Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

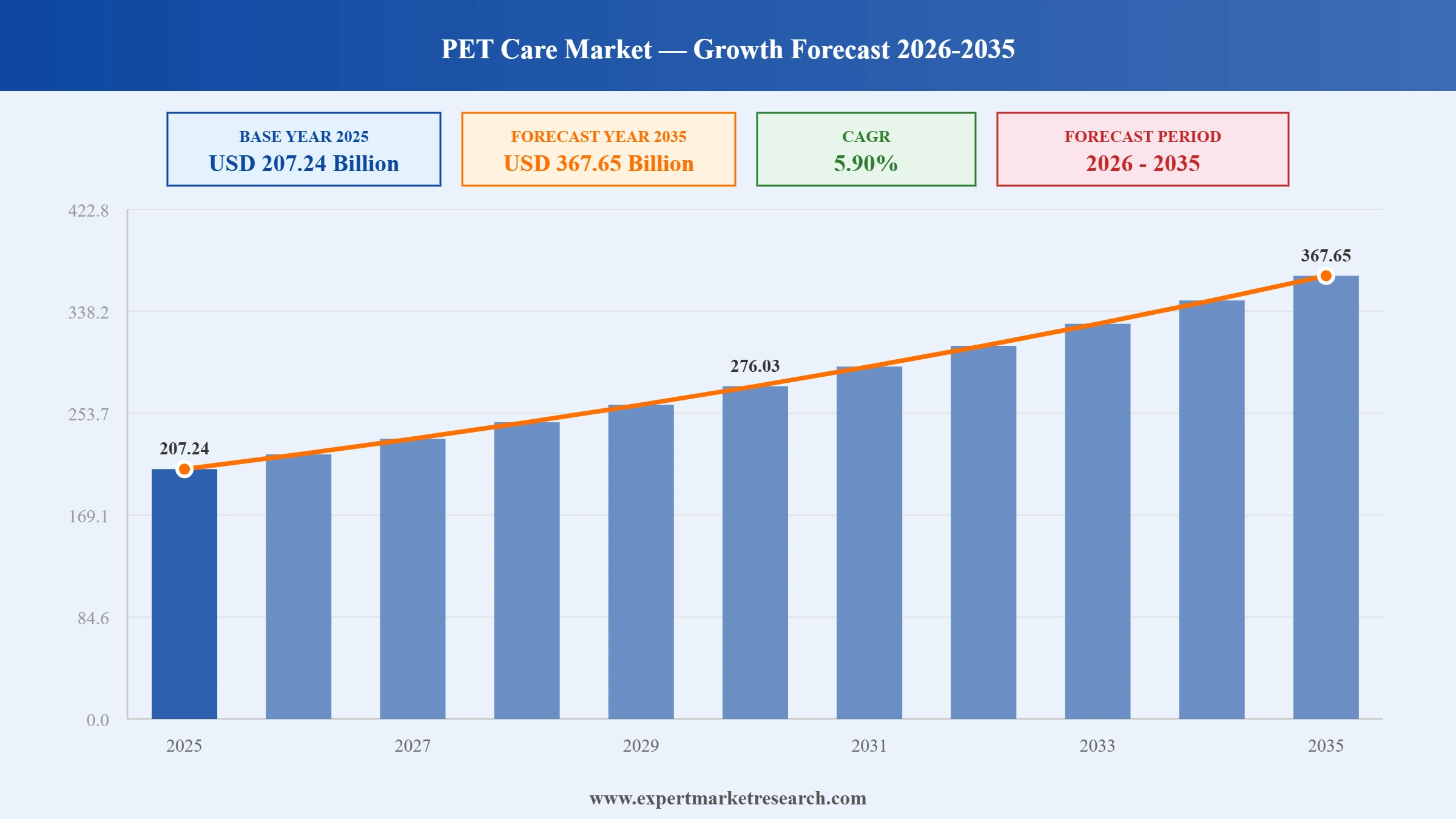

The global pet care market was valued at USD 207.24 Billion in the year 2025 and is projected to reach USD 367.65 Billion by 2035, growing at a CAGR of 5.90% during the forecast period 2026 and 2035, according to Expert Market Research. This sustained and compounding growth reflects the deepening integration of companion animals into household life across every major region globally, driving structural expansion in pet food, veterinary services, grooming, accessories, insurance, and technology-enabled care products.

The pet care industry occupies a uniquely resilient position within consumer spending: pet owners across income brackets consistently classify expenditure on companion animal health and nutrition as non-discretionary, maintaining spending levels even during periods of broader economic pressure. This spending resilience, combined with accelerating premiumisation in pet nutrition, the expansion of veterinary services infrastructure, and the rapid growth of organised pet care services in emerging markets, positions the global pet care market as one of the most durable long-term growth categories within the consumer goods and healthcare sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The pet care market encompasses the full spectrum of products and services purchased by pet owners for the health, nutrition, grooming, safety, and well-being of companion animals. The market spans pet food and treats, veterinary and pharmaceutical products, grooming and hygiene products, accessories including collars, cages, and bedding, pet insurance, boarding and training services, and emerging technology products including smart feeders, GPS tracking devices, and remote health monitoring systems. Companion animals served include dogs, cats, birds, fish, reptiles, and small mammals, with dogs and cats accounting for the dominant share of global pet care expenditure.

