Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

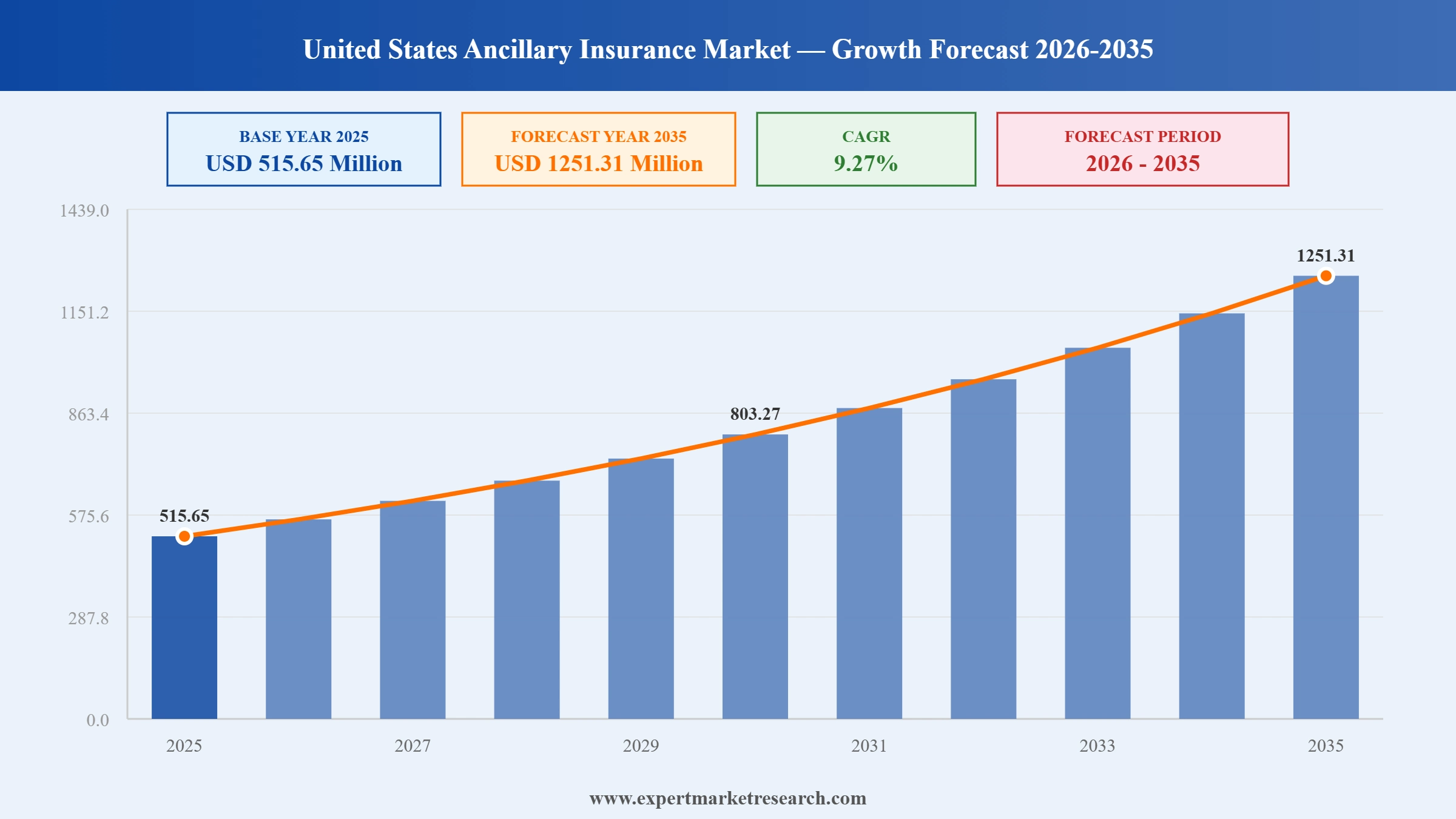

The United States ancillary insurance market reached a value of USD 515.65 Million at 2025 and is projected to expand at a CAGR of around 9.27% during the forecast period of 2026-2035. With the gig economy expansion, rising high deductible health plans, employer led voluntary benefits, and digital embedded insurance distribution, the market is expected to reach USD 1251.31 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United States ancillary insurance market is moving from a basic employer benefit add on into a portable, digital, and demographically tailored category. Carriers like Aflac, MetLife, Aetna, and Humana are deepening dental, vision, and hearing portfolios, while platforms such as Stride Health are embedding ancillary cover for gig workers at Uber and DoorDash. Rising high deductible health plans, IRS adjustments to FSAs, and steeper out of pocket exposure on ACA and Medicare plans are pushing households toward supplemental cover for everyday and unexpected costs.

In March 2026, IRS confirmed 2026 inflation adjustments lifting the health FSA salary reduction limit to USD 3,400 with adjusted carryover rules. The change reinforces ancillary insurance attach at renewal as HSA and FSA users actively budget for dental, vision, and supplemental spend.

In October 2025, MetLife released its 23rd Annual US Employee Benefit Trends Study, signalling deeper employer focus on dental, vision, and supplemental health benefits. The data has been used by HR teams to redesign 2026 enrolment, lifting ancillary insurance uptake across mid market and enterprise employers.

In March 2025, Aflac's 2025 proxy filing detailed Aflac Benefits Solutions as the platform supporting Aflac Dental and Vision in the US. The structure consolidates dental and vision underwriting, claims, and distribution into one platform, sharpening Aflac's position as the leading US supplemental insurer.

