Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

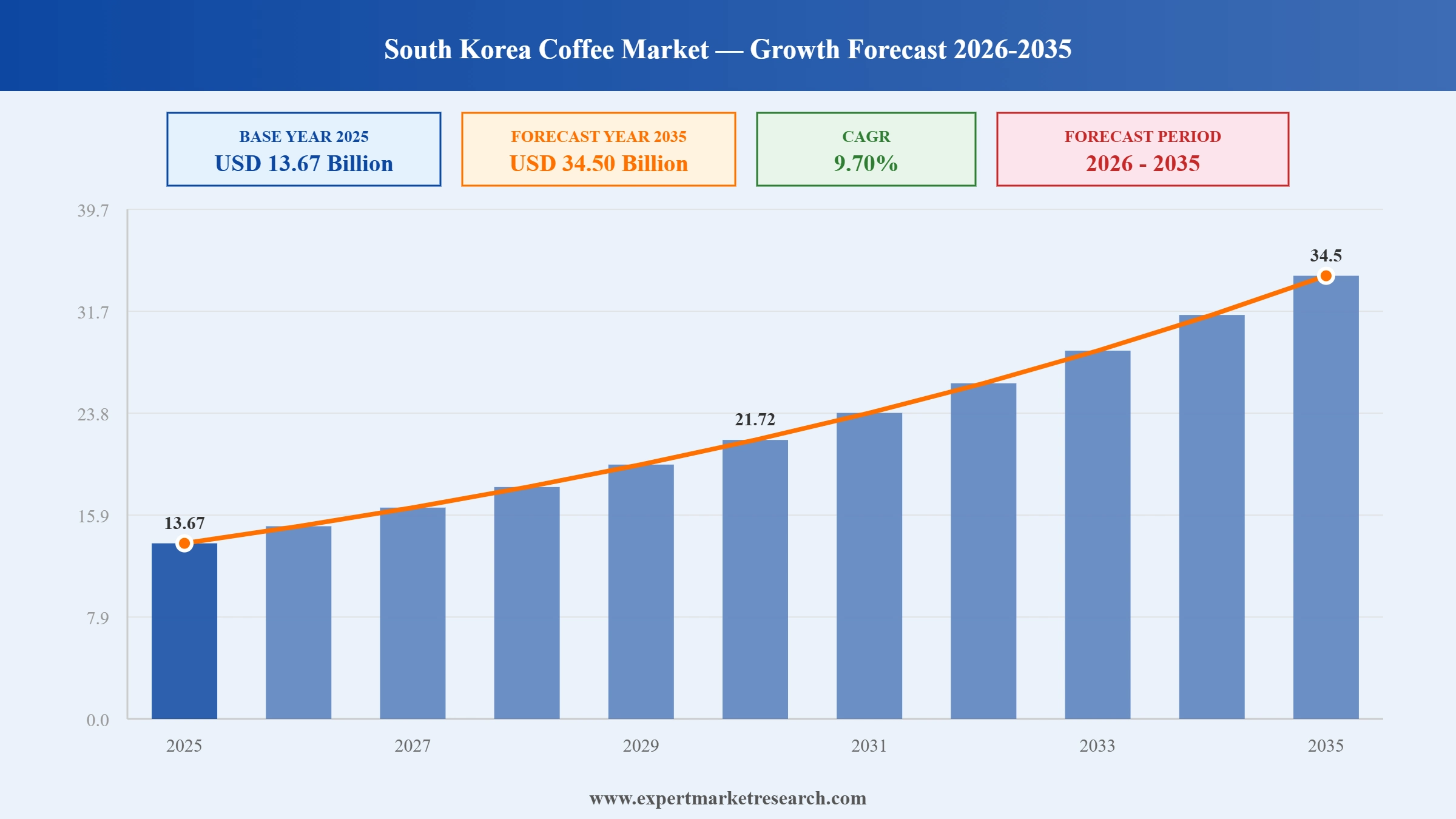

The South Korea coffee market reached a value of USD 13.67 Billion at 2025 and is projected to expand at a CAGR of around 9.70% during the forecast period of 2026-2035. With South Korea ranking among Asia's top coffee-consuming nations with over 405 cups consumed per capita annually, the rapid proliferation of specialty and low-cost franchise coffee chains across major cities, rising demand for premium and ready-to-drink formats, and widespread AI-integrated café technology, the market is expected to reach USD 34.50 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| South Korea Coffee Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 13.67 |