The modern pet care market is shaped by a convergence of emotional, social, and economic forces: the humanisation of pets as family members rather than property; the application of human health and wellness paradigms to companion animal care; and the entry of sophisticated retail, technology, and healthcare companies into a sector that was historically dominated by specialist manufacturers and independent veterinary practices. This convergence is expanding the market's structural complexity and creating commercially attractive sub-segments across every tier of the care value chain.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The humanisation of pets the progressive social and cultural phenomenon in which companion animals are attributed with family member status and treated accordingly in terms of care investment and emotional priority is the foundational demand driver of the global pet care market. As pet owners increasingly apply the standards of human healthcare, nutrition, and lifestyle to their companion animals, the commercial definition of adequate pet care has expanded substantially. Spending patterns that were once confined to basic nutrition and routine veterinary check-ups now extend to therapeutic nutrition, preventive pharmaceutical care, behavioural training, wellness services, pet insurance, and lifestyle accessories that mirror the product categories available in human consumer markets. This expansion of the "pet parent" consumer identity is irreversible, culturally embedded, and accelerating across every major market regardless of income level, though the rate of premium product adoption varies significantly by geography.

Premiumisation the structural consumer shift from standard pet food toward nutritionally enhanced, ingredient-transparent, breed-specific, life-stage-targeted, and functionally positioned products is the single most commercially significant trend reshaping the pet food segment. Pet owners who view their animals as family members apply their own health and wellness values to pet nutrition decisions, creating sustained demand for grain-free, organic, raw, high-protein, weight-management, and veterinarian-formulated food products. Functional pet foods ranging from probiotic-enriched formulas to cognitive health treats for ageing pets are generating premium pricing power and superior margin profiles for manufacturers who invest in ingredient quality and clinical substantiation. Nestlé Purina's BRL 2.5 billion investment in Brazilian wet pet food manufacturing capacity in March 2026 reflects industry confidence in the durability of premium pet nutrition demand across both developed and emerging markets.

Veterinary care is the most rapidly expanding segment within the broader pet care services market, driven by the convergence of rising pet ownership, growing consumer investment in companion animal health, expanding veterinary clinic infrastructure, and the integration of technology into both clinical and remote care delivery. Pet owners' increasing willingness to invest in diagnostic services, preventive pharmaceutical treatments, specialist referrals, and elective procedures is expanding the commercial opportunity for veterinary service operators significantly. In North America, where the veterinary care market commands substantial consumer attention across multiple GSC query categories, the consolidation of veterinary practices into multi-site groups and the emergence of hybrid care models combining in-person clinics with 24/7 virtual consultation exemplified by Chewy's April 2026 acquisition of Modern Animal are reshaping care delivery economics and expanding geographic access.

Emerging markets represent the most compelling long-term growth opportunity for the global pet care industry. In India, China, Brazil, and Southeast Asia, rising disposable income, urbanisation, and changing household structures are driving first-generation pet ownership at scale. Agriculture and Agri-Food Canada noted in May 2026 that dogs account for approximately 85% of India's pet population, with organised pet care adoption accelerating rapidly as branded products displace homemade and unbranded solutions. In China, the State Council Information Office noted approximately 17.07 million people engaged in exotic pet ownership by April 2025, alongside established cat and dog ownership concentrated in urban centres. These markets are characterised by younger, digitally native pet owner demographics who are highly receptive to e-commerce, direct-to-consumer brands, and social-media-informed pet care decisions, creating commercially distinct demand profiles that are increasingly attractive to global brands and domestic manufacturers alike.

Technology is penetrating every layer of the pet care value chain, from connected feeding and monitoring devices for companion animals to AI-powered veterinary diagnostic tools and e-commerce platforms that enable subscription-based nutrition delivery and telehealth consultations. The US pet tech market is projected to grow at a CAGR of 13.10% between 2026 and 2035, according to Expert Market Research, with tracking equipment, monitoring devices, smart feeding systems, and entertainment technology collectively expanding the technology-enabled segment. Chewy's evolution into an integrated pet healthcare ecosystem through its Vet Care clinics and digital pharmacy infrastructure represents the most advanced commercial expression of this trend: a vertically integrated model that combines care, commerce, and services within a single relationship platform. Platform-level integration of pet health data, purchase history, and veterinary records is creating the foundation for personalised, proactive care models that will define the competitive frontier of the pet care market through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The functional pet nutrition segment which encompasses foods, treats, and supplements formulated to address specific health objectives including joint mobility, cognitive function, digestive health, immune support, and weight management is the fastest-growing subsegment within pet food. Vet-backed product formulations, which carry credibility signals that resonate strongly with health-conscious pet owners, are gaining disproportionate market share at premium price points. Elanco Animal Health's launch of the Pet Protect supplement line covering joint health, multivitamins, Omega-3, calming, allergy, and immune support reflects the broadening commercialisation of the functional pet nutrition category across pharmaceutical-grade and mass-market channels simultaneously.

