Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

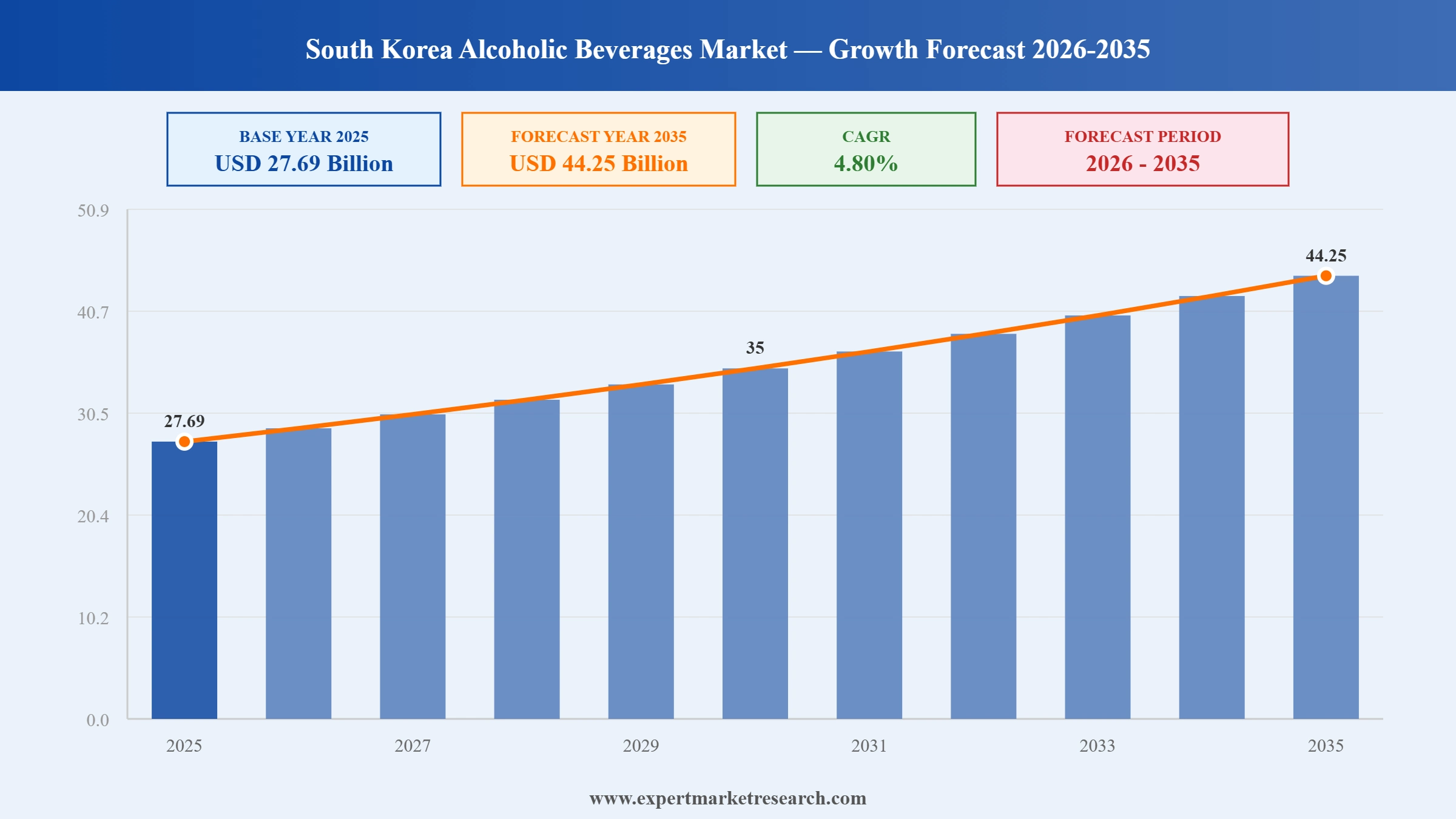

The South Korea alcoholic beverages market reached a value of USD 27.69 Billion at 2025 and is projected to expand at a CAGR of around 4.80% during the forecast period of 2026-2035. Underpinned by South Korea's vibrant on-trade drinking culture, accelerating premiumisation across imported spirits and wine, ongoing product innovation in soju and beer, and growing consumer appetite for low-alcohol and craft alternatives, the market is expected to reach USD 44.25 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea alcoholic beverages market is undergoing meaningful structural evolution, as the traditional dominance of soju and domestic beer is now layered with accelerating premiumisation, expanding craft category experimentation, and a clear shift toward health-conscious, lower-alcohol product portfolios. Global beverage players are deepening their South Korean footprint while domestic producers respond with rapid innovation cycles designed to capture younger and experience-oriented consumers. These interacting trends are collectively reshaping competitive dynamics, distribution priorities, and category growth rates across the entire market.

