Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global pasta sauce market reached a value of USD 3.82 Billion at 2025 and is projected to expand at a CAGR of around 5.60% during the forecast period of 2026-2035. With premiumisation, clean-label reformulation, plant-based expansion, and rapid e-commerce growth, the market is expected to reach USD 6.59 Billion by 2035.

Compound Annual Growth Rate

5.6%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global pasta sauce category is being reshaped by four converging forces - premiumisation through clean-label and organic recipes, plant-based reformulation, format and flavour innovation (fusion and specialty SKUs), and the rapid migration of consumer purchases to e-commerce and D2C channels.

Formula One announced Barilla as the sport's official pasta partner. As part of the deal, Barilla unveiled an F1 wheel-shaped pasta SKU; while the headline product is a pasta shape, Barilla's broader sauce portfolio (Mulino Bianco, Pomi'-aligned products, and regionally tailored bases) gains co-marketing exposure across F1 events globally. The partnership reflects Barilla's deepening investment in lifestyle and sports-based brand-building beyond traditional grocery channels.

Barilla Group officially launched the Barilla Innovation & Technology Experience (BITE), a 150,000 sq ft facility in Parma backed by over USD 25 Million of investment, designed to accelerate development across pasta, sauces, and bakery. The centre consolidates Barilla's R&D, sensory science, and pilot-scale manufacturing for new sauce recipes - including premium tomato bases and pesto reformulations - and signals a structural commitment to category leadership in the global pasta and sauce ecosystem through 2035.

Barilla announced its entry into the UK fresh pasta market through a direct-to-consumer (D2C) and e-commerce-led approach. The strategic move complements Barilla's broader sauce portfolio - fresh pasta and ambient pasta sauces are typically cross-purchased - and indicates that incumbents are leveraging D2C platforms to capture premium-tier consumers and reduce reliance on retailer-controlled shelf space. The move also signals heightened competitive intensity in the UK pasta and sauce category.

Carbone Fine Food, the chef-led brand spun out of the Major Food Group restaurant operation, introduced five new pasta-sauce flavours in the United States - Sweet Pepper and Onion, Mediterranean Marinara, Mac & Cheese Alfredo, Black Truffle Alfredo, and Lemon Pepper Alfredo. The expansion deepens Carbone's premium-tier positioning and reinforces the US premiumisation trend, where organic, low-sodium, and clean-label variants command 20–40% price premiums over conventional alternatives in supermarkets.

US start-up Sauz launched two new fusion sauces - Miso Garlic Marinara and Brown Butter Alfredo - described as the first commercially available Asian-Italian fusion pasta sauces. Distribution expanded to Whole Foods and Sprouts nationwide, validating the premium fusion segment as a credible whitespace within the broader category. The launch typifies how independents are leveraging chef-led, ingredient-forward storytelling to gain modern-trade shelf space and create category-disruption pressure on incumbents.

Major incumbents are investing heavily in dedicated innovation infrastructure to defend share against premium independents. Barilla's November 2025 launch of the BITE innovation centre in Parma - backed by over USD 25 Million - is the clearest signal: BITE concentrates R&D, sensory science, and pilot manufacturing to accelerate sauce reformulation and clean-label moves. The global pasta sauce market growth therefore depends on incumbents' ability to translate R&D into shelf-ready SKUs that match independent brands' premium claims.

Independents are launching chef-led, fusion-format SKUs that move beyond traditional Italian profiles. Sauz's January 2025 launch of Miso Garlic Marinara and Brown Butter Alfredo, distributed via Whole Foods and Sprouts, exemplifies the trend. Carbone Fine Food's February 2025 expansion (Black Truffle Alfredo, Mac & Cheese Alfredo) similarly leverages restaurant credibility for premium shelf positioning. These launches validate that flavour breadth - not just Italian heritage - now drives growth in modern-trade pasta sauce sections.

Vegan and plant-based variants now anchor approximately 46% of new-launch demand, according to industry trackers. Kraft Heinz expanded its Classico line into plant-based variants, while smaller brands led the way on dairy-free Alfredo and meatless Bolognese. Plant-based pasta sauces also double as health-positioning vehicles, with low-sodium and clean-label claims attached. This trend is accelerating the migration of premium dollars from animal-protein sauces toward vegetable-, legume-, and nut-based formulations across global markets.

Pasta sauce is increasingly migrating to direct-to-consumer and e-commerce channels. Barilla's November 2025 entry into UK fresh pasta via a D2C/e-commerce playbook - bypassing some retailer-controlled shelves - is illustrative. E-commerce is enabling premium-tier and bundle-led selling, longer-tail SKU economics, and subscription-based purchase journeys. Modern-trade share remains dominant globally, but the fastest growth in distribution is being captured by online and specialty channels through 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Pasta sauce is a cream-based liquid or semi-solid, which is used as a delicious topping over pasta as well as other Italian dishes like pizza and lasagne. A combination of ingredients like tomatoes, onions, garlic, cheese, grasses, and seasonings is widely used for a special flavour and taste. It is rich in many macronutrients, vitamins, minerals as well as fibres. The most popular variants are red, green, dairy, carnivorous, emulsified, butter, and vegetable sauces. They are typically packaged and distributed with plastic bags and packets in glass and aluminium containers.