Pet fitness and wellness encompassing structured exercise, weight management programmes, preventive pharmaceutical care, and physical therapy for companion animals is an emerging commercial category with significant revenue potential. GSC data for the Expert Market Research pet care page shows 109 impressions at position 46 for "pet fitness care market," signalling meaningful search demand for this sub-topic. The GCC market, which registers 119 impressions for "gcc pet obesity market" in GSC data, represents a geographically specific wellness concern driven by the prevalence of sedentary indoor pet lifestyles in hot-climate urban environments across Gulf Cooperation Council countries. Both the pet fitness and pet obesity sub-segments are expected to generate growing product and service demand across veterinary, nutrition, and connected device categories.

Smart pet technology is transitioning from discretionary lifestyle purchase to mainstream care tool as device costs decline, connectivity infrastructure matures, and pet owners become accustomed to data-driven health management for their own lives. The product categories driving adoption include GPS tracking collars and location devices, smart automatic feeders with portion control and scheduling functions, wearable health monitors that track activity levels and vital signs, interactive cameras with two-way audio for remote monitoring, and AI-powered health analytics platforms that identify behavioral changes associated with health deterioration. The 13.10% CAGR projected for the US pet tech market through 2035, according to Expert Market Research, reflects the early-stage adoption curve of a category with substantial room for penetration expansion as price points fall and consumer familiarity grows.

Sustainability is becoming a significant product positioning and purchasing criterion for a growing segment of environmentally conscious pet owners, particularly in Western European and North American markets. Demand for sustainable packaging, certified-organic ingredients, ethically sourced protein alternatives including insect-based and plant-based formulas, and responsibly manufactured accessories is creating product innovation incentives across the pet food and grooming segments. Brands that credibly communicate their environmental credentials through ingredient sourcing transparency, packaging reduction, and carbon footprint commitments are gaining commercial traction among millennial and Gen Z pet owners who apply their personal environmental values to purchasing decisions for companion animals.

