Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

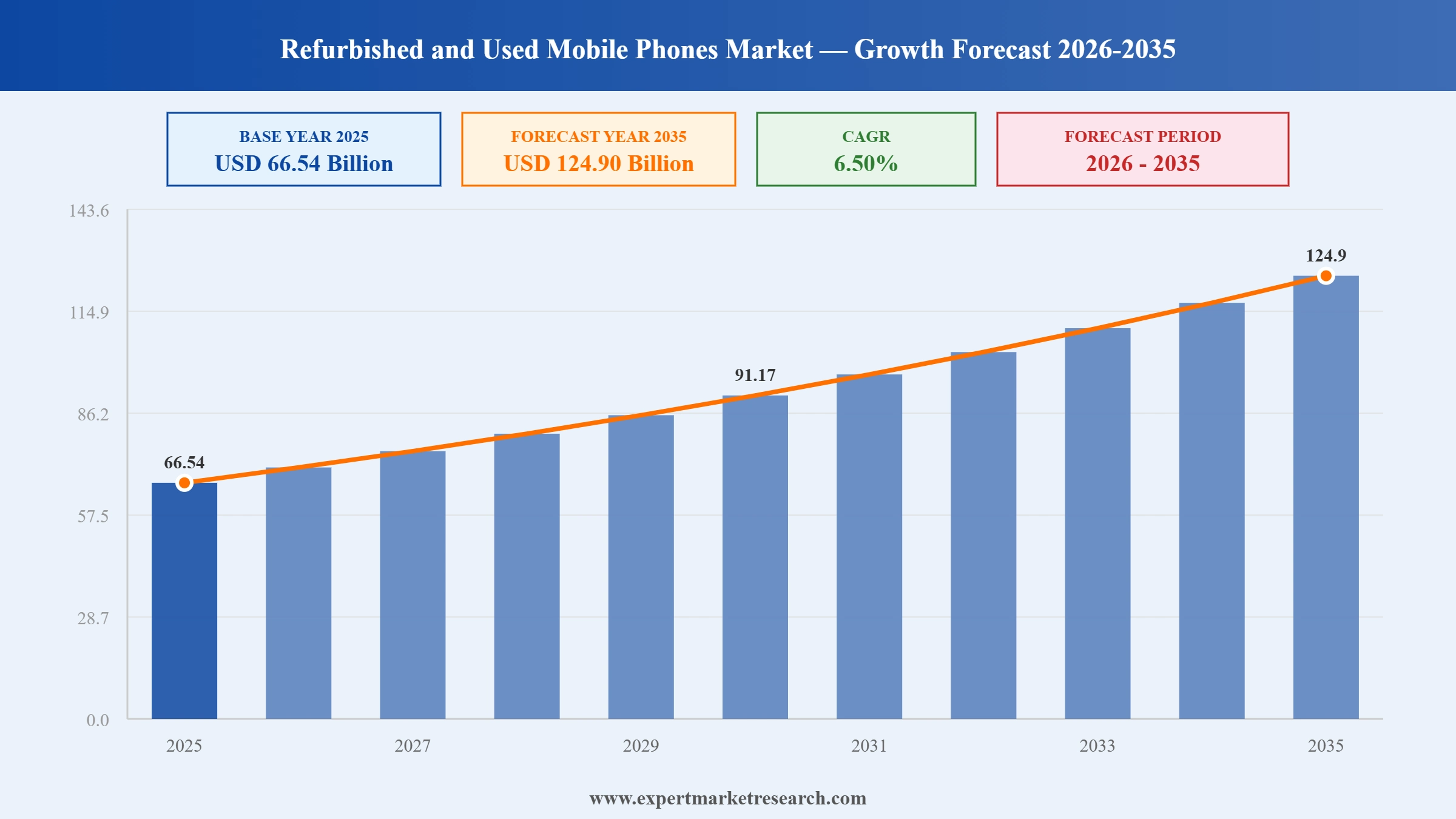

The global refurbished and used mobile phones market reached a value of USD 66.54 Billion at 2025 and is projected to expand at a CAGR of around 6.50% during the forecast period of 2026-2035. Fuelled by rising flagship smartphone prices making certified pre-owned devices an increasingly rational consumer choice, growing sustainability awareness driving circular economy adoption, expanding OEM-led certification programs from Apple and Samsung, and the rapid scale-up of e-commerce resale platforms, the market is expected to reach USD 124.90 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global refurbished and used mobile phones market is experiencing a structural maturation phase, as manufacturer-led certification programs from Apple, Samsung, and Google elevate quality standards and consumer trust in the secondary device channel. E-commerce platforms are simultaneously raising grading transparency, warranty quality, and return convenience, reshaping the purchase experience for a broader and more quality-conscious buyer base. These dynamics, combined with regulatory pressure from the EU's Right to Repair directive and rising flagship smartphone prices, are collectively broadening the market's total addressable consumer and enterprise base.

Apple expanded its certified refurbished iPhone program to the Netherlands, Belgium, and Ireland in April 2026, adding extended warranty coverage. The expansion deepens Apple's circular economy commitments and intensifies competition with Back Market and carrier-led refurbished phone programs across Europe.

Samsung Electronics launched a year-round Galaxy Trade-In Program in January 2025, allowing customers to trade in used Galaxy devices without buying a new phone. Piloting in South Korea and France, the program boosts supply of certified pre-owned smartphones globally.

Amazon launched its Renewed Premium program for refurbished smartphones in the United States in Q4 2024, offering higher-grade refurbished devices with extended warranties and stricter quality controls. The program targets quality-conscious buyers seeking certified pre-owned devices at competitive prices.

Back Market partnered with Visible, an app-based wireless service from Verizon, in September 2024, bundling every smartphone purchase with a USD 20 monthly subscription for twelve months. The partnership reduces total device costs and strengthens certified refurbished handset adoption.