Stride Health continues to partner with marketplaces including Uber and DoorDash to embed portable dental and vision cover for gig workers. With more than 50% of the US workforce expected to be independent over the next decade, the platform led model is reshaping ancillary insurance distribution.

Freelancers and platform workers lack employer benefits, creating fresh demand for portable dental and vision policies. Stride Health's Uber and DoorDash partnerships are propelling the United States ancillary insurance market growth toward standalone, no annual commitment products with low monthly premiums.

As employers shift to high deductible health plans and family premiums approach USD 27,000 annually, households increasingly buy dental, vision, accident, and hospital indemnity cover. This out of pocket exposure is one of the most durable engines for the United States ancillary insurance market.

Modern payroll and benefits administration platforms now embed ancillary insurance enrolment directly into HR software. The move shortens enrolment and lifts attach for Aflac, MetLife, Aetna, and Guardian across small and mid market employers, reinforcing the United States ancillary insurance market.

Original Medicare does not cover many routine dental, vision, and hearing services, creating a structural gap that Aflac, Humana, and Ameritas products fill. With baby boomers aging, this senior pool is one of the most predictable demand engines for the United States ancillary insurance market.

Employers are layering voluntary critical illness, accident, and hospital indemnity on top of core dental and vision. With Aflac and MetLife pushing accident and disability products, the ancillary insurance category is widening beyond traditional dental and vision in the United States ancillary insurance market.

The EMR’s report titled “United States Ancillary Insurance Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