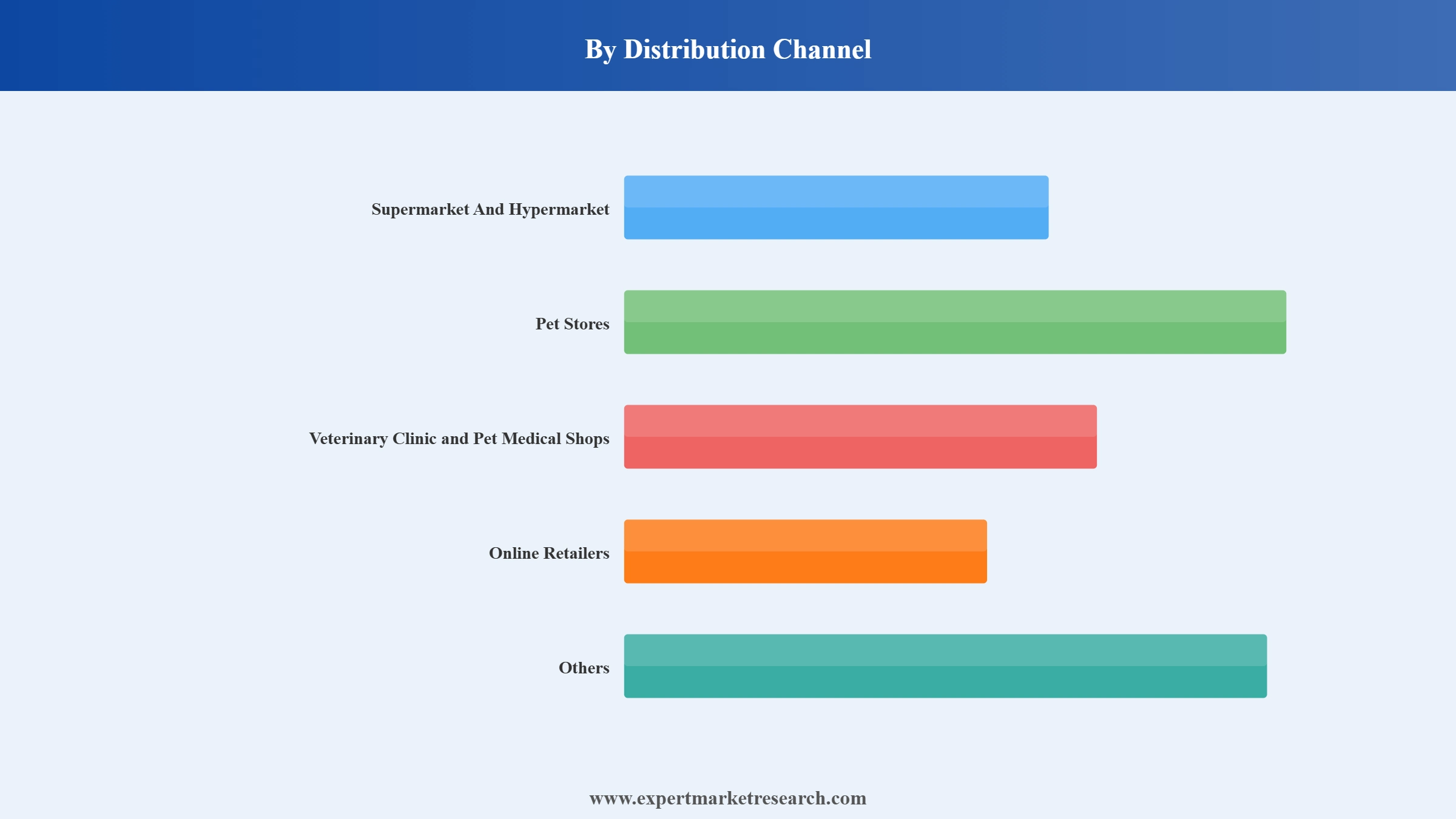

Online retail channels are fundamentally reshaping pet care distribution, enabling subscription-based nutrition delivery, direct-to-consumer brand building, and platform-level integration of health data with purchase recommendations. E-commerce platforms for pet care benefit structurally from the replenishment nature of core product categories food, litter, and medications require regular purchase on predictable schedules making subscription models and loyalty programmes commercially effective retention tools. Chewy's reported net sales of USD 3.36 billion for Q1 fiscal year 2026 ended May 3, 2026, representing 7.7% year-over-year growth, demonstrates the commercial scale achievable through pure-play online pet care retail with integrated veterinary services.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global pet care market faces compound challenges that test both product manufacturers and service providers simultaneously. The premiumisation of pet nutrition while a powerful revenue growth driver concentrates market share in higher-priced categories that are sensitive to consumer confidence and discretionary income shifts; Capstone Partners observed in its April 2026 sector update that middle- and lower-income households in North America are demonstrating trade-down behaviour toward value-positioned and efficacy-focused consumable formulations, creating margin pressure for premium-tier brands dependent on volume from this demographic. Veterinary services face a structural workforce shortage, with veterinary professional availability failing to keep pace with the growth in companion animal populations and owner expectations, constraining clinic capacity and extending wait times in key markets. Raw material price volatility affecting protein inputs, packaging materials, and active pharmaceutical ingredients creates cost uncertainty that compresses manufacturer margins and requires sophisticated supply chain management capabilities that smaller operators often lack. Regulatory complexity compounds these challenges: balancing consumer demand for functional additives such as probiotics and cannabidiol-based products with evolving regulatory standards across different jurisdictions can extend product development timelines and increase compliance costs significantly.

Several structural dynamics constrain the pace of global pet care market expansion, particularly in high-potential emerging market geographies. Consumer price sensitivity in price-conscious markets including India, Southeast Asia, and parts of Latin America limits the penetration of branded, organised pet care products relative to homemade and unbranded alternatives, requiring significant investment in consumer education and distribution infrastructure before commercial returns materialise. The concentrated nature of the pet food manufacturing landscape where a small number of global companies including Mars Petcare, Nestlé Purina, and Hill's Pet Nutrition command disproportionate shelf space and retailer relationships creates formidable barriers for independent and emerging brands seeking scale distribution. Supply chain disruption risk, which was acutely demonstrated during the pandemic period, continues to pose intermittent challenges to pet food manufacturers dependent on complex global ingredient sourcing. In the veterinary and pharmaceutical segments, the intellectual property landscape for novel therapeutic compounds and prescription nutrition products requires substantial R&D investment with long return timelines, moderating innovation pace relative to human pharmaceutical development.

The global pet care market presents substantial and diversifying investment and revenue opportunities across every dimension of the value chain. Emerging markets most prominently India, China, Brazil, and Southeast Asian economies represent structurally underpenetrated addressable markets where the combination of rising disposable income, cultural shifts toward pet ownership, and expanding e-commerce infrastructure is creating the conditions for sustained double-digit revenue growth in organised pet care categories. The veterinary and preventive healthcare segment offers particularly compelling opportunity as the convergence of telehealth, wearable monitoring, and AI-powered diagnostics creates scalable integrated care models that can serve geographically dispersed pet owner populations more efficiently than traditional clinic infrastructure alone. The pet insurance segment growing rapidly as pet owners seek financial protection against escalating veterinary costs is attracting investment from both established insurers and pet-sector pure plays, with the North American Pet Health Insurance Association reporting written premium crossing USD 5.2 billion at year-end 2024. Functional nutrition, sustainable product lines, and smart pet technology each represent commercially attractive niche opportunities within the broader premium market that reward brand credibility, ingredient transparency, and technological differentiation.

