Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

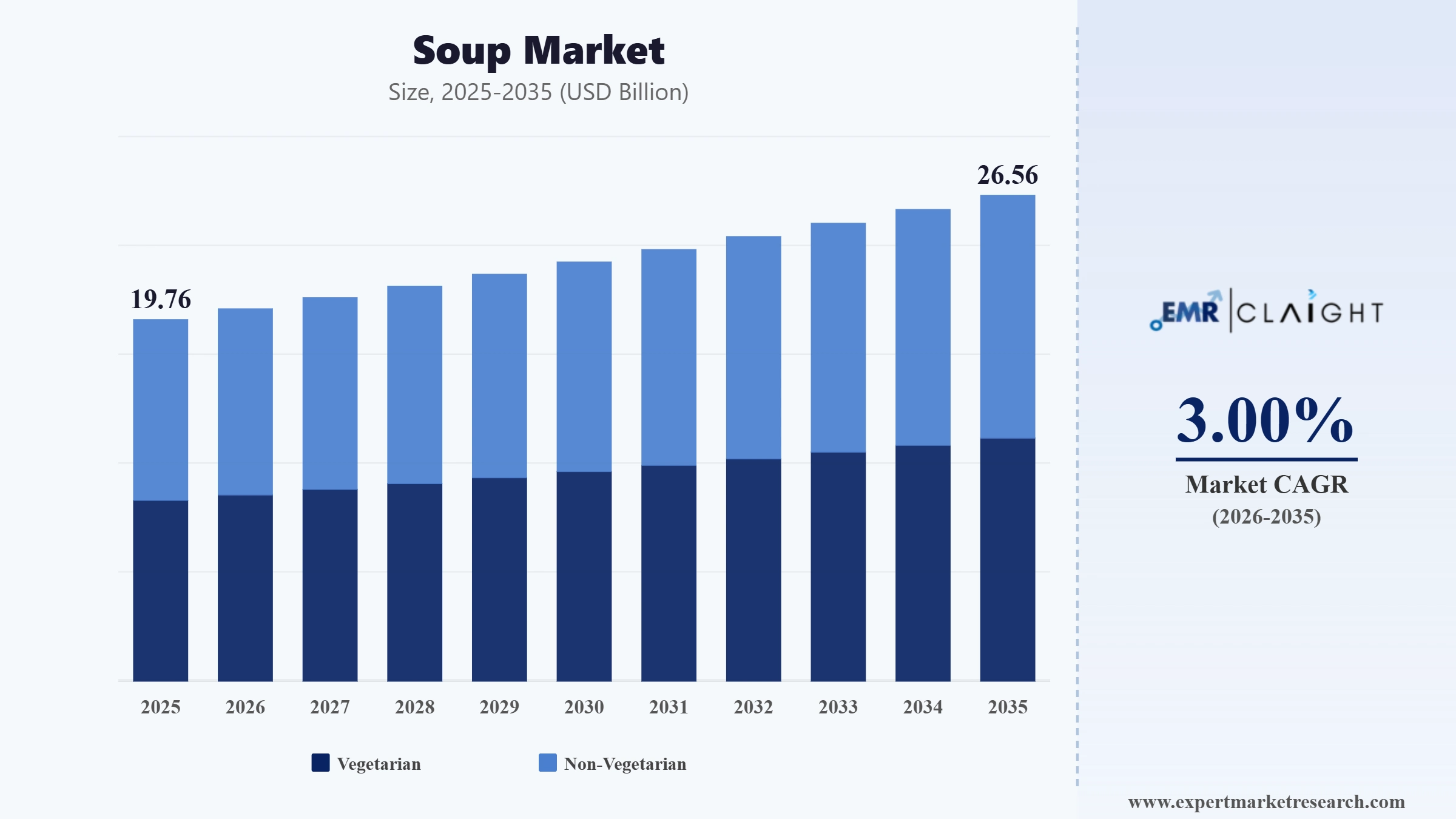

The global soup market size attained a value of USD 19.76 Billion in 2025. The market is further expected to grow in the forecast period of 2026-2035 at a CAGR of 3.00% to reach USD 26.56 Billion by 2035.

According to Yahoo Finance, The Campbell's Company closed at $20.94 on April 16, 2026, with the market capitalisation at $6.243 billion and trailing 12-month revenue of roughly $10 billion. The stock has fallen in six of the last ten sessions, reflecting investor concerns over condensed and ready-to-serve soup weakness, tariff-driven input costs, and slower category recovery heading into the June earnings release.

