Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

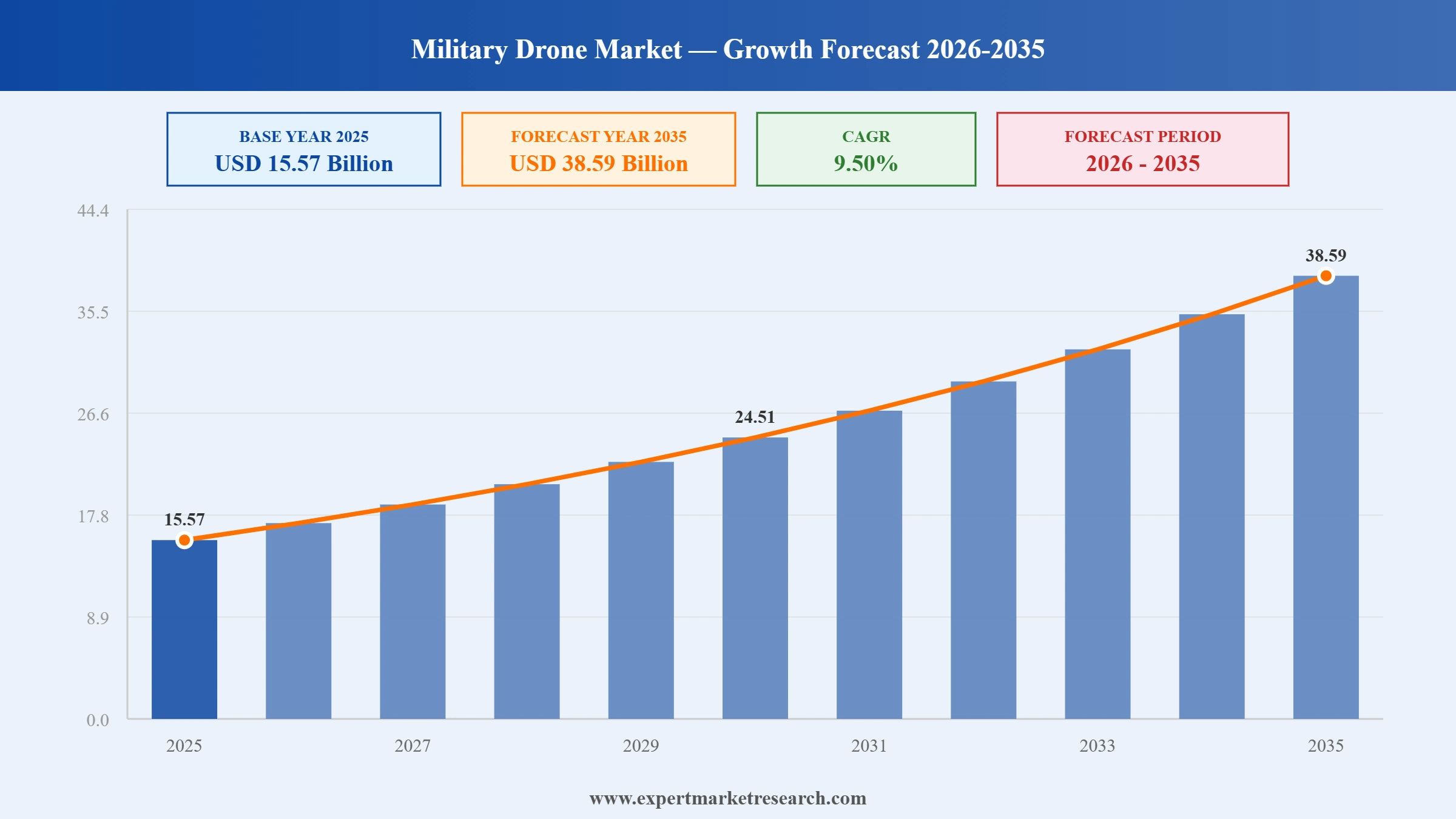

The global military drone market attained a value of USD 15.57 Billion in 2025 and is projected to expand at a CAGR of 9.50% through 2035. The market is further expected to achieve USD 38.59 Billion by 2035. The increasing use of autonomous swarm technology and the domestic defense industry push towards the acquisition of the latest military drones in the area of surveillance, reconnaissance, electronic warfare, and precision strikes.

There are two major driving factors that are supporting the increasing military drone market growth. On the one hand, governments are spending more on the development of the counter-drone ecosystem requiring the use of unmanned systems that can be identified and coordinated. On the other hand, defense departments prefer software-enabled drones with an open architecture, which allows adding new payloads to them without updating the whole fleet.

A significant development in the military drone market was Anduril Industries' April 2025 launch of the Copperhead family of autonomous underwater and aerial weapons. The firm added this weapon line to its autonomous defense system portfolio. In addition, Anduril Industries is expanding its software-defined Lattice technology platform in order to include unmanned systems in the defense network. This indicates the changing trends in the procurement process where the United States Department of Defense is focusing on low-cost autonomous systems and quick production processes, urging defense agencies to diversify drone procurement process away from traditional drones.

Changes in defense modernization policies and operational needs are leading to changes in the procurement processes in the military drone market. There is an increased need for drones that can operate with manned aircraft, conduct intelligence missions, perform electronic warfare operations, precision strikes, and have interoperability. For example, in June 2026, United States-based firm unveiled a deep-reach ISR drone, enabling surveillance beyond tactical frontlines with extended operational intelligence capabilities. Drone manufacturers are using modular architecture of the payload of drones, use of AI-based navigation, swarming technologies, and open-source software which enables future upgrading. Strategic alliances between defense contractors, software firms, and sensor providers are increasing the deployment cycles and cutting down the cost of lifecycle.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India took steps towards a USD 2 billion investment in military drones, boosting its efforts to improve domestic production, surveillance technologies, and defense modernization programs. Companies can grow their capacity to build drones indigenously, produce components and AI-driven mission systems to cater to growing defense procurement demands, leveraging such developments in the military drone market.

