Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

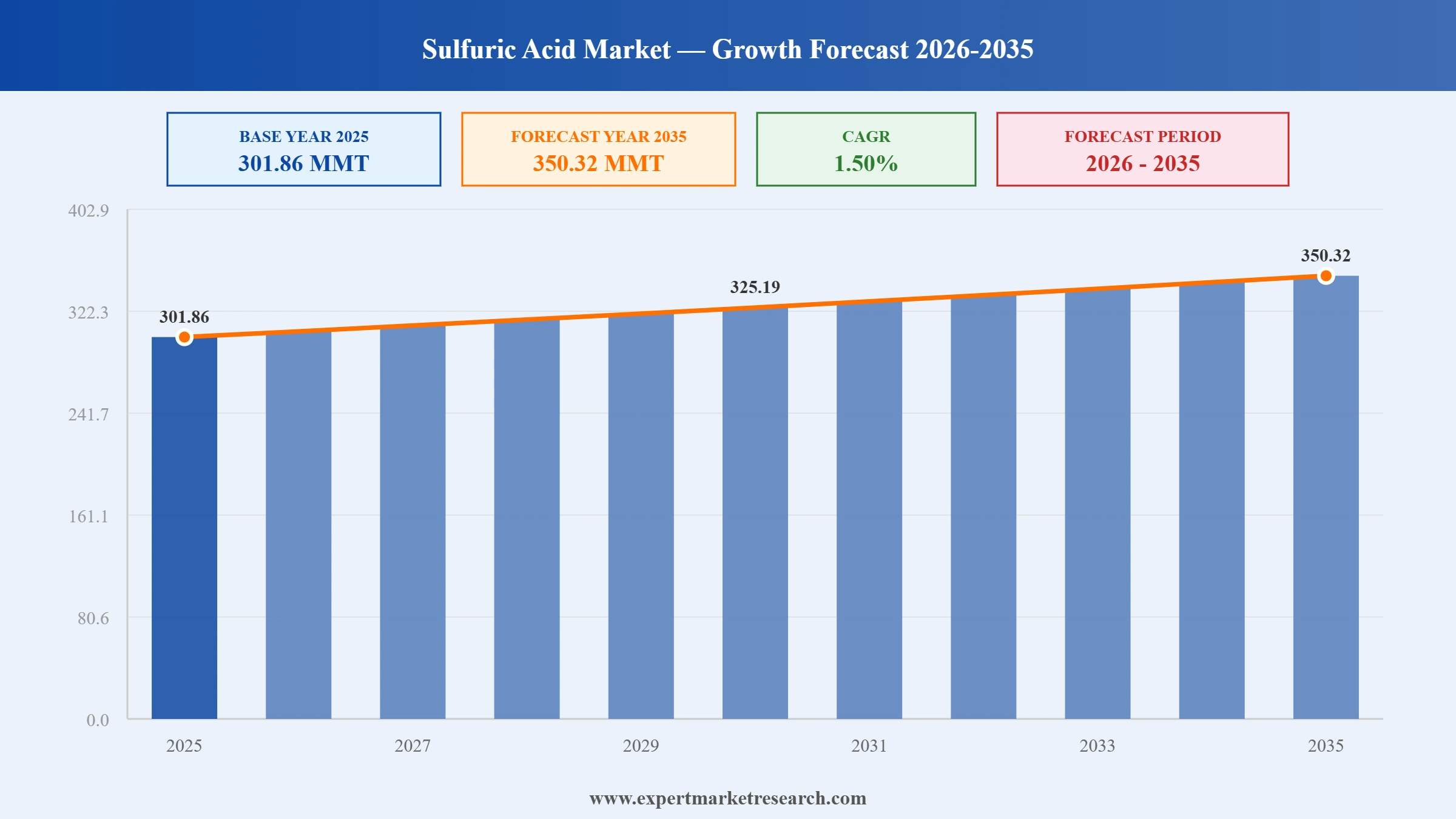

The Global Sulfuric Acid Market reached a volume of 301.86 MMT at 2025 and is projected to expand at a CAGR of around 1.50% during the forecast period of 2026-2035. With phosphate fertilizer-led demand, accelerating semiconductor-grade investments, expanding EV battery recycling, and shifts in Asia-Pacific export flows, the market is expected to reach 350.32 MMT by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Sulfuric Acid Market Report Summary | Description | Value |

| Base Year | MMT | 2025 |

| Historical Period | MMT | 2019-2025 |

| Forecast Period | MMT | 2026-2035 |

| Market Size 2025 | MMT | 301.86 |

| Market Size 2035 | MMT | 350.32 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 1.50% |

