Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

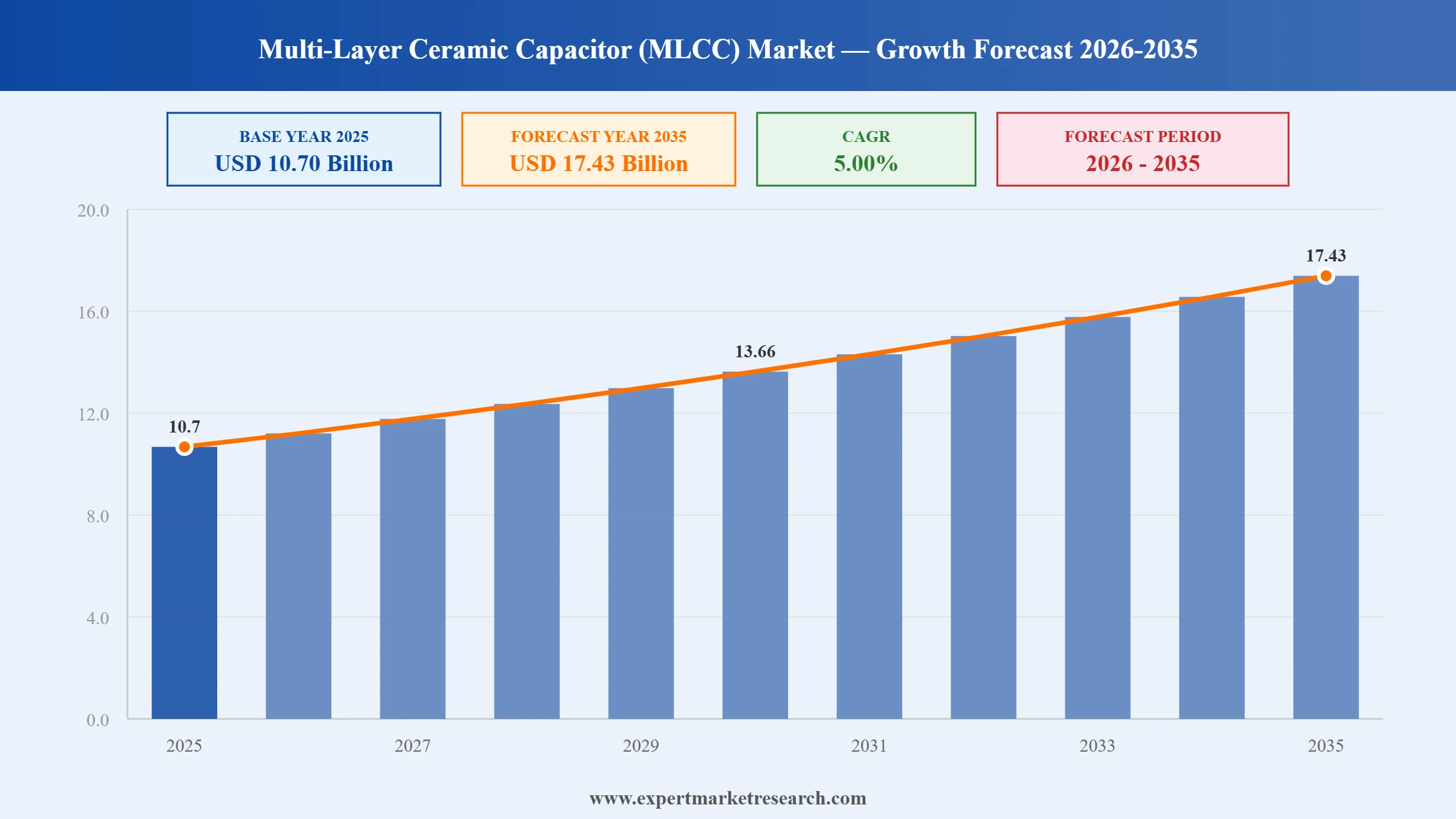

The global multi-layer ceramic capacitor (MLCC) market reached a value of USD 10.70 Billion at 2025 and is projected to expand at a CAGR of around 5.00% during the forecast period of 2026-2035. With surging AI server deployment driving unprecedented demand for high-capacitance, high-voltage MLCCs, rapid automotive electrification increasing capacitor content per vehicle, expanding consumer electronics production, growing 5G telecommunications infrastructure rollout, and rising precision manufacturing and industrial automation requirements, the market is expected to reach USD 17.43 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global multi-layer ceramic capacitor (MLCC) market is undergoing a structural transformation driven by the AI infrastructure build-out, which is reshaping pricing, capacity allocation, and supply chain priorities among the world's leading MLCC manufacturers. The proliferation of AI servers, which consume 10 to 20 times more MLCCs than smartphones, is creating unprecedented supply tightness for high-capacitance, high-voltage components. This is driving simultaneous price increases by Japanese and Korean manufacturers, accelerated capacity investment, and a strategic reallocation of production lines toward high-value-added components across the global multi-layer ceramic capacitor (MLCC) market.

Samsung Electro-Mechanics (SEMCO), the second-largest MLCC manufacturer globally, reached an internal consensus on price adjustments and began evaluating a 5% to 10% increase across select MLCC product lines, following price actions by Murata Manufacturing and Taiyo Yuden. The decision was driven by surging AI server demand pushing capacity utilisation above 80% at SEMCO's facilities, with the company's book-to-bill ratio consistently exceeding 1 for multiple consecutive quarters. Goldman Sachs responded by upgrading its 2026 MLCC price forecast for the global multi-layer ceramic capacitor (MLCC) market from flat to a 0-5% increase.