HiteJinro launched Terra Zero, an alcohol-free beer, on March 19, 2026, alongside a limited-edition flavoured soju combining chocolate and pistachio notes targeting university-aged consumers. The back-to-back releases reflect HiteJinro's strategic pivot toward low-ABV and experiential products for health-conscious demographics.

Oriental Brewery launched Kas All Zero in August 2025, positioning it as a beer simultaneously alcohol-free, sugar-free, calorie-free, and gluten-free. The product addresses the growing health-conscious segment in the South Korea alcoholic beverages market seeking guilt-free on-trade and retail beverage options.

Barrell Craft Spirits officially entered the South Korea alcoholic beverages market in May 2024, with UOT appointed as its on- and off-trade distributor. The launch reflects growing South Korean consumer demand for premium imported craft spirits beyond mainstream whiskey and vodka categories.

Jeju Beer Co., South Korea's leading craft beer maker, sold a controlling stake from its founding family to a domestic buyer in March 2024. The deal highlighted growing M&A activity and consolidation reshaping South Korea's craft beer landscape amid shifting consumer preferences.

Premiumisation is reshaping the South Korea alcoholic beverages market as consumers trade up to imported spirits and wines. Rising incomes have boosted premium whiskey and wine demand, with global players like Diageo and Pernod Ricard expanding South Korean market presence.

Soju dominates the South Korea alcoholic beverages market, commanding the largest volume share through HiteJinro's Chamisul and Lotte Chilsung's Chum Churum. Product innovation including zero-sugar variants and fruit-flavoured expressions launched in 2024 is broadening soju's appeal among younger health-conscious consumers.

Low-ABV and alcohol-free products are gaining traction in South Korea's alcoholic beverages market. HiteJinro launched Terra Zero alcohol-free beer in March 2026, while Oriental Brewery's Kas All Zero in August 2025 targeted consumers seeking zero-sugar, zero-calorie, and gluten-free beverage options.

Convenience stores are a key channel in the South Korea alcoholic beverages market, driving impulse purchases of soju, beer, and RTD highballs across the country's dense retail network. The channel reflects South Korea's vibrant social culture and late-night consumption habits.

Flavoured alcoholic beverages are among the fastest-growing categories in the South Korea alcoholic beverages market, with annual launches rising from 2 in 2020 to 78 in 2024. This fivefold growth reflects demand for sweeter, lower-ABV options among younger Korean drinkers.

The report of Expert Market Research's titled "South Korea Alcoholic Beverages Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

