Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

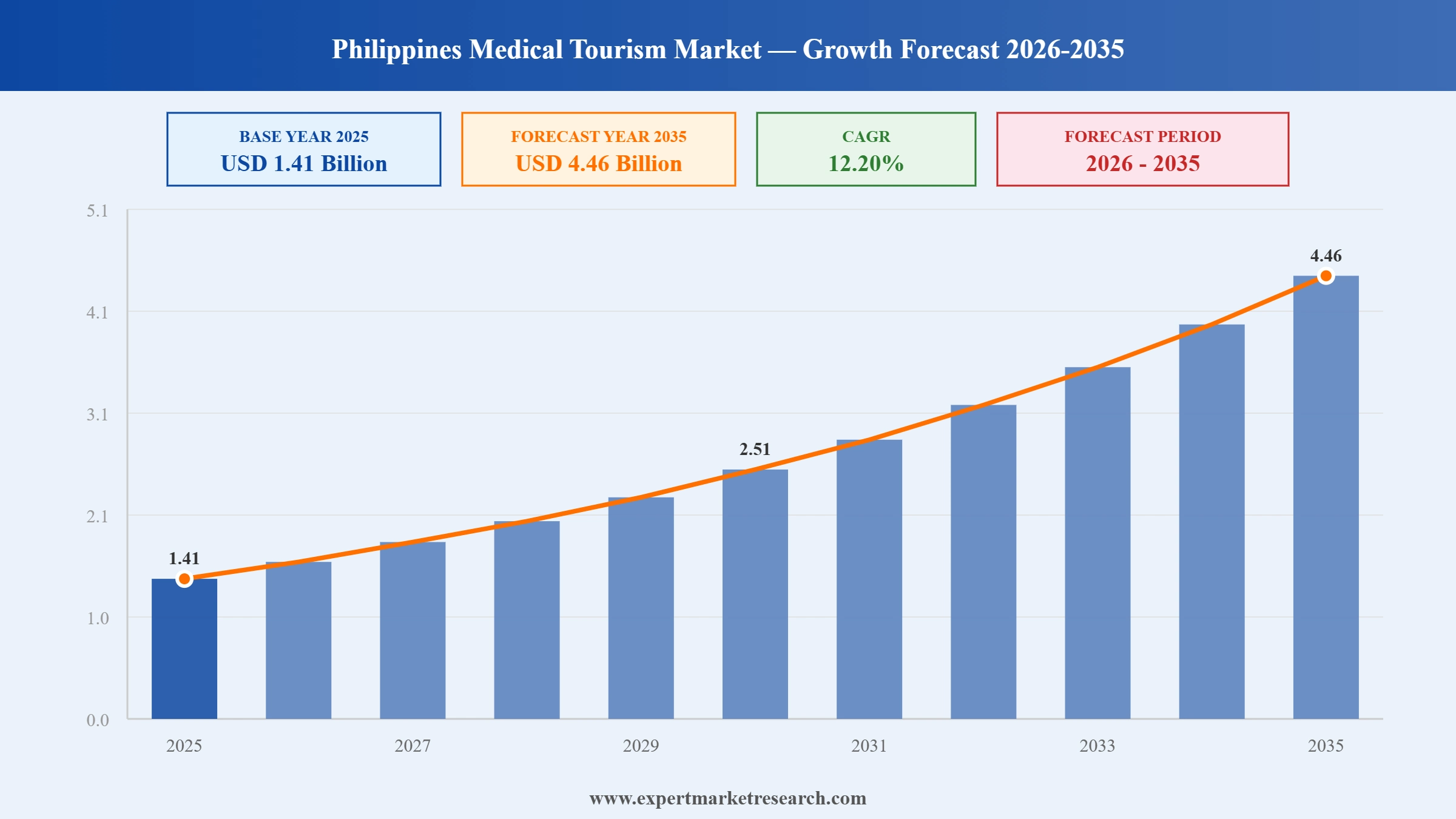

The Philippines Medical Tourism Market reached a value of USD 1.41 Billion at 2025 and is projected to expand at a CAGR of around 12.20% during the forecast period of 2026-2035. With growing inbound demand for affordable cosmetic and medical procedures, expanding JCI-accredited hospital infrastructure, increasing government-backed medical tourism promotion through the Filipino Brand of Wellness initiative, and rising foreign direct investment in healthcare facilities, the market is expected to reach USD 4.46 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Philippines medical tourism market is being shaped by a convergence of factors: rising global healthcare costs that push patients toward affordable alternatives, government-led initiatives packaging the country’s natural and cultural appeal alongside medical services, the rapid adoption of advanced surgical technologies, and growing foreign investment in healthcare infrastructure. The country’s bilingual, internationally trained workforce and growing base of JCI-accredited hospitals remain central to its competitive positioning.

Asian Hospital and Medical Center formalized a partnership with Shinagawa Healthcare Solutions Corporation under its Hospital Engagement and Alliance Linkage (HEAL) program, designed to facilitate knowledge exchange, enhance service delivery standards, and create cross-referral pathways between the two institutions. Shinagawa Healthcare Solutions brings expertise in diagnostics, eye care, and preventive health screening, areas that align well with the high-value outpatient and wellness segments of the Philippines’ medical tourism market. The partnership reinforces a broader trend of Philippine private hospitals building bilateral alliances with regional and global healthcare providers to strengthen clinical capabilities and expand their international patient base.

The Medical City announced a major expansion initiative targeting provinces outside Metro Manila, with plans to open at least 28 additional clinics over the following two years. The strategy prioritises provinces with populations of at least two million, enabling The Medical City to tap into previously underserved regional markets while simultaneously creating additional capacity for domestic and international patient services. This expansion extends TMC’s nationally recognised brand of JCI-accredited, tertiary-level care beyond its Pasig City flagship and existing provincial hospitals in Clark, Iloilo, Laguna, and Pangasinan, addressing both domestic healthcare access gaps and rising demand from medical tourists arriving from the Pacific Islands, the United States, and Australia.