Taiyo Yuden Co., Ltd. issued a formal price increase notice raising prices on low-to-mid capacitance consumer-grade MLCCs and select automotive MLCC products by approximately 6% to 13% effective for orders from May 2026, making it the first major manufacturer to formally announce broad-based price adjustments in the current cycle. The increase reflected both surging AI-driven demand tightening supply of component materials including silver and palladium, and Taiyo Yuden's strategic pivot toward higher-margin automotive and AI server applications within the global multi-layer ceramic capacitor (MLCC) market.

Murata Manufacturing Co., Ltd., the global leader in the MLCC market holding approximately 40% market share, announced price increases of 15% to 35% for AI server high-capacitance MLCCs, high-end automotive-grade MLCCs, and RF/microwave MLCCs, effective from April 2026 based on order receipt date. The announcement followed Murata's reporting that its high-end MLCC orders grew 20% to 25% quarter-over-quarter in Q1 2026, with production lines at full capacity. The company's Fukui R&D facility and Southeast Asia manufacturing expansions are targeted at meeting AI server MLCC demand in the global multi-layer ceramic capacitor (MLCC) market.

Murata Manufacturing Co., Ltd. completed construction of its advanced R&D and prototyping facility in Fukui Prefecture, Japan, focused on next-generation MLCC technologies including sub-0.5-micron copper electrode processes that could double capacitance density while significantly reducing production costs. Concurrently, Murata opened a new packaging and distribution operation in India to serve the growing South Asian electronics manufacturing ecosystem. These investments reinforced Murata's dominant position and long-term technology leadership across the global multi-layer ceramic capacitor (MLCC) market.

The global AI server deployment cycle, led by NVIDIA GB200 and GB300 rack systems, is generating unprecedented MLCC demand. A single next-generation GPU rack requires approximately 440,000 MLCCs for power filtering and decoupling functions, versus around 30,000 for a conventional server. This structural demand shift is redirecting production capacity of leading manufacturers including Murata, Samsung Electro-Mechanics, and Taiyo Yuden toward high-capacitance, low-equivalent-series-resistance Class 2 products, creating supply tightness that is reshaping pricing dynamics across the entire global multi-layer ceramic capacitor (MLCC) market. Murata Manufacturing estimates AI server MLCC demand will increase 3.3-fold by 2030 compared to 2025 levels.

