Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

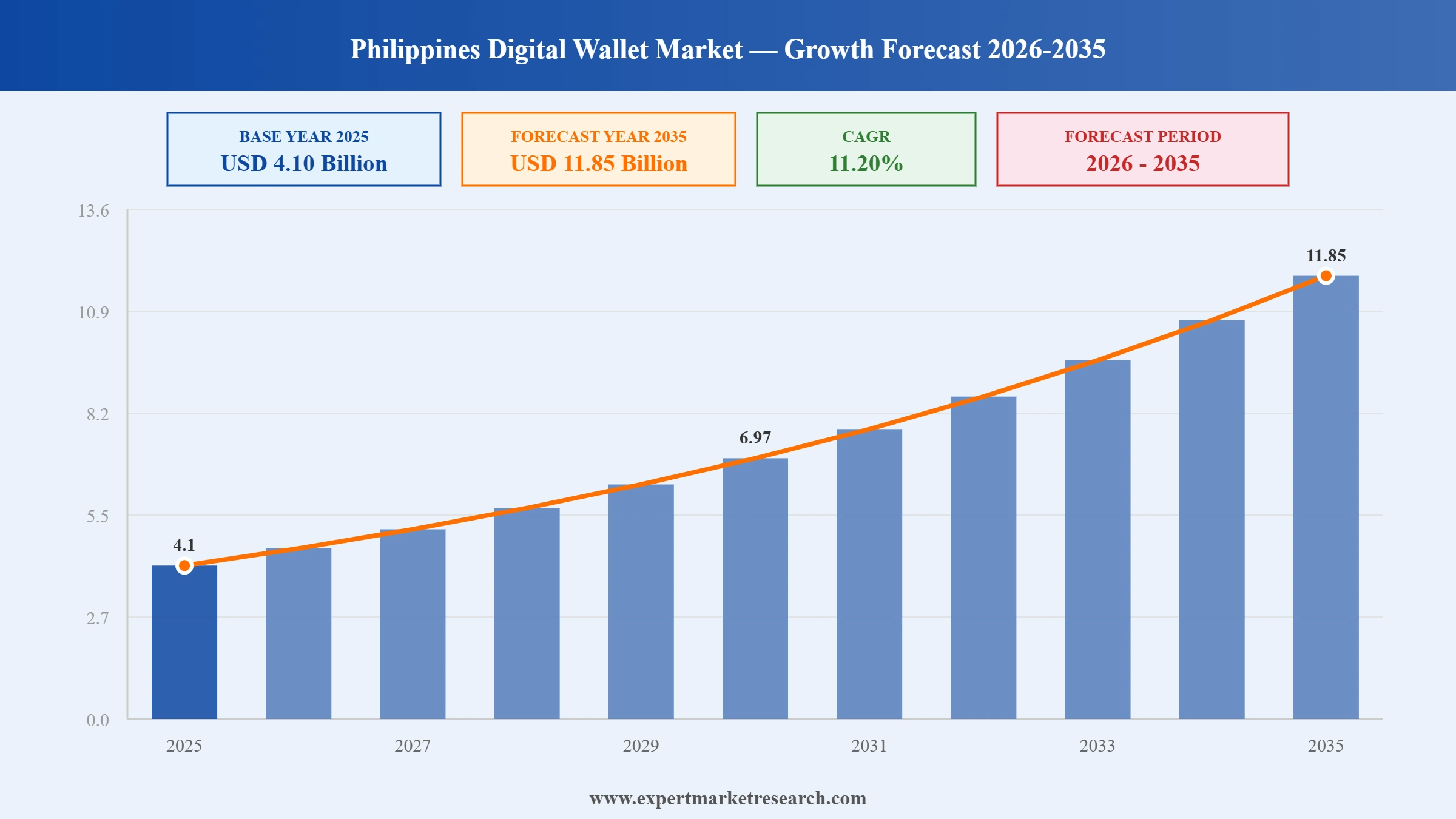

The Philippines Digital Wallet Market reached a value of USD 4.10 Billion at 2025 and is projected to expand at a CAGR of around 11.20% during the forecast period of 2026-2035. With rising smartphone and internet penetration, government-backed cashless payment initiatives under the National Retail Payment System, growing e-commerce adoption, and the pivotal role of digital wallets in channeling OFW remittances, the market is expected to reach USD 11.85 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Digital Wallet Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