According to The Campbell's Company, second-quarter fiscal 2026 results released on March 11, 2026 showed US soup sales decreased 4%, pressured by condensed soups, ready-to-serve soups, and broth. CEO Mick Beekhuizen cited storm-related shipment delays and tariffs, while the Rao's brand surpassed $1 billion in trailing 12-month sales, underscoring a widening gap between premium pasta-sauce growth and traditional canned soup performance.

Soup is a liquid food mostly prepared by cooking vegetables, fish, legumes, and meat, among others, with seasoning in water, milk, or any liquid medium. Soups are often slow-cooked and retain the nutrition of their ingredients. They are also commonly consumed during illnesses as the consumption of soups accounts for various health benefits. They can promote digestion, enhance heart function, aid in weight loss, and strengthen bones.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Soup Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 19.76 |

| Market Size 2035 | USD Billion | 26.56 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 3.5% |

| CAGR 2026-2035 - Market by Country | India | 3.6% |

| CAGR 2026-2035 - Market by Country | China | 3.4% |

| CAGR 2026-2035 - Market by Category | Vegetarian | 3.3% |

| CAGR 2026-2035 - Market by Product | Liquid | 3.8% |

| Market Share by Country 2025 | Mexico | 1.9% |

The increasing demand for instant soup with additional nutrition, which can serve as an appetiser or as a complementary side dish to proper heavy meals, is contributing to the soup market growth. Instant dry soup mixes loaded with vegetables and nutritional combinations, such as creamy potato, broccoli cheddar, pea, scallion, ginger, and mushroom, among others, are gaining traction among the working population, augmenting the market share. Meanwhile, soups can also serve as a source of rich nutrition for school/college students or those living alone who are facing the problem of the inaccessibility of healthy snacks. In this regard, the convenience and nutritional benefits offered to consumers far from home through soup are likely to expand the share of the instant soup market.

Meanwhile, the demand for organic soups is likely to witness a spike in the forecast period, because of the medicinal properties and rich flavours of organic soups. Innovative organic soup recipes such as green vegetables with wakame seaweed and thongweed soup and organic pumpkin with quinoa and kombu seaweed soup are rich in vitamins and minerals and can be beneficial for those suffering from high blood pressure and their demand can increase the overall organic soup market revenue.Over the forecast period, the anticipated increase in the prevalence of chronic blood pressure-related disorders, dementia, and metabolic syndromes, among others, coupled with the increasing accessibility of organic soups via the e-commerce channel also boosts the demand for organic soup. At a regional level, in North America, the U.S. soup market accounts for a decent portion of the market share.

The Expert Market Research’s report titled “Soup Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

The major categories of soup are:

The demand for vegetarian soup in the market has been growing, influenced by several factors that reflect changing consumer preferences and broader food sector trends. Increasing awareness of health and wellness has led many consumers to seek out healthier food options. Vegetarian soups, often low in calories and high in nutrients, align well with this trend.

There is a growing shift towards vegetarian and vegan lifestyles, driven by health reasons, ethical concerns about animal welfare, and environmental considerations. This shift has directly increased the demand for vegetarian and plant-based food products, including soups. The busy lifestyles of modern consumers have also heightened the demand for convenient meal options. Vegetarian soups, especially ready-to-eat or easy-to-prepare varieties, offer a quick and healthy meal solution.

The market is broadly divided on the basis of product into:

The demand for dried soup in the market has been influenced by various factors, reflecting consumer preferences, lifestyle changes, and industry vertical trends. Dried soup, known for its convenience and shelf stability, accounts for a substantial soup market share.

One of the primary drivers for the demand for dried soup is its convenience. Dried soups are easy to store, have a long shelf life, and can be prepared quickly, making them an ideal choice for busy lifestyles. They are particularly popular among working individuals, students, and people with limited time for cooking. These soups are available in a wide range of flavours and types, including traditional recipes and exotic, international cuisines. This variety caters to diverse taste preferences and encourages consumer experimentation.

Based on the packaging type, the market is segmented into:

The demand for pouched packaging in the market has been growing, influenced by several factors that align with broader trends in consumer preferences, convenience, and sustainability. Pouched packaging, often used for ready-to-eat and easy-to-prepare soups, offers several advantages that have contributed to its increasing popularity.

Pouched soups are easy to store, handle, and prepare, making them a convenient choice for consumers with busy lifestyles. The packaging often allows for direct heating (like microwaveable pouches), simplifying the preparation process and reducing the need for additional cooking utensils. Furthermore, the lightweight and compact nature of pouched soups makes them ideal for on-the-go consumption, work lunches, camping, and travel.