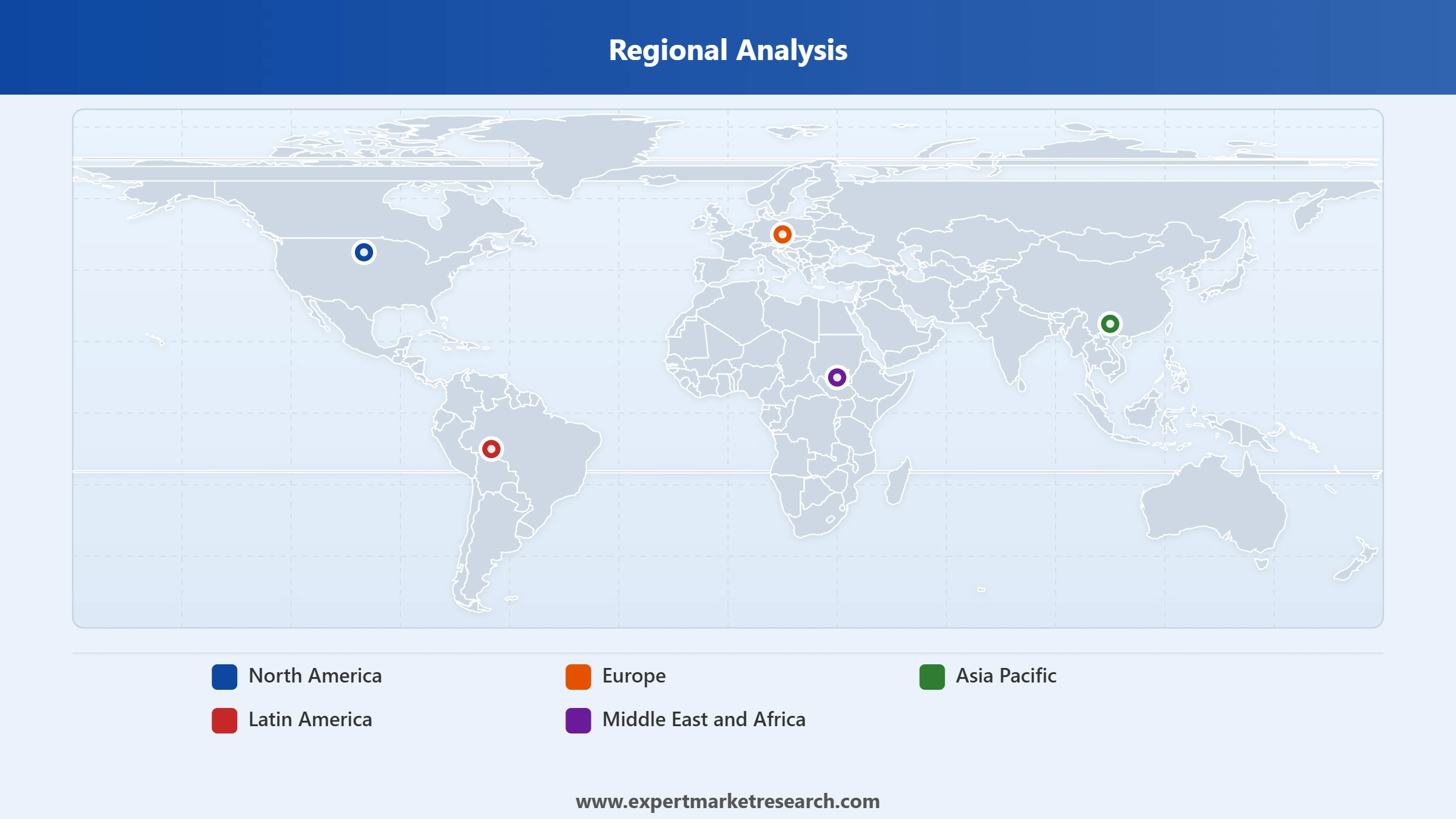

| CAGR 2026-2035 - Market by Region | Asia Pacific | 1.7% |

| CAGR 2026-2035 - Market by Country | India | 2.0% |

| CAGR 2026-2035 - Market by Country | China | 1.6% |

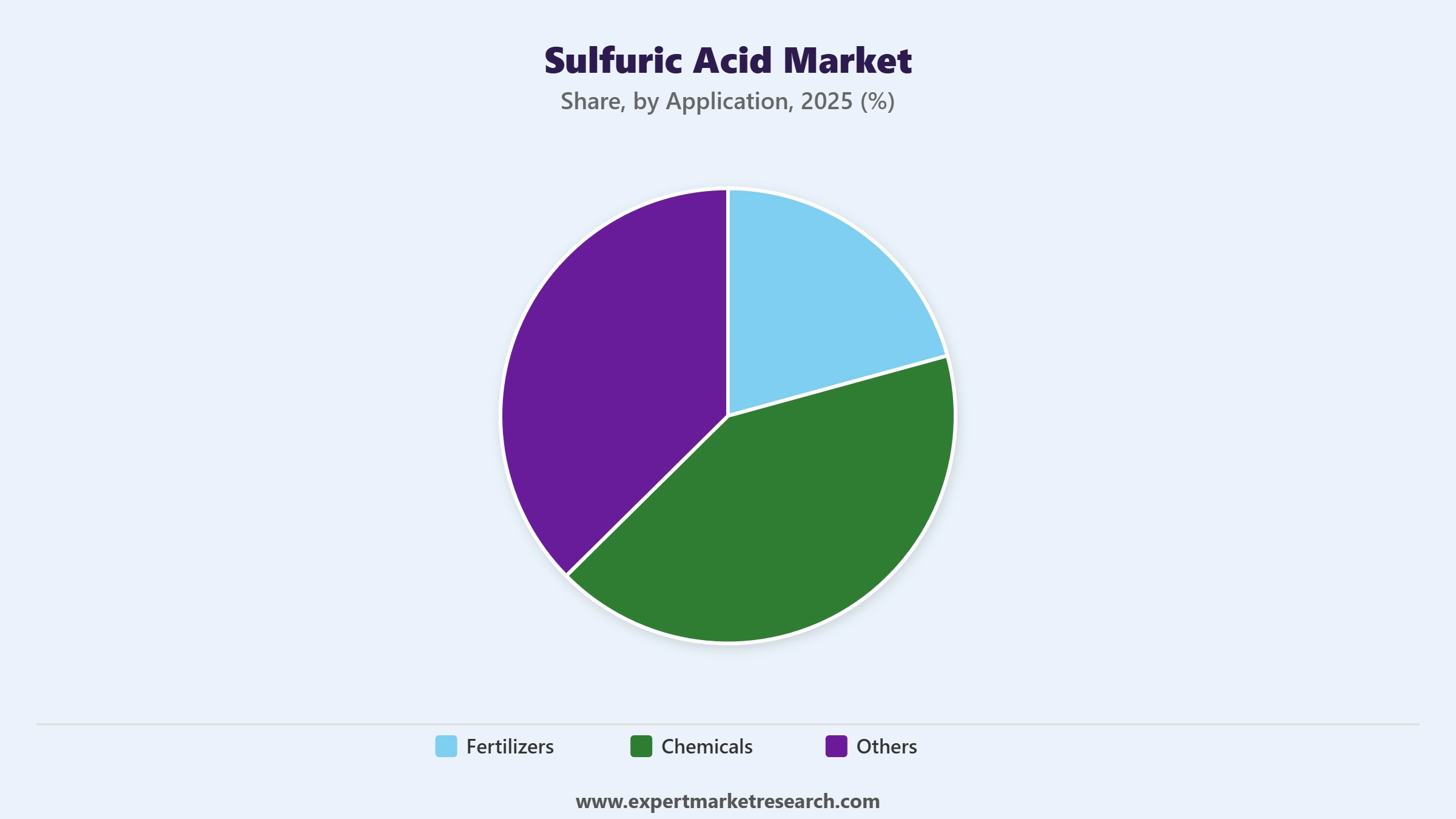

| CAGR 2026-2035 - Market by Application | Fertilizers | 1.8% |

| CAGR 2026-2035 - Market by Application | Chemicals | 1.4% |

| Market Share by Country 2025 | France | 3.0% |

The Global Sulfuric Acid Market is being shaped by semiconductor-grade investments, EV battery recycling demand, geopolitically driven trade-flow shifts, and continued reliance on phosphate fertilizer end-use, with regional capacity additions reshaping pricing dynamics.