| Market Size 2035 | USD Billion | 34.50 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 9.70% |

| CAGR 2026-2035 - Market by Distribution Channels | Online | 13.2% |

| CAGR 2026-2035 - Market by End Use | Retail | 10.3% |

| Market Share 2025- Market by Distribution Channels | Online | 15.4% |

South Korea's coffee market is at an inflection point where specialty quality, ultra-low-cost franchise scale, and AI-powered café technology are competing and coexisting simultaneously. The market has evolved from basic instant coffee dominance to a layered ecosystem of premium specialty cafés, technology-enabled kiosks, and subscription-based home brewing. Both domestic franchise challengers and global players are adapting strategies to a consumer base that is simultaneously price-sensitive and quality-demanding within the South Korea coffee market.

In February 2026, Starbucks Korea launched the Aerocano, a handcrafted iced coffee created using an aeration technique applied to cold espresso, making South Korea the first global market for the beverage. Starbucks chose Korea specifically because of the country's exceptional iced coffee culture, where consumers drink cold coffee year-round, confirming South Korea's position as a global trendsetter within the South Korea coffee market.

By June 2025, Mega MGC Coffee had grown to 3,889 stores across South Korea, becoming the largest coffee franchise by store count in the country and the fastest-growing coffee brand in Korean history. Founded in Hongdae in 2015, it reached comparable brand penetration to Starbucks in under a decade, fuelled by ultra-competitive pricing with an iced Americano at around KRW 1,700, fundamentally reshaping competitive dynamics within the South Korea coffee market.

In April 2025, Canadian coffee operator Tim Hortons introduced its first retail packaged coffee line in South Korea, designed to build stronger brand connection among Korean consumers and access the country's high-value in-home coffee market. The launch represented a strategic move in the company's global retail expansion strategy, adding a branded at-home product to complement its South Korean café footprint within the South Korea coffee market.

In July 2024, the Philippines-based Jollibee Group acquired a 70% stake in Compose Coffee, South Korea's fast-growing budget coffee franchise founded in Busan in 2014, in the group's largest acquisition ever by store count. The USD 340 million deal signalled growing international investor confidence in South Korea's low-cost coffee franchise segment, with Compose operating over 2,600 stores, further intensifying competitive pressure within the South Korea coffee market.

The HoReCa channel anchors the South Korea coffee market, supported by over 100,000 coffee shops operating across the country by 2022, a figure that continued to grow through 2025. The average South Korean adult consumes over 405 cups of coffee per year, one of the world's highest per capita consumption rates. Starbucks, Ediya, and Mega MGC Coffee serve as the dominant HoReCa operators, collectively shaping consumer habits and driving product innovation across the café channel.

Instant coffee maintains the widest retail distribution and the largest product share within the South Korea coffee market by product format, reflecting decades of consumer familiarity with stir-in convenience coffee mixes, particularly among older demographics and busy urban workers. LOTTE-Nestle Korea and Dong Suh Companies operate strong instant coffee portfolios that sustain broad household penetration, while newer premium instant and single-serve formats are modernising the segment for younger South Korean consumers.

Coffee pods and capsules are the fastest-growing product format within the South Korea coffee market growth trajectory, catering to an expanding segment of affluent home brewers who want café-quality espresso at home. The rise of premium pod systems from Nespresso, Dolce Gusto, and Korean private label brands is converting specialty café consumers into at-home premium buyers. Subscription-based repurchasing models further cement loyalty and generate recurring revenue streams for market participants.

Supermarkets and hypermarkets hold the dominant share of retail distribution within the South Korea coffee market, providing broad product range, strong in-store visibility, and competitive pricing for instant coffee, ground coffee, and ready-to-drink formats. Convenience stores play a complementary role, especially for ready-to-drink coffee cans and cups that serve South Korea's large on-the-go consumption occasion, with 7-Eleven, GS25, and CU operating extensive formats across every urban and suburban market.

Online subscription models are building a reliable recurring revenue layer within the South Korea coffee market, particularly for whole bean, ground coffee, and premium pods targeted at quality-conscious home brewers. Platforms including Coupang and Naver Shopping integrate subscription purchase options that convert one-time buyers into regular repeat purchasers. Korea Economic Institute data suggests Koreans consume above 12 cups per week, underlining the high-frequency consumption pattern that makes coffee an ideal subscription category in the South Korean retail landscape.