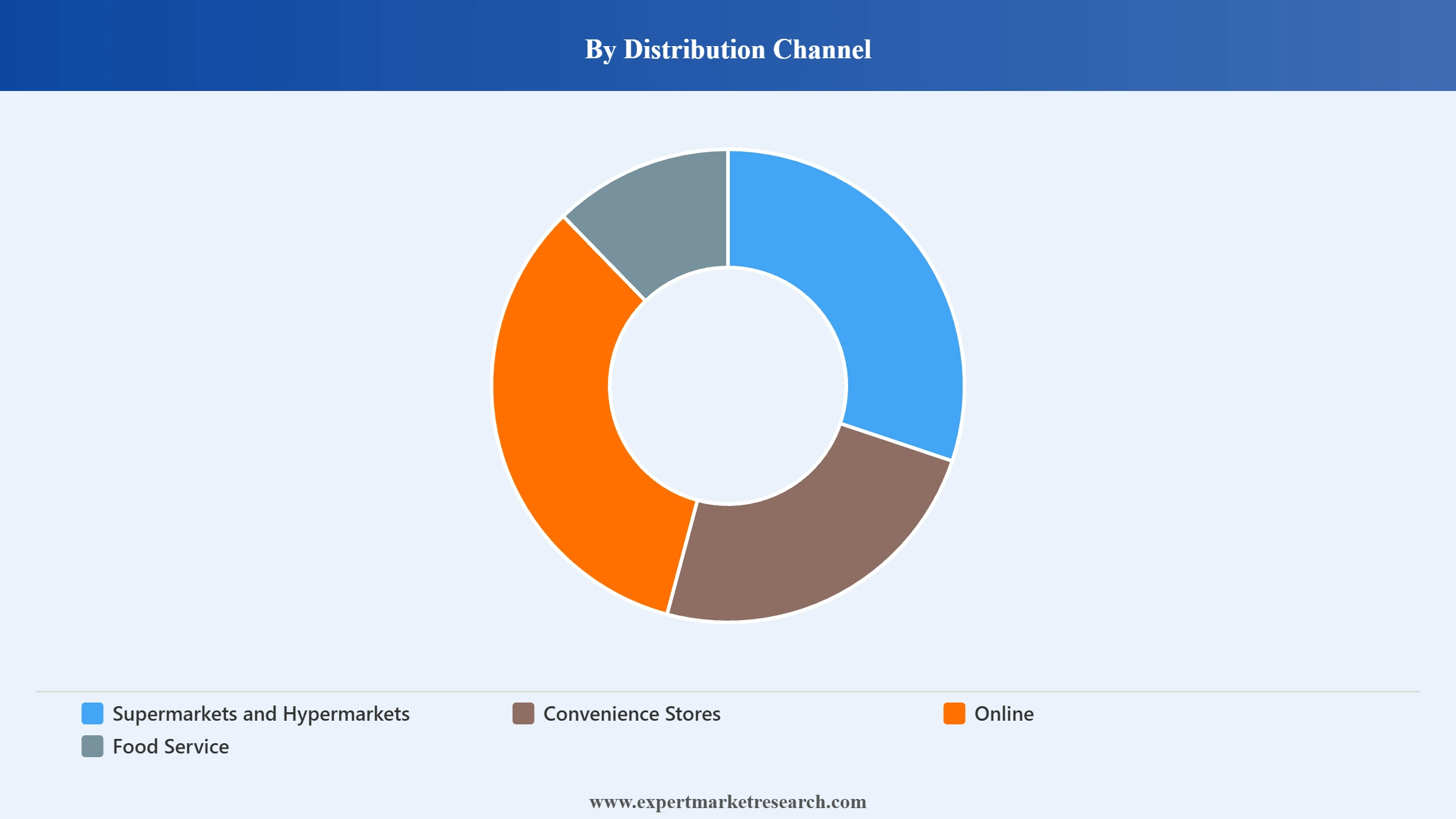

By distribution channel, the market is divided into:

The supermarkets and hypermarkets segment plays a pivotal role in the market, serving as one of the primary distribution channels for soup products. These stores offer a vast array of soup products, ranging from traditional canned soups to more contemporary options like organic, gluten-free, and exotic international flavours. This wide selection caters to diverse consumer preferences and dietary needs, making these retail formats popular shopping destinations.