Metro Pacific Health (MPH) completed the acquisition of a controlling stake in Diliman Doctors Hospital Inc. (DDHI), a 165-bed hospital in Quezon City serving established residential communities including Ayala Heights, Loyola Grand Villas, and Capitol Hills. The acquisition expanded MPH’s inpatient network capacity to over 4,300 beds across its Philippines hospital system. This move is consistent with MPH’s strategy of strengthening its Metro Manila footprint and building capacity for international patient services. The following month, in November 2024, MPH further acquired the City of General Trias Doctors Medical Center Inc. in Cavite, marking its 27th hospital and 16th provincial partnership.

The Department of Tourism of the Philippines officially designated St. Luke’s Medical Center (SLMC) as the country’s lead medical tourism facility, reinforcing the institution’s central role in the Philippines’ broader health tourism strategy. Alongside this recognition, SLMC announced a P18 billion investment to build a new 450-bed hospital in Aseana City, Paranaque, expected to be operational by 2029. The new facility will serve as a third flagship location, complementing existing hospitals in Quezon City and Bonifacio Global City. Tourism Secretary Christina Frasco noted that SLMC accounted for 40 to 50 percent of overall medical tourism receipts in 2023, underscoring its outsized importance to the sector.

St. Luke’s Medical Center introduced the da Vinci Xi robotic surgical system at its Quezon City facility, significantly advancing the hospital’s minimally invasive surgery capabilities. The da Vinci Xi platform allows surgeons to perform complex procedures with enhanced precision, reduced patient recovery times, and smaller incisions compared to conventional open surgery. This adoption places St. Luke’s among a select group of hospitals in Southeast Asia offering robotic-assisted surgery at scale, further strengthening its appeal to international patients seeking high-complexity procedures like cardiovascular, urological, and oncological surgeries at internationally competitive price points.