The Expert Market Research’s report titled “South Korea Coffee Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

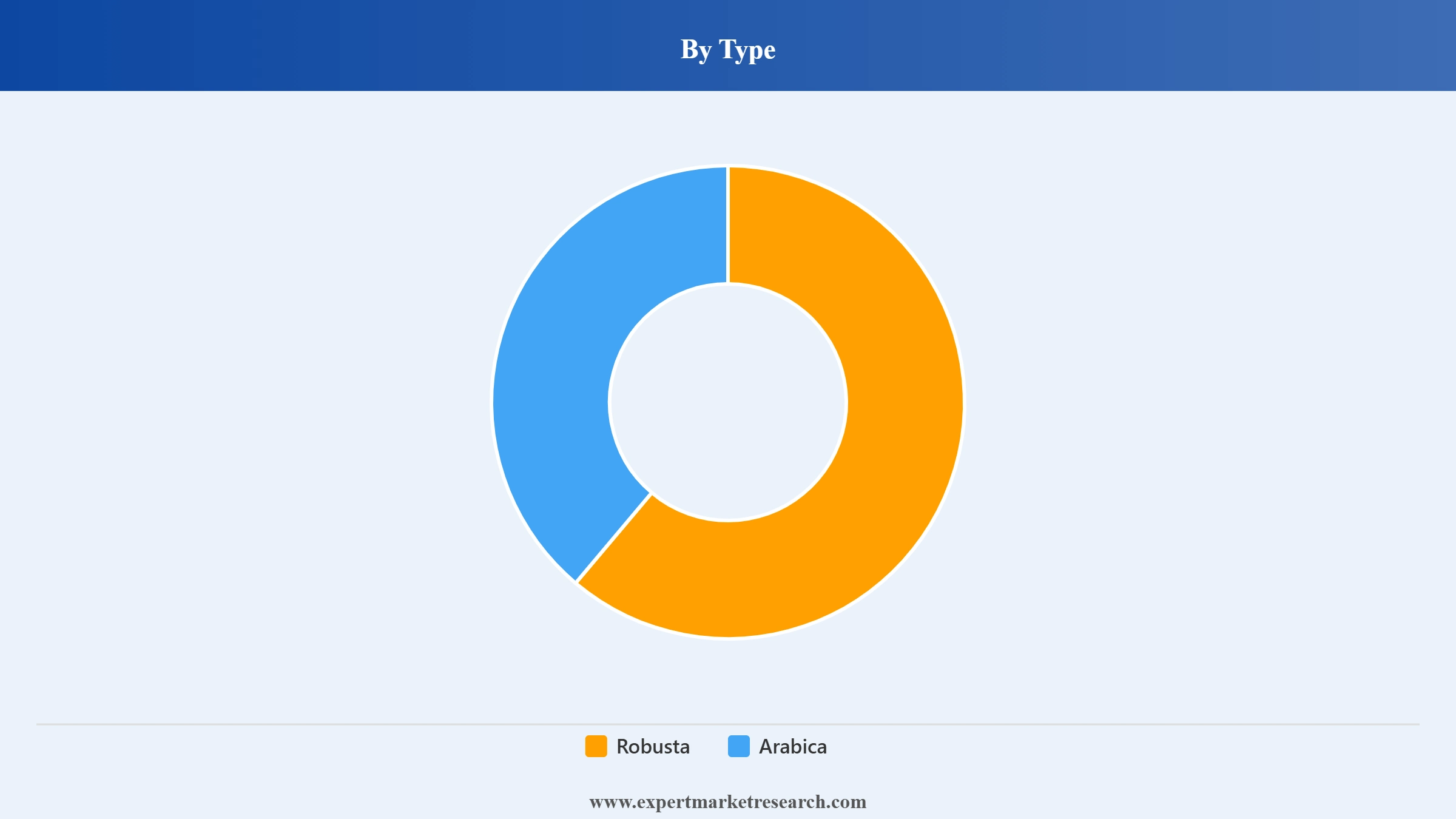

Market Breakup by Type

Key Insight: Arabica holds the dominant share within the South Korea coffee market by type because Korean specialty café culture prizes the variety's flavour complexity, lower bitterness, and premium perception. From high-tech roasteries in Seoul to certified single-origin offerings in specialty chains, Arabica is the standard choice for premium café servings and high-end at-home brewing. Robusta serves the mass instant coffee segment, where its stronger flavour, higher caffeine content, and cost efficiency make it the preferred base for traditional mixed coffee sachets that retain broad popularity across Korean households.