4.10 |

|

Market Size 2035 |

USD Billion |

11.85 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

11.20% |

|

CAGR 2026-2035 - Market by Technology |

Remote |

11.5% |

|

CAGR 2026-2035 - Market by End Users |

Retail & E-commerce |

12.8% |

The Philippines Digital Wallet Market is shaped by OFW remittance digitization, government-backed financial inclusion, rapid QR code adoption, and the evolution of leading platforms into full-stack financial super-apps serving millions of previously unbanked Filipinos.

In February 2026, the Bangko Sentral ng Pilipinas introduced new regulatory requirements compelling digital banks and e-wallet providers to use standardized payment rails, specifically InstaPay and PESONet, for all qualifying digital transactions. The regulation is designed to improve interoperability across the Philippines' fragmented digital payment ecosystem, ensuring faster processing and more reliable fund transfers for users. The policy also strengthens consumer protection by requiring transparency in failed transaction handling and refund timelines. QR code-based payments, which already account for approximately 60% of digital transactions in the Philippines, are expected to benefit from the improved rail standardization as merchants and consumers experience more consistent payment experiences.

In November 2025, Google Wallet officially launched in the Philippines, enabling Android smartphone users to make tap-to-pay contactless transactions at compatible NFC-enabled merchants. The initial rollout supported nine Philippine financial institutions and digital wallet providers, including GCash, Maya, GoTyme Bank, RCBC, China Bank, and EastWest Bank. The launch marked a significant shift in the Philippines' proximity payment landscape, bringing tokenized in-device payments to millions of Android users for the first time. BSP confirmed that both Google Pay and Apple Pay can operate in the country without requiring additional registration, clearing a key regulatory hurdle and opening the path for broader contactless payment adoption across the Philippines.

In February 2025, MatchMove partnered with LuLu Financial Services, the Asian United Bank (AUB), and Mastercard to introduce the Lulu Money Prepaid Mastercard in the Philippines, a financial product specifically designed for Overseas Filipino Workers. The card offers secure, flexible digital wallet functionality for both domestic and international transactions, enabling OFWs and their families to manage remittance inflows, daily spending, and cross-border payments through a single platform. The product addresses a critical pain point for the millions of Filipino households that rely on OFW remittances as a primary income source, channeling those inflows into a trackable, interest-earning digital financial ecosystem.

In January 2025, fintech company D-Wallet Technologies Corp. introduced DTaka, a blockchain-powered e-wallet designed specifically for Overseas Filipino Workers and their families in the Philippines. The platform offers faster and lower-cost remittances through stablecoin-based transfer mechanisms, providing an efficient alternative to traditional SWIFT-based wire transfers. DTaka launched with an initial target of reaching 500,000 users and announced plans to expand its platform to include merchant wallets, consumer loans, and blockchain-based rewards programs. The product reflects a broader trend of blockchain infrastructure being applied to the Philippines' significant remittance corridor to reduce friction and costs for OFW families.

In January 2024, Higlobe and Triple-A formed a strategic partnership to provide Filipino remote workers with instant, fee-free USD payment transfers from the United States, using stablecoin-based infrastructure as the underlying transfer mechanism. The collaboration offers a cost-effective alternative to traditional SWIFT-based remittance services, which typically involve processing delays and multiple fee layers. By combining Higlobe's US-side payment origination capabilities with Triple-A's crypto payment infrastructure, the partnership creates a streamlined corridor for the large and growing segment of Filipino professionals working remotely for US-based companies who require reliable, low-cost USD payment solutions.

