Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

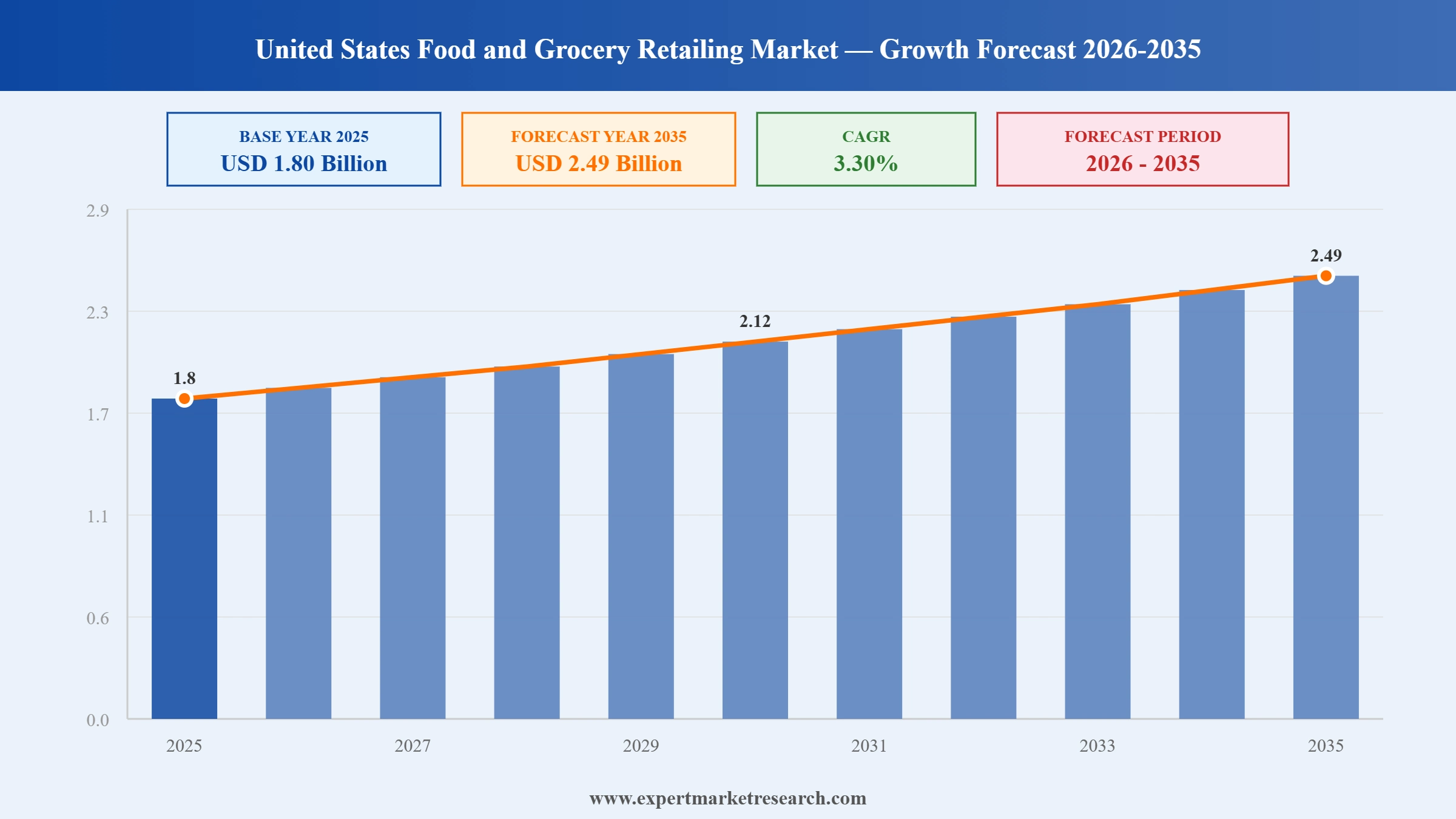

The United States Food and Grocery Retailing Market reached a value of USD 1.80 Billion at 2025 and is projected to expand at a CAGR of around 3.30% during the forecast period of 2026-2035. With accelerating online grocery adoption, evolving consumer preferences towards health and wellness products, expanding private label penetration by leading supermarket chains, and growing investment in AI-powered supply chain and inventory management technologies, the market is expected to reach USD 2.49 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United States Food and Grocery Retailing Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 1.80 |

| Market Size 2035 | USD Billion | 2.49 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.30% |

| CAGR 2026-2035 - Market by Region | Southeast | 3.3% |

| CAGR 2026-2035 - Market by Region | New England | 3.1% |

| CAGR 2026-2035 - Market by Product Type | Online Retail | 3.8% |

| CAGR 2026-2035 - Market by Distribution Channel | Online Retail | 3.6% |

| Market Share by Region | New England | 10.0% |

The United States food and grocery retailing sector is undergoing a structural shift driven by digital adoption, evolving consumer health preferences, sustainability demands, and intense competitive pressures. These forces are collectively reshaping how Americans shop for food and what they expect from retailers.