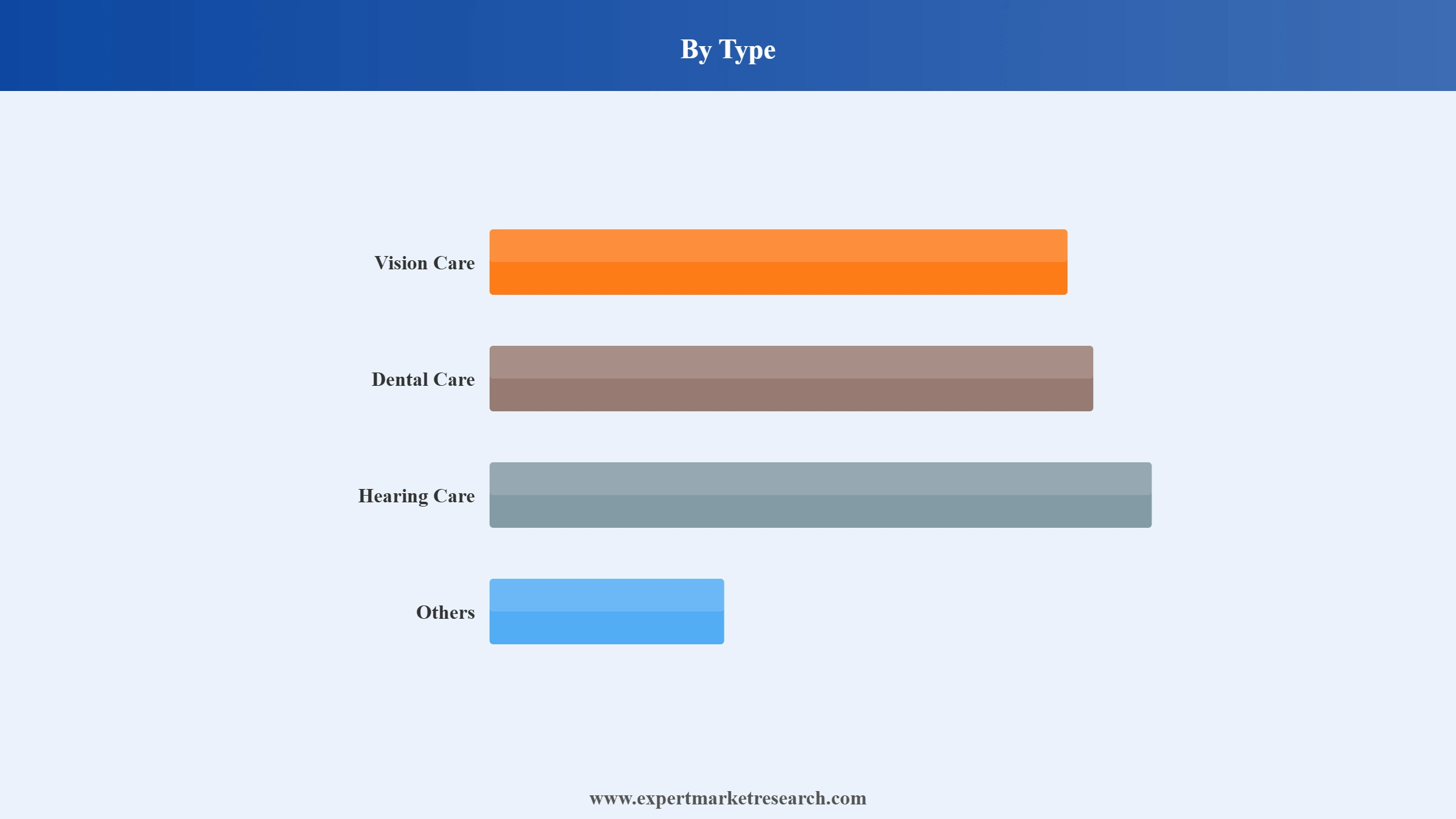

Market Breakup by Type

Key Insight: Dental care dominates the United States ancillary insurance market by enrolment, with around 293 million Americans holding dental coverage. Vision care is a close second, sold widely as a bundled employer benefit alongside dental, while hearing care is the fastest growing tier as the senior population expands and Medicare does not cover routine hearing devices. Aflac, Ameritas, MetLife, and Humana anchor this category with national networks and online enrolment journeys.

Market Breakup by Product Type

Key Insight: Anticipated loss ratio and medical loss ratio products together define how ancillary insurance plans are priced, regulated, and reported by carriers in the United States ancillary insurance market. Medical loss ratio products are increasingly central, especially for plans falling under stricter ACA related reporting and consumer protection requirements. Carriers including Aflac, MetLife, and Aetna design dental and vision plans across both structures to optimise premiums, member experience, and underwriting margins.