On the basis of product type, the pasta sauce market is divided into the following:

Key Insight: Tomato-based sauces hold the largest share - broadly above half of the category, with industry trackers placing the share around 55%. They anchor mass-market demand thanks to familiarity, lower price points, and broad recipe versatility. Pesto-based and Alfredo-based sauces are growing faster than tomato-based on a percentage basis, capturing premium and indulgent occasions. Carbone Fine Food's February 2025 expansion into Black Truffle Alfredo, Mac & Cheese Alfredo, and Lemon Pepper Alfredo illustrates the premium Alfredo whitespace.

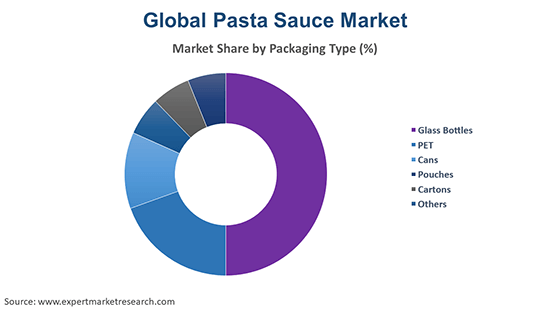

Based on the packaging type, the industry is segmented into:

Key Insight: Glass bottles dominate packaging share, valued at roughly 38.6% of the market in 2024 according to industry trackers, because of their premium signalling, freshness preservation, and recyclability. PET and pouches are gaining share at the value end and in food-service B2B. Cans remain relevant for industrial users and emerging markets where supply-chain robustness is preferred. Sustainability claims are reshaping packaging choices, with lightweight glass and recyclable cartons gaining incremental share.

The distribution channel can be categorised as follows:

Key Insight: Supermarkets and hypermarkets dominate, capturing roughly 47.4% of pasta sauce sales in 2024 thanks to convenience, broad assortment, and price competitiveness. Online and e-retailing is the fastest-growing channel - accelerated by Barilla's UK D2C entry - supported by premium-tier subscription and bundling models. Specialty stores serve gourmet and chef-led brands; convenience stores are smaller but relevant for single-serve and ready-meal-adjacent SKUs.

The regional pasta sauce markets include:

Key Insight: Europe - particularly Italy - is the historical anchor of pasta sauce demand and exports. North America is the largest single regional market by value, with strong premiumisation and clean-label momentum. Asia Pacific is the fastest-growing region (CAGR ~6.3%) on the back of rising disposable incomes, the globalisation of Italian cuisine, and modern-trade expansion. Latin America (Brazil, Mexico) is large, while Middle East and Africa is small but growing as foodservice and e-commerce penetration deepen.

By Type: Tomato-based sauces dominate global type share - roughly 55% - because they anchor mass-market consumption across virtually every region and price tier. They are also the entry point for new pasta consumers in emerging markets, lock in repeat purchase, and provide the volume that supports private label. Carbone Fine Food's February 2025 premium expansion - including a Mediterranean Marinara - reinforces that even premium players ground their pipelines in tomato-base innovation, confirming category leadership.

By Packaging Type: Glass bottles dominate packaging share at ~38.6% in 2024 because they signal premium quality, preserve flavour and freshness, and align with sustainability claims (recyclability and reusability). They are the format of choice for premium tier brands and clean-label launches. The supporting evidence is Sauz's January 2025 Asian-Italian fusion launches in glass jars at Whole Foods, illustrating how premium positioning consistently chooses glass to communicate quality and command higher price points.

By Distribution Channel: Supermarkets and hypermarkets dominate at ~47.4% of pasta sauce sales in 2024, supported by convenience, breadth of assortment, and price competitiveness across mass and premium tiers. Online and e-retailing is the fastest-growing channel and is reshaping distribution economics. Barilla's November 2025 UK D2C entry exemplifies how leading brands now treat e-commerce as a strategic channel rather than an adjunct to modern trade, supporting category premiumisation and tail-SKU economics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America: The largest regional market by value, anchored by the United States and supported by Canada. Drivers include premiumisation, clean-label and low-sodium reformulation, the rise of chef-led brands such as Carbone Fine Food and Rao's (Sovos Brands / Campbell), and the rapid expansion of fusion SKUs from independents like Sauz. Modern-trade chains (Walmart, Kroger, Costco) drive volume; specialty channels (Whole Foods, Sprouts) drive premium share. Investment is flowing into healthier formulations, plant-based variants, and e-commerce private-label. January 2025 launches by Sauz, and February 2025 expansion by Carbone Fine Food, exemplify the innovation pipeline.