One of the defining shifts in Philippines medical tourism market growth has been the deliberate repositioning of the country as a destination that combines clinical care with wellness and travel experiences. The Department of Tourism has moved beyond simply marketing hospital services and now packages medical procedures with the country’s scenic recovery environments, hospitality culture, and indigenous healing traditions. This integrated approach targets patients who want to combine elective or corrective procedures with meaningful travel recovery experiences. In May 2024, the DOT launched the Filipino Brand of Wellness module at the national level, equipping tourism stakeholders and local communities with tools to deliver world-class wellness experiences alongside clinical care.

The Philippine House of Representatives’ approval of the eHealth System and Services Act in 2024 marked a pivotal moment for the country’s ability to serve international patients beyond physical borders. The legislation enables telemedicine and teleconsultation services to be accessed by patients from abroad, allowing Filipino medical professionals to conduct pre-visit assessments, post-procedure follow-ups, and remote health monitoring for medical tourists who have returned to their home countries. This digital health framework significantly enhances the end-to-end patient experience, reduces barriers for first-time patients considering the Philippines, and opens new service revenue streams for hospitals equipped with digital health infrastructure.

Growing confidence among foreign institutional investors in the Philippines’ healthcare market is emerging as a significant structural driver. Foreign companies are investing directly in advanced clinical capabilities, reproductive health services, and diagnostic infrastructure that strengthen the country’s competitiveness as a medical tourism destination. These investments elevate service quality, introduce international clinical standards, and expand the range of specialised treatments available to both domestic and international patients. In September 2024, Japan’s Marubeni Corporation confirmed investment in Conceive IVF Manila Inc., a reproductive health and fertility services provider in the Philippines, reflecting growing international investor appetite for specialised clinical services that attract cross-border patients.

Philippine hospitals are aggressively adopting cutting-edge surgical and diagnostic technologies to close the quality perception gap with leading medical tourism destinations like Thailand and Singapore. Robotic surgery systems, advanced imaging platforms, AI-assisted diagnostics, and minimally invasive procedure suites are becoming standard investment priorities for major private hospital chains. This technology upgrade strategy is designed to attract high-value patients who require complex interventional procedures and are willing to travel for quality care at a significant cost saving compared to the United States, Canada, or Australia. In May 2024, St. Luke’s Medical Center introduced the da Vinci Xi robotic surgical system at its Quezon City facility, making it one of the most technically advanced hospitals in Southeast Asia for complex robotic-assisted procedures.

The report of the Expert Market Research report titled “Philippines Medical Tourism Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Treatment Type

