Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

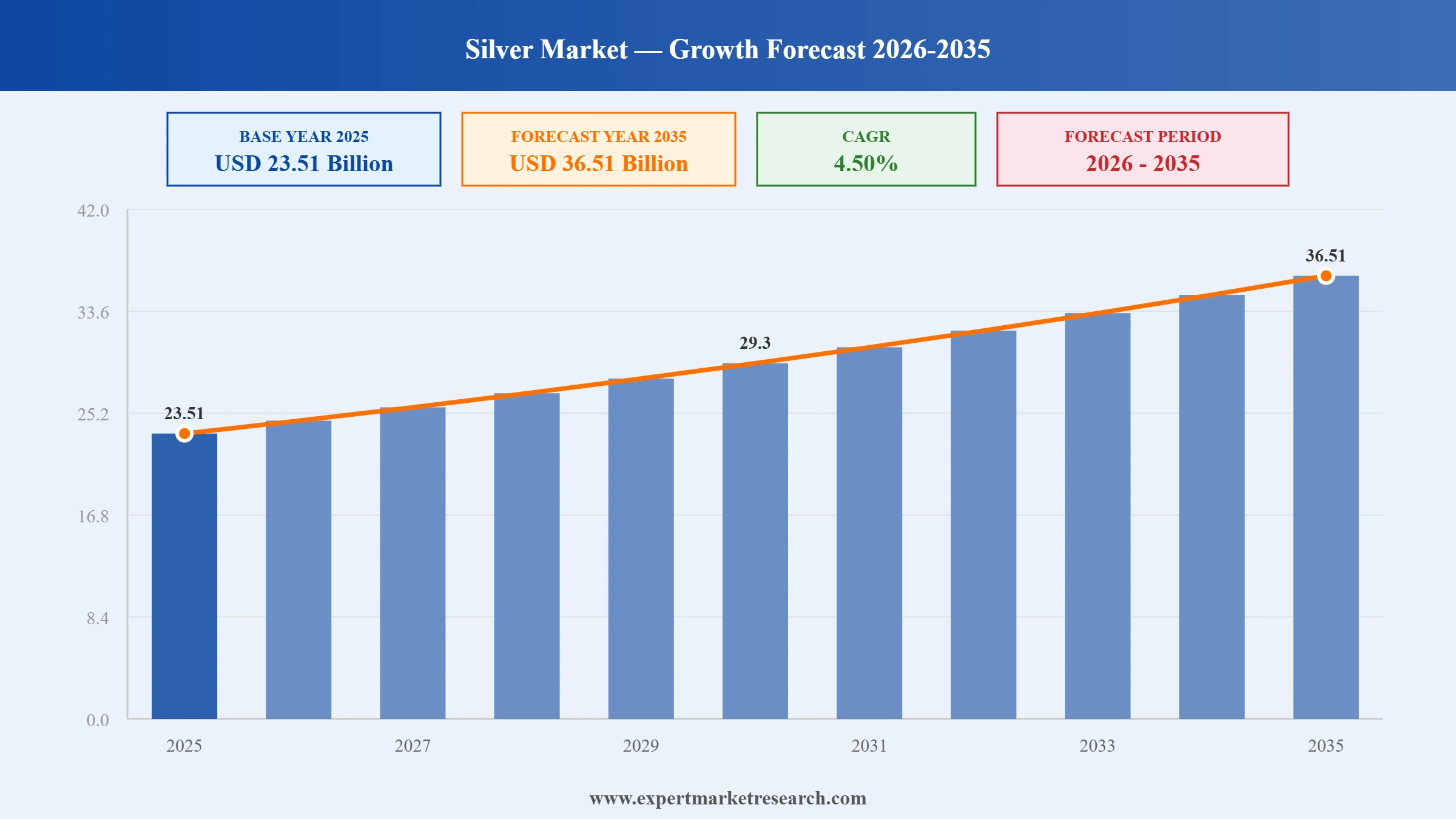

The Silver Market reached a value of USD 23.51 Billion at 2025 and is projected to expand at a CAGR of around 4.50% during the forecast period of 2026-2035. With record industrial fabrication demand driven by solar photovoltaics and electric vehicle proliferation, a structurally persistent global supply deficit compressing available inventory, rising investment demand from geopolitical and economic uncertainty, and expanding application diversity across electronics, pharmaceuticals, and antimicrobial technologies, the market is expected to reach USD 36.51 Billion by 2035.