BASF SE announced an investment in a high double-digit million-euro range to build a new semiconductor-grade sulfuric acid production plant at its Ludwigshafen Verbund site in Germany, with operations targeted for 2027. The facility will serve European chip manufacturers ramping fab capacity under the EU Chips Act. The move strengthens BASF's footprint in ultra-high-purity acid for wafer cleaning and etching, capitalising on regional semiconductor reshoring and reducing dependence on long-haul Asian imports for advanced lithography and packaging customers.

DuPont de Nemours, Inc. announced a major investment in next-generation sulfur recovery technologies aimed at improving conversion efficiency, reducing emissions footprint, and supporting cleaner sulfuric acid production for refineries and chemical producers. The MECS sulfuric acid technology portfolio is being upgraded to deliver higher recovery rates and lower energy intensity, aligning with tightening emissions standards in the US and Europe. The investment positions DuPont to capture demand from refiners and acid plant operators replacing legacy converter beds and absorbers.

China's annual sulfuric acid exports reached 4.65 million metric tons in 2025, a 73.30% increase over 2024, supplying Chile, Morocco, India, Saudi Arabia, and Indonesia for copper, phosphate, and chemical processing. The surge reshaped global trade flows and pricing, but momentum reversed sharply in early 2026 as Chinese exports declined 47.14% year-on-year in January-February. The volatility is forcing fertilizer and copper buyers in import-dependent markets to diversify supply and accelerate domestic capacity additions.

PVS Chemicals, Inc. partnered with Energy Systems Group to implement sustainability and energy-efficiency upgrades at its Chicago sulfuric acid manufacturing facility. The project covers heat-recovery, emissions-reduction, and process-optimisation work designed to lower the plant's carbon intensity and operating costs. The initiative reflects rising industry pressure to decarbonise legacy acid plants and aligns with PVS's broader push for cleaner production at its US sites, complementing its earlier carbon-free energy work at the Belgian operation.

China brought a tranche of 25 new industrial-grade sulfuric acid plants into commissioning, contributing approximately 11.5 million metric tons of fresh annual capacity originally announced in 2023 and ramping through 2025. The additions support phosphate fertilizer producers, copper smelters, and titanium dioxide manufacturers, while reinforcing China's position as a swing exporter. Combined with more than USD 4.3 billion of global investment in new units and regeneration systems between 2022 and 2024, the build-out is reshaping global supply economics and trade balances.

Semiconductor-grade sulfuric acid is emerging as one of the highest-margin niches in the chemicals industry, driven by global fab build-outs and reshored chip-manufacturing capacity. BASF's April 2025 commitment to a Ludwigshafen ultra-pure plant, with a high double-digit million-euro investment, illustrates how producers are aligning premium product lines with the EU Chips Act and US CHIPS Act demand. The trend is supporting Global Sulfuric Acid Market growth by lifting realised prices in select grades, encouraging capital investment in advanced filtration and cleaning steps, and tightening qualification standards for fab-grade acid worldwide.

Sulfuric acid is becoming a structural input in lithium-ion battery recycling as hydrometallurgical leaching scales across the United States, Europe, and Asia Pacific. Operators including Umicore and Redwood Materials use closed-loop sulfuric acid processes to recover lithium, cobalt, and nickel from spent cathodes at lower energy intensity than smelting. Growing EV penetration, regulatory mandates on battery circularity, and capital flows into giga-recycling facilities are reinforcing the role of sulfuric acid in the energy transition, driving sustained demand growth even where commodity acid pricing is otherwise constrained.

Geopolitical disruptions and policy interventions are driving structural volatility in sulfuric acid trade flows. China's January-February 2026 export volumes fell 47.14% year-on-year to 385,000 metric tons, after a record 4.65 million tons exported in 2025. Phosphate fertilizer buyers in Morocco, India, and Southeast Asia, along with Chilean copper producers, are diversifying suppliers and accelerating domestic projects. The trend is creating opportunities for North American, European, and Middle Eastern producers to capture displaced volumes, while also raising input-cost risk for downstream fertilizer and metals manufacturers globally.