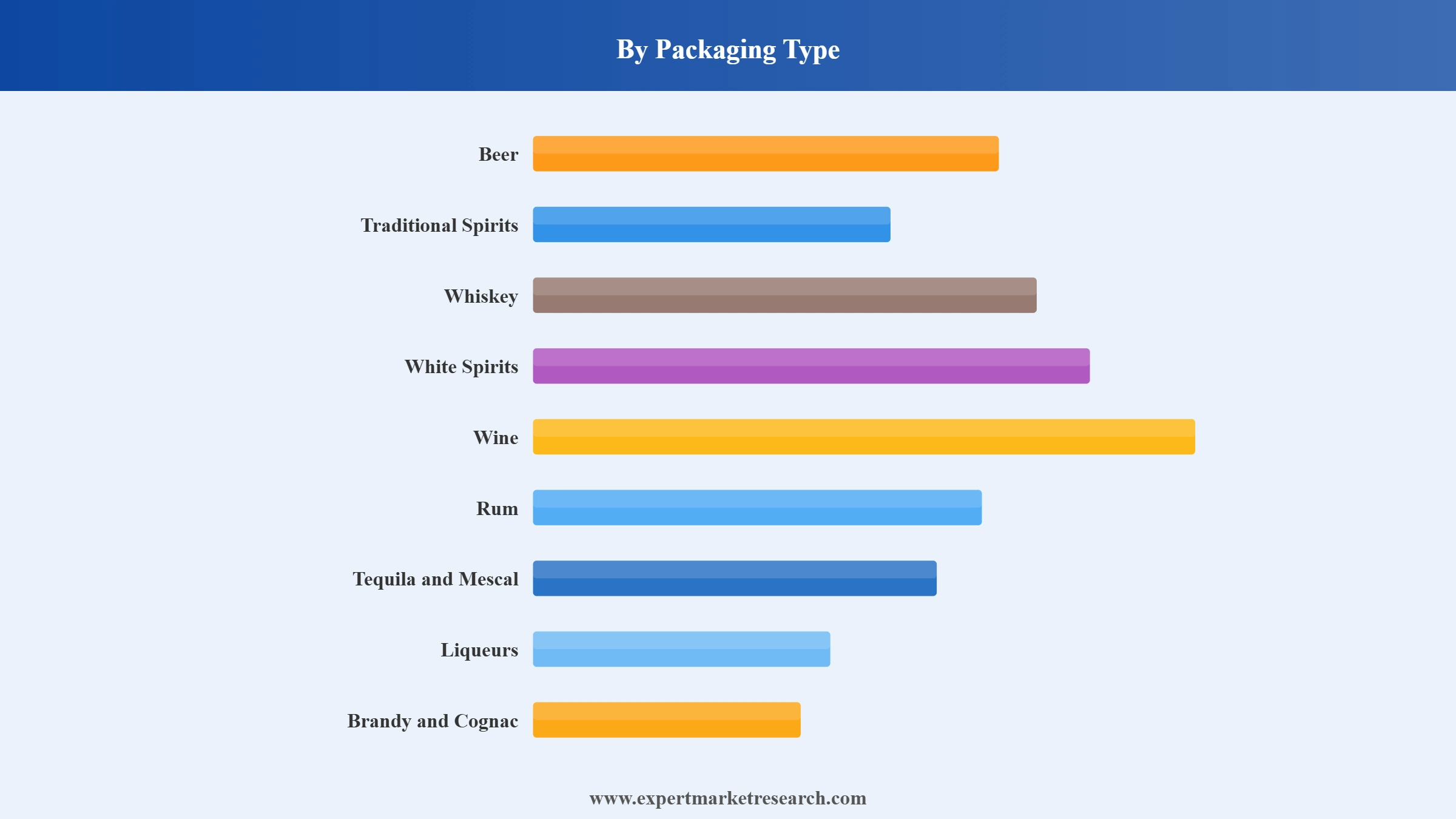

Market Breakup by Packaging Type

Key Insight: Traditional spirits, led by soju, dominate the South Korea alcoholic beverages market by volume, anchored by iconic brands such as HiteJinro's Chamisul and Lotte Chilsung's Chum Churum. Soju's cultural embeddedness, affordability, and universal on-trade and retail availability cement its position as the defining product of South Korean drinking culture. Beer holds the second-largest category share, with domestic mass-market lagers like Terra, Cass, Hite, and Kloud competing alongside a growing craft movement. Within beer, the bottle format holds the larger share while cans are gaining traction through convenience store and outdoor consumption trends. Whiskey is the fastest-growing premium sub-segment, fuelled by South Korean highball culture, while wine is growing steadily as dining habits evolve and import access broadens.

