Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global semiconductor market reached a value of USD 673.18 Billion at 2025 and is projected to expand at a CAGR of around 7.70% during the forecast period of 2026-2035. Driven by surging artificial intelligence chip demand, rapid data centre expansion, automotive electrification, and accelerating geopolitical reshoring initiatives in the United States, Europe, and Asia, the market is expected to reach USD 1413.48 Billion by 2035.

Compound Annual Growth Rate

7.7%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Semiconductor Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 673.18 |

| Market Size 2035 | USD Billion | 1413.48 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.70% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 8.9% |

| CAGR 2026-2035 - Market by Country | India | 10.2% |

| CAGR 2026-2035 - Market by Country | China | 8.5% |

| CAGR 2026-2035 - Market by Component | Memory Devices | 8.7% |

| CAGR 2026-2035 - Market by Application | Automotive | 8.8% |

| Market Share by Country 2025 | France | 3.5% |

The global semiconductor market is undergoing a structural transformation driven by artificial intelligence workloads, geopolitical supply chain diversification, and the rapid expansion of advanced packaging and memory technologies. Record levels of government-backed fab investment across the United States, Japan, Europe, and India are reshaping production geography, while demand for high-bandwidth memory, advanced logic nodes, and power semiconductors accelerates across end markets.

Artificial intelligence is the most transformative demand driver in the global semiconductor market, reshaping product mix across logic, memory, and advanced packaging segments. Nvidia's GPU platforms, AMD's Instinct series, and custom AI accelerators from hyperscalers including Google, Amazon, and Microsoft are absorbing a disproportionate share of advanced node foundry capacity. The shift to AI inference at the edge is extending semiconductor growth beyond data centres into smartphones, automotive, and industrial applications, broadening the addressable market substantially.

Advanced semiconductor packaging, including chip-on-wafer-on-substrate (CoWoS) and fan-out wafer-level packaging (FOWLP) technologies, has emerged as a critical constraint and differentiator in the global semiconductor market. The chiplet architecture approach, adopted by AMD, Intel, and TSMC customers, enables performance scaling without relying solely on node shrinks, reducing development costs and time to market. CoWoS capacity at TSMC became a primary bottleneck for AI accelerator production, prompting significant investment expansion to meet hyperscaler procurement timelines.

Automotive semiconductors represent one of the fastest-growing end markets within the global semiconductor market, fuelled by rising electric vehicle adoption, advanced driver assistance systems (ADAS), and increasing software-defined vehicle content. Power semiconductors, microcontrollers, and imaging sensors for automotive applications are experiencing strong structural demand growth as the average semiconductor content per vehicle rises with electrification. Leading suppliers including Infineon Technologies, NXP Semiconductors, and Texas Instruments are expanding automotive-grade production capacity to address multi-year order backlogs.

Intensifying geopolitical tensions between the United States and China are fundamentally reshaping global semiconductor supply chains. US export controls restricting advanced chip exports to China, combined with the CHIPS and Science Act, the EU Chips Act, and Japan's semiconductor subsidy programmes, are creating parallel supply chain ecosystems. Chinese domestic semiconductor investment has accelerated significantly, with companies including SMIC and Hua Hong advancing to more mature process nodes. The bifurcation of global semiconductor supply chains represents both a structural challenge and an investment opportunity for the industry.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The report of the Expert Market Research's titled "Global Semiconductor Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Component

Key Insight: Logic devices account for the largest share of the global semiconductor market by component, driven by the explosive growth in AI processors, central processing units, and graphics processing units. Memory devices, led by DRAM and NAND flash, are the fastest-growing component segment, propelled by high-bandwidth memory demand from AI data centres. Analogue ICs sustain stable demand from industrial automation and automotive electrification applications globally.

Market Breakup by Application

Key Insight: Consumer electronics is the largest application segment in the global semiconductor market by volume, encompassing smartphones, personal computers, tablets, and wearables. The data centre segment is the fastest-growing application, fuelled by hyperscaler AI infrastructure investment and cloud service expansion. Automotive is a high-growth structural opportunity, with rising semiconductor content per vehicle driven by electrification and ADAS requirements.

Market Breakup by Region

Key Insight: Asia Pacific dominates the global semiconductor market, home to the world's largest foundries, memory producers, and assembly facilities in Taiwan, South Korea, China, and Japan. North America leads in semiconductor design and intellectual property, with fabless leaders including Nvidia, Qualcomm, and AMD driving significant value creation. Europe holds a strategically important position in automotive and industrial semiconductors, anchored by Infineon Technologies, STMicroelectronics, and NXP Semiconductors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Component, logic devices dominate the market due to AI accelerator demand and broad cross-industry adoption

Logic devices represent the largest component segment in the global semiconductor market, encompassing processors, AI accelerators, application processors, and field-programmable gate arrays (FPGAs). The extraordinary growth of AI training and inference workloads has elevated GPU and custom AI chip demand to unprecedented levels, absorbing the majority of advanced node capacity at leading foundries. Nvidia's data centre GPU revenue growth, alongside AMD's MI300X ramp and hyperscaler custom silicon programmes, underscores logic devices' dominant and expanding market position.