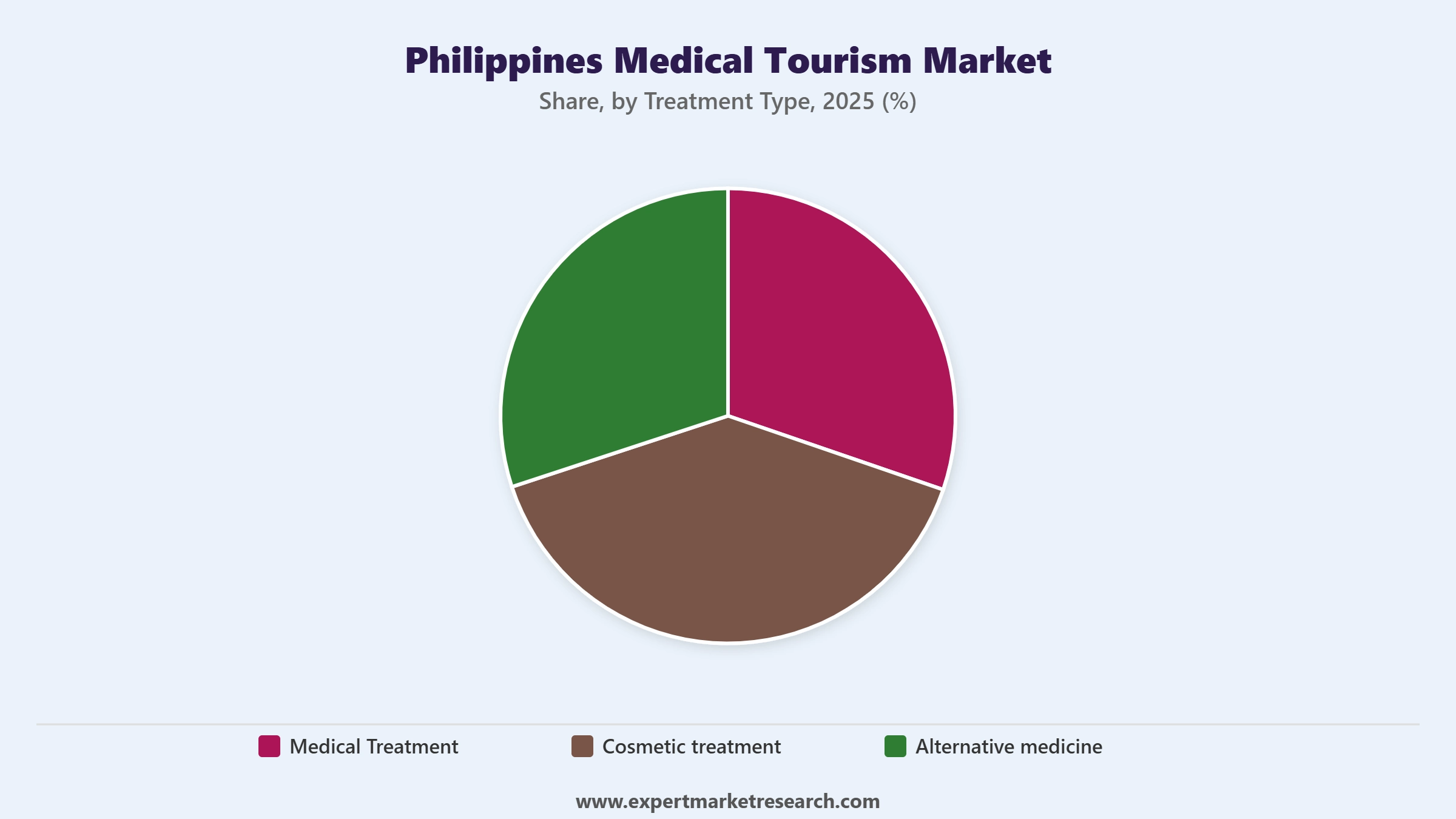

Key Insight: The Treatment Type segmentation reflects the breadth of services driving medical tourism inflows to the Philippines. Medical Treatment remains a cornerstone of the market, with cardiovascular procedures, oncological treatments, and orthopedic surgeries attracting patients from the Pacific Islands, North America, and other Asian countries seeking internationally accredited care at 50 to 80 percent lower costs than at home. Dental procedures represent a high-frequency, repeat-visit category, particularly popular among overseas Filipinos and American retirees. Cosmetic Treatment is the fastest-growing and now the largest single category by market share, with cosmetic procedures and rejuvenation treatments drawing patients seeking facelifts, liposuction, breast augmentation, and skin rejuvenation at competitive prices relative to Western providers. Alternative Medicine, while a smaller segment, is gaining traction as the country’s indigenous healing traditions are packaged within wellness tourism frameworks.