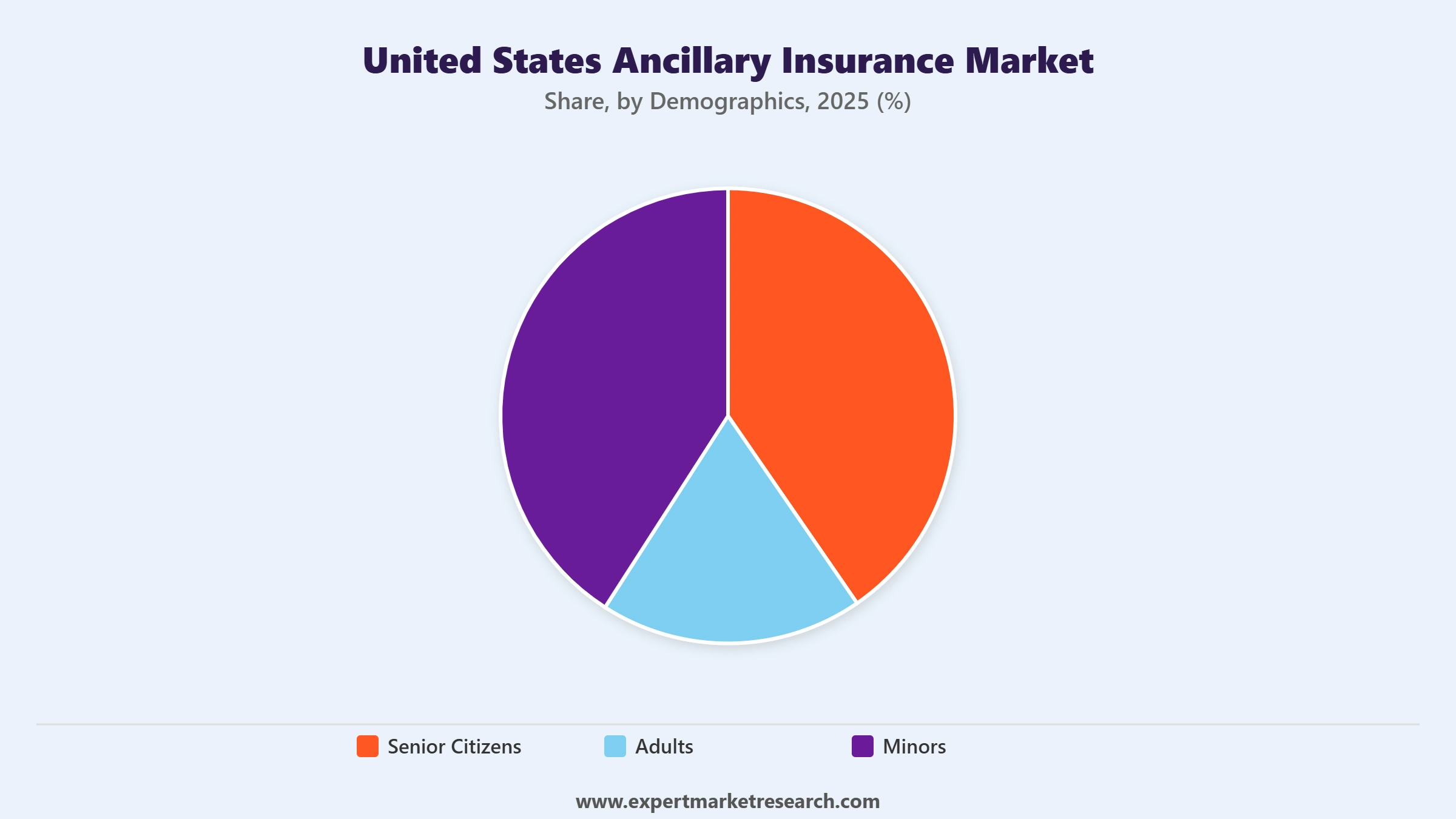

Market Breakup by Demographics

Key Insight: Adults are the largest demographic in the United States ancillary insurance market, anchored by employer sponsored dental, vision, and accident coverage that touches over 72% of full time workers. Senior citizens form the fastest growing segment, driven by Medicare coverage gaps in dental, vision, and hearing that Aflac, Humana, and Ameritas products explicitly fill. Minors are covered mostly through family employer plans and state level child dental programmes, adding a stable but smaller layer.