The Philippines is undergoing a meaningful shift from QR-dominated payments toward a more layered ecosystem that now includes NFC-based tap-to-pay transactions, following the launch of Google Wallet in November 2025. This development adds a new proximity payment dimension to a market that had primarily grown through remote QR transactions. Google Wallet's entry, backed by nine Philippine financial partners including GCash and Maya, signals growing institutional readiness for the next phase of digital wallet evolution in the country. QR payments already account for approximately 60% of all digital transactions in the Philippines as of 2026, and the addition of NFC tap-to-pay through Google Wallet is broadening the use case further, particularly at formal retail merchants in Metro Manila. This convergence is a central factor supporting Philippines digital wallet market growth over the forecast period.

Overseas Filipino Workers represent one of the most powerful structural demand drivers for digital wallets in the Philippines. With OFW remittances accounting for approximately 8.5 to 9.4% of the country's GDP and total inflows expected to exceed USD 36 billion, efficient digital channels for receiving, managing, and spending these funds are essential for millions of Filipino households. Digital wallets offer speed, lower costs, and broader access compared to traditional cash pickup agents. In February 2025, MatchMove launched the Lulu Money Prepaid Mastercard in partnership with AUB and Mastercard, specifically designed for OFW families managing inbound remittances. Products like DTaka, launched in January 2025, further illustrate how blockchain-based wallets are being built explicitly for this remittance corridor.

The Philippines' digital wallet market is being defined by GCash and Maya, which have evolved well beyond basic payment functionality into comprehensive financial super-apps. GCash, which accounted for approximately 89% of the mobile wallet application market share in 2023, now offers savings, investments, insurance, and buy-now-pay-later credit products alongside its core payment services. Maya, formerly PayMaya, functions as both a digital wallet and a licensed digital bank, offering savings accounts with interest rates of up to 6% per annum, cryptocurrency trading, and SME-focused merchant payment solutions. In January 2025, Maya introduced BeetzePlay, a streaming service available exclusively within its app, extending the super-app model into content and entertainment to deepen user engagement within its financial ecosystem.

The Bangko Sentral ng Pilipinas has been actively shaping the Philippines' digital wallet landscape through progressive regulations designed to improve interoperability, consumer protection, and fraud management. BSP Circular 1215 of June 2025 established standardized processes for handling disputed transactions and coordinated verification, raising the operational baseline for all wallet providers and their banking partners. In February 2026, BSP introduced requirements mandating the use of standardized payment rails (InstaPay and PESONet) for digital banks and e-wallet providers, directly improving transfer reliability and reducing failed transaction rates. These regulatory steps are building the institutional trust infrastructure that encourages broader consumer and merchant adoption of digital wallets across all income segments and geographies in the Philippines.

The Expert Market Research's report titled "Philippines Digital Wallet Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

