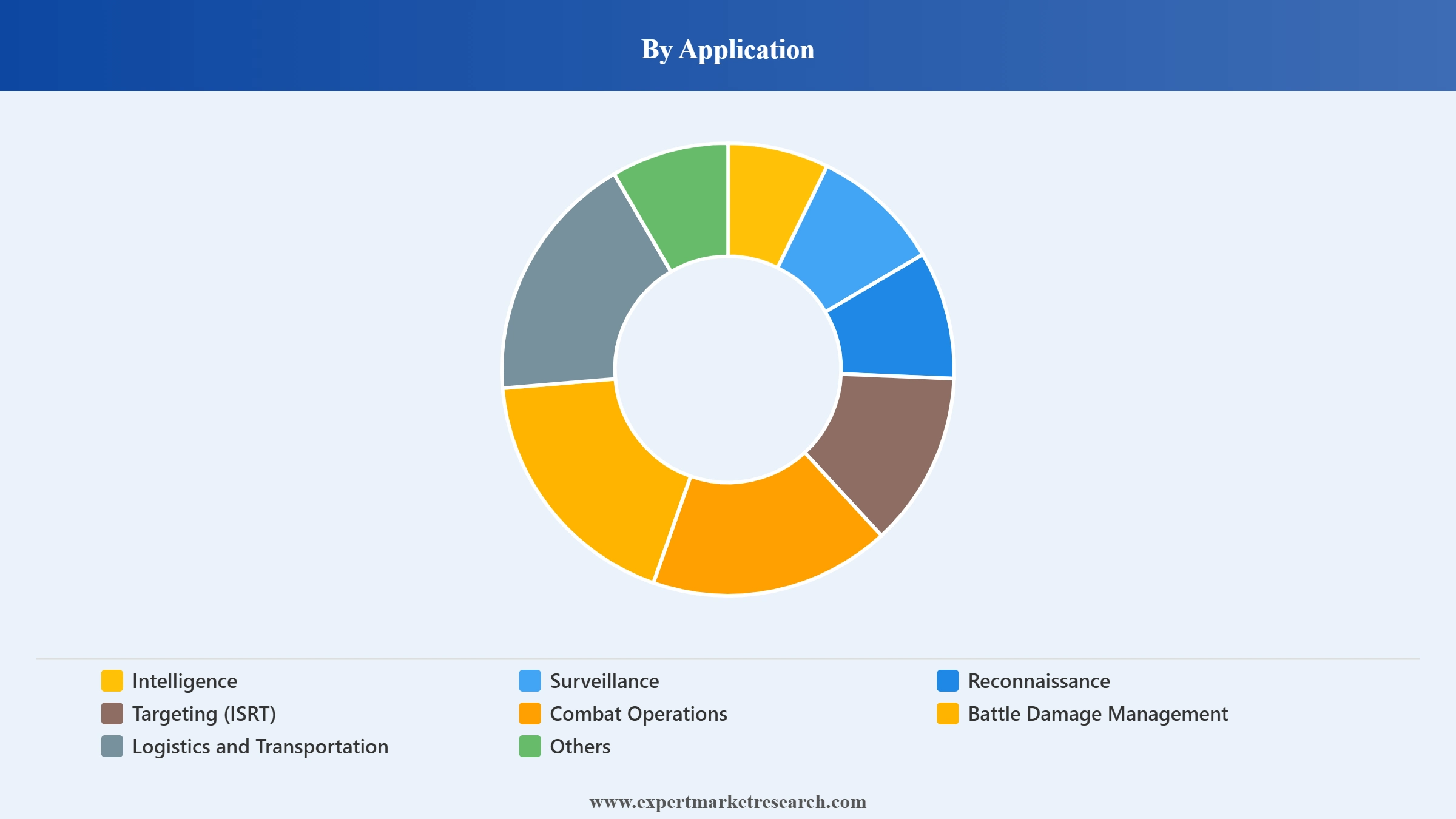

Market Breakup by Application

Key Insight: Intelligence, surveillance, reconnaissance, and targeting is the dominant application segment in the global military drone market, driven by persistent demand for real-time battlefield awareness in contested environments. Combat operations and precision strike applications are growing rapidly, supported by the widespread deployment of armed UAVs including loitering munitions. Logistics and transportation is an emerging segment, with drone-based resupply systems under active development by several military establishments seeking to reduce supply chain vulnerability in forward operational areas.