The Royal Navy tested the launching of combat drones through the use of a ship-based catapult system, providing greater flexibility for operations at sea. Companies can therefore work on ship-based drone launching systems, autonomous carrier systems, and maritime ISR drones.

The successful launch of a strike drone into the seas proved the ability of such autonomous drones to work within hybrid naval fleets for enhanced surveillance and precision strikes. Companies may make investments in autonomous maritime drones, command systems, and endurance vehicles that operate in multi-domain military operations.

Safran collaborated with THEON Sensors in order to develop superior electro-optical technology, which enhances the intelligence, surveillance, targeting and effectiveness of drone operations. Companies may collaborate in developing AI-enabled sensors, imaging payloads and defense electronics for their military drones, following such trends in the military drone market.

The military drone market is undergoing an unprecedented revolution due to the incorporation of artificial intelligence into their software which is used for self-governing, decision-making, identification of targets, and collaborative missions. Companies manufacturing military drones are developing self-reliant drones with minimum human intervention and maximum flexibility on the battlegrounds. For example, in July 2026, the United Kingdom MOD AI Battle Lab advanced military drone training using AI-powered simulation, accelerating autonomous mission planning and operational readiness. On the other hand, the Replicator Initiative by the United States Department of Defense plans to introduce thousands of affordable autonomous systems into the military forces.

Countries are increasingly engaging in domestic manufacturing of their military drones in order to cut their dependency on the foreign defense technologies and make their supply chains more resilient to any shocks. National procurement programs are also providing incentives for the production of drones within countries along with the collaboration of traditional defense companies and new entrants in the military drone market. The Aatmanirbhar Bharat and Innovations for Defence Excellence (iDEX) program of India is providing funding to startup companies that develop unmanned systems and technologies for military applications. As a result, in May 2026, Paras Defence unveiled the Paras-SK50 tactical drone, delivering indigenous surveillance, precision strike capabilities, and enhanced battlefield operational flexibility.

Players in the military drone market are increasingly procuring unmanned aerial vehicles that can operate in line with fighter jets, presenting new growth prospects for cutting-edge autonomous platforms. This kind of technology is allowing to improve intelligence gathering, electronic warfare, and strikes while ensuring the safety of pilots. In March 2026, Anduril began high-speed combat drone production, accelerating autonomous aircraft manufacturing through its advanced large-scale United States production facility. Furthermore, Australia is providing support to the development of Boeing's MQ-28 Ghost Bat for collaborative air combat operations. As a result, there is an increasing demand for advanced autonomous flight software, secure communications equipment, sensors, propulsion systems, and mission computing systems.

Drones are required to operate in the environment of contested electromagnetic spectrum and provide counter-drone capabilities to the forces. Defense contractors are incorporating electronic warfare payload, anti-jamming equipment, secure communications capabilities, and cyber resilient navigation solutions into new generations of unmanned vehicles. Moreover, the member countries of NATO are intensifying their efforts to enhance integrated air and missile defense capability through the integration of surveillance drones with counter-unmanned aircraft systems. Aligning with such trends in the military drone market, in June 2026, Indra unveiled a tethered drone system, enhancing tactical electronic warfare through persistent surveillance, communications interception, and battlefield protection.

The need for sustained intelligence, surveillance, and reconnaissance services is prompting the acquisition of advanced military drones that have the capacity to function outside national boundaries and at sea. The need for unmanned aircraft with satellite capability, beyond visual line of sight capability, and multi-sensors is becoming more common among governments that want to monitor their territories continuously, boosting the military drone market expansion. In July 2026, NATO announced procurement of up to five MQ-4C Triton drones, strengthening maritime surveillance and long-endurance ISR capabilities. Additionally, many countries in the Indo-Pacific region are making increased investments in unmanned border monitoring.

The EMR’s report titled “Global Military Drone Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