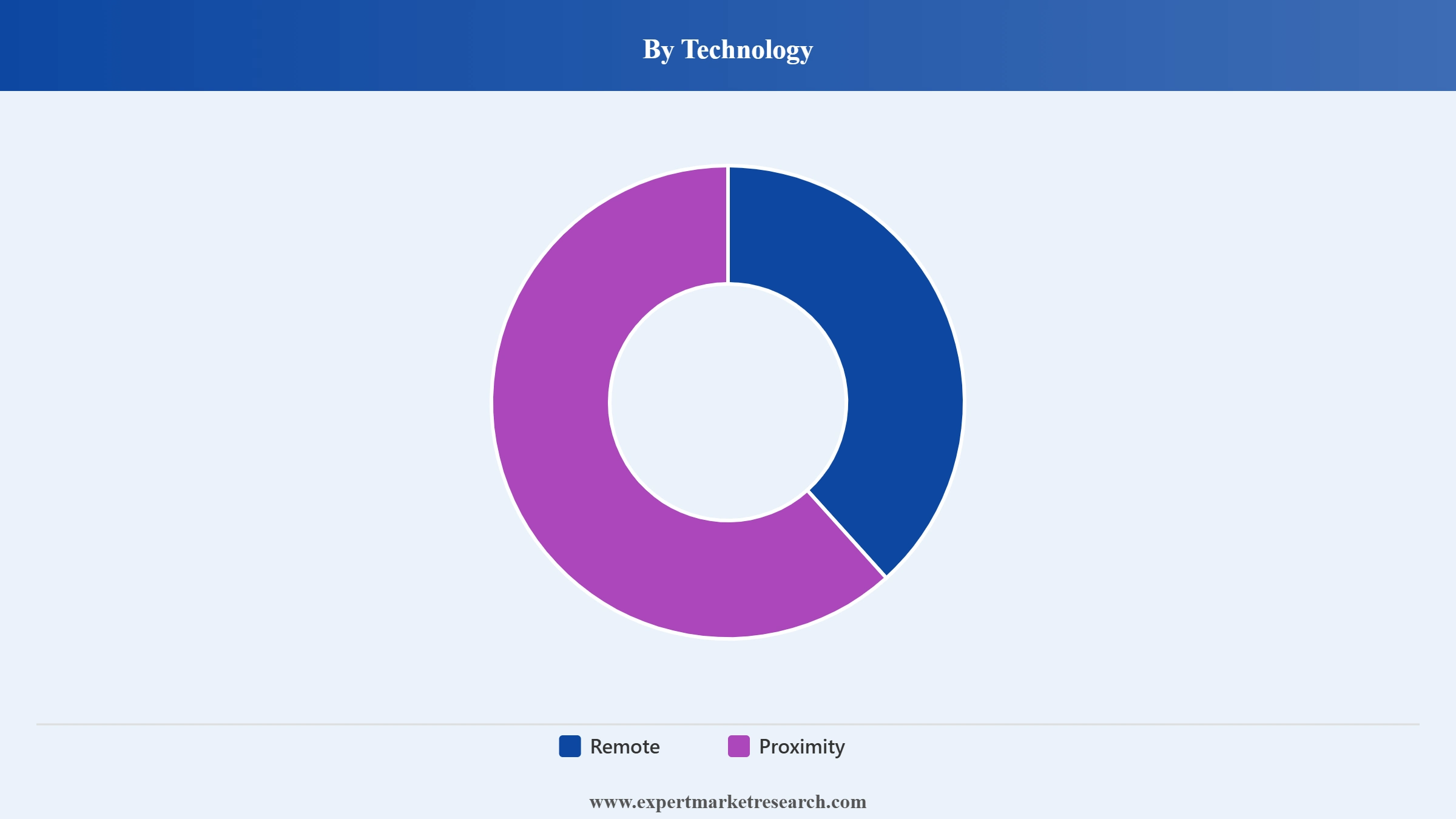

Market Breakup by Technology

Key Insight: Remote payments dominate the Philippines Digital Wallet Market, reflecting the country's payment behavior, which has been shaped by widespread adoption of QR code-based transactions through GCash and Maya. Remote digital wallet usage spans person-to-person fund transfers, OFW remittance receipt, bill payments, and e-commerce checkout flows, all of which are conducted without physical proximity to a merchant terminal. QR code payments alone account for approximately 60% of all digital transactions in the Philippines as of early 2026. Proximity payments, while the smaller segment, are gaining momentum following the November 2025 launch of Google Wallet, which introduced NFC-based tap-to-pay capabilities to millions of Android users. The growth of contactless infrastructure at formal retail outlets, particularly in Metro Manila, is expected to drive above-average CAGR for proximity payments over the forecast period.