These stores are typically easily accessible to a large segment of the population, making them a convenient choice for regular grocery shopping. They also often offer competitive pricing and frequent promotions, such as discounts, buy-one-get-one-free offers, and loyalty programs, which can significantly influence consumer purchasing decisions.

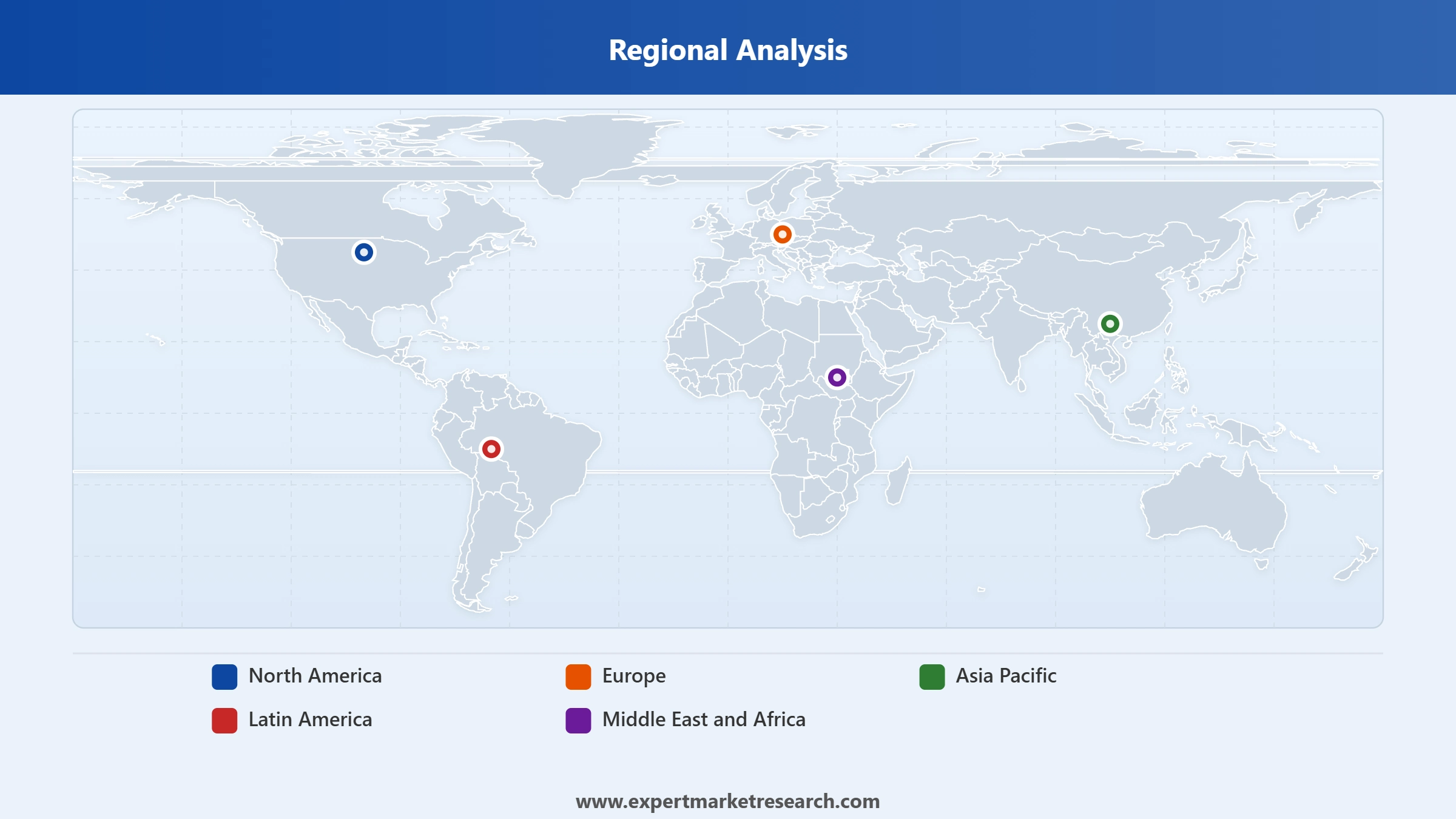

The report also covers the regional markets for soup, which are as follows:

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Increasing Health Consciousness

The increasing health consciousness of consumers and healthy eating trends have led to a surge in the soup market demand, especially during the winter seasons. Soups offer a combination of both nutrition and taste without adding many calories. The increasing demand for wellness products also makes soup an obvious choice and aids market growth. The introduction of gluten-free and organic variants has enhanced the product demand. As the emphasis on sustainability flourishes, eco-friendly soup packaging with nutritional information offered by several brands is also accelerating the growth of the market. As soups offer numerous vegan choices as well, they are popular among the vegan population, which has witnessed a significant rise in the past few years.