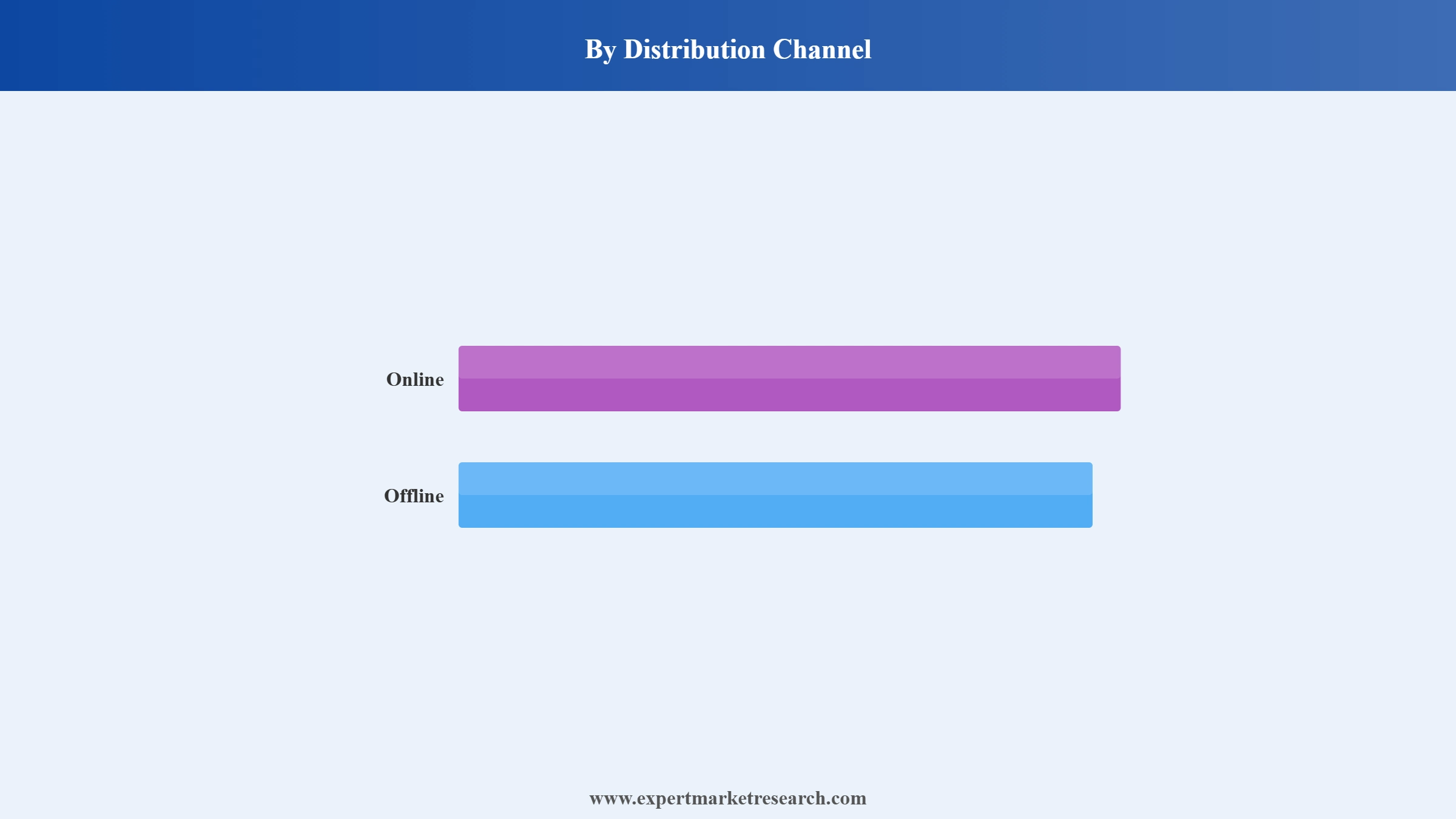

Online channels are the dominant distribution mechanism in the global refurbished and used mobile phones market, accounting for over 60% of purchases. Amazon Renewed, Back Market, and OEM storefronts offer transparent grading, warranty-backed listings, and doorstep delivery for buyers globally.

Asia Pacific leads the refurbished and used mobile phones market growth with approximately 39% market share in 2025. Vast population, rising middle-class demand for affordable 5G devices, and expanding e-commerce ecosystems in China, India, and Southeast Asia underpin regional leadership.

Europe's Right to Repair regulations are expanding the global refurbished and used mobile phones market by growing device supply. Mandatory repairability requirements and extended producer responsibility laws oblige manufacturers to support refurbishment, broadening certified device availability across EU member states.

Rising flagship prices are pushing buyers toward the refurbished and used mobile phones market. Apple's iPhone 16 Pro Max lists at USD 1,399.99, while refurbished equivalents sell at 30-40% discounts, making secondary device purchases an increasingly rational consumer choice globally.

Enterprises are adopting certified refurbished smartphones to cut fleet costs and meet sustainability targets, expanding the global refurbished and used mobile phones market. Carrier trade-in programs build supply, with AT&T alone collecting 12.5 million devices in 2024 for secondary redistribution.

The report of Expert Market Research's titled "Global Refurbished and Used Mobile Phones Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