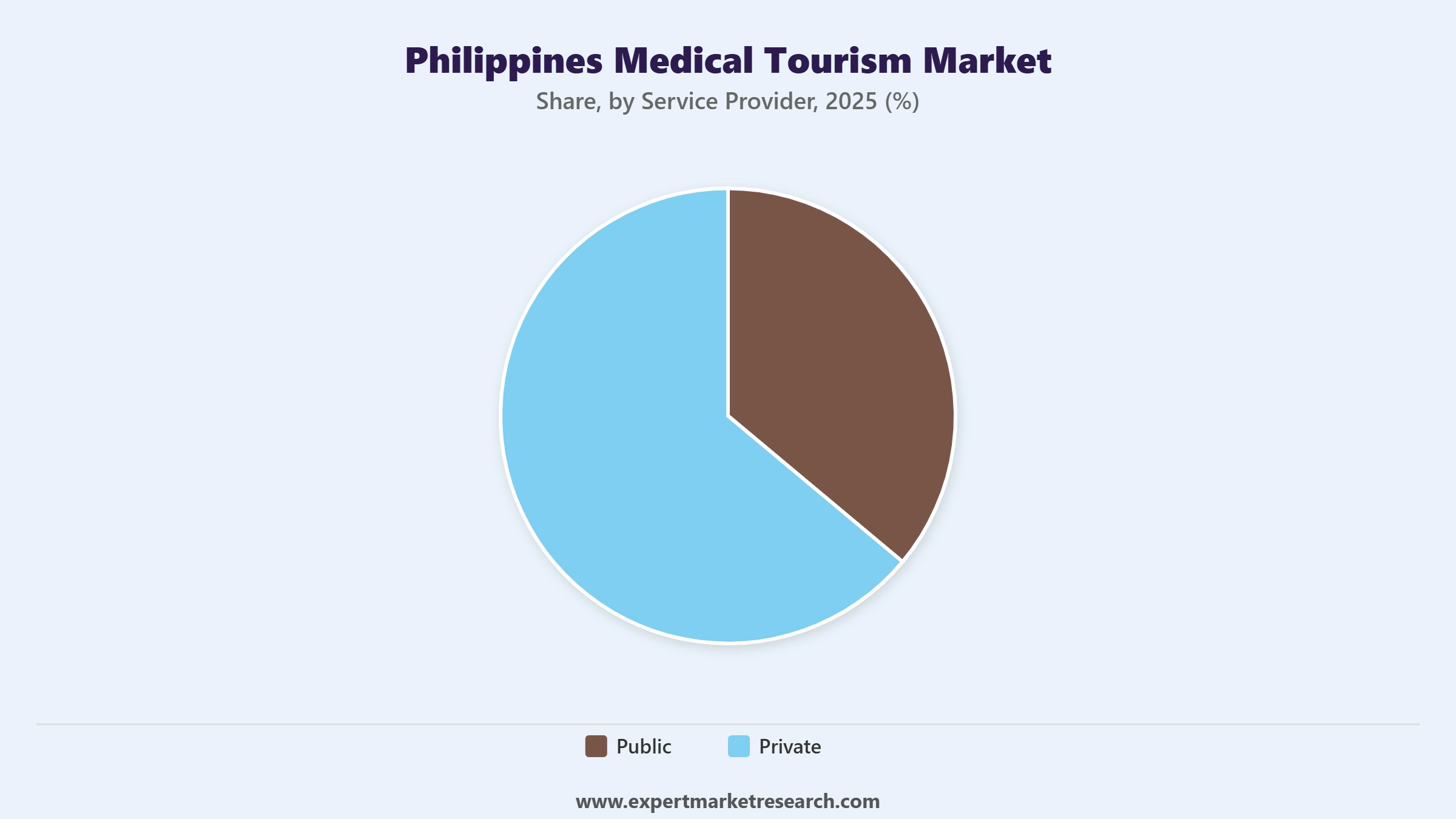

Market Breakup by Service Provider

Key Insight: The private healthcare sector dominates the Philippines medical tourism market, commanding approximately 65% of total revenue from the medical tourism segment in 2025. JCI-accredited private hospitals including St. Luke’s Medical Center, The Medical City, Asian Hospital, and Makati Medical Center are the primary facilities servicing international patients, offering 24/7 concierge services, dedicated international patient lounges, and language interpretation support. The public healthcare sector, while substantially larger in terms of total patient volume nationally, plays a limited role in formal medical tourism given infrastructure constraints and capacity pressures from domestic demand. Ongoing government investment in public health facility upgrades and the DOT’s accreditation programs are gradually creating pathways for public hospitals to participate in attracting lower-budget international patients, particularly from nearby Southeast Asian countries.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Treatment Type: Cosmetic Treatment has emerged as the dominant sub-segment within the Philippines medical tourism market, accounting for approximately 35% of total market revenue in 2025. This reflects the global surge in demand for accessible, high-quality aesthetic procedures from patients in North America, Australia, and the Middle East, who find Philippine costs 50 to 70% lower than in their home markets. Facelifts, rhinoplasty, liposuction, and breast augmentation are among the most sought-after procedures. Medical Treatment follows as the second-largest sub-segment, supported by patients seeking cardiovascular, oncological, and orthopedic procedures at internationally accredited private hospitals. Alternative Medicine, while a growing niche, remains a smaller share contributor, primarily attracting wellness tourists interested in holistic healing experiences combined with leisure travel.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Service Provider: Private service providers account for the dominant share of the Philippines medical tourism market, holding approximately 65% of sector revenue in 2025. This reflects the concentration of internationally accredited, high-quality care within private hospital networks rather than the public healthcare system. Private hospitals have made deliberate investments in patient experience infrastructure specifically for international visitors, including dedicated international patient departments, concierge services, and multilingual support. Public sector providers, while growing in relevance through DOT accreditation programs, currently serve a smaller share of formal medical tourism due to capacity constraints from domestic patient volumes and infrastructure gaps relative to private institutions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

CALABARZON is the fastest-growing regional market for medical tourism in the Philippines, driven by the region’s expanding private hospital capacity and its dual advantage of proximity to Metro Manila and access to more relaxed, suburban recovery environments. Cities like Calamba in Laguna, which now hosts branches of Manila-based hospital networks, and Lipa in Batangas, are becoming secondary referral and recovery destinations for international patients arriving through Manila. The region’s growing middle-class population base supports the development of outpatient specialty clinics for cosmetic procedures, dental services, and fertility treatments that also attract overseas Filipino clients and nearby international visitors. Investment in provincial hospital infrastructure by major groups, including The Medical City’s planned expansion into provinces with over two million populations, is expected to cement CALABARZON’s emergence as the country’s second-most significant medical tourism zone by 2034.