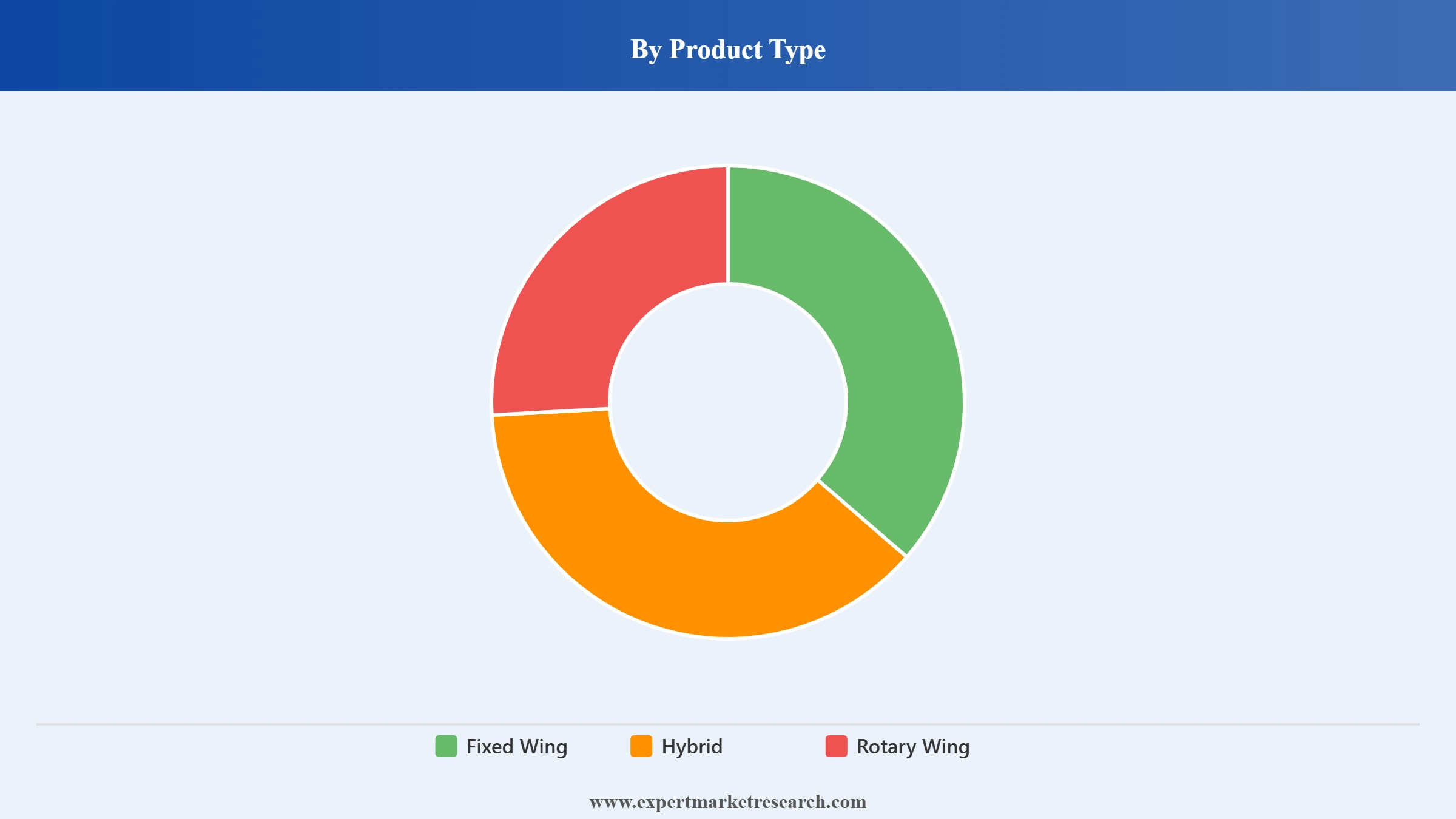

Market Breakup by Product Type

Key Insight: The military drone market is characterized by different operational needs in all product types. The fixed-wing type predominates due to their ability to fly long distances, carry a large payload, and perform strategically. The hybrid type of drones is experiencing fast growth because they are effective in flying and can take off vertically when needed tactically. Rotary wing drones continue to sustain their importance when conducting short missions like reconnaissance and urban warfare, especially where hovering capabilities are needed. Military organizations are adopting a multi-drone fleet approach, which incorporates long-range missions and tactical use. For example, in July 2026, France showcased a mobile FPV swarm drone launcher, enabling rapid battlefield deployment and scalable autonomous strike capabilities.

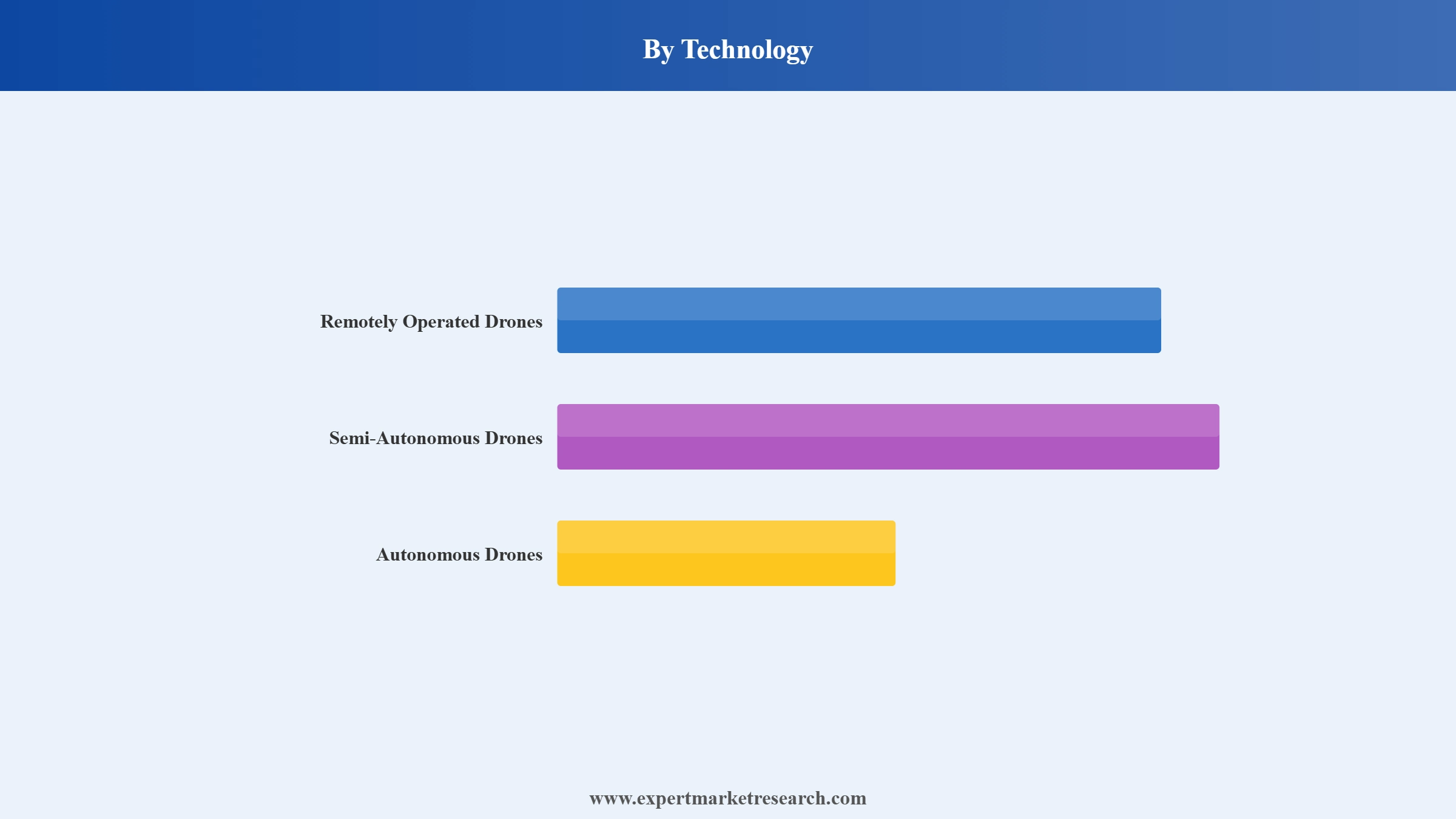

Market Breakup by Technology

Key Insight: The segmentation of technology showcases the gradual process of increasing autonomy by the military. Remotely operated drones lead the military drone market growth through their reliability of operation, human supervision, and military doctrine. The semi-autonomous drones act as a link between conventional and futuristic operations through automation of certain processes and navigation as well as keeping the decision-making under the control of the operators. Autonomous drones are being deployed at the fastest rate as they increase the efficiency of missions and decrease the workloads while allowing the coordination of more than one platform.