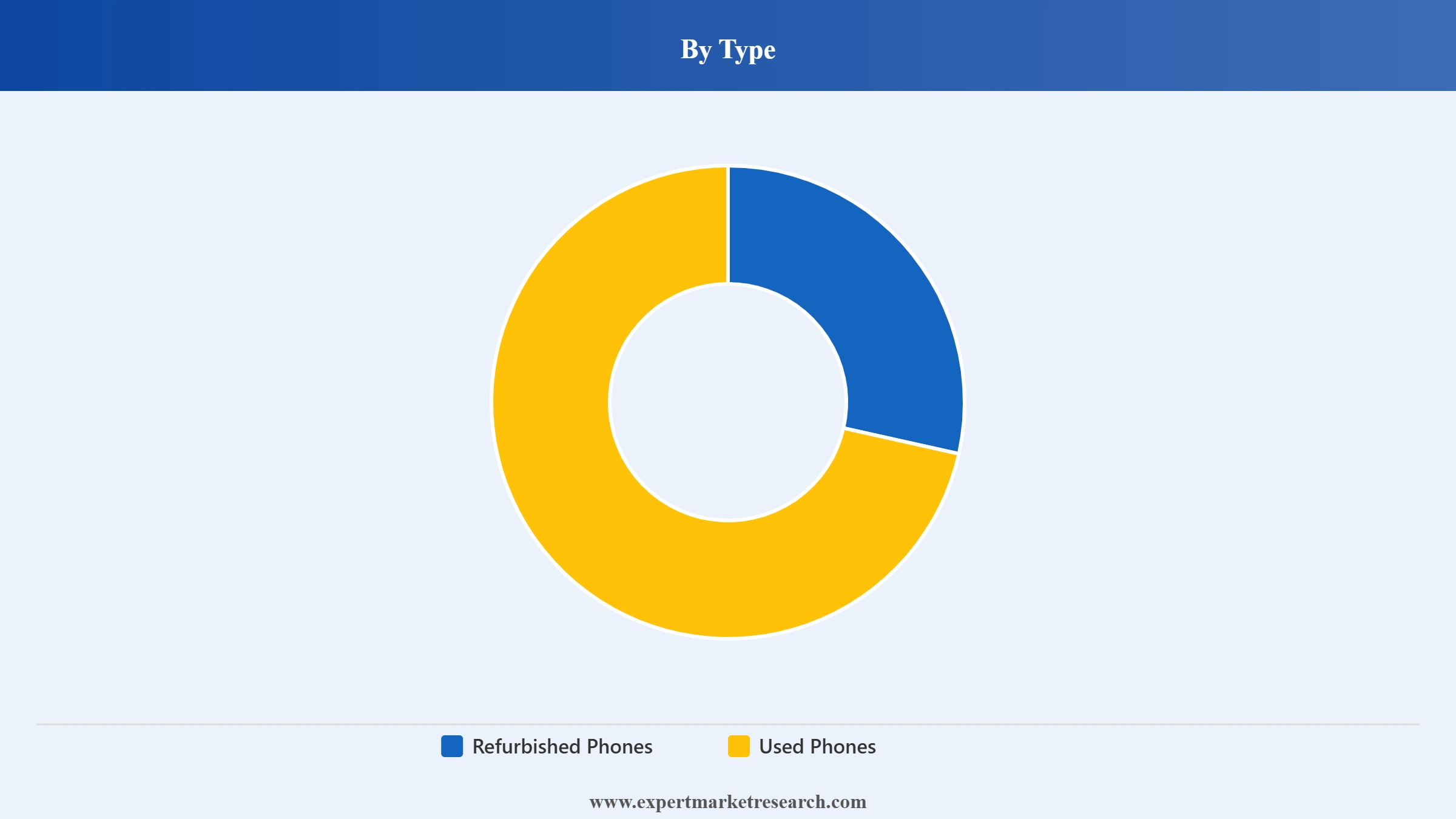

Market Breakup by Type

Key Insight: Refurbished phones dominate the global refurbished and used mobile phones market, accounting for over 58% of segment revenue, underpinned by the quality assurance and B2B compatibility that certified refurbishment processes deliver. Devices undergo diagnostic repair, component replacement, data wiping, software updates, and grading before resale, reducing buyer risk and enabling corporate IT fleet integration. OEM programmes from Apple and Samsung, which bundle AppleCare+ and Samsung Certified Re-Newed warranties, have materially lifted consumer and enterprise confidence. Used phones represent the fastest-growing sub-segment, driven by extreme price sensitivity in emerging markets including India, Sub-Saharan Africa, and Southeast Asia, where no-frills connectivity at the lowest cost outweighs warranty considerations.