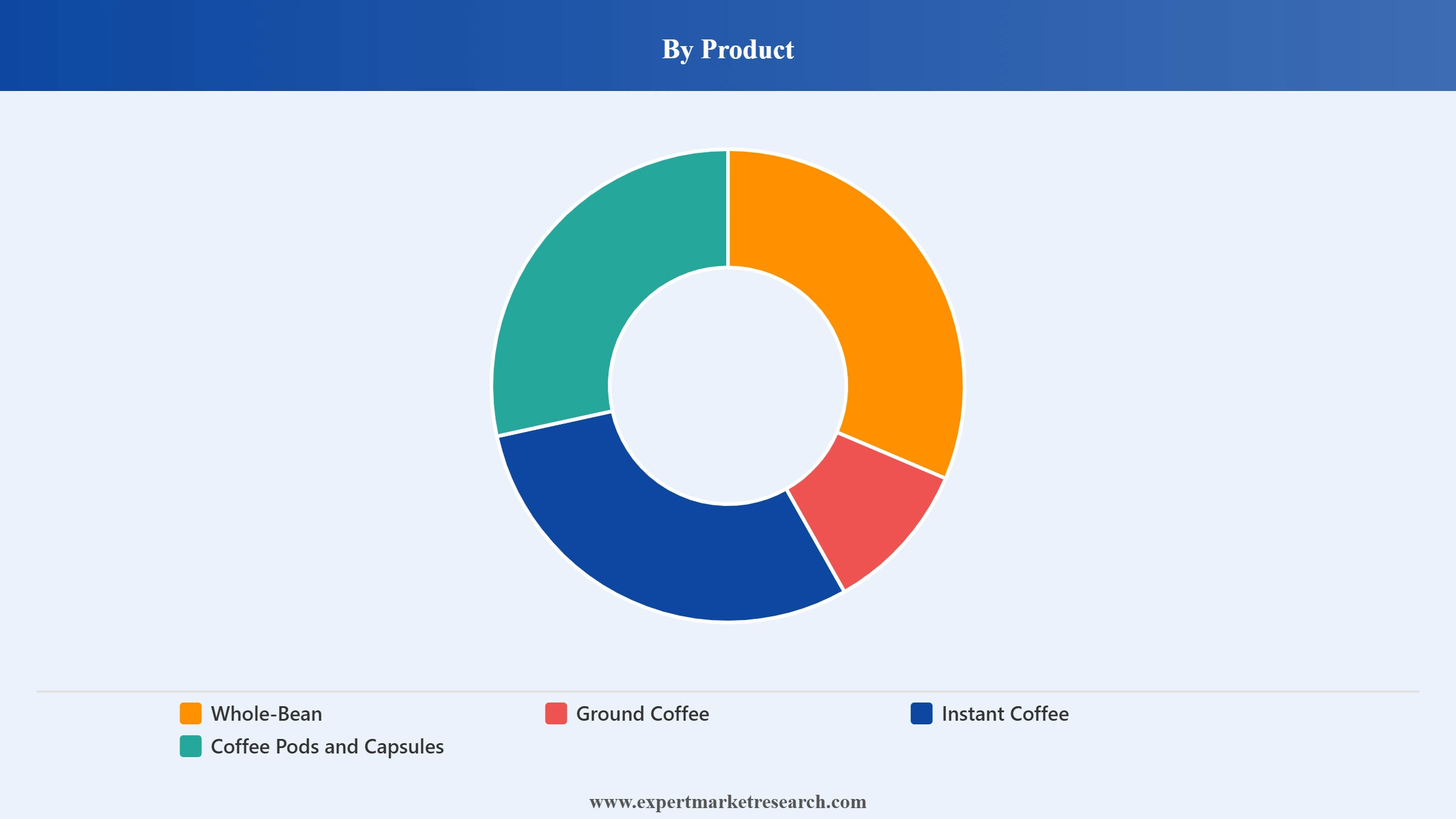

Market Breakup by Product

Key Insight: Instant coffee holds the largest product share within the South Korea coffee market, reflecting decades of consumer familiarity with convenient mix-in formats that remain widely purchased across all age groups and income levels. Coffee pods and capsules are the fastest-growing product format, driven by the growing appetite for home espresso quality among affluent consumers with premium single-serve systems. Whole bean and ground coffee benefit from South Korea's maturing specialty coffee culture, with roasteries and subscription coffee services driving home-brewing adoption among discerning quality-focused consumers.