The transition to electric vehicles and advanced driver-assistance systems is a major structural growth driver for the global multi-layer ceramic capacitor (MLCC) market. A conventional internal combustion engine vehicle contains approximately 1,000 MLCCs, while a battery electric vehicle requires 6,000 to 10,000 MLCCs, representing a 6 to 10-fold increase in per-unit content. Taiyo Yuden's 1000V MLCC series for EV traction inverters and Murata's high-temperature automotive-grade components address the stringent reliability requirements of automotive electrification, supporting sustained high-margin growth in the automotive application segment of the global multi-layer ceramic capacitor (MLCC) market.

Rapid 5G infrastructure rollout across North America, Europe, and Asia Pacific is driving growing demand for high-frequency RF/microwave MLCCs used in antenna filters, power amplifiers, and millimetre-wave signal processing modules. Murata's 0402-size high-capacitance MLCCs and specialised RF components serve this infrastructure application segment. The miniaturisation requirements of 5G small cells and massive MIMO antenna arrays demand MLCC products with exceptional precision and temperature stability, supporting the Class 1 (NP0/C0G) segment of the global multi-layer ceramic capacitor (MLCC) market.

The relentless miniaturisation of electronic devices and advanced packaging architectures such as chiplets and 3D integrated circuits is driving demand for ultra-small MLCC formats in the global multi-layer ceramic capacitor (MLCC) market. Murata Manufacturing launched the world's smallest 006003 MLCC measuring 0.06mm x 0.03mm, enabling integration in densely packed semiconductor package designs. Embedded MLCCs including Taiyo Yuden's 22 microfarad 0402 product optimised for close IC placement represent the frontier of this miniaturisation trend, supporting premium pricing and technology differentiation in the competitive MLCC landscape.

The report of the Expert Market Research's titled "Global Multi-Layer Ceramic Capacitor (MLCC) Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