According to Bloomberg, China imported roughly 836 tons of silver in March 2026, far above the 10-year seasonal average of 306 tons, fueled by surging retail investor appetite and robust solar manufacturing demand. As the world's largest silver consumer, this record intake underscores tightening global supply conditions and reinforces structural bullishness across the physical silver market.

As reported by Fortune, silver stabilised near $73 per ounce by late March 2026 after peaking above $121 in January, as markets repriced expectations to just one Federal Reserve rate cut this year. Despite the correction, persistent supply deficits and strong industrial demand from solar, AI data centres, and electronics continue to support silver's long-term market fundamentals.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Silver market is being defined by record industrial demand driven by the clean energy transition and AI infrastructure buildout, a persistent multi-year supply deficit putting upward pressure on prices, significant M&A activity reshaping the competitive landscape among major producers, and silver's increasing strategic importance as both a critical industrial input and a safe-haven investment asset.

The Silver Institute published its report titled "Silver, The Next Generation Metal" in December 2025, produced by Oxford Economics, providing a detailed five-year industrial demand forecast for silver across photovoltaics, electric vehicles, and AI-linked data center infrastructure. The report projects continued growth in silver's industrial applications through 2030, with solar PV, EV powertrain electrification, and data center power infrastructure identified as the three primary structural demand drivers. The findings reinforce silver's transition from a precious metal to a critical industrial commodity.

Vizsla Silver completed the closing of USD 300 million in convertible notes on November 24, 2025, providing more than double the capital required to construct its Panuco Project in Mexico. The low-cost financing, carrying a 5% coupon approximately 50% below conventional project finance rates, combined with approximately USD 200 million in pre-existing cash, gives Vizsla over USD 500 million in total financing capacity. The Panuco Project, targeting first silver production in H2 2027, offers a post-tax NPV of USD 1.137 billion and positions Vizsla as a significant new entrant in Mexico's silver production landscape.

Pan American Silver Corp. completed its acquisition of MAG Silver Corp. on September 4, 2025, in a transaction valued at approximately USD 2.1 billion comprising USD 500 million in cash and approximately 60.2 million Pan American shares. The deal adds a 44% joint venture stake in the high-grade Juanicipio silver mine in Zacatecas, Mexico, operated by Fresnillo plc, significantly expanding Pan American's silver reserve base, near-term cash flow generation, and long-term exploration optionality through the Larder and Deer Trail projects. The acquisition reinforces Pan American's position as one of the world's leading silver producers.

The Silver Institute released the World Silver Survey 2025 in April 2025, confirming that global silver industrial fabrication demand reached a new all-time high of 680.5 million ounces in 2024, marking the fourth consecutive year of record industrial consumption. The survey highlighted solar photovoltaics, electric vehicles, grid infrastructure, and AI-related electronics as the primary demand drivers. The report also confirmed a structural market deficit of 148.9 million ounces in 2024, the fourth consecutive year of demand exceeding supply, with the cumulative four-year deficit reaching approximately 678 million ounces.

First Majestic Silver's Santa Elena mine in Mexico produced a new annual record of 10.3 million silver equivalent ounces in 2024, representing a 7% increase compared to 2023. The milestone reflects the company's ongoing operational improvements at the mine and demonstrates the expanding production capabilities of mid-sized silver producers responding to elevated silver prices and sustained demand growth. First Majestic's performance at Santa Elena underlines Mexico's continued dominance as the world's largest silver-producing country, contributing approximately 23% of global silver output.