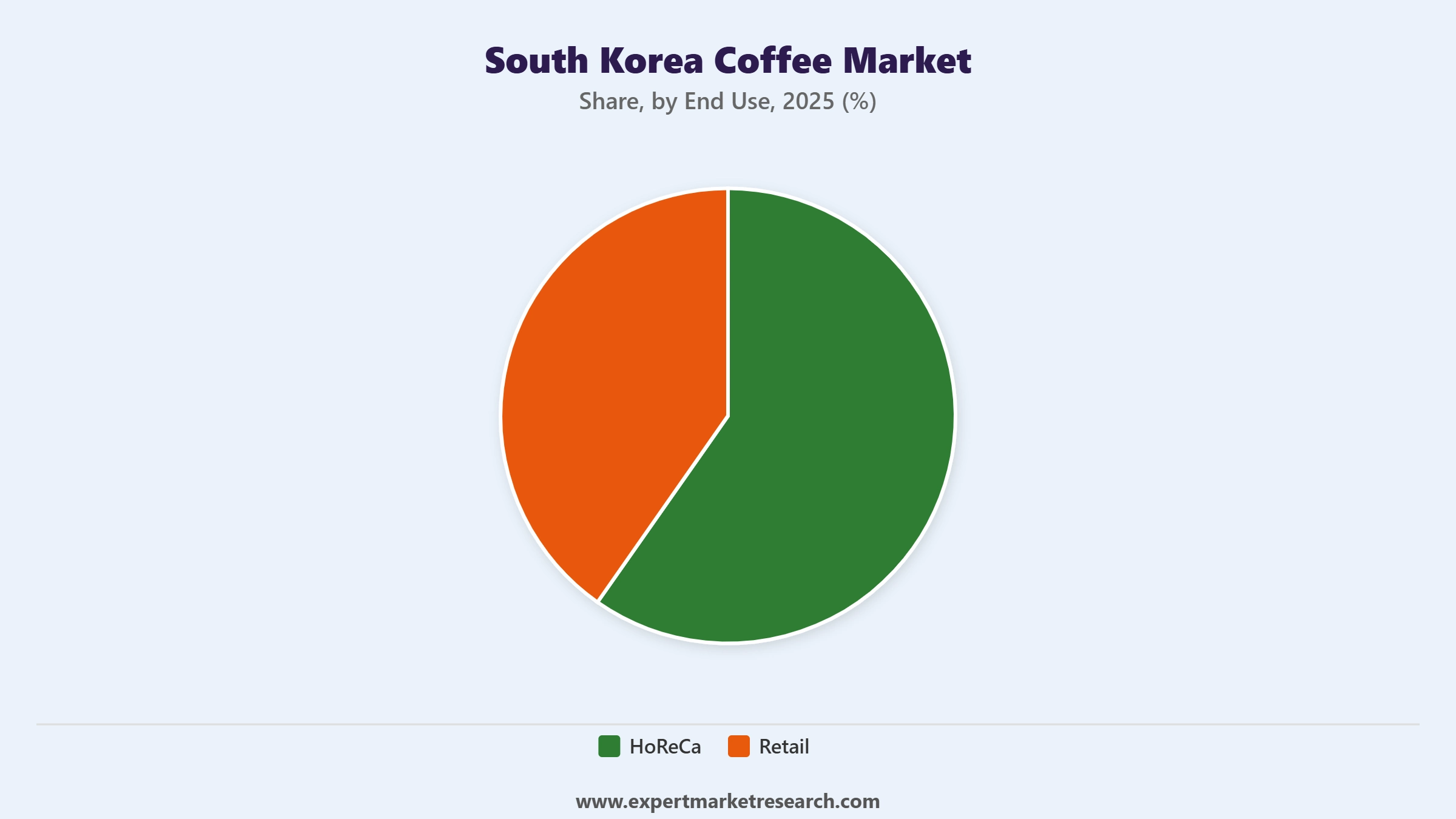

Market Breakup by End Use

Key Insight: HoReCa holds the dominant end use share within the South Korea coffee market, anchored by over 100,000 coffee shops operating across the country and deeply embedded social coffee consumption habits. Retail is growing steadily, supported by premium at-home brewing trends, cold brew penetration reaching 22 to 25 percent of households, and growing subscription model adoption across e-commerce platforms. The dual-channel structure ensures that both professional café quality and accessible at-home convenience continue to drive overall market volume expansion throughout the forecast period.