Phosphate fertilizer producers consume around 57% of global sulfuric acid output, anchoring long-run demand stability for the market. Governments across China, India, Morocco, and Southeast Asia continue to prioritise food-security investments, sustaining sulfuric acid pull from phosphate rock digestion. Even as growth in fertilizer-grade acid is modest, scale economics keep this segment central to producer planning, while Morocco's OCP and India's PPL/Coromandel groups are extending phosphate capacity. The dynamic underscores why fertilizer end-use remains the foundation of global sulfuric acid balance, even as semiconductor and battery recycling lead growth.

The Expert Market Research’s report titled “Global Sulfuric Acid Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Application

Key Insight: Fertilizers represent the dominant application, absorbing approximately 57.20% of global sulfuric acid volumes in 2025 through phosphate rock digestion to produce phosphoric acid and downstream phosphate fertilizers. Anchored by demand from China, India, Morocco, and Indonesia, this segment underpins long-run market stability. The Chemicals segment is the fastest-growing application as battery, semiconductor, and specialty synthesis use cases push for high-purity grades, traceability, and tighter technical collaboration. BASF's April 2025 semiconductor-grade plant in Ludwigshafen and the rapid ramp of hydrometallurgical battery recyclers underline how chemical end-uses are reshaping the producer pricing mix and capital allocation across major hubs.

Market Breakup by Region

Key Insight: Asia Pacific commands the largest regional share, with approximately 51.20% of global consumption in 2025, anchored by phosphate fertilizer producers in China and India, and rapidly expanding semiconductor and battery recycling demand across China, Korea, Taiwan, and Southeast Asia. North America is supported by smelter and refining captives plus PVS Chemicals' US footprint, while Europe is anchored by BASF's Ludwigshafen and INEOS Group operations. Latin America's demand is driven by Chilean copper smelters, while Middle East and Africa demand stems from Moroccan and Saudi phosphate complexes, including OCP's flagship export-oriented operations supplying global fertilizer producers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Application segmentation, Fertilizers and Chemicals represent the dominant categories of demand and revenue. Fertilizers account for roughly 57.20% of global sulfuric acid volumes in 2025, anchored by phosphate rock digestion across China, India, Morocco, and Southeast Asia, where governments prioritise food-security investments and crop-yield resilience. Chemicals, while smaller in volume share, are the fastest-growing application driven by semiconductor-grade demand, EV battery recycling, and specialty synthesis. BASF's April 2025 announcement of a semiconductor-grade plant in Ludwigshafen and the global ramp of hydrometallurgical battery recyclers using closed-loop sulfuric acid leaching reinforce why chemicals is the most strategically important segment for premium pricing, technical differentiation, and long-run producer capital allocation across major sulfuric acid hubs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Region segmentation, Asia Pacific and the combined Latin America-Middle East and Africa block dominate demand. Asia Pacific commanded around 51.20% of global consumption in 2025, with China alone exporting 4.65 million metric tons in 2025, a 73% rise versus 2024. The region anchors fertilizer, semiconductor, and battery applications, attracting incremental capacity from local producers including Chung Hwa Chemical Industrial Works, Ltd. Latin America anchors copper-smelter demand in Chile, while the Middle East and Africa rely on Moroccan phosphate plants. Recent China export volatility, with January-February 2026 volumes falling 47%, demonstrates why regional concentration influences global pricing and procurement strategies.

Within the Production-Mix lens, captive smelter acid and dedicated sulfur-burning plants together shape supply economics. Captive smelter acid from copper, zinc, and nickel operations forms the backbone of regional supply in Chile, Indonesia, and parts of Africa, while dedicated sulfur-burning plants underpin merchant supply in North America and Europe. Recent investments in regeneration units, including the USD 4.3 billion globally allocated for production and regeneration systems between 2022 and 2024, are improving sustainability and reliability. DuPont's February 2025 investment in next-generation sulfur recovery exemplifies how upgraded converter and absorber technology is becoming a competitive differentiator across both captive and merchant supply.