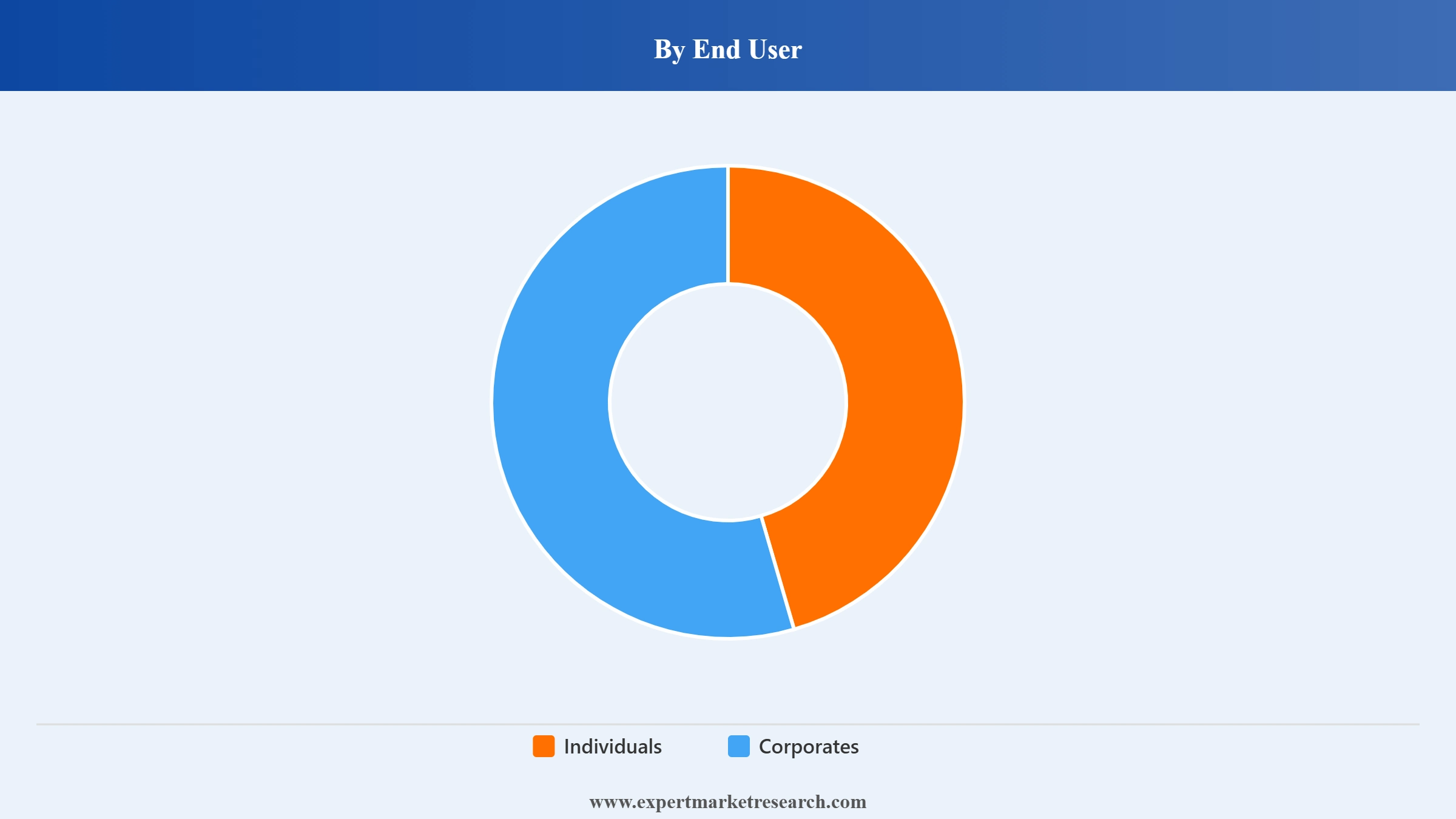

Market Breakup by End User

Key Insight: Corporates are the dominant end user channel in the United States ancillary insurance market, sourcing dental, vision, accident, and disability cover on behalf of full time workers through brokers and benefits platforms. Aflac, MetLife, Guardian, and Aetna serve this channel through group plans and federal FEDVIP style programmes. Individual purchases are the faster growing end user pool, propelled by gig economy expansion, Medicare Advantage shoppers, and digital direct to consumer carriers like Aflac's DVH plans for individuals.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, dental care dominates the market on the back of mass employer enrolment and 293 million covered Americans

Dental care leads the United States ancillary insurance market because it is the most commonly offered employer benefit alongside core medical, with about 93% of employers offering dental in 2024 and roughly 293 million Americans enrolled. Aflac, MetLife, Aetna, Humana, Delta Dental, and Guardian dominate this category through PPO and DHMO networks, federal FEDVIP plans, and digital member portals that simplify enrolment and claims.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vision care is the second largest type and is sold heavily as a bundled employer benefit with dental, with around 82% of employers offering it in 2024. Hearing care is the fastest growing tier, lifted by an aging population and Medicare coverage gaps on routine hearing aids. Aflac's combined Dental, Vision, Hearing plans, administered with EyeMed and Nations Hearing, illustrate how carriers are widening the ancillary insurance bundle.

By product type, medical loss ratio products are gaining ground as regulators push consumer value

Medical loss ratio based products are gaining ground in the United States ancillary insurance market as state and federal regulators push for stricter premium to claims ratios, especially for group health products and certain individual policies. Aflac, MetLife, Humana, and Aetna design dental and vision plans that meet these reporting requirements, balancing competitive premiums with adequate provider reimbursements and member benefits.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Anticipated loss ratio products remain widely used for traditional supplemental cover such as accident, hospital indemnity, and critical illness, where benefits are paid in lump sum or schedule based formats. Aflac's individual short term disability and DVH plans, alongside Manhattan Life Group's supplemental products, illustrate how this structure supports lower premium, fixed benefit ancillary insurance design across the United States ancillary insurance market.