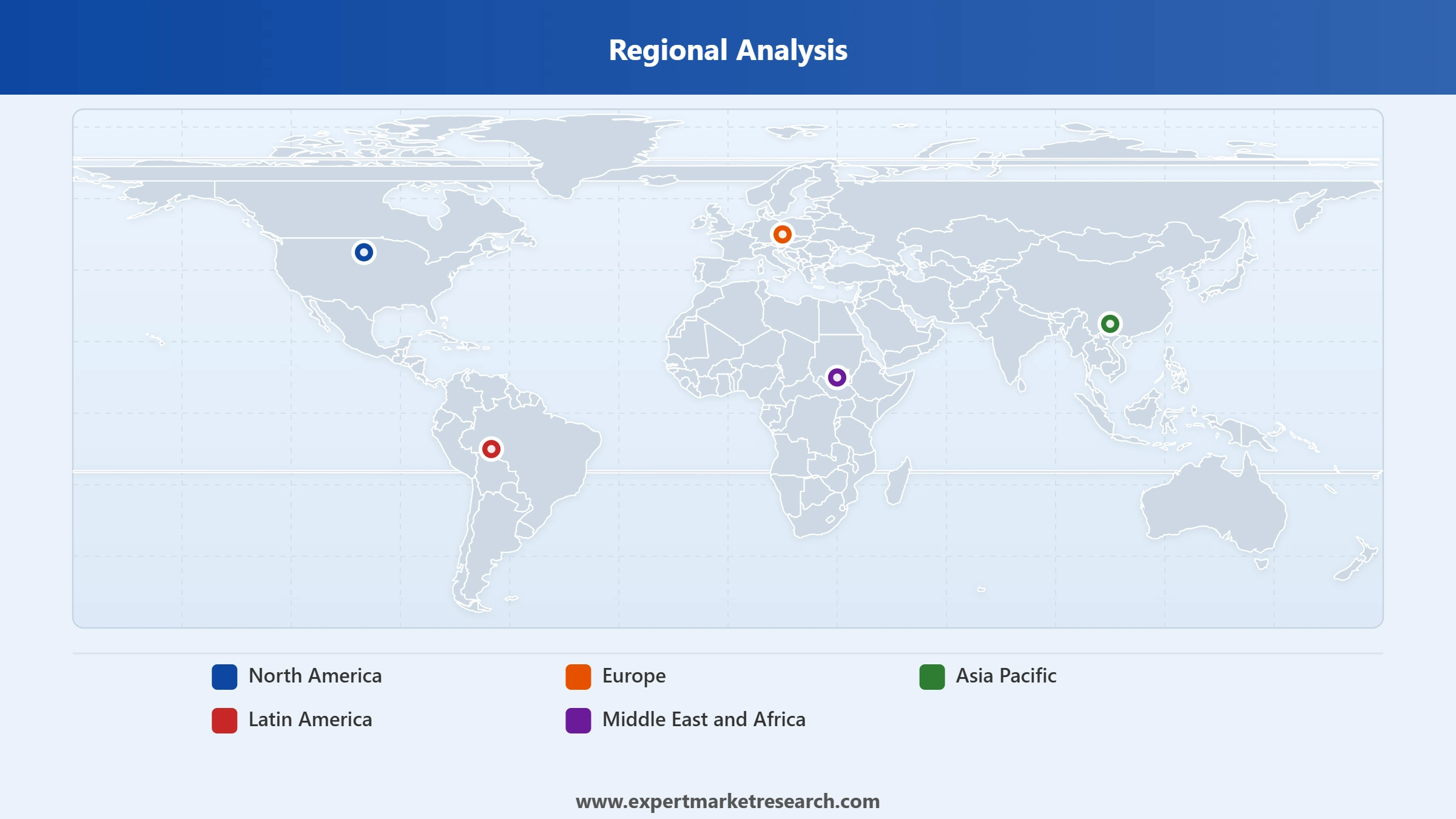

Market Breakup by Region

Key Insight: North America leads the global military drone market, underpinned by the United States' dominant defence budget and extensive operational UAV experience across multiple theatres. Europe is a significant and fast-growing market, driven by post-conflict rearmament and intensified NATO drone procurement. Asia Pacific is the fastest-growing region, with China, India, and Japan making major investments in indigenous and imported UAV platforms. The Middle East and Africa market is expanding rapidly, driven by border security needs and ongoing regional conflicts.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, fixed wing drones dominate the market due to superior endurance and long-range operational capabilities

Fixed wing military drones command the largest share of the global military drone market, valued for their ability to operate at high altitudes for extended durations, carry substantial payloads, and cover vast geographical areas. Platforms such as the General Atomics MQ-9 Reaper, Northrop Grumman RQ-4 Global Hawk, and Elbit Systems Hermes series represent the most operationally deployed fixed wing categories, serving surveillance, intelligence gathering, and precision strike roles for the United States and allied nations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rotary wing drones are gaining meaningful adoption in the global military drone market for tactical operations where hover capability, vertical takeoff and landing, and close-range manoeuvring are operationally essential. Naval boarding operations, urban surveillance, and forward-deployed casualty evacuation trials represent key growth applications. Hybrid drones, combining fixed wing efficiency with rotary wing versatility, are an emerging product type attracting investment from defence programmes seeking platforms that can operate across diverse terrain without fixed runway infrastructure.

By Technology, remotely operated drones account for the dominant share due to proven operational track record and established command infrastructure