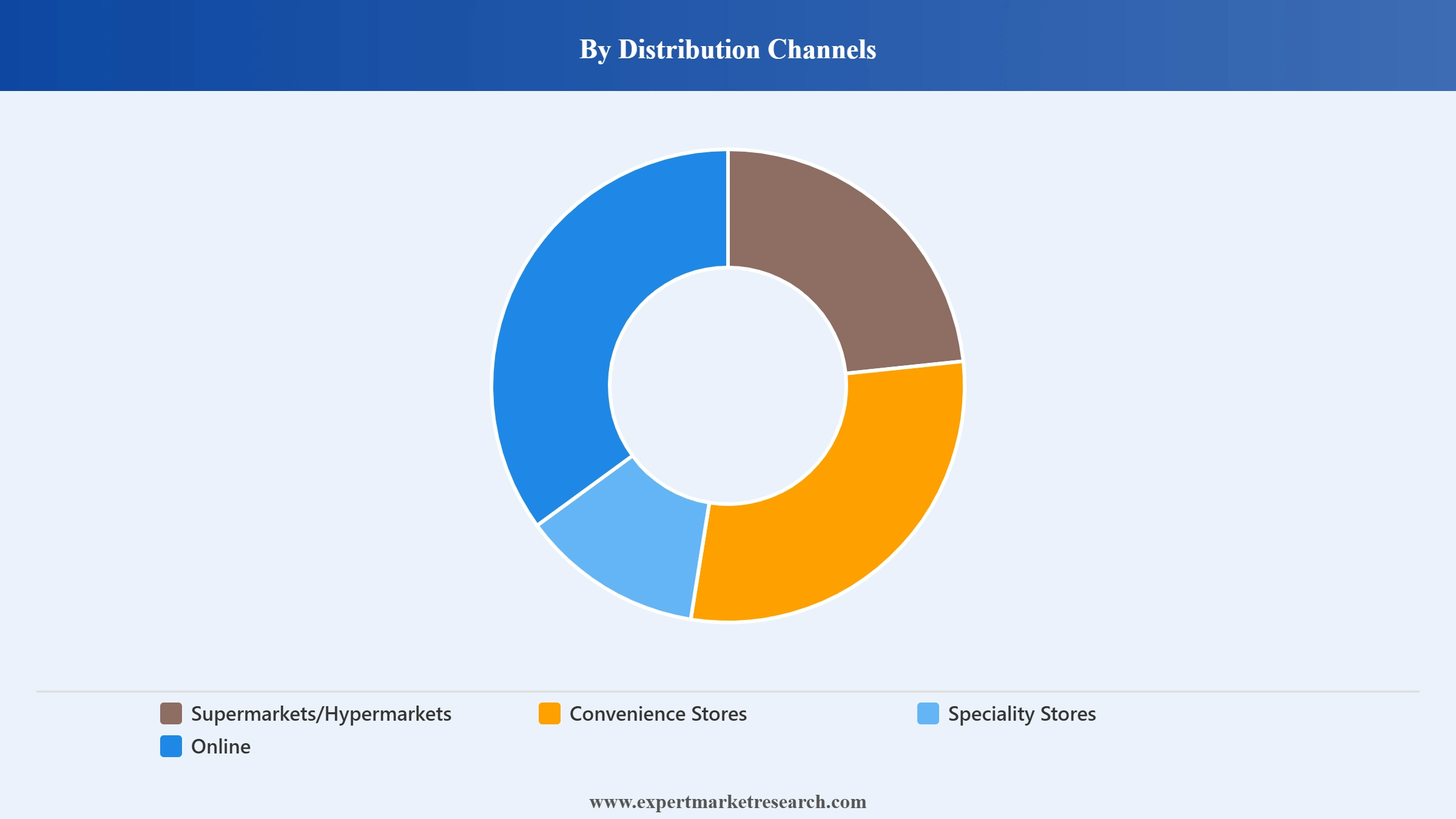

Market Breakup by Distribution Channels

Key Insight: Supermarkets and hypermarkets hold the largest distribution share within the South Korea coffee market because they offer the broadest assortment of instant coffee, ground coffee, and ready-to-drink products at competitive prices accessible to the widest consumer base. Specialty stores are the fastest-growing channel, expanding as premium coffee culture deepens and consumers seek origin-specific and expertly curated coffee product selections. Online is growing rapidly through subscription models and Coupang's same-day delivery service, which converts high-frequency repeat coffee purchases into digitally managed recurring orders.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, Arabica accounts for the dominant share of the market due to premium café demand and superior flavour profile