By demographics, adults dominate the market on the strength of employer benefits and family enrolment

Adults dominate the United States ancillary insurance market because employer sponsored benefits and family enrolment plans concentrate dental, vision, accident, and disability cover in the working age population. With over 72% of full time workers accessing some form of ancillary cover, adults aged 18 to 64 represent the deepest pool of consistent premium volume for Aflac, MetLife, Aetna, Humana, and Guardian across the United States.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Senior citizens form the fastest growing demographic, lifted by an aging population, Medicare's gaps in dental, vision, and hearing benefits, and rising disposable retirement income. Aflac's DVH for Seniors, Humana Dental, and Ameritas vision plans target this pool. Minors are covered largely through family employer plans and state level child dental schemes, adding a stable smaller share to the United States ancillary insurance market.

By end user, corporates dominate the market on the back of broker led group enrolment

Corporates dominate the United States ancillary insurance market as employer sponsored ancillary benefits remain the standard way for working adults to access dental, vision, accident, and supplemental cover. Brokers, benefits platforms, and modern HR software embed ancillary insurance directly into enrolment journeys. Aflac, MetLife, Guardian, and Aetna anchor this channel through group plans and federal FEDVIP dental and vision programmes for government employees.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Individuals are the faster growing end user pool, lifted by gig economy expansion, Medicare Advantage shoppers, and digital direct to consumer journeys. Stride Health partnerships with Uber and DoorDash, Aflac's individual DVH plans, and online quoting tools illustrate how the carriers are reaching freelancers and Medicare eligible seniors directly, widening the addressable base of the United States ancillary insurance market.