The EMR’s report titled “Pet Care Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

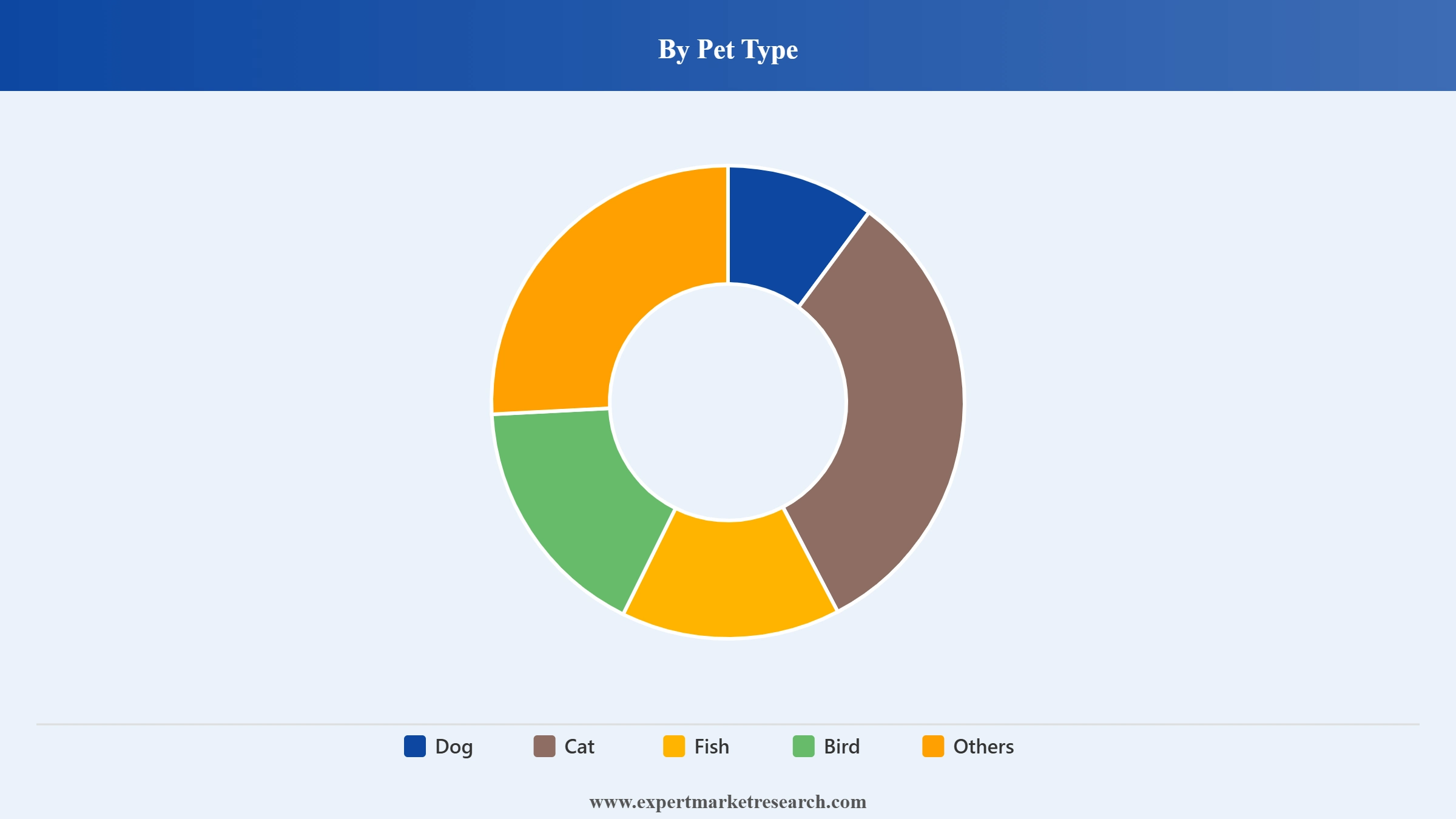

Market Breakup by Pet Type

Dogs command the largest revenue share within the global pet care market, driven by their dominance as the most widely owned companion animal type globally and the breadth and depth of spending across all care categories that dog ownership generates. Dogs require daily feeding, regular veterinary care, grooming based on breed-specific needs, training services, exercise accessories, and insurance, creating a comprehensive and recurring commercial relationship that makes the dog owner segment disproportionately valuable to pet care operators across all segments.

Cats are the fastest-growing pet type segment by CAGR, driven by their suitability for smaller urban living environments, lower maintenance demands relative to dogs, and the growing appeal of cat ownership among single-person households and working professionals in high-density cities. Rising cat ownership in Japan, South Korea, China, and European metropolitan areas is expanding the addressable market for cat-specific nutrition, healthcare, and accessories.

Others including birds, fish, reptiles, and small mammals represent a growing segment as exotic pet ownership expands globally, with China's State Council Information Office noting approximately 17.07 million people engaged in exotic pet ownership by April 2025.