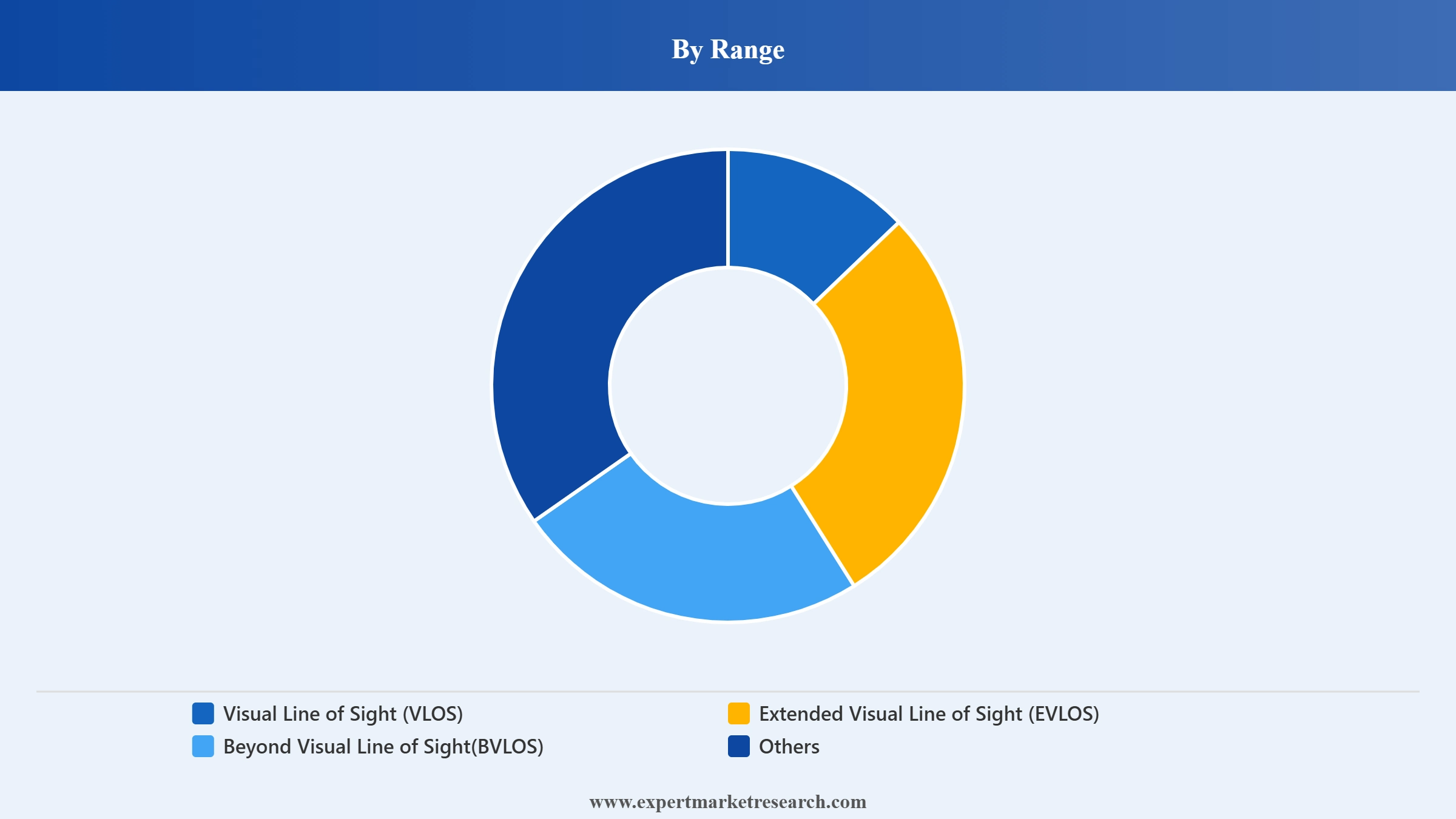

Market Breakup by Range

Key Insight: Range capabilities largely impact the purchasing decisions for drones for military purposes. BVLOS drones dominate the military drone market because of their efficiency when it comes to intelligence, surveillance of sea areas, and strategic surveillance. EVLOS drones are fast becoming popular owing to the fact that they provide more flexibility during operation without requiring too much infrastructure support. VLOS drones are employed for reconnaissance missions and training purposes within a short distance where there is a need for immediate operator control. In January 2026, India selected Shield AI's V-BAT drones with Hivemind autonomy software, enhancing AI-enabled surveillance and autonomous military mission capabilities.

