Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

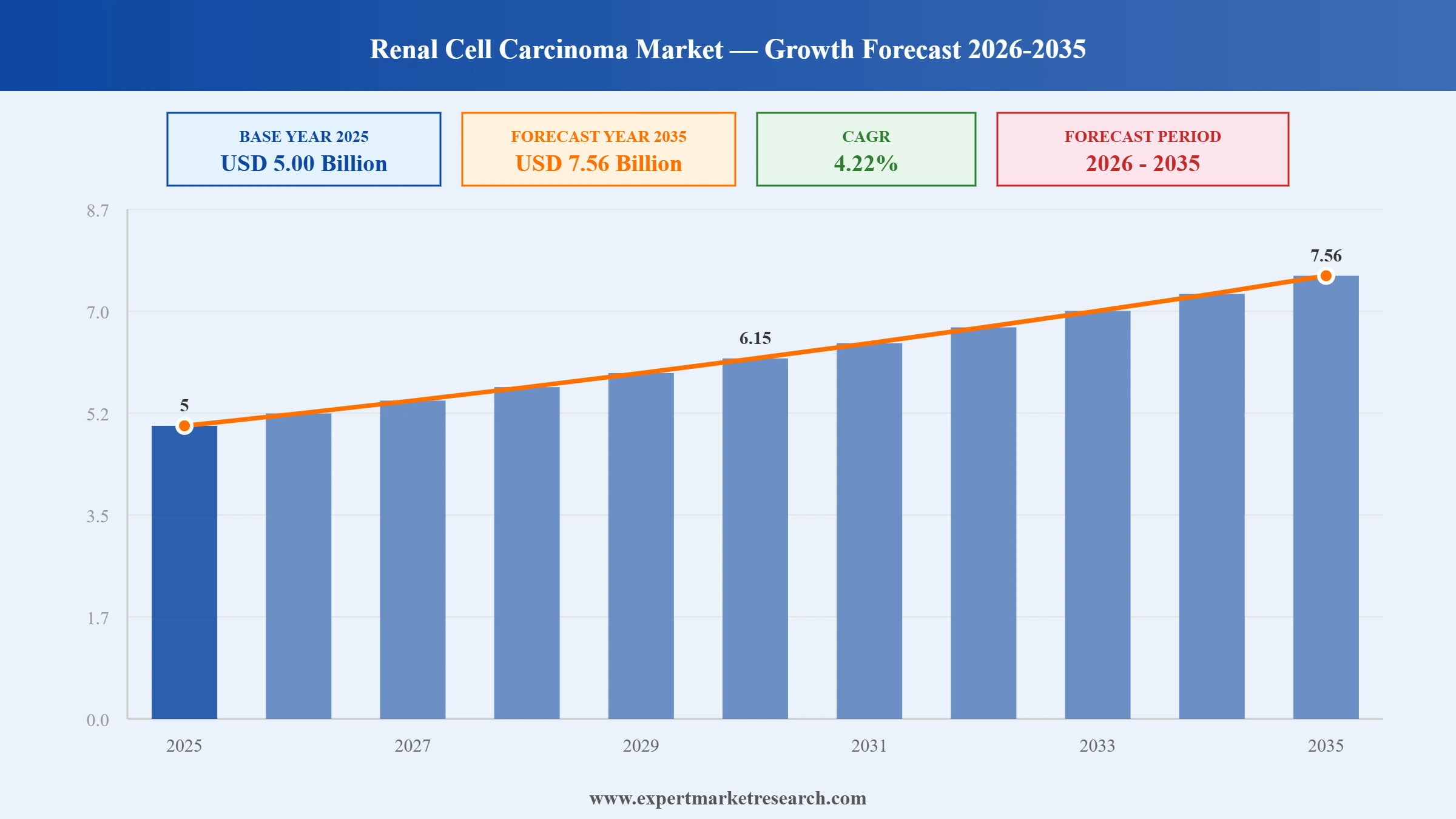

The renal cell carcinoma market was valued at USD 5.00 Billion in 2025. It is poised to grow at a CAGR of 4.22% during the forecast period of 2026-2035, and reach USD 7.56 Billion by 2035. The market growth is driven by increasing incidence of renal cell carcinoma, rising adoption of targeted therapies, immunotherapy advancements, and expanding clinical research improving treatment outcomes globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market is experiencing steady growth due to the rising incidence of kidney cancer and increasing adoption of targeted therapies and immunotherapies. Advancements in precision medicine and biomarker-driven treatment approaches are improving patient outcomes. Expanding clinical trials, strong pipeline development, and growing healthcare investments are further supporting market expansion across developed and emerging regions globally. The market reached a value of approximately USD 5.00 Billion in 2025.