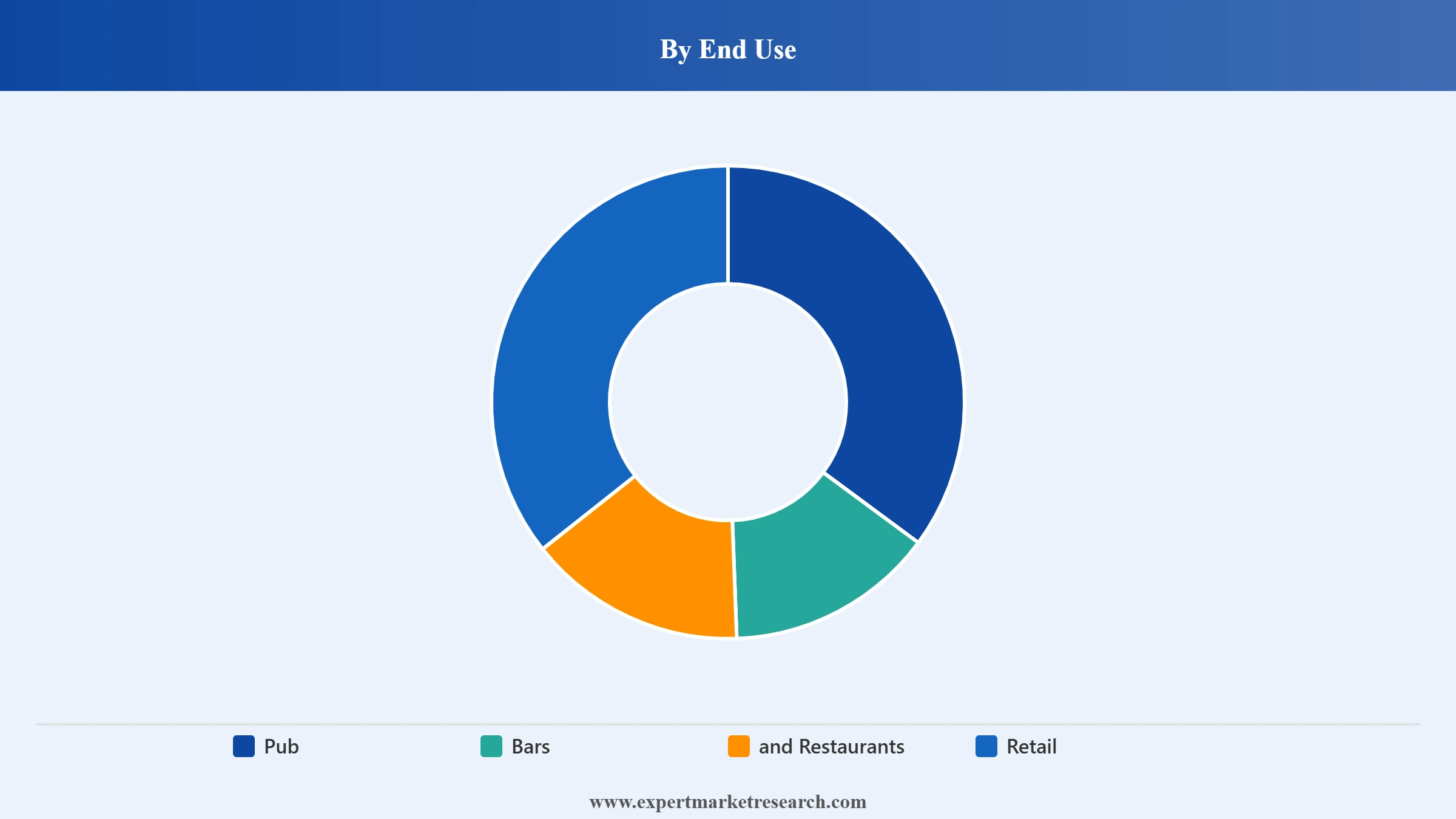

Market Breakup by End Use

Key Insight: Pub, bars, and restaurants account for approximately 65% of the South Korea alcoholic beverages market, reflecting the deeply embedded on-trade drinking culture that makes alcohol central to business dinners, social gatherings, and everyday Korean dining occasions. Korean barbecue restaurants, pojangmacha street stalls, and norebang entertainment venues are the primary on-trade demand drivers, generating consistent high-volume consumption of soju and beer. The retail segment is growing steadily, powered by a dense convenience store network and expanding home consumption, with RTD products and canned formats gaining particular traction for off-premise occasions.