Arabica holds the dominant share within the South Korea coffee market because South Korea's specialty café culture, anchored by over 100,000 coffee shops, sets Arabica as the professional standard for espresso, filter, and pour-over preparation. Consumers associate Arabica with quality, nuance, and the authentic café experience, making it the bean of choice for premium at-home brewing products and specialty retail. Domestic roasteries, high-tech coffee labs, and the growing single-origin segment all reinforce Arabica's commercial leadership across the South Korea coffee market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Robusta remains commercially important within the South Korea coffee market, particularly in the instant coffee segment where its stronger flavour and affordability make it ideal for traditional three-in-one coffee mixes that retain wide household penetration among older consumers and price-sensitive demographics. Robusta also finds application in espresso blends at volume-driven café chains that prioritise consistency and cost efficiency over single-origin distinction. Its role as the functional backbone of the mass coffee market ensures sustained demand through the forecast period.

By product, instant coffee accounts for the dominant share of the market due to deep consumer familiarity and broad retail distribution

Instant coffee holds the largest product share within the South Korea coffee market because decades of consumer familiarity with stir-in convenience formats have embedded it across all age groups and household income levels. Traditional three-in-one coffee mixes, which blend instant coffee, creamer, and sugar in a single sachet, remain a daily staple for millions of South Korean consumers, particularly among older demographics and busy urban workers. Strong retail shelf placement by Dong Suh Companies and LOTTE-Nestle Korea sustains high-volume repeat purchasing across supermarkets and convenience stores.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Coffee pods and capsules are the fastest-growing product format within the South Korea coffee market at a CAGR of around 12.00%, driven by growing appetite among affluent home brewers for café-quality espresso. Premium pod systems from Nespresso, Dolce Gusto, and Korean private label brands are converting specialty café consumers into at-home premium buyers. In February 2026, Starbucks Korea launched the Aerocano as the world's first market for the innovative cold coffee format, underscoring South Korea's appetite for premium-engineered coffee products that is also lifting demand for premium packaged and pod-format coffee across retail channels.

By end use, HoReCa accounts for the dominant share of the market due to deeply embedded café culture

HoReCa dominates the South Korea coffee market end use structure because South Korean coffee consumption is predominantly a social and out-of-home activity. With over 100,000 coffee shops serving a population of 51.7 million and per capita consumption of over 405 cups per year, the density of café service and the cultural norm of meeting over coffee sustains HoReCa's dominant position. Mega MGC Coffee's 3,889-store network by mid-2025 and Starbucks Korea's sustained premium positioning together represent the competitive extremes that define the HoReCa channel within the South Korea coffee market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Retail is a growing end use segment within the South Korea coffee market, driven by cold brew penetration in households, premium capsule system adoption, and online subscription purchasing. Tim Hortons' introduction of its first retail packaged coffee line in South Korea in April 2025 reflects how international operators recognise the commercial opportunity in South Korea's at-home premium coffee segment. The Korea Economic Institute reports that Koreans consume over 12 cups per week, creating a high-frequency retail repurchasing pattern that sustains strong revenue growth in the retail channel.

By distribution channels, supermarkets and hypermarkets account for the dominant share of the market due to broad product range and competitive pricing

Supermarkets and hypermarkets hold the largest distribution share within the South Korea coffee market because they provide the broadest assortment of instant, ground, and ready-to-drink coffee formats at prices accessible to the widest consumer base. Their dense network of stores across South Korea ensures consistent product availability for the majority of everyday coffee purchasers, and strong shelf placement by brands including Dong Suh, LOTTE-Nestle, and Namyang Dairy sustains high visibility and repeat purchase frequency across the South Korea coffee market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Specialty stores are the fastest-growing distribution channel within the South Korea coffee market, driven by the deepening of premium coffee culture and consumer desire for origin-specific, expertly roasted, and artisanal coffee products that mainstream grocery retail does not comprehensively serve. Online is accelerating through Coupang and Naver subscription models that convert high-frequency coffee purchasers into recurring digital buyers. Tim Hortons' April 2025 retail packaged coffee entry and Mega MGC Coffee's scale reinforce how both offline and online channels are simultaneously evolving to serve the breadth of South Korean coffee consumer preferences.