Rising Targeted Therapy Innovations Driving the Market Development

Growing demand for precision oncology and expanding late-stage pipelines are driving market development. For instance, in October 2025, researchers reported that lenvatinib plus everolimus demonstrated improved outcomes as a second-line treatment for advanced renal cell carcinoma. This progress is enhancing therapeutic strategies and supporting biomarker-guided evaluation, including glomerular filtration rate (GFR), strengthening long-term market development.

Key trends shaping the market include rising adoption of immunotherapies, increasing use of targeted therapies, expanding clinical trials, and growing focus on personalized treatment approaches globally.

Rising Clinical Trial Advancements Supporting the Market Expansion

The rising incidence of kidney cancer and increasing investment in targeted therapies are accelerating market growth. For instance, in April 2026, Kura Oncology, Inc. reported positive clinical data for darlifarnib combined with cabozantinib, demonstrating meaningful tumor response in previously treated renal cell carcinoma patients. This advancement is strengthening precision treatment adoption and supporting monitoring approaches using creatinine, driving market growth.

Market Breakup by Indication Type

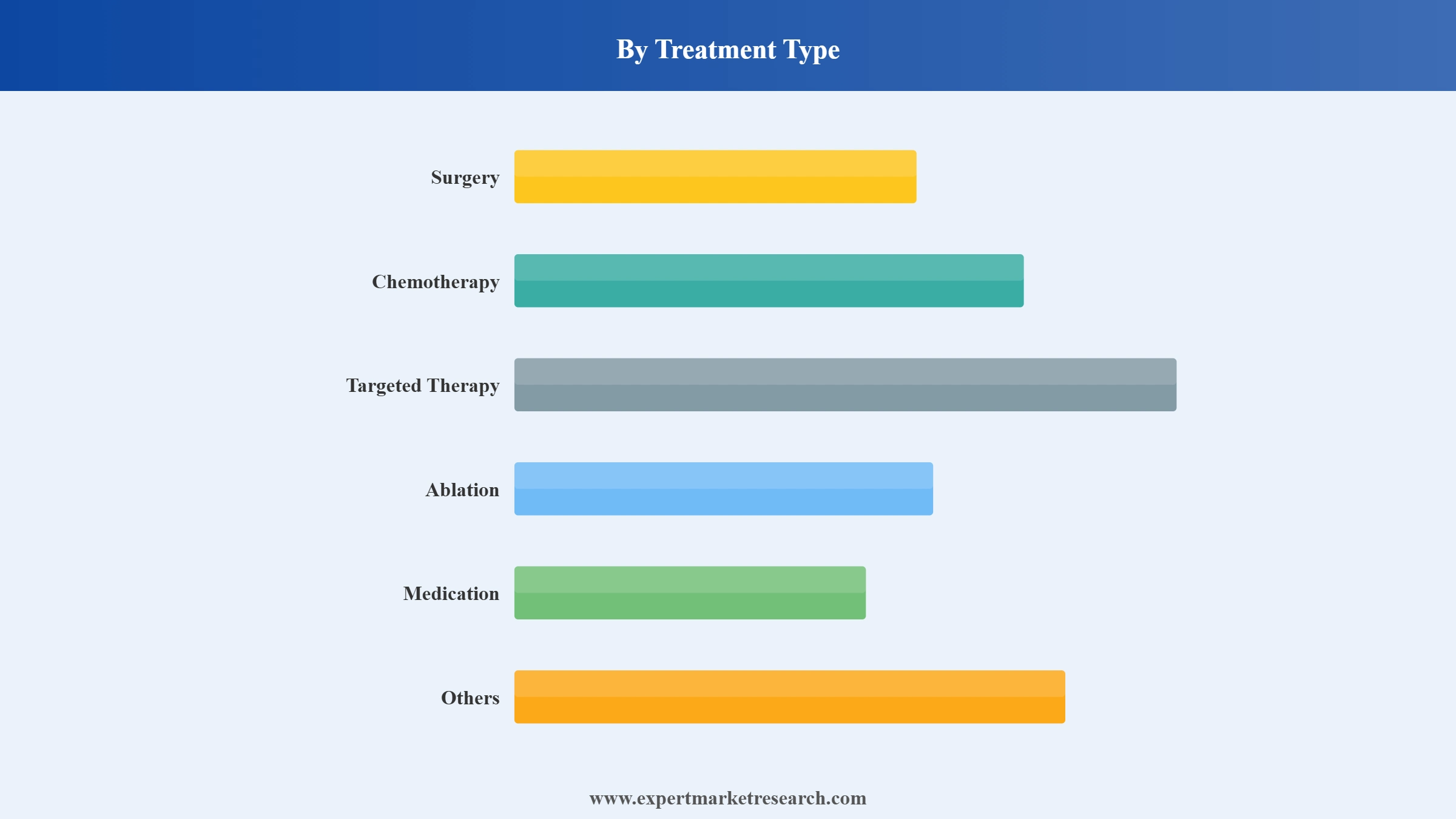

Market Breakup by Treatment Type

Market Breakup by Diagnosis

Market Breakup by Dosage Form

Market Breakup by Route of Administration

Market Breakup by End User

Market Breakup by Distribution Channel

Market Breakup by Country

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Targeted Therapy Expected to Dominate the Market Segment by Treatment Type

The targeted therapy segment led the market, accounting for around 45% share in the historical period. Its dominance is driven by strong clinical efficacy, widespread adoption, and continued innovation in precision oncology. Increasing use of biomarker-driven approaches, including glomerular filtration rate (GFR) assessment, is improving treatment selection and supporting sustained growth across advanced RCC management globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United States dominated the market with over 40% share in the historical period. This leadership is supported by advanced healthcare infrastructure, strong reimbursement systems, and high adoption of novel therapies. Growing emphasis on early detection and disease monitoring, including the use of creatinine, is enhancing clinical outcomes and reinforcing the country’s position in the global RCC market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The key features of the market report comprise patent analysis, funding and investment analysis, and strategic initiatives by the leading players. The major companies in the market are as follows:

Headquartered in Laval, Canada, and founded in 1959, Bausch Health Companies Inc. focuses on specialty pharmaceuticals, primarily in gastroenterology, dermatology, and ophthalmology. The company has limited direct exposure to renal cell carcinoma but supports oncology care through adjunct therapies. Its broader clinical focus aligns with monitoring disease burden, including indicators such as creatinine in patient management settings globally.

Abbott is a global healthcare company headquartered in Abbott Park, Illinois, specializing in diagnostics, medical devices, nutrition, and branded generic pharmaceuticals. In the renal cell carcinoma market, the company supports oncology care through advanced diagnostic solutions and biomarker monitoring technologies that aid in disease detection and treatment management. Abbott’s strong focus on precision diagnostics and patient monitoring contributes to improved clinical decision-making and enhances overall cancer care outcomes across healthcare settings.

Merck KGaA, headquartered in Darmstadt, Germany, and founded in 1668, is actively involved in oncology, including renal cell carcinoma treatment through immunotherapy combinations such as Bavencio. The company continues to expand clinical research in RCC. Its oncology strategy supports biomarker-driven treatment approaches, including evaluation of glomerular filtration rate (GFR) for improved patient stratification and therapeutic monitoring globally.

AbbVie Inc., headquartered in North Chicago, Illinois, USA, and founded in 2013, is a major biopharmaceutical company focused on oncology, immunology, and targeted therapies. While not a primary RCC leader, its oncology pipeline contributes to combination strategies. The company’s research supports biomarker-based monitoring approaches, including the use of acute kidney injury biomarker indicators in clinical oncology settings.

Other key players in the market are Johnson & Johnson Services, Inc., AstraZeneca PLC, Merck & Co., Inc., Mylan N.V., Eli Lilly and Company, and Pfizer, Inc., and Bayer AG.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$3299 $2969

$5499 $4949

$6999 $5949

$8199 $6969

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Indication Type |

|

| Breakup by Treatment Type |

|

| Breakup by Diagnosis |

|

| Breakup by Dosage Form |

|

| Breakup by Route of Administration |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,299

USD 2,969

tax inclusive*

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,199

USD 6,969

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.