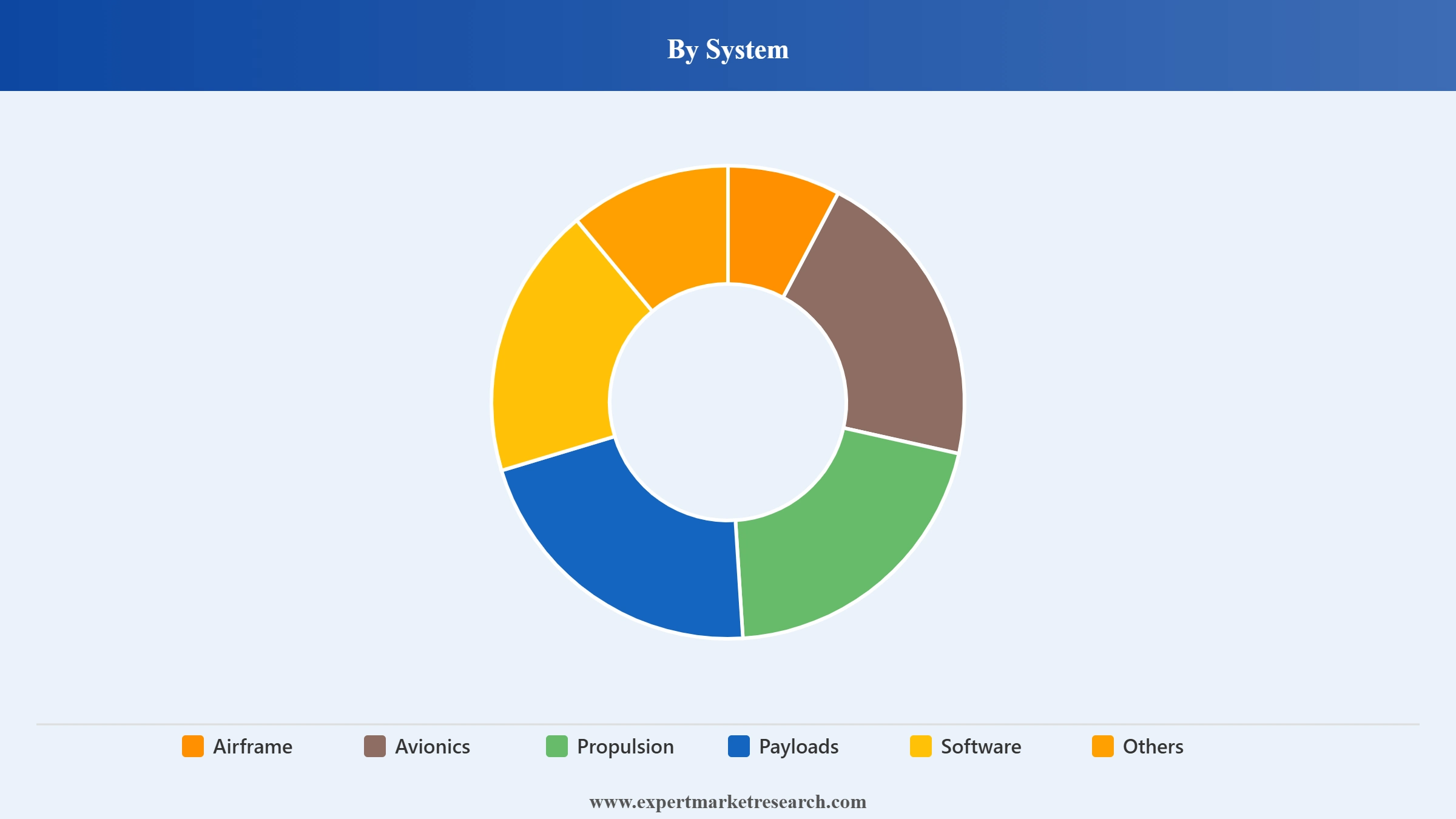

Market Breakup by System

Key Insight: System segmentation, as considered in the military drone market report, shows the increasing convergence of modern hardware with intelligent software. Payloads systems prevail since the success of any operation relies on complex systems for sensing, surveillance and targeting. Airframe offers efficiency in terms of structure, whereas avionics ensure navigation and efficient control during flight. Propulsion technologies such as electric propulsion engines, turboprop engines, and turboshaft engines cater to the different requirements of mission endurance and performance. The software segment is growing due to increased capacity for autonomy, cyber security, and mission optimization. In July 2026, Dassault Aviation and Harmattan AI successfully tested the Namib electronic warfare payload, enhancing Rafale F4 drone-supported mission survivability.