Silver's role in the clean energy economy has expanded significantly, with the metal now accounting for 59% of total global silver consumption through industrial applications, up from approximately 50% a decade ago. The solar photovoltaic sector alone consumed 197.6 million ounces in 2024, representing 19% of total global silver demand. EV powertrains, 5G infrastructure, and AI-related data centers are adding further structural demand layers that did not exist at meaningful scale even five years ago. According to the Silver Institute's World Silver Survey 2025, silver industrial demand reached 680.5 million ounces in 2024 for the fourth consecutive year of record consumption, a trajectory driven by the global economy's irreversible shift toward electrification, digital infrastructure, and renewable energy deployment.

The global silver market has recorded a supply deficit for the seventh consecutive year in 2025, with demand structurally outpacing mine production due to slow-responding byproduct supply, limited new primary silver project pipelines, and rapidly rising industrial consumption. Global silver mine output stood at approximately 819.7 million ounces in 2024, up less than 1% year-on-year, while analysts projected a market deficit of roughly 149 million ounces for 2025. Silver bullion gained 24.94% in the first half of 2025, following its 21.46% gain in 2024, with prices reaching an all-time high of $54.24 per ounce in October 2025. This price environment is encouraging exploration investment and project financing while simultaneously prompting thrifting efforts among solar panel manufacturers to reduce per-unit silver loading.

The silver mining sector is experiencing a wave of strategic consolidation, with major producers acquiring high-quality assets to strengthen reserve bases and cash flow profiles. Pan American Silver's USD 2.1 billion acquisition of MAG Silver, completed in September 2025, is the most significant transaction, adding the Juanicipio mine's world-class silver production to Pan American's portfolio. The silver market growth story is attracting both industry operators and financial investors, with new project financing vehicles also emerging. Vizsla Silver's USD 300 million convertible note financing in November 2025 reflects the improved availability of project finance capital for high-quality silver development projects in Mexico's established mining districts.

Beyond its well-established industrial and investment roles, silver is increasingly penetrating high-growth specialty segments including pharmaceuticals, water treatment, and personal care. Silver's antimicrobial properties are gaining clinical relevance as antibiotic resistance concerns grow globally, driving demand for silver-based wound dressings, medical coatings, and surface treatments in hospitals and healthcare facilities. The World Health Organization's warning that resistant infections could claim 10 million lives annually by 2050 is channeling research investment into silver-based solutions as an alternative pathway. In 2024, DuPont unveiled stretchable silver-based conductive inks for smart wearable applications, reflecting how silver innovation is simultaneously penetrating healthcare and next-generation consumer electronics.

The Expert Market Research's report titled "Silver Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