The Philippines medical tourism market features a mix of hospital operators, medical tourism facilitators, and international patient management companies. The competitive landscape is divided between large private hospital systems that are the direct providers of medical services and intermediary companies that channel international patients toward these facilities. Private hospital networks including The Medical City, St. Luke’s Medical Center, and Asian Hospital compete on JCI accreditation status, clinical specialisation, technology investment, patient experience quality, and pricing for international all-inclusive packages.

On the facilitator side, companies like MedicalTourism.com and Al Afiya Medi Tour serve as the critical interface between patients in source markets and Philippine hospitals, offering consultation, logistics, travel coordination, and post-care support. This intermediary layer is growing in sophistication as international patients demand end-to-end managed services rather than self-arranged hospital visits. The market is still relatively fragmented compared to medical tourism leaders like Thailand, giving significant room for consolidation and premium service development over the forecast period.

Health and Leisure is a medical tourism company operating in the Philippines, facilitating international patient access to a range of medical and wellness services offered by accredited hospitals and clinics across the country. The company focuses on bridging the gap between overseas patients, particularly from the Pacific Islands and Southeast Asian markets, and Philippine healthcare providers. It assists with travel arrangements, hospital liaison, accommodation, and post-procedure recovery coordination, making it a one-stop partner for patients seeking comprehensive medical tourism support within the Philippines.

MedicalTourism.com is a US-based global medical tourism platform that connects patients from around the world with accredited healthcare providers in destinations including the Philippines. The platform serves as a marketplace and resource hub, providing information on hospital accreditations, procedure costs, treatment options, and patient testimonials to support informed healthcare travel decisions. For the Philippine market, MedicalTourism.com helps channel patients from North America, Europe, and the Middle East toward JCI-accredited Philippine hospitals seeking cardiovascular, orthopedic, cosmetic, and dental treatment. The platform’s global reach makes it a key facilitator of international patient flows into the Philippines.

Al Afiya Medi Tour is a medical tourism facilitator that channels patients from the Middle East and Gulf Cooperation Council countries toward international healthcare destinations, including accredited hospitals in the Philippines. The company provides end-to-end medical tourism management services including pre-travel consultations, visa facilitation, hospital liaison, translation support, and post-treatment follow-up coordination. As Gulf-based demand for affordable surgical and cosmetic procedures at internationally certified facilities grows, Al Afiya Medi Tour plays an important role in routing that demand toward the Philippines, particularly given the country’s competitive pricing for procedures like cardiovascular surgery, orthopaedic treatment, and cosmetic interventions.