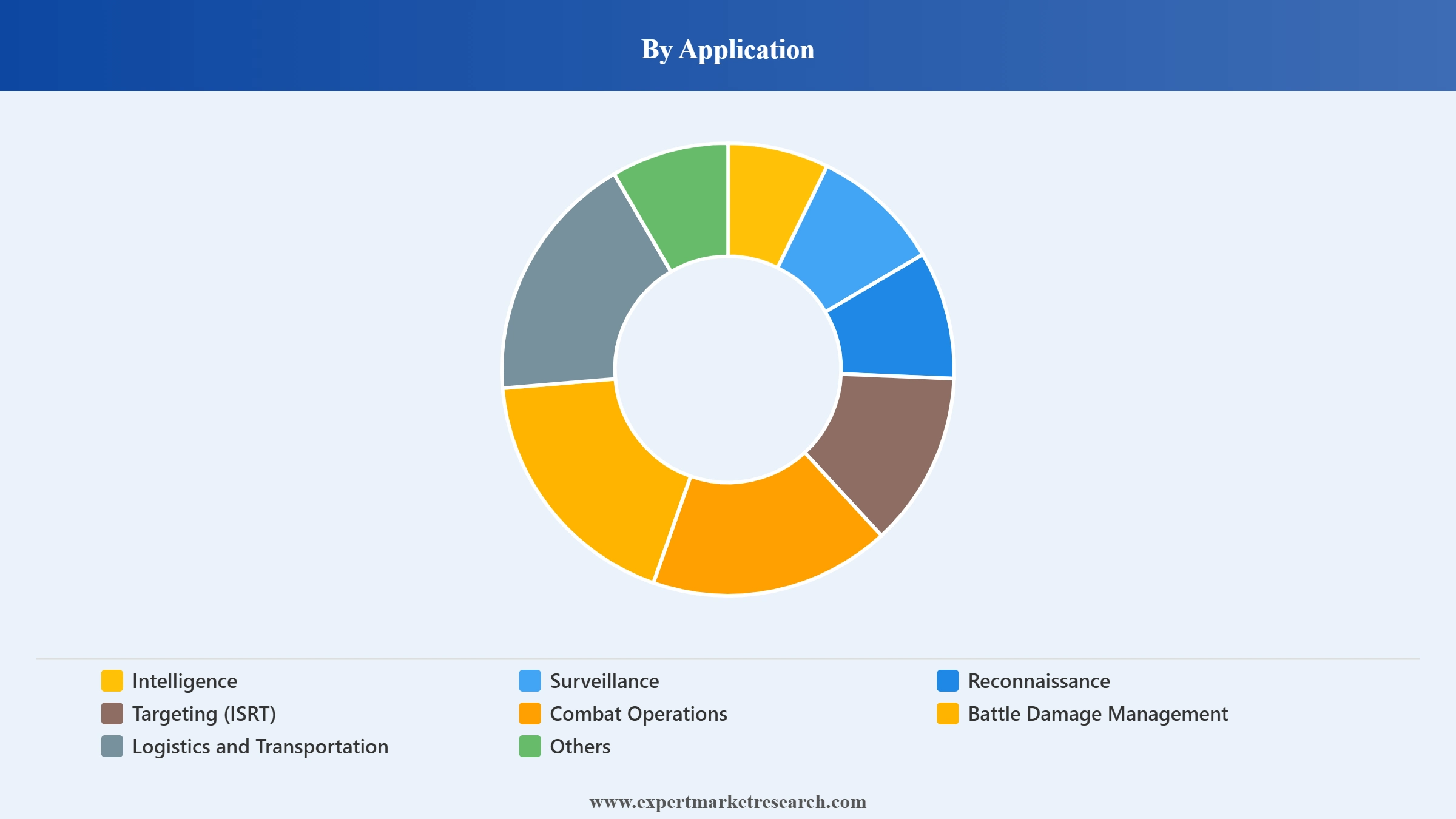

Market Breakup by Application

Key Insight: Diversity in applications is a result of an expanded use of drones within military operations. The dominance of ISRT continues to persist in the market owing to intelligence advantages that are required for successful military operations. Precision engagement and force multiplication are becoming increasingly common within combat operations through the use of unmanned systems. Battle damage assessment allows for quick evaluation of the situation after strikes, through aerial imagery. Logistical operations are rapidly expanding their market shares through improved supply chains and reduced exposure of people during operations, accelerating the military drone market penetration. In July 2026, Australia successfully deployed the Aladdin air-launched delivery drone from a C-130, enabling precise autonomous tactical resupply missions.