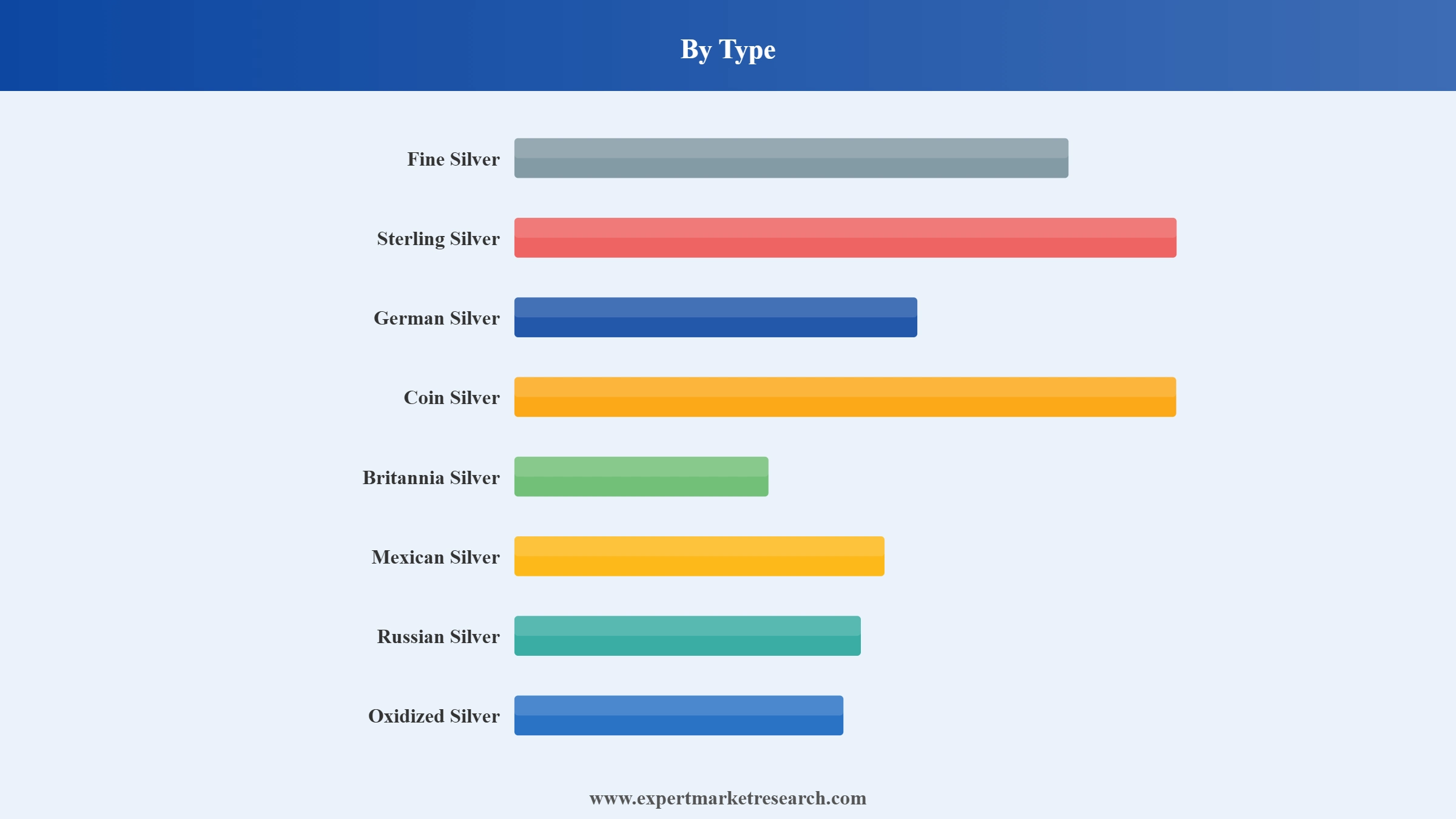

Market Breakup by Type

Key Insight: Fine silver commands the largest share by type in the global silver market, given its critical role in industrial applications, particularly photovoltaics, electronics, and pharmaceutical manufacturing where high-purity silver is a non-negotiable input. According to the U.S. Geological Survey, industrial-grade fine silver demand surged 13% in 2023, with solar and EV sectors providing the primary volume. Sterling silver maintains a strong second position, serving as the dominant material for jewelry and silverware across Western markets and growing premium jewelry consumption in India, China, and Southeast Asia. Oxidized silver is gaining traction in artisanal and fashion jewelry categories, particularly among younger consumers attracted to its distinctive aesthetic.