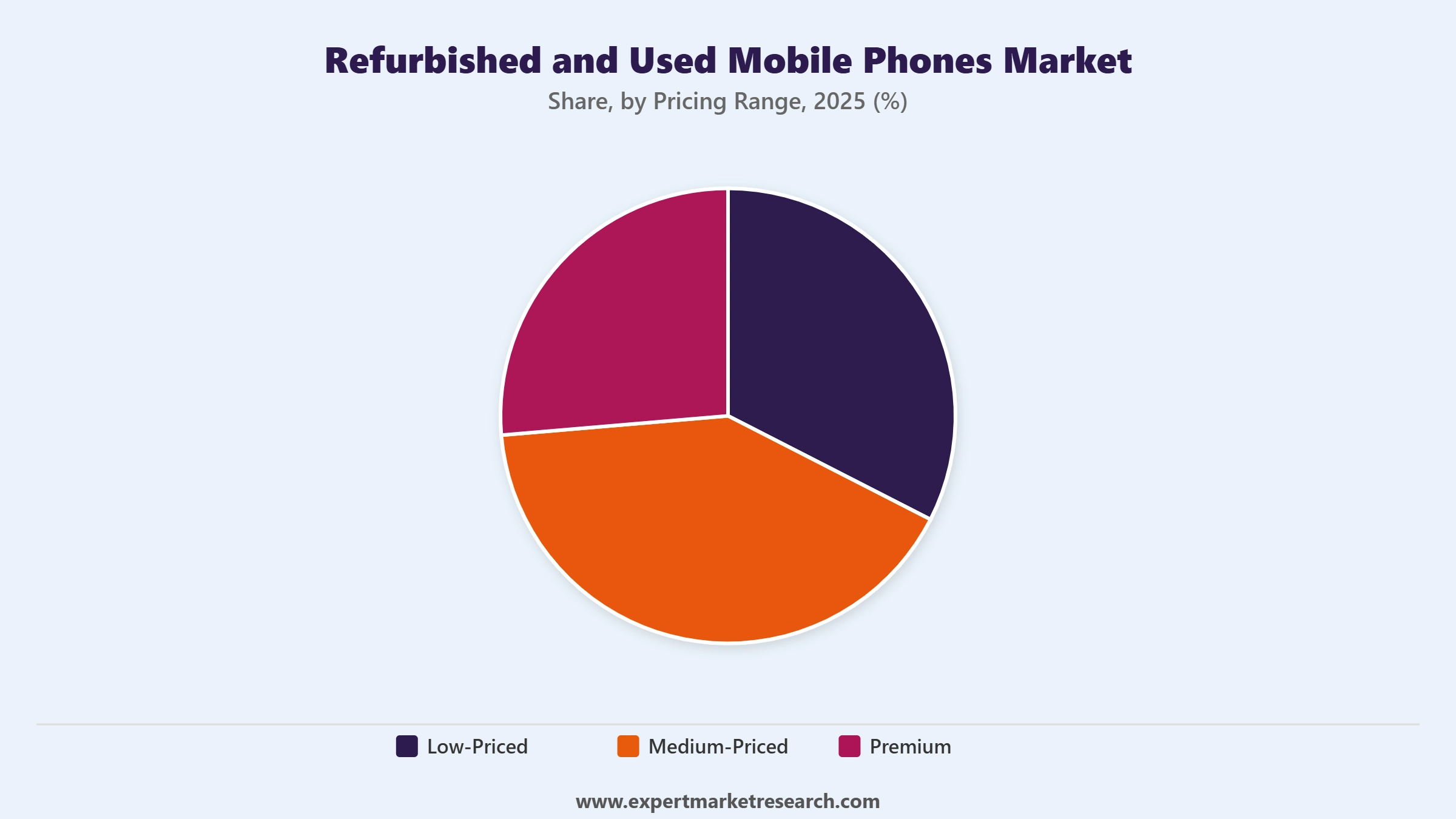

Market Breakup by Pricing Range

Key Insight: Medium-priced devices capture the largest share of the global refurbished and used mobile phones market by pricing range, commanding over 45% of revenue, as they deliver the most compelling combination of performance, features, and cost savings relative to new flagship equivalents. Buyers in this range gain access to near-current-generation hardware at 30-50% below retail prices, making the value proposition compelling for both individual consumers and corporate fleet managers. Low-priced devices are the fastest-growing sub-segment, expanding rapidly across first-time smartphone buyers, students, and rural populations in emerging economies where digital inclusion programmes support affordable device access. Premium refurbished devices are gaining traction as OEM certification programmes and extended warranty coverage reduce risk perception for high-ticket secondary purchases.