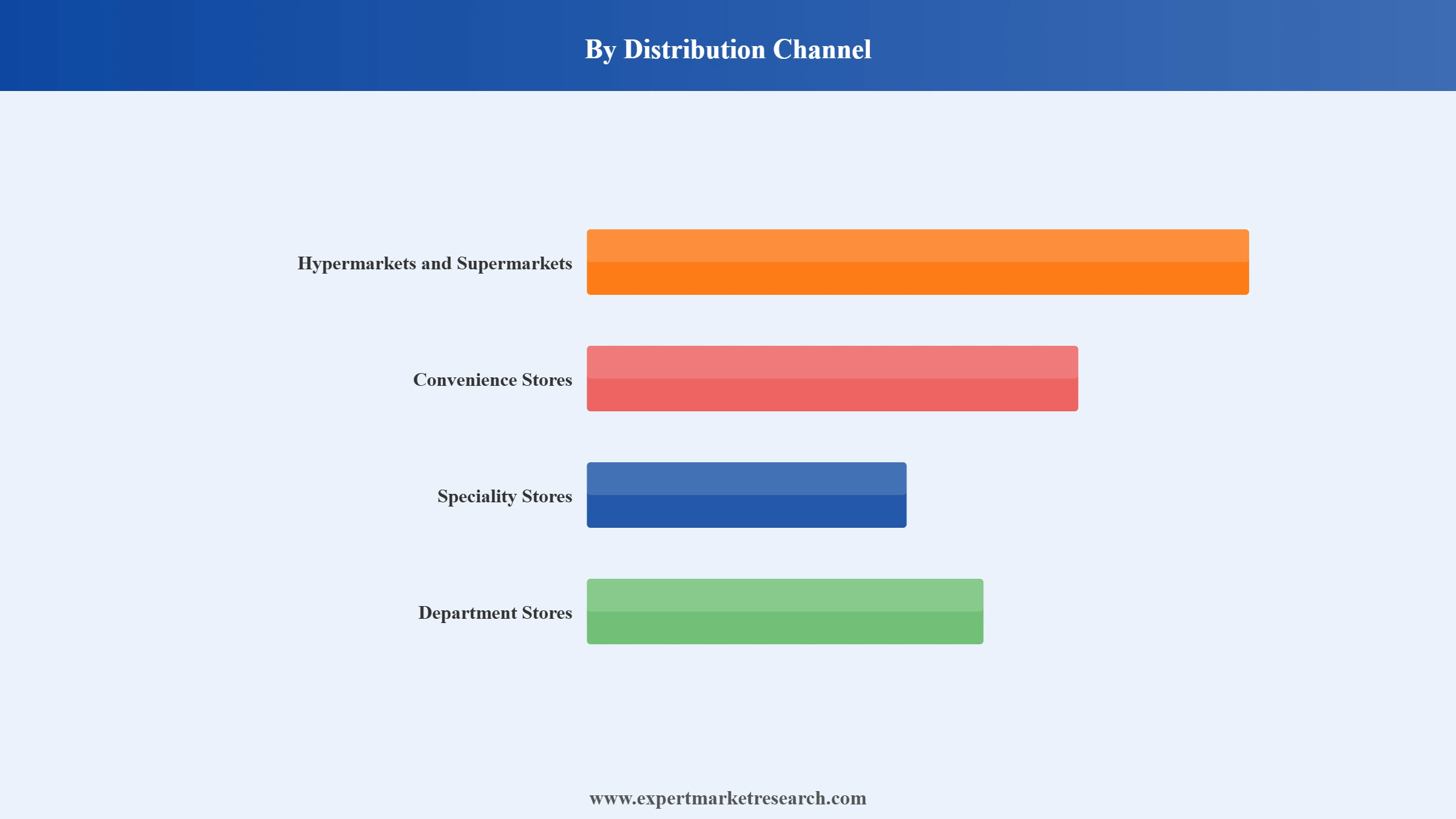

Market Breakup by Distribution Channel

Key Insight: Hypermarkets and supermarkets hold the leading off-trade distribution share in the South Korea alcoholic beverages market, offering consumers the widest product range across domestic and imported categories at competitive prices. Major retail chains such as E-Mart, Lotte Mart, and Homeplus serve as primary purchase destinations for planned household alcohol buying. Convenience stores are the fastest-growing channel, capitalising on South Korea's uniquely high store density and 24-hour operating model to capture impulse and late-night purchases across soju, beer, and ready-to-drink formats. Speciality stores are gaining relevance for premium wine, whiskey, and craft beer, catering to discerning consumers seeking curated selections and knowledgeable retail experiences.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Packaging Type, traditional spirits dominate the market due to soju's deeply embedded cultural significance, affordable price positioning, and universal availability across on-trade and retail channels in South Korea

Traditional spirits, driven by soju, command the largest share of the South Korea alcoholic beverages market by volume, with HiteJinro's Chamisul and Lotte Chilsung's Chum Churum holding the two dominant brand positions. Soju's deep cultural significance in Korean social life, spanning business dinners, family occasions, and everyday relaxation, makes it uniquely resistant to category disruption and sustains predictable high-volume consumption year-round. Makgeolli, the traditional rice wine, is also experiencing renewed interest, particularly among younger consumers drawn to its authentic Korean credentials and perceived wellness associations.