The Medical City (TMC) was founded in 1967 and is headquartered in Pasig City, Metro Manila, Philippines. TMC is one of the Philippines’ foremost private tertiary care hospital networks, operating a 115,000-square-meter flagship complex in Pasig alongside provincial hospitals in Clark, Iloilo, Laguna, and Pangasinan, and an international facility in Guam. TMC holds JCI accreditation and is certified for acute myocardial infarction care, making it one of only four JCI-accredited hospitals in the Philippines. The hospital serves over 40,000 inpatients and 400,000 outpatients annually. Its centres of excellence span cardiovascular care, oncology, regenerative medicine, wellness and aesthetics, and neurosciences, making it a leading destination for complex medical procedures among both domestic patients and international visitors.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Interested in understanding where the Philippines medical tourism market is heading between 2026 to 2035? Our comprehensive report covers affordable healthcare trends, treatment type growth trajectories, competitive hospital dynamics, and regional opportunity maps across Metro Manila, CALABARZON, and beyond. Whether you are a hospital operator, a medical tourism facilitator, or an investor evaluating the Philippine healthcare space, this report gives you the clarity and depth you need. Download your free sample now and discover the key opportunities in the growing Philippines medical tourism space.

Upto 15% Off

USD

$3099 $2789

$1999 $1799

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 1.41 Billion.

The market is projected to grow at a CAGR of 12.20% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 4.46 Billion by 2035.

The Philippines medical tourism market is driven by several complementary forces. Healthcare costs in developed nations, particularly the United States, Canada, and Australia, are forcing patients to seek affordable, high-quality alternatives abroad, where procedures in the Philippines can cost 50 to 80% less. The country’s English-speaking, internationally trained medical workforce lowers language and communication barriers for foreign patients. Rising JCI accreditation among private hospitals builds international patient confidence in clinical quality standards. Growing government support through the Department of Tourism’s Filipino Brand of Wellness and the Health Tourism Industry Blueprint is systematically elevating the country’s profile. Foreign investment in healthcare infrastructure and the adoption of advanced surgical technologies like robotic surgery systems further strengthen the value proposition. Additionally, the eHealth System and Services Act of 2024 enables telemedicine to serve international patients before and after their visits.

The Philippines medical tourism market is segmented by treatment type into Medical Treatment (covering Cardiovascular Procedures, Oncological Procedures, Orthopedic and Spine Procedures, Dental Procedures, and Others), Cosmetic Treatment (covering Cosmetic Procedures, Rejuvenation Procedures, and Others), and Alternative Medicine. Cosmetic Treatment is the largest and fastest-growing category, commanding approximately 35% of market revenue in 2025, driven by strong international demand for affordable aesthetic procedures. Medical Treatment remains a large and steady segment supported by JCI-accredited private hospitals offering internationally competitive pricing for complex interventional care.

The Philippines medical tourism market is being shaped by four key trends. First, the Filipino Brand of Wellness initiative is repositioning the Philippines as a holistic medical destination that integrates clinical care with wellness and leisure experiences. Second, the eHealth System and Services Act of 2024 is enabling telemedicine and remote patient management, extending the care continuum to international patients beyond their in-country visit. Third, foreign investment in healthcare infrastructure, particularly from Japanese and regional investors, is upgrading clinical capabilities and expanding specialized treatment options. Fourth, the rapid adoption of advanced surgical and diagnostic technologies, including robotic surgery systems at leading private hospitals, is closing the quality gap with competing medical tourism destinations in Southeast Asia.

The key players in the market include Health and Leisure, MedicalTourism.com, Al Afiya Medi Tour, World&Schedule, The Medical City, Tapscott Health Inc., and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Treatment Type |

|

| Breakup by Service Provider |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.