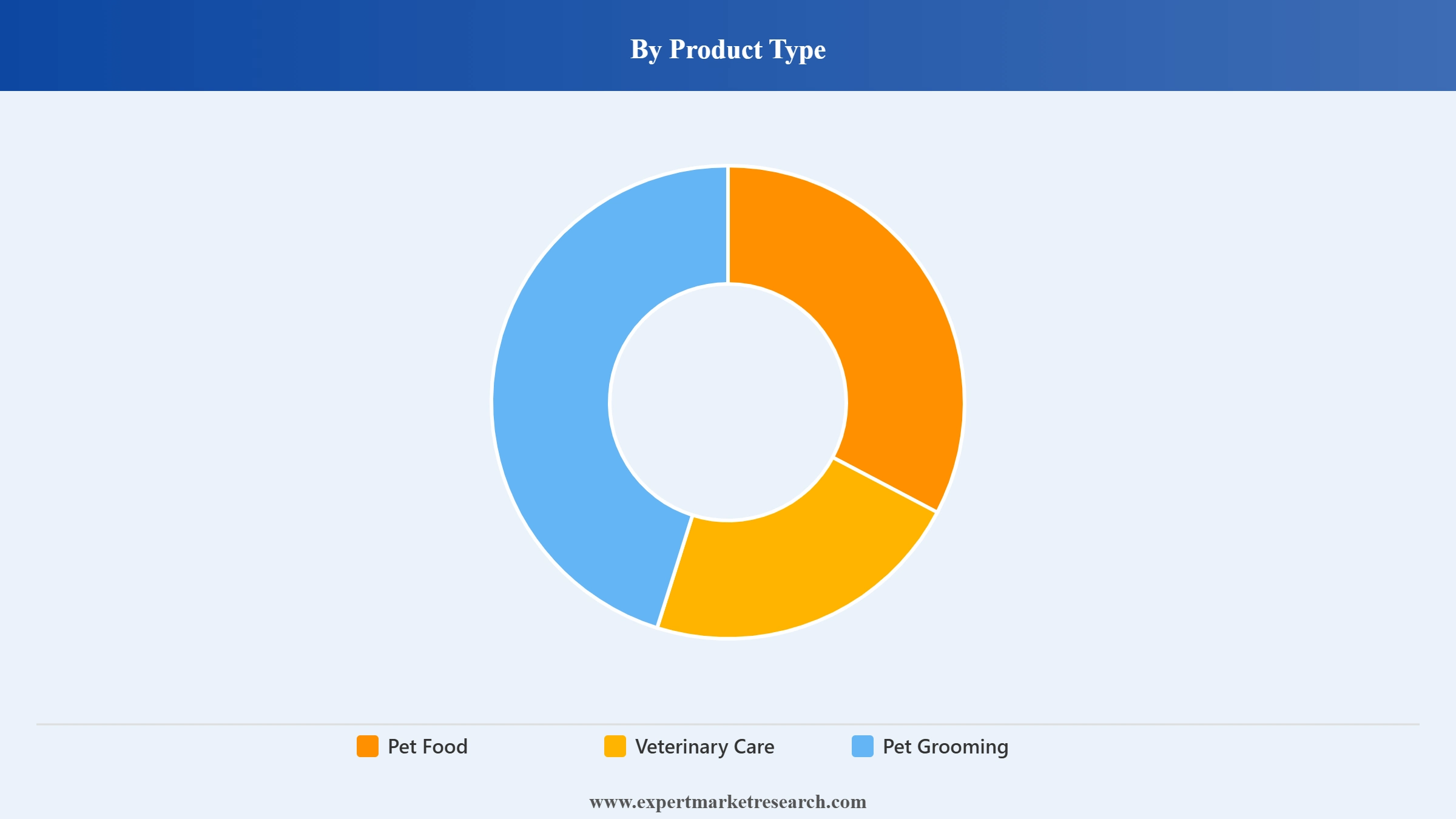

Market Breakup by Product Type

Pet Food and Nutrition represents the largest product segment within the global pet care market, driven by the fundamental daily requirement of companion animal feeding combined with the powerful premiumisation and functional nutrition trends reshaping spending per animal. Pet food encompasses dry kibble formulations, wet and canned products, raw and freeze-dried diets, semi-moist varieties, and treats including dental chews, training treats, and functional snack products. The shift toward breed-specific, life-stage-targeted, and nutritionally enhanced formulations is expanding average selling prices and generating superior margin performance for manufacturers who have invested in product differentiation. Subscription-based meal delivery services for pet food, modelled on the direct-to-consumer fresh pet food platforms pioneered in North America, are gaining adoption in European and Asia Pacific markets as e-commerce infrastructure matures.

Veterinary and Medical Care is the fastest-growing service segment within the global pet care market, encompassing routine wellness visits, diagnostic imaging and laboratory services, surgical procedures, pharmaceutical prescriptions, dental care, and specialist referral services. The integration of veterinary practices into consolidated multi-site operator groups, combined with the emergence of hybrid care models combining in-person examination with telehealth consultation, is both expanding veterinary access and improving the economics of care delivery. Regulatory developments including the FDA's April 2023 enforcement of Guidance for Industry 256 governing pet pharmacy compounding are reshaping the pharmaceutical segment of veterinary care, creating more scalable operating environments and new consolidation opportunities.

Pet Grooming and Hair Care Products encompass professional grooming services, including bathing, clipping, de-shedding, and styling, as well as retail grooming products including shampoos, conditioners, brushes, nail care tools, and dental hygiene products. GSC data showing 52 impressions for "pet hair care market" and three grooming-specific queries reflects meaningful consumer information demand in this sub-segment. The grooming market benefits from the non-discretionary character of hygiene maintenance for long-haired breeds and from the premiumisation of pet grooming services into spa-format experiences that command premium pricing.