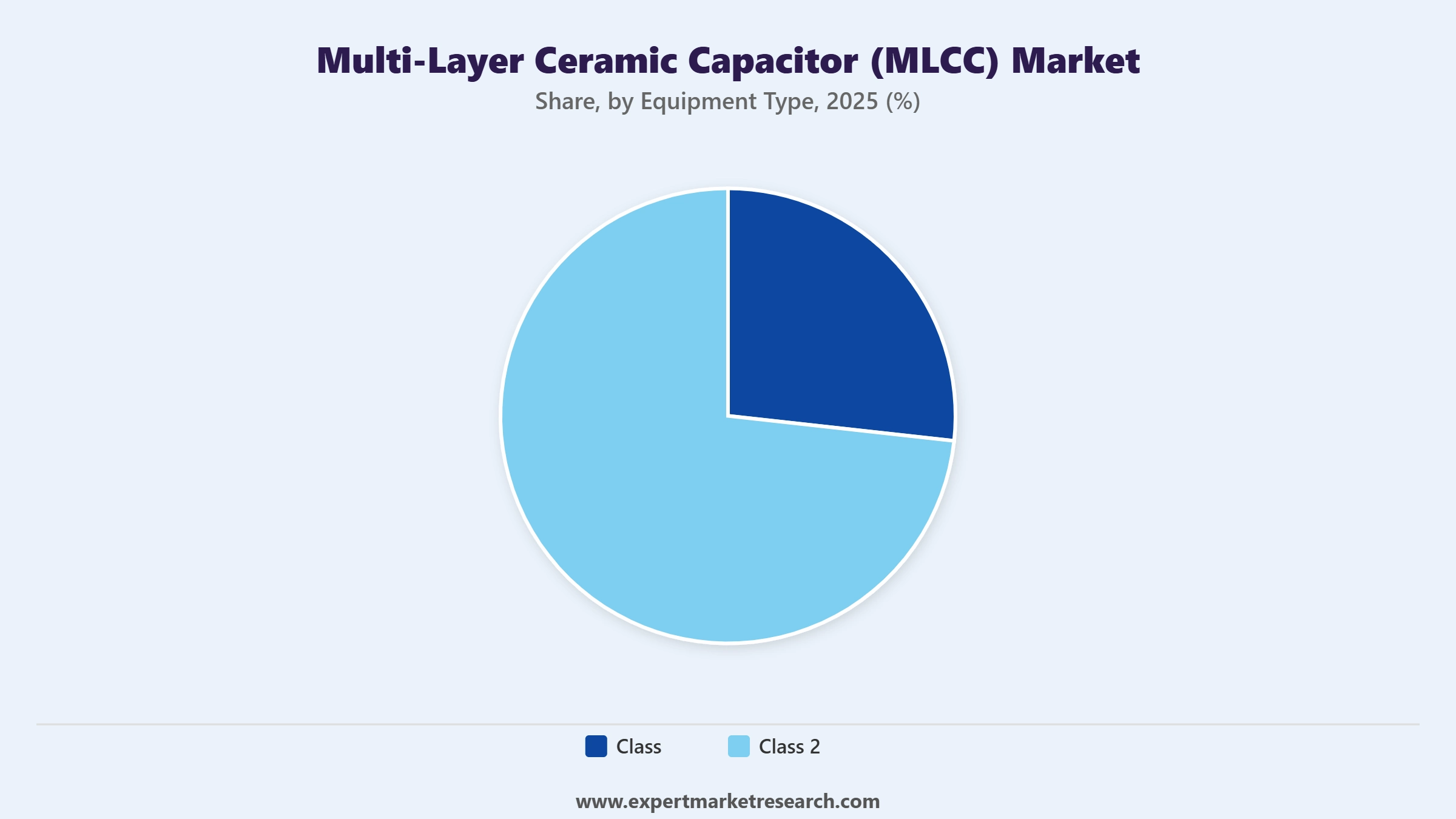

Market Breakup by Equipment Type

Key Insight: Class 2 capacitors, particularly X7R and X5R grades, dominate the global multi-layer ceramic capacitor (MLCC) market by volume and revenue, serving the broadest range of applications including consumer electronics, data centres, and automotive power management where high capacitance density is the primary requirement. Class 2 demand is being dramatically amplified by AI server deployment, with high-capacitance X7R MLCCs experiencing acute supply tightness and 15-35% price increases from Murata in March 2026. Class 1 (NP0/C0G) commands premium positioning in precision RF, medical, and automotive applications requiring temperature-stable, low-loss performance.