Memory devices are the fastest-growing component category, driven by the high-bandwidth memory requirements of AI computing infrastructure. HBM3 and HBM3E memory, produced primarily by Samsung and SK Hynix, commands significant premium pricing relative to standard DRAM. NAND flash demand benefits from data centre storage expansion and premium smartphone adoption. Microcomponents, including microcontrollers, retain stable demand from automotive and industrial automation applications, maintaining consistent revenue contribution within the global semiconductor market.

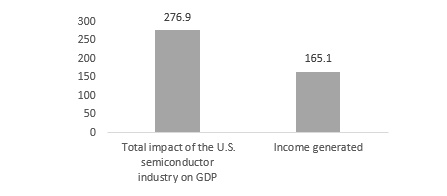

U.S. SEMICONDUCTOR INDUSTRY ON GDP AND INCOME, 2021, IN USD BILLION

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, data centre accounts for the fastest-growing share due to AI infrastructure investment by global hyperscalers

The data centre application segment is the fastest-growing end market in the global semiconductor market, driven by hyperscaler investment in AI training clusters, inference servers, and cloud computing infrastructure. Companies including Microsoft, Google, Amazon, and Meta are committing record capital expenditure to AI semiconductor procurement, with Nvidia GPU allocations representing multi-year supply commitments. The rise of large language models and generative AI services is creating sustained, inelastic demand for advanced logic and memory semiconductors across the data centre category.

Consumer electronics remains the largest application segment by shipment volume, with smartphone and PC semiconductor demand serving as the primary revenue base for the global semiconductor market historically. However, automotive semiconductors are gaining structural importance as electric vehicle penetration increases globally. Advanced semiconductor content per electric vehicle, encompassing power management ICs, ADAS processors, battery management systems, and in-vehicle networking chips, is significantly higher than in conventional internal combustion engine vehicles, driving durable demand expansion from automotive manufacturers.

By Region, Asia Pacific dominates the market due to integrated manufacturing ecosystems, leading foundries, and largest end-market volume

Asia Pacific commands the largest share of the global semiconductor market, underpinned by the world's most advanced semiconductor manufacturing ecosystems in Taiwan, South Korea, Japan, and China. TSMC's leadership in advanced node logic production, Samsung and SK Hynix's dominance in memory, and China's expanding foundry capacity collectively position the region as indispensable to global semiconductor supply chains. Government investment programmes in Japan, India, and South Korea are further reinforcing Asia Pacific's manufacturing capacity for the coming decade.

North America leads the global semiconductor market in design value and intellectual property, generating the highest revenue per chip through fabless business models. The CHIPS and Science Act is catalysing significant reshoring of advanced manufacturing to the United States, with TSMC, Samsung, and Intel collectively investing over USD 200 billion in domestic US fab capacity. Europe's semiconductor industry is anchored in automotive, industrial, and power semiconductor segments, with the EU Chips Act targeting a doubling of Europe's global market share to 20% by 2030.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the market due to world-leading foundry capacity, vertically integrated memory manufacturers, and the highest concentration of semiconductor end markets

Asia Pacific leads the global semiconductor market, hosting the world's most advanced and highest-volume semiconductor manufacturing infrastructure. TSMC, headquartered in Hsinchu, Taiwan, produces over 90% of the world's most advanced logic chips below 7nm, making it indispensable to global technology supply chains. Samsung and SK Hynix in South Korea collectively account for over 70% of global DRAM production and lead in high-bandwidth memory for AI. Japan's semiconductor equipment and materials industries are critical to global fab operations, while China's domestic chip industry is accelerating investment across mature and advancing process nodes.

North America is the principal semiconductor design region, generating the majority of global semiconductor intellectual property value through fabless companies including Nvidia, Qualcomm, Apple Silicon, AMD, and Broadcom. The United States government's CHIPS and Science Act is driving a historic reshoring of advanced manufacturing, with over USD 52 billion in federal subsidies supporting domestic fab construction. TSMC's Arizona facilities, Samsung's Texas fab, and Intel's Ohio gigafab collectively represent over USD 200 billion in planned US manufacturing investment through the decade.

The global semiconductor market is highly concentrated at the advanced node level, with TSMC, Samsung Foundry, and Intel Foundry collectively controlling the majority of sub-7nm logic production capacity. The memory segment is dominated by Samsung Electronics, SK Hynix, and Micron Technology. The fabless segment is led by Nvidia, Qualcomm, Apple Silicon, AMD, and Broadcom. Competitive dynamics are increasingly shaped by AI chip performance, advanced packaging capability, manufacturing yield at leading nodes, and geopolitical supply chain positioning.