The United States ancillary insurance market is concentrated around a handful of large carriers including Aflac, MetLife, Aetna, Humana, Guardian Life, Ameritas, Manhattan Life, and Nationwide. Aflac leads the supplemental health space, while MetLife and Aetna anchor large group dental and vision through FEDVIP and corporate channels. Humana and Ameritas are deep in senior dental and vision, particularly around Medicare Advantage and individual markets.

Competition is increasingly defined by digital distribution, platform embedded enrolment, network strength, and the ability to bundle dental, vision, hearing, accident, and hospital indemnity cover into one membership. Aflac Benefits Solutions, MetLife's annual employee benefit trends study, and gig platform partnerships like Stride Health are reshaping how the United States ancillary insurance market is built and sold.

Founded in 1955 and headquartered in Columbus, Georgia, Aflac is the number one provider of supplemental health insurance in the United States. The company offers dental, vision, hearing, accident, hospital indemnity, and disability products, distributed through brokers, group enrolment, and digital direct to consumer channels via the Aflac Benefits Solutions platform.

Established in 1887 and headquartered in Lincoln, Nebraska, Ameritas Mutual Holding Company offers a broad portfolio across insurance, financial services, and employee benefits. The company is a major provider of group and individual dental and vision insurance, serving more than two million members and partnering with brokers, employers, and benefits platforms nationwide.

Headquartered in Hartford, Connecticut and now part of CVS Health, Aetna provides medical, pharmacy, dental, vision, behavioural health, and group life and disability coverage across the United States. The company plays a major role in employer sponsored ancillary benefits and federal dental and vision programmes through its FEDVIP networks.

Founded in 1868 and headquartered in New York City, MetLife is one of the world's largest financial services and insurance providers. Its ancillary portfolio includes dental, vision, accident, disability, and supplemental health products, anchored by group employer relationships, FEDVIP plans, and the company's 23rd Annual US Employee Benefit Trends Study released in October 2025.

Other key players in the market are Manhattan Life Group Inc., Humana Inc., The Guardian Life Insurance Company of America, Nationwide, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the full intelligence on the United States ancillary insurance market 2026 with our latest report. See how gig economy growth, high deductible health plans, employer voluntary benefits, senior demand, and digital platforms are reshaping dental, vision, hearing, and supplemental coverage. Whether you build a carrier, broker employer benefits, run a benefits platform, or invest in US insurance, this report gives you the clarity to act. Download your free sample today and explore the key opportunities across United States ancillary insurance.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 9.27% between 2026 and 2035.

Key strategies driving the market include focusing on flavour innovation, expanding in Tier-2 cities, building B2B foodservice tie-ups, and promoting plant-based variants through retail partnerships.

Early detection of health problems and extended and inexpensive hospital stays are the key industry trends propelling the growth of the market.

The various types of ancillary insurance are vision care, dental care, and hearing care, among others.

Based on product type, the market can be divided into anticipated loss ratio and medical loss ratio.

On the basis of demographics, the market can be segmented into senior citizens, adults, and minors.

The end-users of the market are individuals and corporates.

The key players of the United States ancillary insurance market are Aflac Incorporated, Ameritas Mutual Holding Company, Aetena Inc., Metlife Services and Solutions, LLC, Manhattan Life Group Inc., Humana Inc., The Guardian Life Insurance Company of America, and Nationwide, among others.

Examples of ancillary services include ultrasounds, physical therapy, lab testing, and X-rays. Hospitals, physician offices, and independent diagnostic testing centres are the three types of facilities where ancillary services are typically found.

An incidental claim, an additional claim, or a counterclaim are examples of ancillary claims. Such a claim may be made by a party if it directly relates to the same issue as the primary dispute.

In 2025, the United States ancillary insurance market reached an approximate value of USD 515.65 Million.

The key challenges are high regulatory compliance costs and low consumer awareness delay adoption of innovative ancillary plans.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Product Type |

|

| Breakup by Demographics |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.