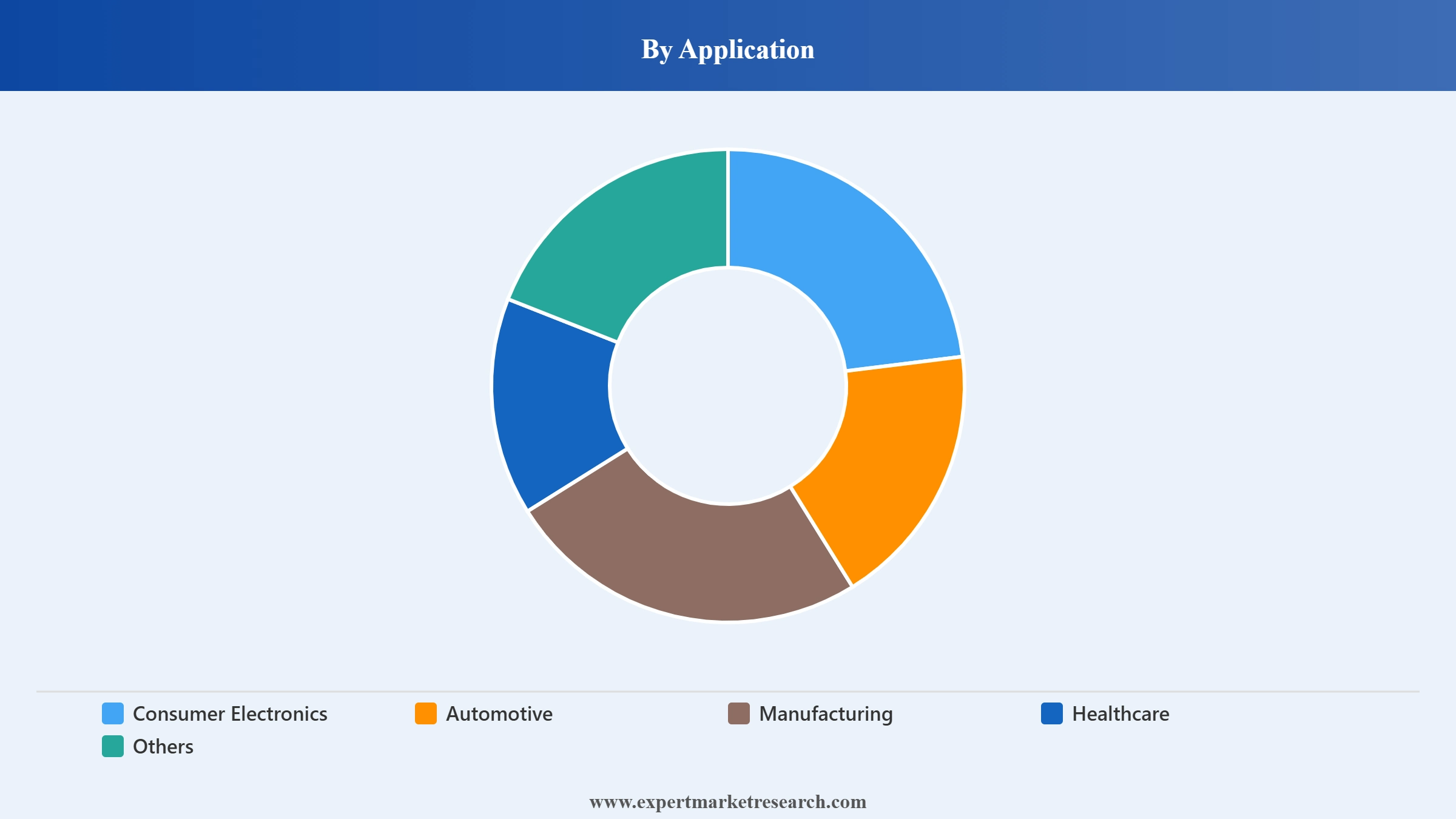

Market Breakup by Application

Key Insight: Consumer electronics commands the largest application share of the global multi-layer ceramic capacitor (MLCC) market, driven by the enormous global volume of smartphones, tablets, laptops, and wearables, each consuming hundreds to thousands of MLCCs for power management, RF filtering, and signal processing. The automotive segment is the fastest-growing application by value, propelled by EV electrification increasing MLCC content 6 to 10-fold per vehicle. The others segment, encompassing AI servers and data centre infrastructure, is the highest-impact growth driver for premium high-capacitance, high-margin MLCC product variants.