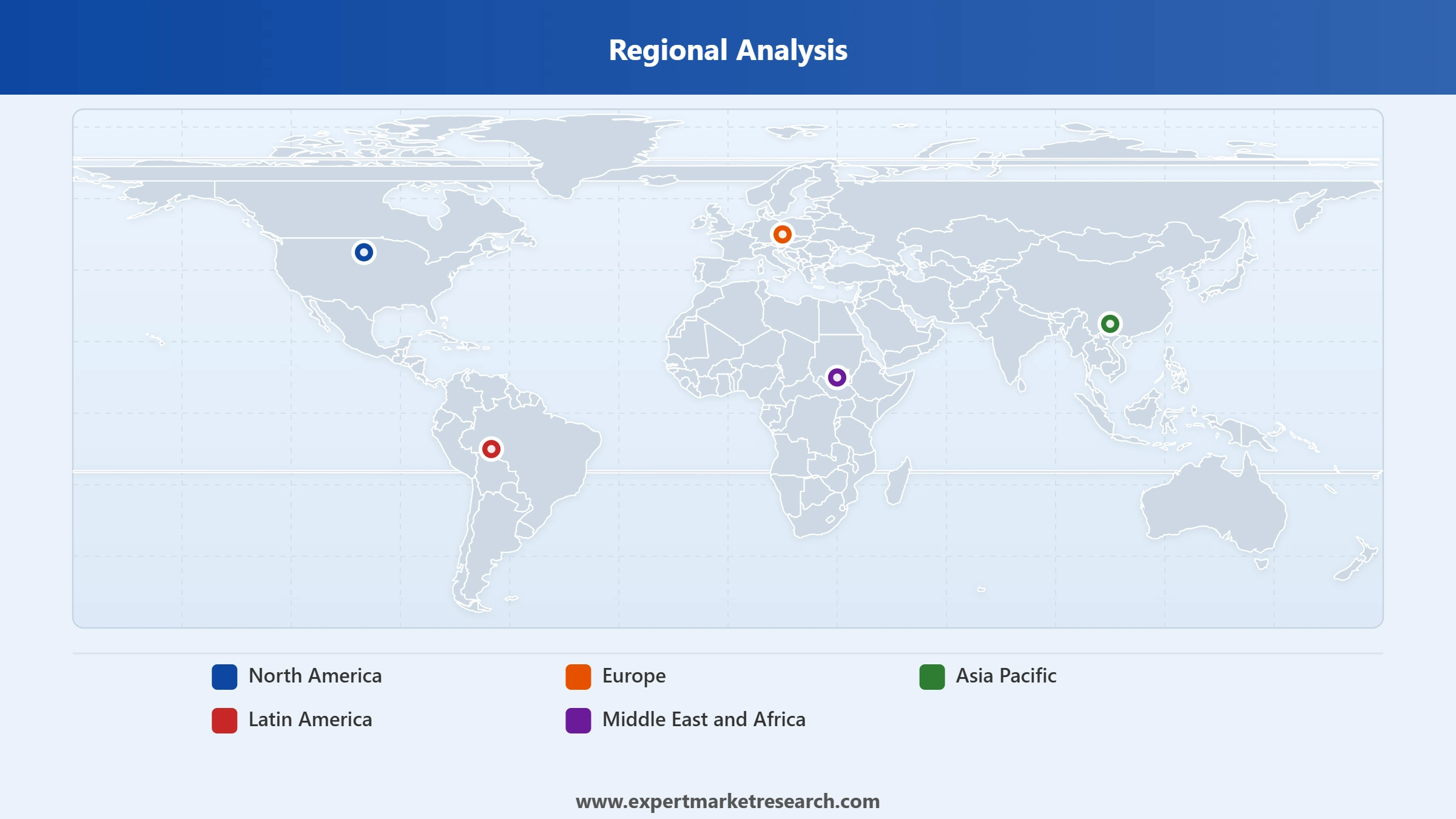

Market Breakup by Region

Key Insight: Regional demand in the military drone market varies depending on defense priorities and local industries. North America sustains its leadership position with the help of technological advances, effective acquisition plans, and reputable defense contractors. Europe concentrates on defense cooperation, developing new technologies, and upgrading unmanned systems. The Asia Pacific region experiences the highest growth rates due to increased defense spending, regional security issues, and local manufacturing capacity. Latin America focuses on improving border control capabilities utilizing affordable unmanned systems. The Middle East and Africa regions are investing more in military drones to improve security of borders, gathering intelligence, and securing critical infrastructure facilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, fixed wing drones lead the market due to extended endurance and strategic surveillance capabilities

The fixed wing military drones represent the dominant share in the military drone market as they offer high endurance, high altitude operations, and broad coverage for intelligence purposes. The defense departments employ such platforms in order to provide border security, maritime surveillance, long-distance reconnoitering, and persistent battlefield surveillance where operational efficiency is a must. The capacity to lift heavy loads, advanced radar systems and multiple sensors integration make them appropriate for military missions. The ongoing development of high-altitude long-endurance platforms increases their procurement among advanced defense establishments. In March 2026, China demonstrated the Atlas drone swarm system, enabling AI-driven autonomous coordination, precision strikes, and large-scale multi-drone battlefield operations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The hybrid military drones experience the fastest rate of growth in the military drone market as they incorporate the features of vertical takeoff and efficient fixed-wing flight. Thus, they are appropriate for dynamic military missions. The armed forces tend to favor hybrid platforms for tactical surveillance, special operations, disaster relief, and remote deployment where the traditional runways are not available. They improve their fuel efficiency, operation range, and adaptability to meet the changing battlefield needs. For example, in April 2026, ISS Aerospace unveiled the HAL10 launcher, enabling rapid deployment of ten WASP drones for scalable battlefield surveillance operations.

By technology, remotely operated drones secure the dominant share of the market through proven reliability and secure mission control

The use of remotely piloted drones is gaining popularity across the overall military drone market scope due to the fact that it offers a means for an operator’s supervision when conducting ISR activities and precision strikes. Defense agencies see such systems as the ideal opportunity for retaining the ability for humans to make decisions during difficult military missions. The use of reliable communication systems, established control technologies, and compatibility with existing military infrastructure enhances the reliability of remotely operated systems. In April 2025, Optiemus Unmanned Systems unveiled four advanced defense drones, strengthening indigenous surveillance, reconnaissance, loitering munition, and tactical mission capabilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Autonomous drone technology is the fastest-growing sector in the military drone market since militaries look for rapid deployment and reduced need for pilot efforts. The use of autonomous navigation, obstacle detection, target recognition, and swarm technology enables such drones to execute complex missions without human help. Modern defense companies implement machine learning algorithms, edge computing, and mission planning features into new systems. Such features enhance the speed of operations, survivability, and scalability. In July 2026, Namib integrated an electronic warfare payload, enhancing drone resilience against jamming, spoofing, and contested electromagnetic battlefield environments.

By range, Beyond Visual Line of Sight (BVLOS) dominates the market through long-range strategic surveillance operations

BVLOS drones are largely contributing to the military drone market revenue due to the support they provide for missions of extended reconnaissance, border security, sea surveillance, and intelligence gathering in large areas of operations. Being coupled with satellite communications and secure command networks allows BVLOS drones to conduct uninterrupted operations. The increasing demand of military forces on BVLOS capabilities is explained by the need to increase the situational awareness. In July 2026, Echodyne opened a new MESA radar manufacturing facility, expanding production capacity to meet growing global defense and counter-drone demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Extended Visual Line of Sight (EVLOS) drones are growing in popularity due to their increased mission range in comparison with the operational range of visual drones without additional strategic infrastructures used for long-range missions. They are becoming increasingly popular among military forces for use in reconnaissance, border patrol, artillery support, and battlefield surveillance, reshaping the military drone market dynamics. In April 2026, AeroVironment launched the MAYHEM 10 autonomous drone, enabling modular ISR, electronic warfare, precision strike, and communications missions.

Payload systems secure the largest share of the market owing to expanding multi-sensor intelligence collection requirements

Payload systems account for the largest share of the military drone market, as mission success heavily depends on advanced sensors, imaging technologies, and surveillance capabilities. The cameras, EO/IR, radar, LiDAR, CBRN sensors, and intelligence equipment help armed forces perform various roles in their missions. Defense forces are focused on building modular payload architectures that enable quick mission customization without the need for platform replacement. The improvements in sensors' precision and integration also contribute to procurement prospects of global defense modernization programs. In October 2025, Lockheed Martin partnered with Saildrone, integrating lethal payloads onto autonomous USVs for advanced maritime defense and surveillance missions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Software is becoming the fastest-growing segment of the military drone market due to the dependence of defense forces on autonomous navigation software, cybersecurity solutions, real-time battlefield analytics, and mission planning using artificial intelligence technology. The use of software-defined technology is necessary for securing communications, executing collaborative missions, predictive maintenance, and upgrading systems rapidly. Open architecture systems help to continuously improve software capabilities during the operational life cycle of UAVs.