Pet Accessories span a broad range of non-consumable products including collars, leads, harnesses, bedding, crates, carriers, litter solutions, environmental enrichment toys, and safety products. Accessories represent the most fashion-forward segment of the pet care market, with design, brand, and lifestyle positioning playing a growing role in purchase decisions alongside functional criteria.

Market Breakup by Distribution Channel

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the world's largest and most sophisticated pet care market, anchored by the United States where the pet industry reached USD 158 billion in total consumer spending in 2025 according to the American Pet Products Association. North America benefits from the world's highest per-pet spending levels, the most advanced veterinary care infrastructure, the deepest penetration of premium nutrition and functional food products, and the most developed pet insurance market. Multiple GSC query clusters including "north america veterinary care market" with over 208 combined impressions across six related queries confirm sustained research interest in the North American sub-market. The consolidation of veterinary practices into multi-site groups, the expansion of integrated pet healthcare platforms combining e-commerce with clinic services, and the premiumisation of both food and service categories continue to drive above-market revenue growth in North America relative to the broader global pet care market.

Europe is the second-largest regional pet care market globally, characterised by high pet ownership penetration in Germany, France, the United Kingdom, and the Netherlands and a strongly developed premium food culture shaped by European consumer preference for clean-label, natural-ingredient products. GSC data reveals meaningful UK-specific research activity with queries including "uk pet care market size" (69 impressions), "uk home and pet care market" (21 impressions), and "uk pet care market" (10 impressions) reflecting a commercially distinct sub-market that warrants specific coverage. Pets at Home, the UK's largest pet care specialist retailer, reported statutory revenue of GBP 1,482.1 million for fiscal year 2025, reflecting the organised pet retail market's continued scale in the UK despite broader economic pressure. The UK pet care market is further characterised by relatively high pet insurance adoption rates, strong demand for veterinary specialist services, and a growing premium grooming services sector.

Asia Pacific is the fastest-growing regional market in the global pet care industry, driven by the simultaneous expansion of pet ownership across China, India, South Korea, Japan, Australia, and Southeast Asian economies at different stages of the pet care market development curve. China's pet economy has benefited from official government attention, with the State Council Information Office acknowledging the economic significance of the companion animal sector in April 2025. India's pet care industry is projected to grow at a CAGR that leads major economies through the forecast decade, driven by a combination of rising disposable income among urban working-age populations, growing social normalisation of organised pet care, and expanding e-commerce infrastructure that provides first-time access to branded products in non-metro markets. Agriculture and Agri-Food Canada confirmed in May 2026 that dogs account for approximately 85% of India's pet population, indicating a dog-centric market structure similar to Western markets that supports strong pet food and veterinary care revenue potential.

The GCC pet care market is an emerging and commercially distinctive sub-market within the broader Middle East region, driven by high-income urban pet ownership concentrated in Saudi Arabia, the UAE, Qatar, and Kuwait. GSC data showing 119 impressions for "gcc pet obesity market" at position 69 signals a regionally specific health concern the prevalence of sedentary, indoor pet lifestyles in hot-climate urban environments that is driving demand for both veterinary weight management services and functional nutrition products. The GCC market is characterised by high willingness-to-pay for premium imported pet care products, limited domestic pet care manufacturing, and a growing veterinary services sector supported by expatriate demand and rising national awareness of companion animal welfare. The formal pet food market in the GCC is expanding rapidly as traditional attitudes toward pet ownership evolve, creating a long-runway adoption opportunity for organised pet care brands entering the region.

Latin America is a priority emerging market for the global pet care industry, with Brazil, Mexico, and Argentina representing the largest commercial opportunities within the region. Nestlé Purina's BRL 2.5 billion investment in a new Brazilian wet pet food factory in March 2026 is the most significant recent signal of global industry confidence in Latin American market growth potential. Brazil already hosts one of the world's largest pet populations and a growing middle-income pet owner demographic that is transitioning toward branded and premium pet nutrition products. The region is characterised by strong dog ownership culture, an expanding veterinary services sector, and the rapid emergence of specialist pet retail and e-commerce channels that are replacing traditional informal distribution models.

The global pet care market is characterised by a concentrated core of large multinational consumer goods and healthcare companies controlling the highest-volume product categories, alongside a dynamic ecosystem of specialist brands, regional leaders, and emerging challengers across premium, functional, and technology-enabled sub-segments. Key players in the global pet care market include Mars, Incorporated; Nestlé Purina PetCare; Hill's Pet Nutrition (Colgate-Palmolive); Royal Canin; Blue Buffalo (General Mills); Spectrum Brands Holdings; Zoetis, Inc.; Central Garden and Pet Company; Chewy, Inc.; Petco Animal Supplies; and PetSmart, Inc., among others profiled in the full Expert Market Research Pet Care Market Report.