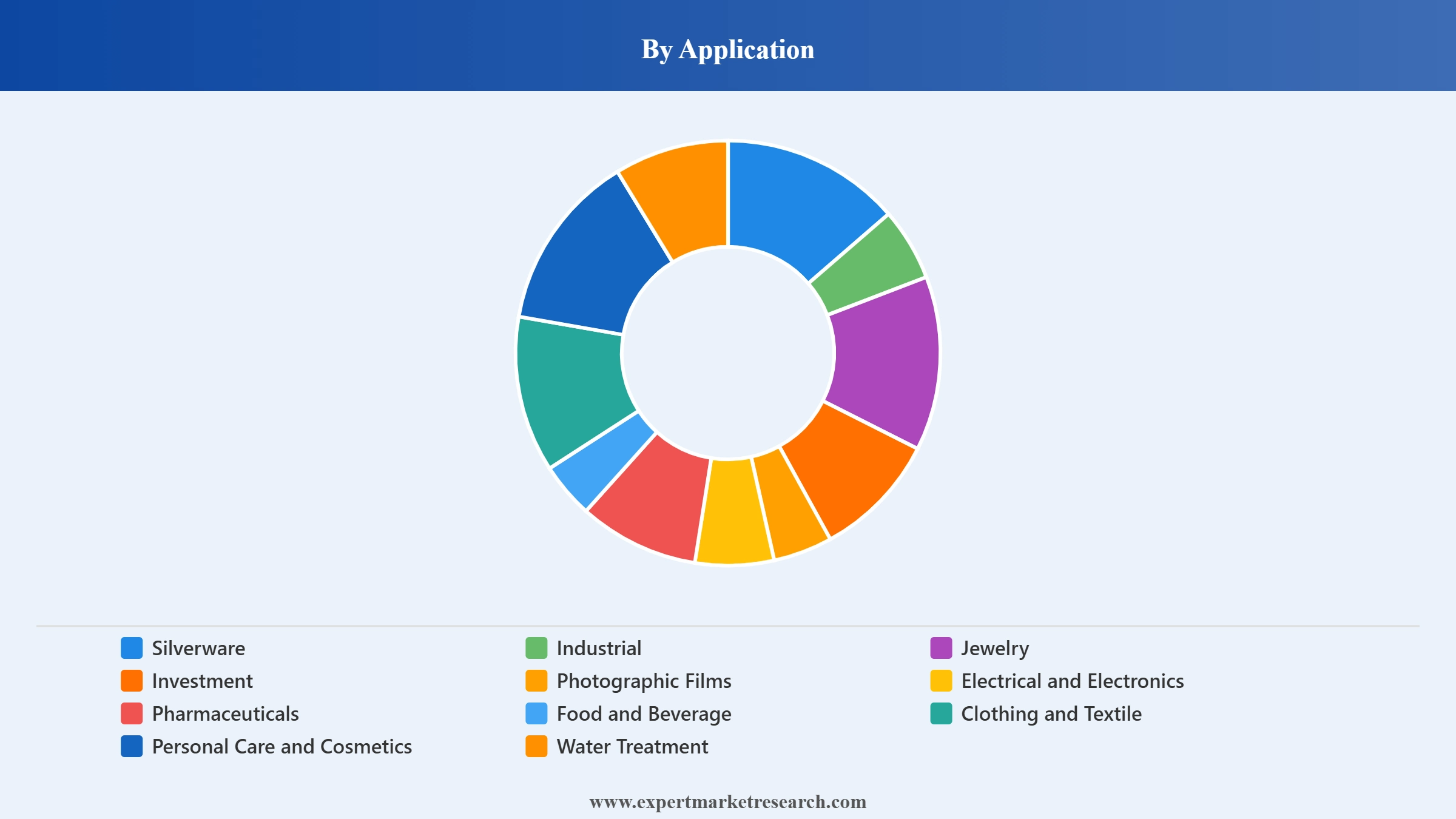

Market Breakup by Application

Key Insight: Industrial application is the dominant segment in the global silver market, representing approximately 59% of total silver consumption in 2024. Within industrial applications, electrical and electronics is the largest sub-segment, with solar photovoltaics accounting for 19% of total global silver demand in 2024 alone, up from just 5% in 2015. The automotive/EV sector, 5G infrastructure, and AI data center development are adding sustained structural demand layers. Jewelry remains the second-largest application by value, with silver jewelry fabrication growing 3% to 208.7 million ounces in 2024 according to the Silver Institute. Investment demand acts as a key price-influencing segment, with silver ETPs backed by physical silver creating additional demand while removing metal from industrial supply availability. Pharmaceutical applications are among the fastest-growing segments, driven by antimicrobial silver adoption in healthcare products.