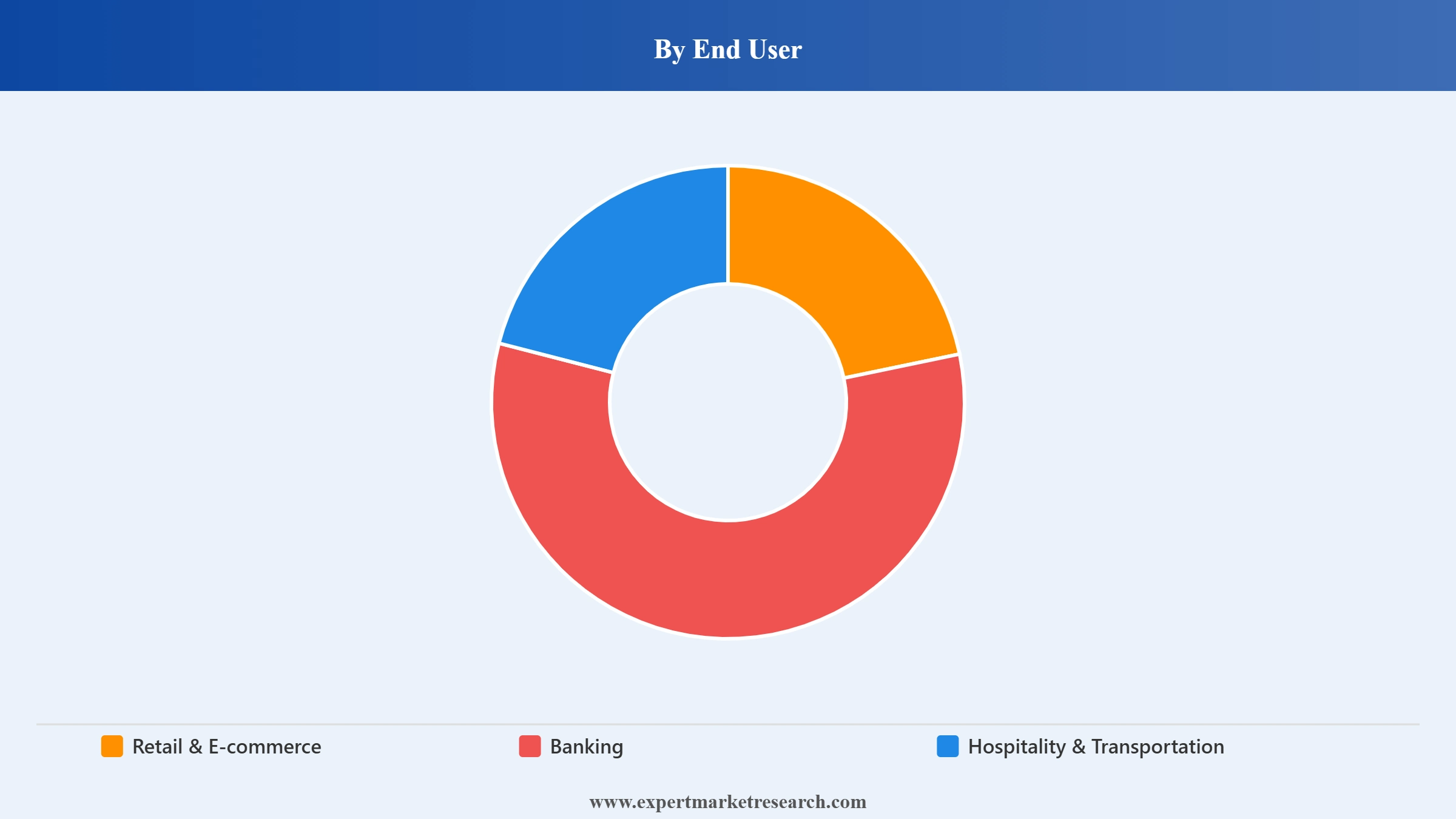

Market Breakup by End User

Key Insight: Retail and E-commerce is the dominant end-user segment in the Philippines Digital Wallet Market, supported by the country's rapidly growing e-commerce sector, which reached USD 17 billion in 2021 and was projected to reach USD 24 billion by 2025 according to the International Trade Administration. Digital wallets are deeply embedded in e-commerce checkout flows on leading platforms, and QR code payment acceptance at sari-sari stores, wet markets, and SME merchants creates a broad everyday retail use case. Banking represents a complementary segment, with GCash and Maya's partnerships with licensed digital banks enabling seamless account management and higher-value transactions within the wallet ecosystem. Hospitality and Transportation is a fast-growing segment as ride-hailing apps, airlines, hotels, and the growing tourism infrastructure in the Philippines increasingly adopt digital wallet payment acceptance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Technology