Beer holds the second-largest share of the South Korea alcoholic beverages market, underpinned by mass-market domestic lagers including Cass, Terra, Hite, and Kloud. OB's Cass commands the leading domestic beer position by volume, while HiteJinro's Terra has built significant market share since its 2019 launch through aggressive marketing. The craft beer segment, while smaller in volume, drives premiumisation within the category, with Jeju Beer and a growing network of urban microbreweries attracting younger, flavour-conscious consumers. Whiskey is the standout growth segment, with South Korea's highball culture and growing preference for blended and single malt Scotch driving both on-trade and off-trade volume expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, pub, bars, and restaurants account for the dominant share of the market due to South Korea's strong on-trade drinking culture and the central role of alcohol in social dining and entertainment occasions

Pub, bars, and restaurants dominate the South Korea alcoholic beverages market end-use landscape, accounting for approximately 65% of total consumption. The social norm of combining food and alcohol at shared dining tables makes on-trade venues the primary consumption channel for soju, beer, and increasingly, premium whiskey highballs. Korean barbecue restaurants, where soju and beer are ordered as standard accompaniments, function as the single most consistent volume driver in the market, supported by the dense urban restaurant density in Seoul, Busan, and other metropolitan centres.

The retail segment is gaining share within the South Korea alcoholic beverages market, driven by home consumption trends and the expanding convenience store channel. Retail alcohol purchases through CU, GS25, and 7-Eleven convenience stores reflect the uniquely spontaneous purchase behaviour of South Korean urban consumers, who frequently buy soju, beer, and RTD products for immediate consumption. The premiumisation trend is also entering retail through wine and imported spirits sections in department stores and speciality retailers, where consumers can explore a curated range of products not typically found in mainstream supermarket aisles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, hypermarkets and supermarkets account for the dominant off-trade share of the market due to their broad product assortment, competitive pricing, and established consumer preference for planned alcoholic beverage purchases

Hypermarkets and supermarkets hold the leading distribution channel position within the South Korea alcoholic beverages market's retail segment, providing comprehensive product assortments spanning domestic soju, beer, imported wine, whiskey, and spirits at competitive price points. Large-format retailers including E-Mart, Lotte Mart, and Homeplus serve as anchor destinations for household alcohol purchases, particularly for special occasions and social gatherings. Their shelf space allocations accommodate both mass-market and premium imported products, enabling consumer exploration of wider beverage categories within a single shopping trip.

Convenience stores are the fastest-growing distribution channel in the South Korea alcoholic beverages market, leveraging South Korea's world-leading store density per capita to drive 24-hour impulse purchases across all key categories. The convenience format has become particularly important for RTD soju cocktails, canned beer, and flavoured alcoholic beverages, which are compact, single-serve, and aligned with the on-the-go consumption behaviour of younger urban demographics. Speciality stores are gaining ground in the premium segment, particularly for imported wine and whiskey, where knowledgeable staff and curated selections provide a differentiated retail experience that attracts discerning consumers willing to pay higher price premiums.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea alcoholic beverages market is moderately concentrated at the domestic production level, with HiteJinro, Oriental Brewery, and Lotte Chilsung commanding dominant positions in the soju and beer segments through established brand equity, deep distribution infrastructure, and significant production scale. The top five market participants account for approximately 75% of total volume, reflecting the consolidating effect of scale, cultural relevance, and decades of consumer relationship-building. The premium and imported segments are considerably more fragmented, with global players including AB InBev, Heineken, Diageo, Pernod Ricard, Carlsberg, and Beam Suntory pursuing OEM partnerships, targeted marketing, and product localisation strategies to capture growing demand.

Competitive dynamics are increasingly shaped by the no-and-low alcohol movement, with domestic leaders investing in alcohol-free beer and zero-sugar soju to retain younger, health-conscious consumers. Global spirits companies are simultaneously leveraging South Korea's Hallyu-aligned lifestyle culture and the highball cocktail trend to expand premium whiskey and white spirits consumption. The craft beer segment, while undergoing consolidation through transactions like the Jeju Beer ownership change, continues to attract consumers seeking flavour variety and local craft authenticity.