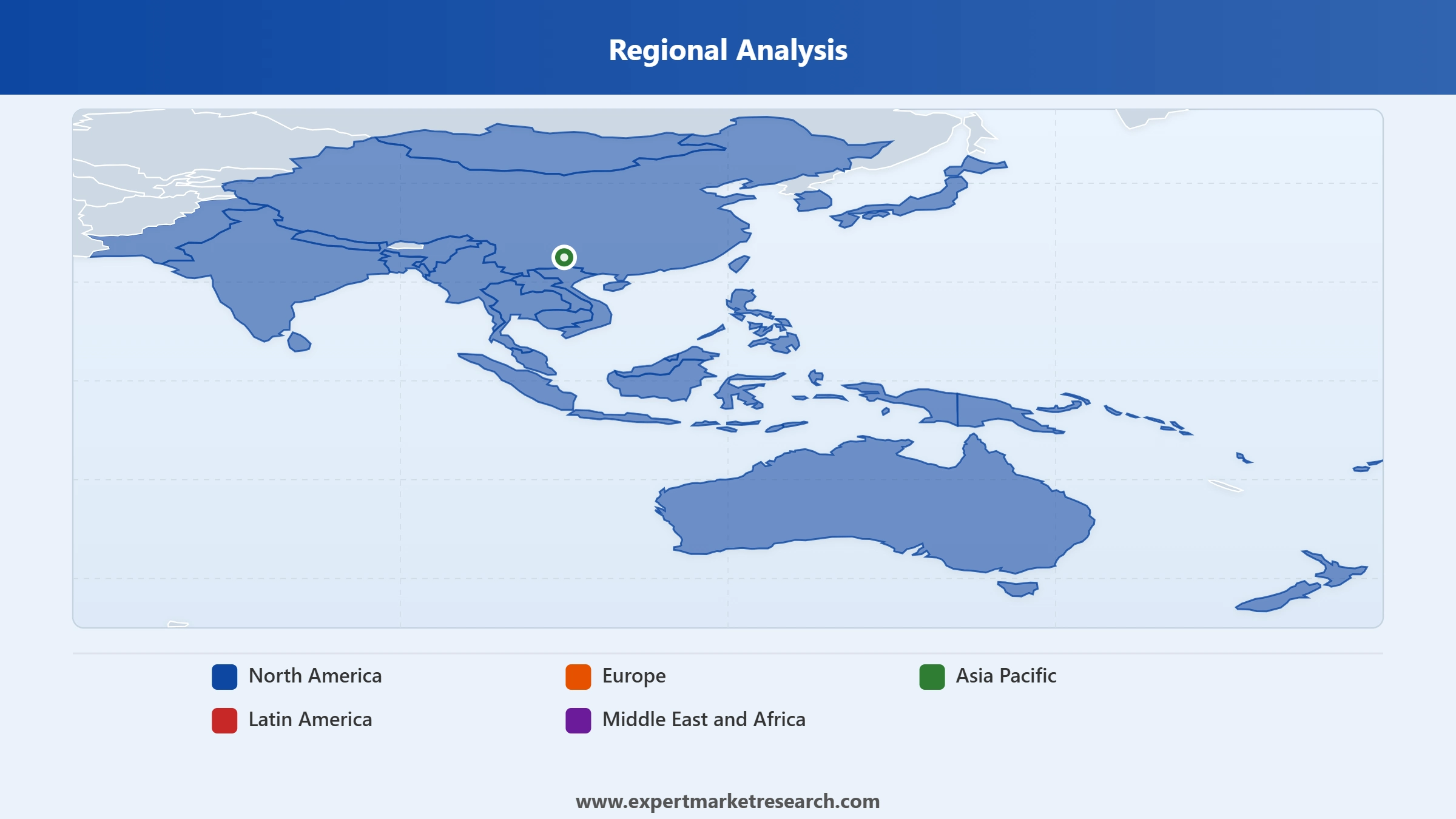

Market Breakup by Region

Key Insight: ASIA PACIFIC dominates the global multi-layer ceramic capacitor (MLCC) market both by production and consumption, hosting the world's leading manufacturers including Murata Manufacturing and Kyocera Corporation in Japan, Samsung Electro-Mechanics in South Korea, Taiyo Yuden across Japan and Southeast Asia, and Darfon Electronics in Taiwan. The region's dominance is reinforced by deep integration with the Asian consumer electronics and automotive OEM supply chains. NORTH AMERICA is the fastest-growing consumption market for premium AI server MLCCs, driven by hyperscale data centre investment by major technology companies.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Equipment Type, Class 2 capacitors account for the dominant share of the market due to the high volume requirements of consumer electronics, automotive, and AI data centre applications.