Remote payments command the dominant share of the Philippines Digital Wallet Market, driven by the country's QR code-first payment culture and the leading role of GCash and Maya in facilitating remote digital transactions. With QR payments accounting for approximately 60% of all digital transactions nationally, remote wallet usage is deeply embedded in everyday Filipino financial behavior, spanning OFW remittance receipt, utility bill payments, e-commerce purchases, and peer-to-peer transfers. In 2023, GCash alone accounted for approximately 89% of mobile wallet application market share, underscoring how concentrated and remote-transaction-driven the Philippines market is. Proximity payments are growing from a small base, with the November 2025 Google Wallet launch marking the beginning of a structural shift toward NFC-enabled tap-to-pay behavior, particularly among Metro Manila's urban consumer base.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End User

Retail and E-commerce holds the dominant position among end-user segments in the Philippines Digital Wallet Market. The segment's strength is rooted in the Philippines' rapidly expanding online commerce sector and the deep integration of GCash and Maya into e-commerce platform checkout flows on sites like Lazada and Shopee. QR code acceptance at physical retail merchants, including sari-sari stores and informal market vendors, creates an additional mass-market retail wallet use case that extends well beyond formal e-commerce. The Banking segment supports digital wallet usage through deposit, savings, and credit product integrations, with GCash Padala and Maya Center agent networks extending last-mile financial access. Hospitality and Transportation is an emerging growth segment as ride-hailing platforms like Grab, airline booking sites, and hotel chains ramp up digital wallet acceptance across the Philippines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Metro Manila and the surrounding National Capital Region represent the largest and most developed digital wallet market within the Philippines, anchored by the concentration of fintech companies, licensed digital banks, and formal retail infrastructure that requires consistent digital payment acceptance. GCash's parent company Mynt, Maya, GrabPay, and Coins.ph all operate from Manila, and the BSP's regulatory presence creates a policy environment that actively encourages digital payment innovation. The density of smartphone users, internet connectivity, and tech-savvy younger consumers in Metro Manila creates a receptive market for new digital wallet features, including the November 2025 launch of Google Wallet's tap-to-pay functionality with nine local financial partners. The region contributes the largest share of total digital wallet transaction volume in the Philippines, and its fintech ecosystem sets the product and regulatory benchmarks that other regions follow.

The Visayas and Mindanao regions, while currently contributing a smaller share of digital wallet transaction volume, represent the Philippines market's most important long-term growth opportunity. These regions contain millions of underbanked Filipinos who rely on OFW remittances as a primary income source, making them a natural target for digital wallet providers seeking to capture inbound remittance flows into managed digital accounts. GCash's agent network and Maya Center's 55,000 partner touchpoints are already active in these regions, providing last-mile access to digital financial services in areas where traditional bank branches are scarce. Improving mobile data coverage through DICT and NTC-led connectivity projects is gradually raising smartphone internet access rates across the Visayas and Mindanao island groups, which is expected to drive meaningful new user growth for digital wallet providers over the forecast period.

The Philippines Digital Wallet Market is characterized by a dominant domestic duopoly at the consumer-facing layer, with GCash and Maya commanding the vast majority of active users and transaction volume. Global technology companies and international payment networks participate primarily as infrastructure partners, providing card network rails, cloud services, and tokenization capabilities that support the domestic super-app platforms. Regulatory oversight from BSP defines the competitive operating environment, with interoperability mandates and anti-fraud regulations shaping how players compete on service reliability and consumer trust.