Asia Pacific is the leading regional market, holding around 51.20% of global sulfuric acid consumption in 2025 and continuing to grow on the back of phosphate fertilizer expansion, semiconductor capacity build-outs, and EV battery recycling investments. China remains the dominant producer-exporter, with 25 new industrial-grade plants adding roughly 11.5 million metric tons of capacity by 2025 and exports reaching 4.65 million tons that year, primarily flowing to Chile, Morocco, India, Saudi Arabia, and Indonesia. India and Indonesia are scaling phosphate processing and metals refining, while Korea and Taiwan are expanding semiconductor-grade demand. Volatility in early-2026 Chinese export volumes is creating pricing tension and accelerating diversification efforts across the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America and Europe represent stable, technology-led markets where high-purity grades and sustainability investments are central. In the United States, PVS Chemicals' Chicago plant sustainability project and broader semiconductor-driven demand are reinforcing investment cases for high-purity acid. In Europe, BASF's April 2025 semiconductor-grade plant at Ludwigshafen and ongoing INEOS Group operations underpin capacity, while regulatory pressure under the EU emissions trading system continues to push decarbonisation upgrades. DuPont's February 2025 sulfur-recovery technology investments will benefit both regions, where refiners and acid plant operators are upgrading converter beds, absorbers, and emissions controls to meet tightening environmental standards and customer sustainability expectations.

The Global Sulfuric Acid Market is moderately consolidated among integrated chemical majors and regional specialists. Producers compete on scale, captive feedstock access, high-purity capability, sustainability credentials, and proximity to phosphate, metals, and semiconductor customers. Integrated players such as BASF SE, INEOS Group, and DuPont de Nemours, Inc. anchor merchant supply across Europe and North America.

Mid-tier specialists including PVS Chemicals, Inc. and Chung Hwa Chemical Industrial Works, Ltd. compete on regional service, regeneration expertise, and high-purity offerings. Competitive priorities have shifted towards semiconductor-grade investments, decarbonisation of legacy plants, and resilience against trade-flow volatility, particularly given the swings in Chinese exports through 2025-2026. Capacity additions in China, Morocco, and Saudi Arabia are reshaping regional balances, while regeneration and sulfur-recovery upgrades are emerging as a key differentiator for merchant producers serving refining and metals customers.

Founded in 1865 and headquartered in Ludwigshafen, Germany, BASF SE is a global chemicals leader producing industrial and specialty sulfuric acid. In April 2025, the company announced a high double-digit million-euro investment to build a semiconductor-grade sulfuric acid plant at Ludwigshafen, targeting startup in 2027.

Founded in 1802 and headquartered in Wilmington, USA, DuPont de Nemours is a diversified chemicals company whose Clean Technologies unit is a major MECS sulfuric acid technology licensor. In February 2025, DuPont announced a major investment in next-generation sulfur recovery technology to enhance efficiency and reduce environmental impact.

Founded in 1998 and headquartered in London, United Kingdom, INEOS Group is one of the world's largest privately owned chemical companies, producing industrial sulfuric acid alongside intermediates and polymers. The group operates across Europe, North America, and Asia, serving fertilizer, metals processing, and chemical manufacturing customers globally.

Founded in 1945 and headquartered in Detroit, USA, PVS Chemicals, Inc. is a North American specialist in sulfuric acid manufacturing, regeneration, and distribution. The company operates plants in the United States and Belgium, and is advancing sustainability upgrades at its Chicago facility while supplying refining, semiconductor, and industrial customers.

Other key players in the market are Chung Hwa Chemical Industrial Works, Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Sulfuric Acid Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on capacity build-outs, trade flow shifts, and top growth regions. Whether you are scaling fertilizer production, launching a semiconductor-grade line, or expanding battery recycling capacity, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Sulfuric Acid industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate volume of 301.86 MMT.

The market is projected to grow at a CAGR of 1.50% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about 350.32 MMT by 2035.

Stakeholders are investing in emission-optimized upgrades, expanding high-purity production lines, strengthening logistics networks, forming feedstock partnerships, and deploying digital QA tools to win long-term contracts and meet rising sustainability and traceability expectations.

The key market trends include the increase in the demand for electronic-grade sulfuric acid and rising applications of sulfuric acid in chemicals.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Fertilisers and chemicals, among others, are the leading applications of sulfuric acid in the market.

The key players in the market include INEOS Group, BASF SE, DuPont de Nemours, Inc., PVS Chemicals, Inc., and Chung Hwa Chemical Industrial Works, Ltd., among others.

Producers face tightening emission regulations, volatile sulfur feedstock prices, rising demand for specialty high-purity grades, complex logistics for safe bulk movement, and increasing customer requirements for traceability, sustainability certification, and supply-chain transparency.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.