The industry is characterised by extreme capital intensity, with a leading-edge logic fab requiring investment of USD 20 to 30 billion, creating high barriers to entry and sustaining the dominance of incumbents. Strategic alliances between fabless designers, foundry partners, and advanced packaging providers are becoming essential to managing supply chain risk and accelerating time to market. Governments' industrial policy interventions across the United States, Europe, Japan, and India are reshaping competitive dynamics by introducing subsidised capacity that alters cost structures for chipmakers globally.

Founded in 1968, headquartered in Santa Clara, California, United States. Intel is one of the world's largest semiconductor companies by revenue, serving data centre, client computing, network, and edge markets. Intel's IDM 2.0 strategy repositions the company as both an internal chip designer and an external foundry provider through Intel Foundry Services. Intel's 18A process node, incorporating RibbonFET Gate-All-Around transistor technology, is targeting re-entry into the leading-edge foundry market, competing directly with TSMC's N2 process for next-generation AI and client chip production.

Founded in 1978, headquartered in Boise, Idaho, United States. Micron Technology is one of the world's three leading DRAM and NAND flash memory producers, alongside Samsung Electronics and SK Hynix. Micron is a primary supplier of HBM3E memory for AI data centre applications, competing directly for Nvidia GPU stack supply allocation. The company is investing significantly in US domestic memory production capacity, supported by CHIPS Act subsidies, with advanced memory fabs planned in New York and Idaho serving both AI and consumer electronics demand.

Founded in 1985, headquartered in San Diego, California, United States. Qualcomm is the global leader in mobile application processors and wireless modem semiconductors, powering the majority of Android premium smartphones with its Snapdragon platforms. Qualcomm's Snapdragon 8 Elite processor, produced on TSMC's 3nm process, delivers industry-leading AI inference performance for on-device AI applications. Qualcomm is diversifying beyond mobile into automotive, extended reality, and PC markets, with its Snapdragon X Elite PC platform targeting the AI-PC transition as a major structural growth opportunity.

Founded in 1969, headquartered in Suwon, South Korea. Samsung Electronics is the world's largest memory semiconductor producer and a leading integrated device manufacturer, operating both Samsung Semiconductor and Samsung Foundry divisions. Samsung holds a dominant position in DRAM and NAND flash memory globally, and its foundry division competes with TSMC for advanced logic node contracts using Gate-All-Around transistor technology from its 3nm process onward. Samsung's semiconductor division is the primary revenue driver of the broader Samsung Electronics conglomerate and a central player in AI memory supply chains.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the full scope of the global semiconductor industry with our in-depth 2026 market report. From AI accelerator demand and advanced packaging innovation to geopolitical supply chain shifts and regional fab investment, this report equips technology investors, chip designers, foundry operators, and enterprise procurement teams with the strategic intelligence needed to navigate the world's most complex and consequential technology market. Download your free sample today and position your organisation ahead of the next wave of semiconductor growth.

North America Analog Semiconductor Market

Asia Pacific Analog Semiconductor Market

Upto 15% Off

USD

$2999 $2699

$4839 $4355

$5999 $5099

$7259 $6170

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market was valued at USD 673.18 Billion in 2025.

The market is projected to grow at a CAGR of 7.70% between 2026 and 2035.

The revenue generated from the semiconductor market is expected to reach USD 1413.48 Billion in 2035.

Technological advancements, growing consumer electronics demand, environmental concerns and defence and aerospace are the major trends impacting the semiconductor market trends.

The semiconductor market is categorised according to the components, which include memory devices, logic devices, analogue IC, OSD and microcomponents.

The key players are Intel Corporation (NASDAQ: INTC), Samsung Electronics Co., Ltd., Texas Instruments, Nvidia Corporation, Micron Technology, Inc. (NASDAQ: MU), Qualcomm Technologies, Inc. (NASDAQ: QCOM), SK Hynix Inc. (KRX: 000660), Taiwan Semiconductor Manufacturing Company Limited, Broadcom Inc., MediaTek Inc., and NXP Semiconductors N.V. among others.

Based on the application, the market is divided into automotive, industrial, data centre, telecommunication, consumer electronics, aerospace and defence, healthcare, and others.

The market is broken down into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The Asia-Pacific region is the fastest-growing region in the global semiconductor market, driven by technological advancements, and the surging demand for consumer electronics.

The top five companies in the semiconductor market are Intel Corporation (NASDAQ: INTC), Samsung Electronics Co., Ltd., Texas Instruments, Nvidia Corporation, and Micron Technology, Inc. (NASDAQ: MU).

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,839

USD 4,355

tax inclusive*

Five User License

Five User

USD 5,999

USD 5,099

tax inclusive*

Corporate License

Unlimited Users

USD 7,259

USD 6,170

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.