Market Breakup by Distribution Channel

Key Insight: Online channels dominate the global refurbished and used mobile phones market by distribution channel, accounting for over 60% of purchases. Dedicated marketplaces including Back Market, Swappa, and Amazon Renewed provide standardised grading transparency, flexible payment options, return policies, and wide model availability that offline retailers cannot match at scale. OEM-operated online storefronts are the fastest-growing online sub-channel, as brands seek to monetise secondary device demand directly while maintaining warranty and user experience control. Offline channels retain significance in emerging markets where digital payment penetration is limited and consumers prefer in-hand device inspection, while carrier trade-in desks serve as the primary offline inventory intake mechanism feeding certified online resale pipelines.

Market Breakup by Region

Key Insight: Asia Pacific commands the dominant share of the global refurbished and used mobile phones market with approximately 39% of global market value in 2025, driven by the region's massive population base, rising middle-class smartphone aspirations, and strong demand for affordable digital connectivity in China, India, Indonesia, and Vietnam. North America and Europe follow, with mature recommerce ecosystems, strong Right to Repair regulatory tailwinds, and high carrier trade-in programme penetration. Latin America and Middle East and Africa represent the fastest-growing regional markets, supported by large underserved populations, rising mobile penetration, and increasing preference for certified secondary devices as alternatives to unaffordable new flagship hardware.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, refurbished phones dominate the market due to certified quality assurances, warranty-backed consumer trust, and strong B2B enterprise adoption across corporate device fleet management

Refurbished phones command the dominant share of the global refurbished and used mobile phones market, holding over 58% of segment revenue, anchored by the quality assurance that formal refurbishment processes provide. Apple's Certified Refurbished program, which includes battery and component inspection, new accessories, and AppleCare+ eligibility, and Samsung's Certified Re-Newed programme, which guarantees 100% genuine parts, set quality benchmarks that independent third-party refurbishers increasingly replicate. B2B adoption is a particular strength, as corporate IT departments prefer warranty-backed certified devices for mobile device management system compatibility, data security, and lifecycle predictability.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Used phones are the fastest-growing type segment in the global refurbished and used mobile phones market, expanding due to extreme price sensitivity in high-growth emerging markets where unverified second-hand handsets represent the only financially accessible path to smartphone ownership. India, Sub-Saharan Africa, and Southeast Asia are the primary demand centres for used phones, where informal peer-to-peer resale channels and consumer-to-consumer platforms facilitate high-volume transactions despite limited quality guarantees. Trade-in programmes operated by carriers and OEMs are increasingly channelling used devices into structured resale pipelines, gradually formalising a segment that has traditionally operated outside organised commerce.

By Pricing Range, medium-priced devices account for the dominant share of the market due to their optimal balance of affordability and performance that resonates with the broadest range of consumer and enterprise buyers globally

Medium-priced devices hold the dominant share of the global refurbished and used mobile phones market by pricing range, capturing over 45% of revenue by delivering near-current-generation smartphone performance at 30-50% below original retail prices. Devices in this range, typically corresponding to one or two-generation-old flagship models from Apple, Samsung, and Xiaomi, offer consumers the cameras, processing speeds, and connectivity standards they want without the cost of new hardware. Corporate buyers favour medium-priced certified refurbished devices for their balance of performance, manageability, and cost efficiency in bulk device procurement for field workforce and enterprise mobility programmes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Low-priced devices are the fastest-growing sub-segment within the global refurbished and used mobile phones market's pricing range dimension, driven by digital inclusion programmes in emerging economies, rising first-time smartphone buyer populations, and government-led connectivity initiatives in South Asia, Sub-Saharan Africa, and Latin America. Premium refurbished devices are gaining share as OEM certification programmes and warranty extensions reduce the perceived risk of high-ticket secondary purchases. In April 2026, Apple's expansion of its certified refurbished iPhone programme to three additional European markets with extended warranty coverage specifically targeted premium segment buyers who had previously hesitated due to warranty limitations.