The South Korea coffee market is defined by a dual competitive structure: a small number of well-capitalised global and domestic operators in the HoReCa channel, competing against highly fragmented ultra-low-cost franchise chains and independent specialty cafés. Dong Suh Companies, LOTTE-Nestle Korea, and Namyang Dairy dominate the institutional and retail instant coffee segment, while Starbucks holds the premium HoReCa position and Ediya and Mega MGC Coffee compete fiercely in the value and mid-market café franchise space.

Competitive intensity is increasing as international brands expand retail packaged formats, domestic franchise challengers scale rapidly, and private equity investment flows into high-growth coffee chains. Strategic priorities across leading players include loyalty app integration, AI-powered ordering systems, sustainable sourcing certifications, cold brew product expansion, and subscription model development to retain consumers across multiple occasions throughout the day.

Founded in 1956 and headquartered in Seoul, South Korea, Dong Suh is the country's leading instant coffee company, operating the widely recognised Maxwell House and Dongsuh brands. The company has built dominant retail distribution across supermarkets and convenience stores, making its instant coffee mixes a staple in South Korean households. Dong Suh continues to innovate with premium instant coffee formats and ready-to-drink products to capture the evolving preferences of the South Korea coffee market.

Founded in 1971 and headquartered in Seattle, USA, Starbucks entered South Korea in 1999 and has become the benchmark premium café brand in the country. Starbucks Korea operates an extensive store network in Seoul and other major cities, and its seasonal drinks and digital loyalty program generate strong repeat footfall. Starbucks consistently outperforms expectations in the South Korean premium HoReCa segment, with cold brew offerings and premium seasonal collections sustaining engagement among its loyal customer base.

Founded in 1987 as a joint venture between LOTTE Group and Nestle, LOTTE-Nestle Korea operates across instant coffee, Nescafe, and Nespresso product lines targeting mass retail, convenience, and premium at-home consumption occasions. The company leverages LOTTE's broad Korean retail distribution network and Nestle's global coffee brand portfolio to maintain strong commercial presence across both the HoReCa and retail end use segments within the South Korea coffee market.

Founded in 2001 and headquartered in Seoul, South Korea, Ediya was formerly the largest coffee franchise chain in Korea by store count, operating over 3,000 locations. While facing increased competitive pressure from ultra-low-cost chains like Mega MGC Coffee and Compose Coffee, Ediya maintains a strong mid-market position by balancing accessible pricing with consistent product quality. The brand continues to evolve its menu and store formats to remain relevant as competitive dynamics intensify within the South Korea coffee market.

Other key players in the market are Namyang Dairy Products Co., Ltd, LUIGI LAVAZZA SPA, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full intelligence on the South Korea coffee market with our comprehensive report. Understand why ultra-low-cost franchise growth, AI-powered café technology, cold brew adoption, and per capita consumption of over 405 cups annually are creating compelling opportunities across every product and channel. Whether you roast and distribute coffee, operate café chains, develop at-home brewing technology, or invest in consumer beverages, this report delivers the clarity you need. Download your free sample today and discover the key growth opportunities across coffee in South Korea.

Australia Coffee and Tea Capsules Market

South Korea Instant Coffee Market

Coffee Pods and Capsules Market

Ready to Drink Coffee Market

Coffee Concentrate Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the South Korea coffee market reached an approximate value of USD 13.67 Billion.

The market is projected to grow at a CAGR of 9.70% between 2026 and 2035.

Key strategies driving the market include integrating AI-driven loyalty systems, trialling sustainable sourcing models, partnering with local cafés, and investing in smart packaging and cold chain logistics to future-proof their coffee operations in Korea.

The inclination toward organic and sustainable coffee and technological innovation are the key industry trends.

The dominant type of coffee in the industry are Arabica and Robusta.

The leading distribution channels in the market are Hypermarkets/Supermarkets, convenience Stores, speciality stores, and online stores among others.

The major players in the South Korea coffee industry are Dong Suh Companies Inc., Namyang Dairy Products Co. Ltd, LOTTE-Nestlé Korea Co., Ltd, Starbucks Corporation, Ediya Co., Ltd., and LUIGI LAVAZZA SPA, among others.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 34.50 Billion by 2035.

COVID-19 slowed down the growth of the market.

The key challenges are sourcing volatility, intense urban saturation, rising labour costs, and growing pressure to meet ESG compliance across supply chains.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Product |

|

| Breakup by End Use |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.