ISRT applications dominate the market through persistent intelligence gathering and strategic battlefield awareness capabilities

ISRT continues dominating the military drone market since military entities need situational awareness even before and during the operation process. With military drones fitted with advanced sensors, there is high resolution imagery, target identification, monitoring of the battlefield, and intelligence gathering without endangering personnel. Persistent surveillance helps enhance the planning process and precision decision-making in land, air, and maritime spaces. Increased spending on intelligent network integration continues to increase the demand for unmanned platforms in ISRT. In July 2026, Indian Air Force launched an indigenous long-range suicide drone project, strengthening autonomous precision strike and domestic defense manufacturing capabilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Logistics and transportation applications continue to boast rapid growth in terms of the military drone market revenue as there is an effort to use faster and efficient methods to deliver supplies in hostile territory by defense agencies. The use of military drones in delivering ammunition, medical equipment, spare parts, and other emergency supplies in remote operational locations is becoming a common practice without endangering any personnel.

North America captures a substantial share of the market through advanced defense modernization and sustained procurement investments

North America constitutes the biggest regional military drone market on account of continuous investment in state-of-the-art defense technologies, autonomous systems, and military modernization efforts. Effective coordination among defense organizations, aerospace companies, software developers, and research institutions helps advance innovations in unmanned systems. Continued procurement of surveillance, combat, and collaborative autonomous systems contributes to the leadership of the region in the global market. High defense budgets, developed industries, and continued technology development programs are expected to contribute to market expansion in the region.

Asia Pacific is expected to be the fastest-growing regional military drone market with the increasing investment in defense budgets, drone manufacturing, and modernization of armed forces in response to the emerging regional security challenges. Investment in unmanned systems, artificial intelligence for defense, and border surveillance technologies is expected to increase to enhance operational capabilities and strengthen national security. Increased defense industry partnerships and localization of technologies might accelerate production capabilities in the region. In July 2026, China unveiled a truck-mounted electromagnetic catapult, enabling runway-free rapid deployment of fixed-wing military drones from mobile platforms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The competition within the global market involves autonomous mission software, modular payload capability, secure communication, and scalable manufacturing capacity. Leading military drone companies are now investing more in navigation through artificial intelligence, collaborative combat systems, electronic warfare payloads, and open architecture platforms to facilitate upgrades in technologies throughout the lifespan of their products. Collaboration between these firms and governments, defense organizations, semiconductor firms, and sensor manufacturers is increasing innovations and shortening time taken to develop them.

Military drone market players are also setting up manufacturing plants within their countries to facilitate the security needs of their nations. The increasing demand for affordable autonomous systems, counter-drone systems, and multi-domain combat systems is expected to create new opportunities for avionics companies, propulsion companies, cybersecurity companies, and artificial intelligence software companies. Firms that provide interoperable and software-defined drone ecosystems that can be adjusted to accommodate battlefield changes are projected to improve their competitive advantage and secure long-term contracts from governments, over the forecast period.

Founded in 1937 and based in Stockholm, Sweden, Saab AB is a pioneer in developing cutting-edge technology in military drones that assist in intelligence, surveillance, and operations. Their concentration on security communication networks, electronic warfare equipment, sensing mechanisms, and mission payload modules contributes to their success. This company's expertise in providing network-centric defense solutions allows armed forces to increase awareness during military missions.

Founded in 1955 and located in San Diego, California, United States, General Atomics remains one of the biggest manufacturers of long-range military drones. The company specializes in manufacturing intelligence, surveillance, reconnaissance, and strike platforms while expanding its capacities in producing autonomous combat planes.

Formed in 1995, Lockheed Martin is based in Bethesda, Maryland, United States, and specializes in the design of state-of-the-art unmanned vehicles combined with artificial intelligence (AI), networking security, and multi-domain command & control. Its specialization includes autonomous mission software, electronic warfare technology, and collaborative defense systems that enhance battlefield connectivity. Regular investment in digital engineering facilitates rapid innovation and boosts overall military drone market growth.

Textron Inc. is formed in 1923 and operates from Boston, United States. It provides tactical military drones for intelligence gathering and surveillance missions. Its specialization includes the design of light-weight airframes, autonomous flight systems, modular payload integration, and scalable manufacturing.

Other key players in the market include Elbit Systems Ltd, Thales Group, BAE Systems Plc, Northrop Grumman Company, AeroVironment Inc., Hindustan Aeronautics Ltd, Israel Aerospace Industries Ltd., and Boeing, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our military drone market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Military Communications Market

Military Shelter Market

Military Helmet Market

Military Robots Market

Military Radar Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 15.57 Billion.

The market is projected to grow at a CAGR of 9.50% between 2026 and 2035.

The military drone market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 38.59 Billion by 2035.

SIPRI USD 2,718B global military spending in 2024; April 2026 Ukraine first fully unmanned combat operation; AI-driven autonomous drone segment at 15.8% CAGR; South Korea fleet doubling; China USD 249B 2025 defence budget; Q2 2025 USD 500M Boeing DoD surveillance UAV contract; DoD Replicator initiative high-volume tactical drone procurement.

The increasing integration of advanced military drones and the rise in border disputes are the key trends propelling the growth of the market.

The major regions in the market for military drones are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key players include Saab AB, General Atomics, Lockheed Martin Corporation, Textron Inc., Elbit Systems Ltd, Thales Group, BAE Systems Plc, Northrop Grumman Company, AeroVironment Inc., Hindustan Aeronautics Ltd, Israel Aerospace Industries Ltd., Boeing, and Others.

The most prevalent fuel used by military drones is hydrogen, and the most prevalent oxidiser is airborne oxygen.

The different technologies for military drones include remotely operated drones, semi-autonomous drones, and autonomous drones.

The primary applications of military drones are intelligence, surveillance, reconnaissance, and targeting (ISRT), combat operations, battle damage management, and logistics and transportation, among others.

The leading segment in the military drone market is expected to be surveillance and reconnaissance drones for intelligence and tactical operations.

According to the market report, North America held the largest market share.

Fixed-wing drones dominate with approximately 66% market share in 2025, driven by superior endurance for ISR missions accounting for approximately 60% of drone procurement. Hybrid drones are fastest-growing at approximately 12-15% CAGR, validated by Bayraktar TB3's NATO exercise performance.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Technology |

|

| Breakup by Range |

|

| Breakup by System |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.