By Distribution Channel, online channels account for the dominant share of the market due to transparent device grading, wide model availability, flexible return policies, and the convenience of direct-to-consumer digital commerce

Online channels dominate the global refurbished and used mobile phones market with over 60% of total purchases, driven by the structural advantages that digital marketplaces hold over physical retail in the secondary device space. Back Market, Amazon Renewed, Swappa, and OEM-operated online stores provide standardised grading systems, comprehensive device histories, warranty documentation, and convenient return windows that build consumer confidence without in-person inspection. In September 2024, Back Market's partnership with Visible bundled wireless service with device purchases, further lowering the total cost of ownership and capturing demand from first-time refurbished device buyers who might otherwise have returned to new handset channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Offline channels retain a meaningful role in the global refurbished and used mobile phones market, particularly in emerging markets where digital payment infrastructure is limited, consumer trust in online transactions is lower, and the ability to physically inspect a device before purchase remains decisive. Carrier retail stores serve as dual-function touchpoints, collecting trade-in devices to feed certified resale pipelines while simultaneously selling certified pre-owned handsets to value-seeking customers. In Q4 2024, Amazon's introduction of its Renewed Premium programme in the United States demonstrated how online channels are raising the quality floor by imposing stricter physical inspection, battery health, and grading standards that increasingly match the experience expectations of offline shoppers.

Asia Pacific dominates the global refurbished and used mobile phones market due to its vast population base, rapidly expanding e-commerce infrastructure, and structural affordability gap between new flagship prices and average consumer purchasing power

Asia Pacific holds approximately 39% of the global refurbished and used mobile phones market, anchored by China's mature refurbishment ecosystem supported by Alibaba and JD.com dedicated secondary device sections, India's fast-scaling secondary market enabled by the UPI digital payments infrastructure and a mobile broadband base exceeding 969 million subscribers, and Southeast Asia's youthful demographics and 20% annual smartphone growth trajectory. Japan's secondary device sales reached 3.15 million units in fiscal 2024, a 15.5% year-on-year rise, supported by wide retail distribution and aggressive certified stock marketing. India's demand significantly exceeds organised supply, indicating substantial untapped growth potential that formal refurbishment networks are actively building capacity to address.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Latin America is the fastest-growing regional market in the global refurbished and used mobile phones market, driven by Brazil's 167 million mobile phone owners, Mexico's 81.7% cellphone usage penetration, and Argentina's regulatory shifts that are redirecting price-sensitive buyers toward certified secondary channels. The region recorded a 19% surge in refurbished phone sales in 2023, and this momentum is accelerating as high import duties, currency inflation, and rising new device prices structurally expand the affordability gap in favour of secondary market options. Europe represents a mature, high-quality secondary market anchored by the EU Right to Repair directive, with Germany holding approximately 24% regional share and a CAGR of 10.1% projected from 2026 to 2033.

The global refurbished and used mobile phones market features a fragmented but rapidly consolidating competitive landscape spanning OEM-operated certified programs, specialist e-commerce refurbishment platforms, carrier-operated trade-in resale channels, and regional third-party refurbishers. OEMs including Apple, Samsung, and Google anchor the premium quality tier through branded certification programs that set grading, warranty, and component standards benchmarked by the broader market. E-commerce platforms including Back Market, Amazon Renewed, and Swappa complement OEM programs by aggregating multi-brand certified inventory at scale, applying AI-powered grading systems, and offering consumer-friendly return and warranty policies that have materially reduced the trust gap in secondary device purchasing.

Telecom carriers including AT&T and Verizon occupy a strategically important dual role as both the primary device collection channel through trade-in programmes and as active secondary market resellers through certified pre-owned storefronts and marketplace partnerships. Competitive differentiation is shifting from price alone toward warranty depth, grading transparency, supply chain reliability, and sustainability credentials, as consumer expectations for secondary device quality continue to rise alongside flagship price inflation. Regional players in India including Cashify, and specialised platforms in Europe such as Recommerce Group and Swappie, are carving out strong regional market positions by combining local collection networks with professional refurbishment standards.