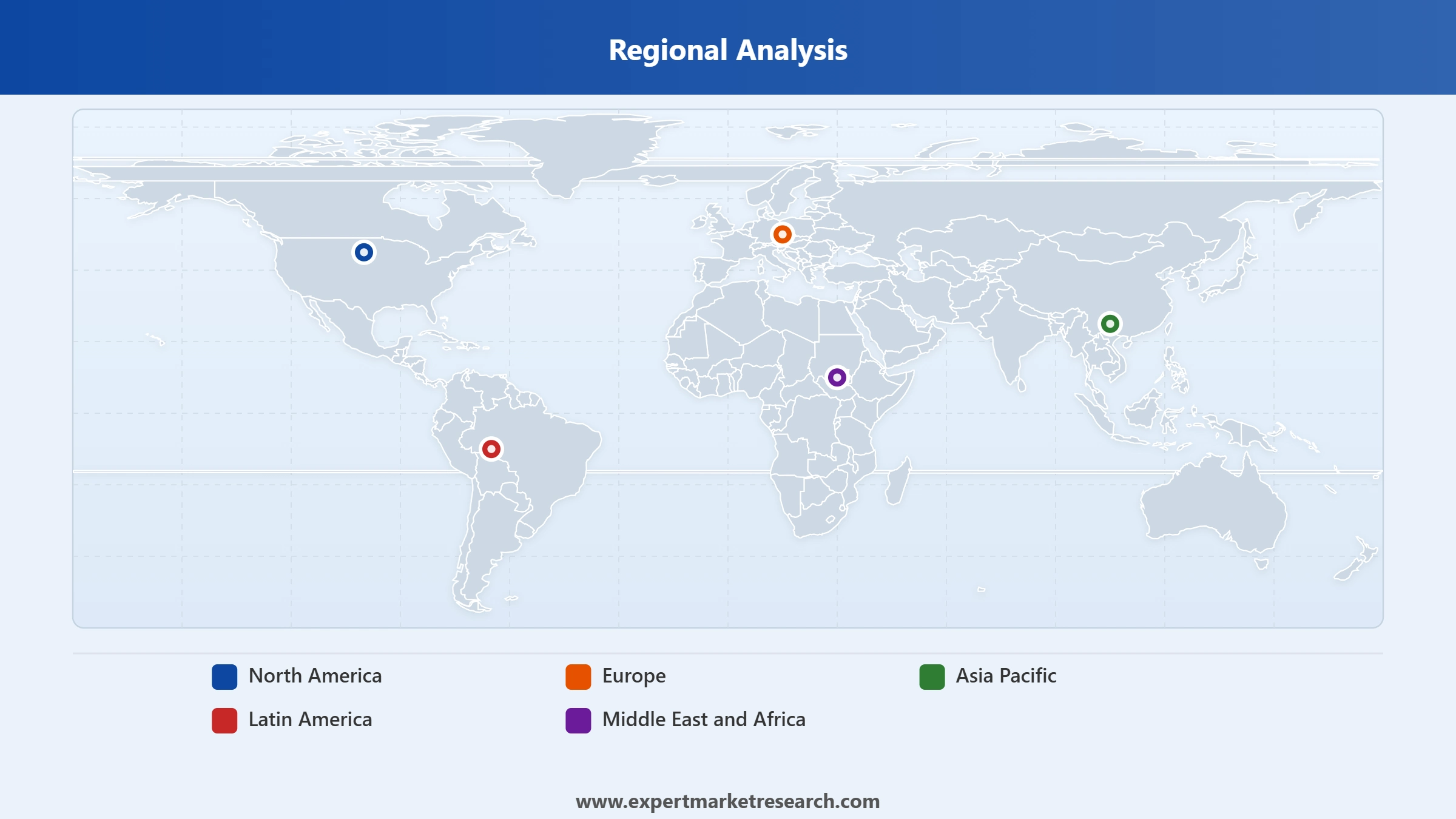

Market Breakup by Region

Key Insight: Asia Pacific leads global silver consumption, with China alone accounting for the largest share of industrial silver demand driven by its massive solar photovoltaic deployment, semiconductor manufacturing, and EV production. Taiwan, Japan, and South Korea contribute significantly through advanced electronics and chip fabrication. Latin America is the world's dominant silver-producing region, with Mexico, Peru, and Chile collectively supplying the majority of global mined silver output; Mexico alone contributes approximately 23% of global production. North America is a significant investment and industrial demand hub, with the United States driving substantial electronics and medical applications. Europe is engaged in silver recycling innovation, with EU Circular Economy Action Plan policies incentivizing silver recovery from e-waste.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Fine silver commands the largest share within the type segmentation, a position rooted in its indispensability across industrial manufacturing. The photovoltaic solar sector's exponential growth has been the most transformative demand factor for fine silver, with its share of total industrial silver demand jumping from just 11% in 2014 to 29% in 2024. This trajectory is expected to continue as global solar capacity additions accelerate toward the IEA's projected multi-terawatt deployment levels through 2035, even as manufacturers work to reduce silver loading per panel through thrifting and technology improvements. Taiwan's TSMC announced USD 100 billion in chip fabrication facilities that will use silver-based interconnects, further cementing fine silver's industrial dominance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Industrial application holds the dominant share of the application segmentation, and the electrical and electronics sub-segment is the largest and fastest-growing within it. Silver's unmatched electrical conductivity properties make it irreplaceable across smartphones, satellites, 5G antenna components, power grid infrastructure, and EV control systems. The World Silver Survey 2025 confirmed that electronics and electrical demand drove the bulk of industrial consumption growth in 2024, reinforcing the structural rather than cyclical nature of this demand. The solar photovoltaic sub-segment within industrial is notable for its pace of share gain, moving from a marginal consumer to representing nearly a fifth of all global silver demand within a decade.