Anheuser-Busch InBev NV, founded in 1852 and headquartered in Leuven, Belgium, is the world's largest beer company operating across more than 50 countries. In South Korea, AB InBev functions through its subsidiary Oriental Brewery, which it acquired in 2014, giving it a commanding domestic market position through the Cass lager brand and access to premium international labels including Hoegaarden and Budweiser produced locally. AB InBev combines global supply chain scale, marketing investment, and advanced brewing technology to maintain competitive leadership in both mass-market and premium beer categories.

HiteJinro Co., Ltd, formed through the 2011 merger of Hite Brewery and Jinro, is South Korea's largest domestic alcoholic beverages company and produces the world's best-selling spirit by volume, Jinro soju, alongside the Chamisul and Chamisul Fresh soju variants. In beer, the company's Terra brand has gained significant market share since its launch, complementing the established Hite lager portfolio. HiteJinro is actively adapting to health-conscious trends, having launched Terra Zero alcohol-free beer in March 2026 and limited-edition flavoured soju expressions targeting younger demographic segments.

Heineken NV, founded in 1864 and headquartered in Amsterdam, Netherlands, is one of the world's largest brewers, operating over 165 breweries in more than 70 countries. In South Korea, Heineken competes in the premium imported beer segment through its flagship Heineken lager and a portfolio of global speciality brands. The company targets South Korean consumers' growing appetite for international beer variety and premium drinking experiences, leveraging its global brand recognition and localised distribution partnerships to build consistent on-trade and retail presence across urban South Korean markets.

Oriental Brewery Co. (OB), operating as a wholly owned subsidiary of Anheuser-Busch InBev since 2014, is South Korea's largest beer company by market volume, accounting for more than 50% of domestic beer sales. Its flagship Cass lager is the best-selling beer brand in South Korea, supported by premium labels including Hoegaarden and Budweiser brewed locally at its facilities. OB launched Kas All Zero in August 2025, a beer simultaneously free of alcohol, sugar, calories, and gluten, underscoring its commitment to the no-and-low alcohol consumer segment.

Other key players in the market are Lotte Chilsung Beverage Co., Ltd, Casillero del Diablo, Carlsberg A/S, Jeju Beer Co. Ltd., Beam Suntory Inc, Muhak Co Ltd, Diageo Plc, Molson Coors Beverage Company, Pernod Richard S.A., Asahi Group Holdings Ltd, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the South Korea alcoholic beverages market 2026 with our comprehensive research report. From soju innovation and no-and-low alcohol trends to premium spirits growth, convenience store channel dynamics, and FAB expansion, this report delivers the market intelligence you need to act decisively. Whether you are entering South Korea, expanding a beverage portfolio, evaluating a distribution partnership, or assessing investment opportunities, download your free sample today and discover the trends shaping this dynamic market.

United States Flavoured Alcoholic Beverages Market

Australia Alcoholic Beverages Market

Mexico Alcoholic Beverages Market

West Africa Alcoholic Beverages Market

South Korea Beverage Ingredients Technologies

South Korea Beverage Consumer Behavior Trends

South Korea Beverage Distribution And Retail Channels

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market was valued at USD 27.69 Billion in 2025.

The market is projected to grow at a CAGR of 4.80% between 2026 and 2035.

The revenue generated from the South Korea alcoholic beverages market is expected to reach USD 44.25 Billion in 2035.

The market is categorised according to the type, which includes beer, traditional spirits, whiskey, white spirits, wine, rum, tequila and mescal, liqueurs, and brandy and cognac.

The market key players are Diageo Plc, Lotte Chilsung Beverage Co., Ltd., Casillero del Diablo, Pernod Richard S.A., Anheuser-Busch InBev NV, HiteJinro Co., Ltd, Heineken NV, Oriental Brewery Co., Carlsberg A/S, Jeju Beer Co., Ltd., Beam Suntory Inc, Muhak Co Ltd, Molson Coors Beverage Company, and Asahi Group Holdings Ltd, among others.

Based on the end-use, the market is divided into pubs, bars, restaurants, and retail.

Based on the distribution channel, the market is divided into hypermarkets and supermarkets, convenience stores, speciality stores, department stores and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Packaging Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.