Class 2 capacitors, encompassing X7R, X5R, and related dielectric grades, hold the dominant revenue share of the global multi-layer ceramic capacitor (MLCC) market, reflecting the massive volume consumption of high-capacitance MLCCs across the broadest application categories. X7R is the most widely deployed Class 2 grade, valued for its combination of stable capacitance from negative 55 to positive 125 degrees Celsius and high capacitance density, making it the dominant choice for consumer electronics power management and automotive ADAS applications. The May 2026 Samsung Electro-Mechanics price increase evaluation of 5-10% reflected the escalating demand for Class 2 components driven by AI infrastructure investment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Class 1 capacitors including NP0/C0G and P100 represent a premium, lower-volume but higher-margin segment of the global multi-layer ceramic capacitor (MLCC) market. NP0/C0G capacitors are specified wherever temperature coefficient of capacitance must approach zero, including RF communications hardware, precision medical devices, and safety-critical automotive control modules. Taiyo Yuden's focus on automotive and communication infrastructure as part of its strategic pivot toward higher-value markets reflects the growing commercial importance of Class 1 precision capacitors. Murata's Fukui R&D facility developments in sub-0.5 micron electrode technology are expected to enhance Class 1 capacitance density over the forecast period.

By Application, consumer electronics accounts for the dominant share of the market due to the enormous global production volumes of smartphones, tablets, laptops, and wearables that individually contain hundreds to thousands of MLCCs.

Consumer electronics commands the largest application share of the global multi-layer ceramic capacitor (MLCC) market, with global smartphone production alone generating demand for tens of billions of MLCC units annually. Each high-end smartphone contains between 800 and 1,200 individual MLCCs for power regulation, RF signal filtering, antenna tuning, and baseband processing. The January 2026 observation that notebook-focused ODMs including Compal and Pegatron reduced material procurement by 5-6% month-over-month illustrates the sensitivity of consumer MLCC volumes to broader macroeconomic and demand conditions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The automotive application is the most strategically important growth segment of the global multi-layer ceramic capacitor (MLCC) market by value, driven by EV penetration multiplying MLCC content per vehicle by 6 to 10 times compared to conventional internal combustion engines. High-voltage automotive MLCCs for traction inverters, battery management systems, and onboard chargers require extreme reliability grades that command premium pricing. The April 2026 Taiyo Yuden price increase of 6-13% specifically included select automotive MLCC products, reflecting the growing pricing power that manufacturers hold in this high-barrier application segment.

Asia Pacific dominates the global multi-layer ceramic capacitor (MLCC) market due to the concentration of leading Japanese, Korean, and Taiwanese manufacturers and deep integration with regional consumer electronics and automotive OEM supply chains.

Asia Pacific commands approximately 55-60% of the global multi-layer ceramic capacitor (MLCC) market revenue, underpinned by the geographic concentration of the world's four largest MLCC manufacturers. Murata Manufacturing holds approximately 40% global MLCC market share from its Japanese manufacturing base, with capacity utilisation consistently above 80% driven by AI server demand. Samsung Electro-Mechanics holds approximately 20% global share from South Korea. Taiyo Yuden in Japan and Darfon Electronics Corporation in Taiwan contribute further to the region's dominant production base. All four companies operate at elevated capacity utilisation due to AI infrastructure demand exceeding supply growth capacity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the fastest-growing consumption region for premium AI server MLCCs within the global multi-layer ceramic capacitor (MLCC) market, driven by hyperscale data centre construction and AI infrastructure investment by major technology companies deploying NVIDIA GB200 and GB300 server systems. Kemet Corporation, headquartered in Greenville, South Carolina, manufactures a range of MLCC products serving North American industrial, medical, and defence markets. European demand for precision automotive and industrial MLCCs is growing with EV production expansion by established automakers, creating sustained demand for high-reliability automotive-grade components from Murata and Taiyo Yuden.

The global multi-layer ceramic capacitor (MLCC) market is highly concentrated, with Murata Manufacturing, Samsung Electro-Mechanics, and Taiyo Yuden collectively accounting for approximately 70-75% of global revenue. This concentration reflects the extraordinary capital intensity, materials expertise, and precision manufacturing capabilities required to produce advanced MLCCs, creating high barriers to entry that have limited competitive disruption from new entrants. Competition at the technology frontier is focused on capacitance density improvements, miniaturisation to 006003 and smaller form factors, and development of ultra-high voltage and temperature-stable automotive and AI server grades.