Remotely operated drones form the backbone of current global military UAV fleets, benefiting from decades of operational validation, mature ground control station ecosystems, and proven reliability across combat and surveillance missions. The category encompasses the majority of currently fielded military drone inventories globally, from small tactical systems operated via handheld controllers to HALE platforms managed through sophisticated satellite-linked command centres. Established vendors including General Atomics, Northrop Grumman, and Elbit Systems generate significant recurring revenue from remotely operated platform sustainment and upgrades.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Autonomous and semi-autonomous drones represent the most dynamic growth area in the global military drone market's technology segmentation. The US Air Force's Collaborative Combat Aircraft programme, which designated the Anduril YFQ-44A, General Atomics YFQ-42A, and Northrop Grumman YFQ-48A in 2025, exemplifies the scale of investment in autonomous wingman systems. In February 2025, Anduril's CCA prototype completed a milestone flight with dual AI software pilots operating within a single sortie, signalling how rapidly autonomous capability is maturing toward operational deployment.

By Range, Beyond Visual Line of Sight accounts for the fastest-growing share due to theatre-level operational requirements

BVLOS operations represent the fastest-growing range segment in the global military drone market, driven by the operational need for persistent, long-range coverage across large and contested geographical areas. Theatre-level surveillance, strategic strike, and maritime patrol missions all require BVLOS-capable platforms, creating sustained procurement demand for HALE and MALE drone systems with satellite communications integration. Investment in BVLOS enablers including encrypted datalinks, AI-assisted navigation, and spectrum management is intensifying as military establishments prepare for multi-domain operational environments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Visual Line of Sight drone operations retain a substantial and structurally important share of the global military drone market, particularly in training, counter-drone operations, and short-range tactical applications. Small VLOS platforms are increasingly used for urban warfare intelligence collection, engineering reconnaissance, and close air support coordination in terrain where satellite links may be contested or unreliable. Extended Visual Line of Sight systems bridge the gap between VLOS and BVLOS categories, offering tactical commanders an operationally flexible and regulatory-simpler option for mid-range surveillance tasks.