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific's dominance in the global silver market is structural, rooted in the region's role as both the world's largest industrial silver consumer and a significant center of downstream processing and manufacturing. China's solar photovoltaic program is the most consequential single driver: the National Energy Administration planned to add 160 GW of solar capacity in 2025 alone, each panel requiring silver paste as a conductive material. China's solar capacity growth of 45% in 2024 drove enormous volumes of silver paste demand, even as manufacturers actively worked to reduce grams per cell through thrifting. Beyond solar, China, Taiwan, South Korea, and Japan collectively dominate global semiconductor fabrication, consumer electronics manufacturing, and EV production, creating deep multi-sector industrial silver demand that is both large in volume and difficult to substitute.

Latin America's role in the silver market is fundamentally different from Asia Pacific's: it is the supply engine of the world. Mexico produces roughly 23% of global silver output, followed by Peru and Chile, with the region collectively hosting some of the world's highest-grade silver deposits. The Juanicipio mine in Zacatecas, Mexico, recently brought under Pan American Silver's portfolio through the September 2025 MAG Silver acquisition, exemplifies the world-class quality of assets in the region. Bolivia and Argentina add further production capacity, while exploration activity in Colombia, Brazil, and Ecuador is expanding the region's long-term production pipeline. However, Latin America faces recurring operational risks including geopolitical disruptions, licensing delays, and community engagement challenges that can interrupt production and introduce volatility into global silver supply chains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global silver market's competitive landscape is dominated by a handful of large, diversified mining companies that produce silver primarily as a byproduct of lead, zinc, copper, and gold mining, alongside a smaller group of pure-play primary silver producers. Fresnillo plc and Pan American Silver are the two largest dedicated silver producers by volume, each operating multiple mines across Mexico, Peru, and other Latin American countries. Glencore, through its massive diversified mining operations, contributes significant silver volumes as a byproduct of base metal production. The sector is undergoing consolidation as elevated silver prices create incentives for strategic acquisitions and merger activity.