Headquartered in Taoyuan City, Taiwan, Darfon Electronics Corp. is a passive component manufacturer producing MLCCs, keyboards, LED lighting, and energy management products. Darfon's MLCC division serves consumer electronics OEMs across the Asia Pacific region, supplying standard-grade X7R and X5R capacitors for mainstream consumer electronics applications. The company competes in the cost-competitive segment of the global multi-layer ceramic capacitor (MLCC) market, leveraging its Taiwan manufacturing base and close relationships with Taiwanese electronics brand customers.

Founded in 1919 and headquartered in Greenville, South Carolina, Kemet Corporation is a leading manufacturer of passive electronic components including MLCCs, tantalum capacitors, and film capacitors serving industrial, automotive, defence, and telecommunications markets. Kemet's MLCC product lines cover a broad range of Class 1 and Class 2 grades with particular strength in high-reliability specifications demanded by North American defence contractors and medical device manufacturers. Kemet was acquired by Yageo Corporation in 2020, strengthening its position within the global multi-layer ceramic capacitor (MLCC) market through enhanced manufacturing scale.

Founded in 1959 and headquartered in Kyoto, Japan, Kyocera Corporation is a diversified technology manufacturer with a significant advanced ceramic components division that includes specialty MLCC production. Leveraging decades of ceramic materials expertise, Kyocera produces high-reliability MLCCs for telecommunications infrastructure, industrial electronics, and precision instrumentation applications. The company's vertically integrated ceramic materials capabilities support the development of specialty grades within the global multi-layer ceramic capacitor (MLCC) market, including high-temperature and high-frequency variants for demanding application environments.

Founded in 1944 and headquartered in Nagaokakyo, Kyoto, Japan, Murata Manufacturing Co., Ltd. is the world's largest MLCC manufacturer with approximately 40% global market share. In March 2026, Murata announced price increases of 15-35% for AI server high-capacitance MLCCs and automotive-grade products effective April 2026, reflecting production utilisation above 80% and order growth of 20-25% quarter-over-quarter in Q1 2026. In February 2026, Murata completed its Fukui R&D facility and opened an India packaging operation, advancing its materials innovation and geographic expansion strategy in the global multi-layer ceramic capacitor (MLCC) market.

Other key players in the market are Samsung Electro-Mechanics Co., Ltd., Taiyo Yuden Co., Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of insights into the global multi-layer ceramic capacitor (MLCC) industry from 2026 with our comprehensive market report. Explore AI server demand impacts, automotive MLCC content growth, pricing trend analysis, capacity investment patterns, and competitive dynamics shaping the market. Whether you are an MLCC manufacturer, electronics procurement specialist, EV supplier, or technology investor, this report delivers the intelligence you need. Download your free sample today and uncover the key opportunities transforming the global multi-layer ceramic capacitor (MLCC) industry through 2035.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 10.70 Billion.

The market is projected to grow at a CAGR of 5.00% between 2026 and 2035.

The key strategies driving the market include the miniaturization for compact electronics, expanding automotive-grade product lines, enhancing high-frequency and high-capacitance performance, investing in production automation, and strategic partnerships. Companies also focus on regional expansion, R&D for new dielectric materials, and aligning with trends in EVs, 5G, AI, and Industry 4.0.

The key trends guiding the growth of the market include the increased adoption of multi-layer ceramic capacitors for IoT applications, their use in the manufacture of smart LCD and LED televisions, and growing research and development activities.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Class and Class 2 are the major equipment types of multi-layer ceramic capacitor (MLCC) in the market. Class is subdivided by type into NP0 (C0G), and P100, among others such as N33 and N75, while Class 2 is subcategorised by type into X7R, and X5R, among others such as Z5U and X7S.

The significant applications of the product in the global multi-layer ceramic capacitor (MLCC) market include consumer electronics, automotive, manufacturing, and healthcare, among others.

The key players in the market report include Darfon Electronics Corp., Kemet Corporation, Kyocera Corporation, Murata Manufacturing Co., Ltd., Samsung Electro-Mechanics Co., Ltd., and Taiyo Yuden Co., Ltd., among others.

The consumer electronics segment dominates the market, accounting for the highest volume of consumption globally.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Equipment Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.