By System, payloads account for the dominant value share of the market due to their direct impact on mission effectiveness

Payloads are the highest-value system category within the global military drone market, as the sensor and weapons integration capabilities they provide directly determine a platform's operational worth. Electro-optical and infrared cameras, synthetic aperture radar, and electronic intelligence payloads are among the most widely procured, enabling the intelligence, surveillance, and targeting missions that define the market's largest application segment. CBRN sensors and LiDAR payloads are growing as military forces expand drone operations into hazardous and complex terrain environments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Software and avionics are rapidly growing system components in the global military drone market, reflecting the shift toward software-defined platforms where mission capability can be updated without hardware replacement. Autonomous flight management software, AI-driven target recognition systems, and encrypted communications architecture are commanding increasing shares of drone programme budgets. The propulsion segment remains strategically important, with electric propulsion gaining ground in tactical drone categories while turboprop and turboshaft engines continue to serve large, long-endurance platforms.

By Application, ISRT accounts for the dominant share of the market due to persistent demand for battlefield intelligence

Intelligence, surveillance, reconnaissance, and targeting is the largest and most structurally durable application segment in the global military drone market. The ability of unmanned platforms to provide continuous, real-time battlefield awareness without risk to human operators makes them indispensable for modern military operations. Fixed wing HALE and MALE drones equipped with multi-sensor payloads sustain persistent ISR across theatre-level areas of operation, informing command decisions, targeting sequences, and force protection measures that would otherwise require manned aircraft with higher operational costs and risk profiles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Combat operations represent the most rapidly expanding application segment in the global military drone market, driven by the proven effectiveness of armed UAVs and loitering munitions in recent conflicts. The Ukrainian conflict has accelerated procurement of expendable loitering munitions globally, with AeroVironment's Switchblade systems representing a benchmark capability. Battle damage management and logistics and transportation applications are evolving segments, with military establishments developing drone-enabled supply chain solutions and autonomous damage assessment tools designed to reduce human exposure in high-risk forward areas.

North America dominates the market due to the United States' dominant defence budget, advanced technology base, and extensive UAV operational history

North America holds the largest share of the global military drone market, driven overwhelmingly by United States defence investment, which funds the world's most advanced and operationally experienced military UAV fleet. The US Department of Defense operates thousands of drone platforms across all categories, from small tactical systems to HALE surveillance platforms, and is investing substantially in next-generation Collaborative Combat Aircraft. Major prime contractors including General Atomics, Northrop Grumman, Lockheed Martin, and AeroVironment are headquartered in the United States, reinforcing the region's dominance across the entire UAV value chain.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing region in the global military drone market, propelled by escalating geopolitical tensions, military modernisation drives, and rising defence budgets across China, India, Japan, and Southeast Asian nations. China's USD 249 billion 2025 defence budget has supported large-scale domestic UAV development and procurement, with indigenous platforms such as the Wing Loong series deployed globally. India is aggressively expanding its military drone capabilities through both domestic development under its Atmanirbhar Bharat initiative and international procurement, targeting surveillance, strike, and logistics drone integration across its armed forces.

The global military drone market is characterised by a highly concentrated competitive structure, with a small group of established defence prime contractors holding the majority of market value through large government contracts and multi-decade platform relationships. Companies including General Atomics, Northrop Grumman, Lockheed Martin, Boeing, and AeroVironment collectively hold substantial shares of UAV procurement across the United States and allied nations. Competition is driven by technology differentiation in autonomy, AI integration, payload capability, and platform endurance.

The competitive landscape is evolving rapidly as new-entrant defence technology companies including Anduril challenge established primes in the autonomous and collaborative combat aircraft segments. Strategic acquisitions are accelerating consolidation, exemplified by AeroVironment's USD 4.1 billion purchase of BlueHalo in May 2025. International competition is intensifying, with Chinese and Israeli manufacturers including Israel Aerospace Industries and Elbit Systems capturing significant export market share through cost-competitive and operationally capable platform portfolios.