Competition in the sector centers on reserve quality, all-in sustaining cost efficiency, geographic diversification across politically stable mining jurisdictions, and the ability to scale production to capture demand upside. Environmental, social, and governance considerations are increasingly important, as institutional investors and government regulators apply greater scrutiny to mining operations' environmental footprint and community relationships. New market entrants with advanced-stage development projects in Mexico and Peru are emerging as the next wave of producers, supported by project finance capital attracted by silver's dual industrial and investment demand dynamics.

Founded in 2008 and headquartered in London with operations primarily in Mexico, Fresnillo plc is the world's largest primary silver mining company by production volume. The company operates several major mines including Fresnillo, Saucito, and Ciénega, and holds a 56% joint venture stake in the Juanicipio mine alongside Pan American Silver. Fresnillo's strategic focus is on expanding production through brownfield development, extending mine lives through exploration, and maintaining cost discipline across its asset portfolio. The company's Mexican operations benefit from established infrastructure, skilled workforce availability, and proximity to global refinery and logistics networks.

Founded in 1994 and headquartered in Vancouver, Canada, Pan American Silver is one of the world's largest primary silver and gold producers, operating mines across Canada, Mexico, Peru, Brazil, Bolivia, Chile, and Argentina. The September 2025 acquisition of MAG Silver added a 44% joint venture interest in the Juanicipio mine in Mexico, significantly expanding Pan American's silver reserve base and near-term cash flow generation. The company's diversified multi-country asset base provides geographic risk mitigation, and its strong balance sheet, including USD 923 million in cash and investments prior to the acquisition, demonstrates financial resilience and strategic flexibility.

Founded in 1974 and headquartered in Baar, Switzerland, Glencore is one of the world's largest diversified natural resource companies, producing silver as a significant byproduct of its base metal mining operations across copper, zinc, and lead mines in Australia, the Americas, and Africa. Glencore's scale, global logistics infrastructure, and trading expertise give it a structural competitive advantage in moving silver from mine to market efficiently. The company is a major supplier to industrial customers globally and benefits from cost advantages inherent in byproduct silver production where silver revenues offset base metal mining costs.

Founded in 2002 and headquartered in Vancouver, Canada, First Majestic Silver is a pure-play primary silver producer with operations concentrated in Mexico. The company's Santa Elena mine produced a record 10.3 million silver equivalent ounces in 2024, a 7% year-on-year increase, reflecting operational improvements and favorable silver pricing. First Majestic focuses on maximizing silver recoveries, maintaining low all-in sustaining costs, and expanding production through mine development and strategic acquisitions. Its pure-play positioning gives investors direct exposure to silver price movements with minimal dilution from gold or base metal production.

Other key players in the market are Polymetal International plc, Coeur Mining, Inc., Hecla Mining Company, Hochschild Mining PLC, Southern Copper Corporation's, Compania de Minas Buenaventura SAA, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Navigate the rapidly evolving silver market with confidence using our comprehensive Silver Market report for 2026 to 2035. Whether you are a mining company evaluating asset strategy, an industrial manufacturer planning procurement, a financial investor building commodity exposure, or a technology company assessing critical input supply, this report provides the data-driven intelligence you need. From industrial demand forecasts across PV solar and EV applications to competitive profiling across 10 leading producers and country-level analysis across five regions, it covers everything. Download your free sample today and gain the edge in understanding what drives the global silver market.

Silver Recycling and Secondary Supply Market

Silver Mining Industry Overview

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the silver market reached an approximate value of USD 23.51 Billion.

The market is projected to grow at a CAGR of 4.50% between 2026 and 2035.

The key players in the market include Fresnillo plc, Pan American Silver Corp., Polymetal International plc, Glencore plc, Coeur Mining, Inc., Hecla Mining Company, Hochschild Mining PLC, First Majestic Silver Corp., Southern Copper Corporation’s, and Compania de Minas Buenaventura SAA, among others.

Key strategies driving the market include focusing on tech-integrated silver, scaling recycling infrastructure, partnering with solar firms, and diversifying supply chains.

The different types considered in the market report are fine silver, sterling silver, German silver, coin silver, Britannia silver, Mexican silver, Russian silver, oxidized silver, and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.