Europe: The historical heart of pasta and pasta-sauce consumption, anchored by Italy with Germany, France, Spain, and the UK as anchor markets. Italy's centuries-old culinary tradition supports strong export volumes, while UK and German consumers drive premium and clean-label demand. Barilla's November 2025 BITE innovation centre in Parma - backed by USD 25 Million plus - and its UK D2C fresh-pasta entry illustrate how European incumbents are re-investing in R&D and direct channels. European retailers also lead on sustainability standards (recyclable packaging, plant-based labelling), shaping global supplier specifications.

The global pasta sauce market is moderately consolidated at the top, with a handful of multinationals - Barilla, Nestlé, General Mills, De Cecco, and Mizkan-led brands - controlling significant share alongside private label and chef-led independents. Competitive priorities have shifted from cost-led commodity tomato base toward premiumisation, plant-based reformulation, fusion flavours, sustainable packaging, and e-commerce/D2C distribution.

The next layer is dynamic: regional leaders, premium independents (Carbone Fine Food, Rao's, Sauz), private-label players (Aldi, Lidl, Costco-Kirkland), and rising emerging-market players are taking share. Multinationals are responding through R&D infrastructure (Barilla BITE), bolt-on M&A, innovation hubs, and sports/lifestyle partnerships (Barilla x Formula One) - making competitive intensity higher and the second tier a meaningful innovation engine.

Founded in 1877 and headquartered in Parma, Italy, Barilla is the world's largest pasta and pasta-sauce maker, with 28 production sites across 9 countries. Capabilities span pasta, ready sauces (Pomi'-aligned, Mulino Bianco), bakery, and fresh pasta. Strengths include the November 2025 BITE innovation centre, the Formula One partnership, the UK fresh-pasta D2C entry, and 84+ active university partnerships supporting open innovation across pasta and sauce R&D.

An Italy-based pasta and pasta sauces specialist, Fratelli operates across Italian and export markets with a focus on traditional tomato-base, pesto, and regional Italian sauce recipes. Capabilities include sourcing of Italian tomato varieties, glass-bottle premium formats, and chef-led recipe development for premium-tier consumers. Strengths sit in heritage credibility and curated specialty distribution channels across Europe and select export markets.

Founded in 1866 and headquartered in Vevey, Switzerland, Nestlé is one of the world's largest food and beverage companies. Capabilities include culinary brands (Maggi, Buitoni-aligned recipes), frozen meals, and ready sauces across global markets. Strengths in pasta sauce stem from chilled and ambient distribution scale, particularly in Europe and Latin America, alongside cross-category R&D and ingredient sourcing power that supports clean-label reformulation.

Founded in 1886 and headquartered in Fara San Martino, Italy, De Cecco is a heritage Italian pasta and pasta sauce producer recognised globally for premium-tier durum-wheat pasta and tomato-base sauces. Capabilities span specialty Italian recipes, premium glass-bottle packaging, and a strong export footprint across North America and Asia Pacific. Strengths include heritage credibility, premium positioning, and recipe authenticity that supports competitive pricing power.

Other key players in the market are Makfa JSC, Durum Gida Sanayi Ve Ticaret A.S, General Mills, Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the global pasta sauce market 2026 with our comprehensive report. Stay ahead of the curve with verified data on premiumisation, plant-based reformulation, packaging innovation, and the strategies of Barilla, Nestlé, De Cecco, and General Mills. Whether you are launching a new sauce range, expanding into a new region, or evaluating channel investments, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving global Pasta Sauce space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 3.82 Billion.

The market is projected to grow at a CAGR of 5.60% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035. to reach USD 6.59 Billion by 2035.

Growth is driven by busy lifestyles fuelling demand for ready-to-use meal solutions, premiumisation around clean-label and organic recipes, plant-based reformulation, R&D investments by incumbents like Barilla, the rise of chef-led independents (Carbone Fine Food, Rao's, Sauz), and rapid e-commerce/D2C distribution growth.

The market is segmented by Tomato-Based, Pesto-Based, Alfredo-Based and Others. Tomato-based sauces dominate at roughly 55% share. Within tomato-based, traditional, marinara, and meat sauces lead, while pesto and Alfredo-based variants capture premium occasions.

Premiumisation through clean-label and organic recipes, plant-based reformulation, fusion and chef-led flavour innovation, sustainable packaging migration, and the rapid expansion of D2C and e-commerce distribution.

The key players in the market include Barilla G. e R., Fratelli S.p.A, Nestlé S.A., F.lli De Cecco di Filippo Fara San Martino S.p.A (De Cecco), Makfa JSC, Durum Gida Sanayi Ve Ticaret A.S, General Mills, Inc. and Others.

North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa are the major regions covered in the market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Packaging Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.