Founded in 1937 and headquartered in Stockholm, Sweden, Saab AB is a leading defence and security company operating across air, land, sea, and civil security domains. In the military drone segment, Saab develops tactical UAV systems including the Skeldar rotary wing platform and the Integra ISR drone, and supports unmanned operations across Scandinavian and international defence markets with integrated surveillance and electronic warfare capabilities.

Founded in 1955 and headquartered in San Diego, California, General Atomics is the developer of the MQ-1 Predator and MQ-9 Reaper platforms, among the most widely deployed military drones globally. The company is developing the YFQ-42A Collaborative Combat Aircraft for the US Air Force and is expanding carrier-based autonomous drone capabilities for the US Navy, cementing its position as a leading developer of armed and ISR UAV systems.

Founded in 1995 and headquartered in Bethesda, Maryland, Lockheed Martin is the world's largest defence contractor. The company produces advanced UAV systems including the Stalker surveillance drone and Indago quadcopter, and is participating in the US Navy's Collaborative Combat Aircraft programme. Lockheed Martin integrates drone capabilities across its broader defence portfolio spanning combat aviation, missile systems, and space technologies for the United States and allied governments.

Founded in 1923 and headquartered in Providence, Rhode Island, Textron is a diversified defence conglomerate with a significant military drone presence through its Textron Systems subsidiary. Textron produces the widely deployed Shadow and Aerosonde tactical UAV platforms for the US Army and allied customers, supporting surveillance, reconnaissance, and target acquisition missions across ground forces and special operations communities.

Other key players in the market are Elbit Systems Ltd, Thales Group, BAE Systems Plc, Northrop Grumman Company, AeroVironment Inc., Hindustan Aeronautics Ltd, Israel Aerospace Industries Ltd., Boeing, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead of the rapidly evolving global military drone landscape with Expert Market Research's comprehensive 2026 report. Access in-depth data on autonomous system adoption trends, platform technology competition, application-level procurement dynamics, and the regions driving the strongest growth in UAV investment. Whether you are a defence prime contractor, technology investor, or government procurement body, this report provides the strategic depth you need to make informed decisions in one of the world's fastest-growing defence markets. Download your free sample today.

Military Communications Market

Military Shelter Market

Military Helmet Market

Military Robots Market

Military Radar Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 15.57 Billion.

The market is projected to grow at a CAGR of 9.50% between 2026 and 2035.

The military drone market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 38.59 Billion by 2035.

SIPRI USD 2,718B global military spending in 2024; April 2026 Ukraine first fully unmanned combat operation; AI-driven autonomous drone segment at 15.8% CAGR; South Korea fleet doubling; China USD 249B 2025 defence budget; Q2 2025 USD 500M Boeing DoD surveillance UAV contract; DoD Replicator initiative high-volume tactical drone procurement.

The increasing integration of advanced military drones and the rise in border disputes are the key trends propelling the growth of the market.

The major regions in the market for military drones are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key players include Saab AB, General Atomics, Lockheed Martin Corporation, Textron Inc., Elbit Systems Ltd, Thales Group, BAE Systems Plc, Northrop Grumman Company, AeroVironment Inc., Hindustan Aeronautics Ltd, Israel Aerospace Industries Ltd., Boeing, and Others.

The most prevalent fuel used by military drones is hydrogen, and the most prevalent oxidiser is airborne oxygen.

The different technologies for military drones include remotely operated drones, semi-autonomous drones, and autonomous drones.

The primary applications of military drones are intelligence, surveillance, reconnaissance, and targeting (ISRT), combat operations, battle damage management, and logistics and transportation, among others.

The leading segment in the military drone market is expected to be surveillance and reconnaissance drones for intelligence and tactical operations.

According to the market report, North America held the largest market share.

Fixed-wing drones dominate with approximately 66% market share in 2025, driven by superior endurance for ISR missions accounting for approximately 60% of drone procurement. Hybrid drones are fastest-growing at approximately 12-15% CAGR, validated by Bayraktar TB3's NATO exercise performance.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Technology |

|

| Breakup by Range |

|

| Breakup by System |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.