The comprehensive EMR report provides an in-depth assessment of the market based on the Porter’s five forces model along with giving a SWOT analysis. The report gives a detailed analysis of the following key players in the global pet care market, covering their competitive landscape and the latest developments like mergers, acquisitions, investments, and expansion plans

Mars, Incorporated is among the largest global pet care companies, operating through its Mars Petcare division which encompasses brands including Pedigree, Whiskas, Royal Canin, Nutro, Greenies, IAMS, and Eukanuba. The company's pet care portfolio spans mainstream and premium dry and wet food, dental health treats, and veterinary-specific therapeutic nutrition products. Mars Petcare's Royal Canin division has established a globally recognised position in breed-specific and veterinarian-recommended nutrition across both canine and feline categories. Mars has additionally invested in companion animal digital health, having launched AI-powered tools for pet health assessment in May 2025. The company's geographic breadth, manufacturing scale, and veterinary channel relationships position it as the dominant force in organised global pet nutrition.

Nestlé Purina PetCare is one of the world's leading pet care businesses, operating a portfolio of globally recognised brands including Purina ONE, Purina Pro Plan, Fancy Feast, Friskies, Dog Chow, Cat Chow, Beneful, and Felix. Purina Pro Plan's strong veterinarian recommendation rates give the brand a defensible premium positioning across both retail and clinical channels. The company's March 2026 inauguration of a BRL 2.5 billion wet pet food manufacturing facility in Vargeão, Brazil demonstrates its strategic commitment to expanding production capacity in high-growth emerging markets. Nestlé Purina's innovation investment in functional nutrition, including probiotic-enhanced formulas and life-stage-specific products, aligns with the consumer trend toward nutritional premiumisation that is driving the pet food segment's superior margin expansion.

Hill's Pet Nutrition, a subsidiary of Colgate-Palmolive Company, specialises in science-backed therapeutic and health-promoting pet nutrition through its two primary product lines: Hill's Science Diet, sold through pet specialty retail channels, and Hill's Prescription Diet, sold exclusively through veterinary clinics and authorised online pharmacies. Hill's holds a strong and defensible position in the veterinary-recommended nutrition segment, with Prescription Diet products generating recurring purchase cycles driven by clinical recommendation for pets with specific health conditions including renal disease, urinary tract health, weight management, and food sensitivities. The veterinary channel relationship that Hill's has cultivated over decades is a significant competitive moat that new entrants to the therapeutic nutrition segment must overcome.

Blue Buffalo Company, Ltd. was founded in 2003 in Wilton, Connecticut and leads the premium all-natural pet nutrition sector. With robust advertising, marketing efforts, and a constant flow of new offerings, the company has achieved impressive growth. Distinguishing itself, Blue Buffalo is the sole pet food brand that advertises on television and employs a 1,500+ strong team of in-store product experts to educate pet owners. Their products are available through major national pet speciality chains and numerous neighbourhood stores across the U.S.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global pet care market was valued at USD 207.24 Billion in 2025, according to Expert Market Research. This figure encompasses total revenue across pet food and nutrition, veterinary and medical care, grooming and hygiene, accessories, pet insurance, boarding, training, and technology-enabled care products globally.

The global pet care market is projected to reach USD 367.65 Billion by 2035, according to Expert Market Research, growing at a CAGR of 5.90% over the forecast period 2026-2035.

Pet humanisation refers to the cultural and emotional phenomenon in which companion animals are accorded family member status, leading owners to apply human health, nutrition, and lifestyle standards to companion animal care. It is the foundational demand driver of the global pet care market, expanding both the scope of products and services purchased and the price points acceptable to pet owners across all income demographics.

Pet food and nutrition leads the global pet care market by revenue share, driven by the daily recurrent nature of companion animal feeding and the powerful premiumisation trend expanding per-unit revenue across dry, wet, raw, and functional nutrition categories.

North America leads the global pet care market as the largest regional market, with the United States pet industry reaching USD 158 billion in 2025 according to the American Pet Products Association. Asia Pacific is the fastest-growing regional market over the forecast period.

Pet food, veterinary care, and pet grooming are different offerings based on product type.

Key players in the global pet care market include Mars, Incorporated; Nestlé Purina PetCare; Hill's Pet Nutrition (Colgate-Palmolive); Royal Canin; Chewy, Inc.; Blue Buffalo (General Mills); Zoetis, Inc.; Spectrum Brands Holdings; Central Garden and Pet Company; Petco Animal Supplies; and PetSmart, Inc., among others detailed in the Expert Market Research Pet Care Market Report.

The global pet care market is projected to grow at a CAGR of 5.90% between 2026 and 2035, according to Expert Market Research, driven by pet humanisation, premiumisation of nutrition, veterinary service expansion, and rising pet ownership in emerging markets.

Growth in the North America veterinary care market is driven by rising per-pet healthcare investment, the consolidation of independent veterinary practices into multi-site groups, the emergence of integrated hybrid care platforms combining physical clinic and telehealth services, expanding pet insurance adoption supporting higher-cost care access, and consumer demand for specialist services and advanced diagnostics.

Key challenges include premium brand margin pressure from consumer trade-down behaviour in mid-income demographics, structural veterinary workforce shortages constraining service capacity, raw material price volatility affecting food manufacturer margins, and regulatory complexity governing functional ingredient use across different jurisdictions.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Pet Type |

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.