International players such as Amazon Web Services, Visa, Mastercard, American Express, Alipay, and PayPal contribute to the Philippines' digital wallet ecosystem primarily through infrastructure, merchant solutions, and cross-border payment channels. These global participants do not directly compete at the retail e-wallet level with GCash and Maya but serve critical roles as payment network partners, cloud providers, and cross-border settlement infrastructure. The recent entry of Google Wallet and the anticipated arrival of Apple Pay in 2026 are adding new competitive dimensions at the proximity payment layer, where international platforms will compete more directly with domestic wallets for NFC-enabled transaction share.

Founded in 2006 and headquartered in Seattle, USA, Amazon Web Services provides cloud computing and digital financial services globally. In the Philippines, AWS serves as a critical backend infrastructure provider for fintech platforms, digital banks, and e-wallet operators. Amazon Pay, embedded within the Amazon e-commerce ecosystem, offers Filipino consumers a digital wallet option for international online purchases. AWS's cloud infrastructure supports payment processing systems for numerous Philippine financial institutions, enabling the scalable real-time transaction processing that modern digital wallets require. The company's e-commerce integration advantage positions Amazon Pay as a preferred option for Filipinos engaged in cross-border online shopping.

Founded in 1958 and headquartered in San Francisco, USA, Visa is a global payment network that plays a foundational role in the Philippines' digital wallet infrastructure. Visa's tokenization and card-on-file services enable Philippine digital wallets to offer Visa-linked card credentials for both online and contactless in-person payments. The November 2025 Google Wallet launch in the Philippines included Visa credit and debit cards among its supported payment methods, reflecting Visa's deep integration with the country's digital payment infrastructure. Visa also partners with Philippine banks and fintech companies to support QR code merchant acceptance and contactless payment expansion across urban and semi-urban areas.

Founded in 1850 and headquartered in New York, USA, American Express is a globally recognized financial services and payments company. In the Philippines, American Express operates primarily in the premium consumer and corporate travel segments, offering credit card products and travel benefits through local banking partnerships. Its digital wallet and contactless payment capabilities are available through select Philippine bank partners that issue American Express-branded products. American Express caters to higher-income urban professionals, corporate clients, and international travelers, making it a relevant participant in the premium segment of the Philippines' growing digital payment ecosystem, particularly in hospitality and transportation use cases.

Founded in 1998 and headquartered in San Jose, USA, PayPal is a leading global digital payments company with significant relevance in the Philippines. In the Philippines, PayPal primarily serves the large community of Filipino freelancers, remote workers, and digital content creators who earn income from international clients and platforms. It provides a reliable, internationally recognized digital wallet for receiving USD and other foreign currency payments and converting them for local use. PayPal's strength in cross-border payment processing, buyer protection features, and integration with major international e-commerce and freelancing platforms makes it an important channel for the Philippines' significant remote work and outsourcing economy.

Other key players in the market are Apple Inc., Google Inc., Airtel, Mastercard, Alipay, Samsung, AT&T, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Philippines Digital Wallet Market 2026 with our comprehensive report. Stay ahead with verified data on technology adoption trends, OFW remittance-driven growth, BSP regulatory developments, and the segments recording the fastest transaction growth. Whether you are a fintech company entering the Philippine market, a global payment network evaluating local partnership opportunities, or an investor assessing the country's digital finance potential, this report provides the strategic clarity you need. Download your free sample today and explore the key opportunities within the Philippines' rapidly growing digital wallet sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Philippines digital wallet market reached an approximate value of USD 4.10 Billion.

The Philippines digital wallet market is assessed to grow at a CAGR of 11.20% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 11.85 Billion by 2035.

The various technologies in the market include remote and proximity.

The key players in the market are Amazon Web Services, Inc., Visa Inc., American Express, PayPal Holdings Inc., Apple Inc., Google Inc., Airtel, Mastercard, Alipay, Samsung, and AT&T, among others.

The various end users in the market include retail & e-commerce, banking, and hospitality & transportation.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.