Apple Inc., founded in 1976 and headquartered in Cupertino, California, United States, is the world's largest technology company by revenue and the dominant brand within the premium refurbished and used mobile phones market globally. Apple's Certified Refurbished program guarantees battery and component inspection, new outer shells and accessories, and AppleCare+ eligibility, setting the quality standard for OEM-branded secondary devices. In April 2026, Apple expanded its certified refurbished iPhone program to three additional European markets, reinforcing its circular economy commitments and competitive positioning in the premium refurbished segment.

Samsung Electronics Co. Ltd, founded in 1969 and headquartered in Suwon, South Korea, is the world's largest smartphone manufacturer by volume and a leading participant in the global refurbished and used mobile phones market through its Certified Re-Newed programme, which guarantees 100% genuine Samsung parts and standardised refurbishment protocols. In January 2025, Samsung launched its year-round Galaxy Trade-In Program globally, enabling customers to exchange used Galaxy devices without a new purchase, expanding certified secondary device supply across South Korea, France, and additional international markets.

Amazon.com, Inc., founded in 1994 and headquartered in Seattle, Washington, United States, operates Amazon Renewed, one of the world's largest certified refurbished electronics marketplaces, offering quality-grade refurbished smartphones, tablets, and accessories with standardised inspection, cleaning, and warranty coverage. In Q4 2024, Amazon launched the Renewed Premium programme for refurbished smartphones in the United States, imposing stricter quality controls and extending warranty terms for higher-grade devices, targeting quality-conscious buyers who had previously prioritised new handsets for reliability assurance.

AT&T Inc., founded in 1983 and headquartered in Dallas, Texas, United States, is one of the world's largest telecommunications companies and a major participant in the global refurbished and used mobile phones market through its carrier trade-in programme, which collected 12.5 million devices in 2024. These devices feed certified pre-owned resale pipelines that serve both individual consumers and business customers. AT&T's network of retail stores and online storefronts positions it as a dual-role market participant, simultaneously driving secondary device supply through trade-ins and demand through certified pre-owned handset sales.

Other key players in the market are Flipkart Internet Private Limited, Reboxed Limited, FoneGiant.com, Verizon, Kempf Enterprises Limited, Nippon Telephone Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the global refurbished and used mobile phones market 2026 with our comprehensive research report. From OEM certification programme expansion and flagship price inflation driving secondary demand, to Asia Pacific's dominant growth, Europe's regulatory tailwinds, and Latin America's accelerating adoption, this report gives you the complete strategic picture. Whether you are entering a new regional market, scaling a refurbishment operation, evaluating a channel partnership, or tracking competitive moves from Apple and Samsung, download your free sample today.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 66.54 Billion.

The market is projected to grow at a CAGR of 6.50% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 124.90 Billion by 2035.

Key strategies driving the market include forming OEM-logistics-tech alliances, investing in AI refurb chains, localising diagnostic hubs, embedding carbon analytics, and developing region-specific B2B bundles with compliance and ESG guarantees to scale trust and impact.

Key trends aiding market expansion include the rising costs of new smartphones, availability of refurbished and used mobile phones on online platforms, and reduction in feature-upgrades in new mobile phones.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The market based on pricing range is segmented into low-priced, medium-priced, and premium.

The lifespan of a refurbished or used mobile phone depends upon multiple factors, such as the manufacturing date, durability, and condition of the mobile phone. Refurbished mobile phones may last longer as their quality has been checked and repairs made.

The primary distribution channels in the market are online and offline.

The key players include Apple Inc., Samsung Electronics Co. Ltd, Amazon.com, Inc., AT&T Inc., Flipkart Internet Private Limited, Reboxed Limited, FoneGiant.com, Verizon, Kempf Enterprises Limited, Nippon Telephone Inc., and Others.

The key challenges are inconsistent global regulations, lack of standardised grading systems, warranty management complexity, and limited consumer trust in used devices.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Pricing Range |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.