Increasing product launches, product offerings, emphasis on advertisement, and several new trends such as energy soups and functional soups are catalysing the market growth. Energy soups, usually drunk cold, are packaged in ready-to-drink bottles with a variety of ingredients, such as sweet potato and mango. Soup is an ideal platform for inculcating various functional ingredients as it is easier to incorporate numerous nutritious foods, such as ginger, beans, soy, and a wide range of vegetables into one soup, and as a result, is contributes to the overall growth of the soup market.

Rising Demand for Healthy Convenience Food

The demand for convenience food owing to urbanisation is a significant driver for the growth of the soups market. The increasing working population and hectic lifestyles have increased the demand for healthy convenience foods and are escalating the sale of pouched soups, which is a strong soups market segment. Increasing disposable income and the rising living standards of the urban middle-class population is increasing the demand for easy ready-to-eat foods. Soups are famous not only as a healthy and nutritious alternative but also as comfort food which is usually delicious and satisfying.

Moreover, globalised culinary practices offer a diverse variety of soups to choose from, which is propelling the market growth. As the popularity of Asian-inspired food is soaring, the popularity of ethnic soups such as Vietnamese Pho soups is also significantly increasing. In various South Asian and developing countries, soups are also considered a representative of modernity and Westernisation. The rising popularity of frozen food, especially in North America and Europe, due to its various advantages is further accelerating the growth of frozen and refrigerated foods, consequently boosting the market growth of soup.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The growth of distributional channels is a critical aspect of the market, as shown by the market research. The robust development of supermarkets, superstores, and convenience stores around the world is one of the crucial soup market trends. Online retail shopping has considerably increased in the past few years. Expansion of instant delivery service platforms and surge in the purchasing power of consumers are also key trends in 2023 as they have boosted the demand for ready-to-eat soup. As soups are also considered immunity boosters, they are witnessing healthy demand among health-conscious consumers.

As per the soup market analysis, the North America accounts for a substantial market share. The regional market features a wide range of soup products, including canned soups, dried soups, broth, and fresh or chilled soups. It is dominated by a few major brands, but there is also a presence of smaller, niche players offering speciality or gourmet soups.

There is a growing preference for healthy and organic soup options among North American consumers. This includes low-sodium, low-calorie, and nutrient-rich soups, as well as those made with organic and non-GMO ingredients. Ethnic and exotic flavours are also gaining popularity, reflecting the diverse cultural influences in the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The report presents a detailed analysis of the following key players in the global soup market, looking into their capacity, market shares, and latest developments like capacity expansions, plant turnarounds, and mergers and acquisitions:

The comprehensive report looks into the macro and micro aspects of the market. The EMR report gives an in-depth insight into the market by providing a SWOT analysis as well as an analysis of Porter’s Five Forces model.

Frozen Meals Industry Demand And Growth

Ready To Eat Meals Market Growth And Insights

Packaged Broth Industry Trends And Outlook

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The soup market reached a value of USD 19.76 Billion in 2025.

The market is estimated to grow at a CAGR of 3.00% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of USD 26.56 Billion by 2035.

The rapid transition towards healthy and nutrition rich drinks, growing demand for convenience and ready-to-cook food products, and increasing awareness about the benefits of soup are the major drivers of the market.

The key trends in the market include the expanding online-retail sector fuelling the sale of clean-labelled soup pouches, innovations in packaging, and increasing demand from students and working population.

Vegetarian and non-vegetarian are the different categories of soup in the market.

Liquid, dried, and frozen, among others, are the various products in the market.

Yes, soups are generally considered to be healthy as they can contain nutrition of various vegetables, proteins, meat products, and culinary spices.

The packaging types of soup in the market are bottled, canned, and pouched, among others.

Campbell Soup Company, The Kraft Heinz Company, Unilever PLC, General Mills Inc., Conagra Brands Inc., B&G Foods, Inc., Nestlé S.A., Baxters Food Group, The Hain Celestial Group, Inc., and Associated British Foods Plc, among others, are the key players in the global soup market, according to the report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Category |

|

| Breakup by Product |

|

| Breakup by Packaging Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.