In June 2025, C&S Wholesale Grocers and SpartanNash announced a definitive merger agreement under which C&S would acquire SpartanNash for USD 26.90 per share in cash, representing total consideration of approximately USD 1.77 billion including assumed net debt. The transaction, unanimously approved by both boards, would bring together complementary distribution networks operating nearly 60 distribution centres across the US and serving close to 10,000 independent retail locations. The merger is expected to generate supply chain efficiencies and translate into lower grocery prices for consumers.

In December 2024, a federal judge granted the Federal Trade Commission's request for a permanent injunction blocking the proposed USD 25 billion merger between Kroger and Albertsons Companies, citing concerns about reduced grocery competition and higher prices for consumers. The ruling ended a merger first announced in October 2022 that would have created the largest traditional supermarket chain in the United States. The decision reinforced the competitive fragmentation of the US grocery retailing landscape and signalled heightened regulatory scrutiny of consolidation within the food and grocery sector going forward.

In May 2024, Nestle launched Vital Pursuit, a dedicated food product line specifically formulated for consumers using GLP-1 weight loss medications such as Ozempic and Wegovy. The range features high-protein, high-fibre, nutrient-dense items portioned to align with the reduced appetite typical among medication users. Marketed directly through US grocery retail channels, this launch represented a significant product innovation move by one of the country's largest food manufacturers, tapping into a rapidly growing consumer segment and reinforcing the health and nutrition shift shaping grocery purchasing behaviour.

In February 2024, Grocery Outlet Holding Corp. announced a definitive agreement to acquire United Grocery Outlet (UGO), an extreme value discount grocery retailer with 40 stores operating across the Southeastern United States. The deal, which closed in early Q2 2024, gave Grocery Outlet an immediate footprint in Tennessee, North Carolina, Georgia, Alabama, Kentucky, and Virginia, marking its entry into a new major region. The acquisition reflects a broader trend of US grocery retailers scaling through regional M&A to compete against national chains and discount operators.

In 2024, Walmart advanced its strategic collaboration with Microsoft to develop cloud-based retail management systems, with a focus on leveraging Microsoft Azure's AI capabilities to improve inventory management, demand forecasting, and personalised shopping experiences across Walmart's extensive US grocery network. The collaboration is intended to strengthen Walmart's operational efficiency and enhance its ability to serve grocery shoppers both in-store and through its online grocery platform, where it captured approximately 37% of total US online grocery sales in Q2 2024, up from 28.2% in Q2 2021.

The rapid growth of online grocery shopping is one of the most consequential structural shifts in US food retailing. According to US Census Bureau data, online grocery sales reached USD 147.5 billion in 2022, marking a 14.5% increase from the prior year, with growth continuing into subsequent years. Walmart captured approximately 37% of total US online grocery sales in Q2 2024, demonstrating how brick-and-mortar incumbents are successfully converting digital demand into market share. Retailers are investing heavily in click-and-collect infrastructure, last-mile delivery networks, and AI-powered inventory systems as online channels become a permanent fixture of grocery purchasing behaviour rather than a pandemic-era anomaly. United States Food and Grocery Retailing Market growth is being directly supported by this digital channel expansion.

US consumers' growing focus on health, nutrition, and wellness is transforming grocery product mix and shelf allocation priorities. Demand for organic, plant-based, high-protein, and low-sugar products has grown substantially, with USDA data indicating that organic grocery sales grew by 30% over three years to 2024. In May 2024, Nestle's launch of the Vital Pursuit product line specifically targeting GLP-1 medication users illustrated how major food manufacturers are reshaping their US portfolio strategies to align with this health-driven consumption shift. Retailers are dedicating more floor and digital shelf space to health-focused categories, and private label wellness lines are gaining share as consumers seek affordable nutritious options.

The US grocery retailing sector continues to consolidate as companies seek scale advantages in purchasing, logistics, and technology investment. While the Federal Trade Commission's blocking of the Kroger-Albertsons merger in December 2024 demonstrated regulatory limits on mega-mergers, smaller scale transactions have continued at pace. In June 2025, C&S Wholesale Grocers announced a USD 1.77 billion acquisition of SpartanNash, creating a combined distribution network spanning nearly 60 centres and serving close to 10,000 independent retail locations nationwide. This transaction reflects the ongoing strategic imperative for US grocery distributors and retailers to achieve greater scale to compete against Walmart, Amazon, and discount channel operators.

US grocery retailers are accelerating investment in artificial intelligence and cloud-based technologies to improve operational efficiency and personalise the shopping experience. Walmart's 2024 collaboration with Microsoft on Azure-powered retail systems exemplifies how the largest operators are leveraging AI for demand forecasting, inventory management, and supply chain optimisation. The National Retail Federation reported in 2024 that 35% of consumers now prefer shopping for groceries through mobile apps, reinforcing digital channel investment priorities. AI-driven personalisation, dynamic pricing tools, and automated replenishment systems are increasingly deployed across both large national chains and mid-tier regional supermarkets seeking to reduce labour costs and improve product availability.

The Expert Market Research's report titled “United States Food and Grocery Retailing Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

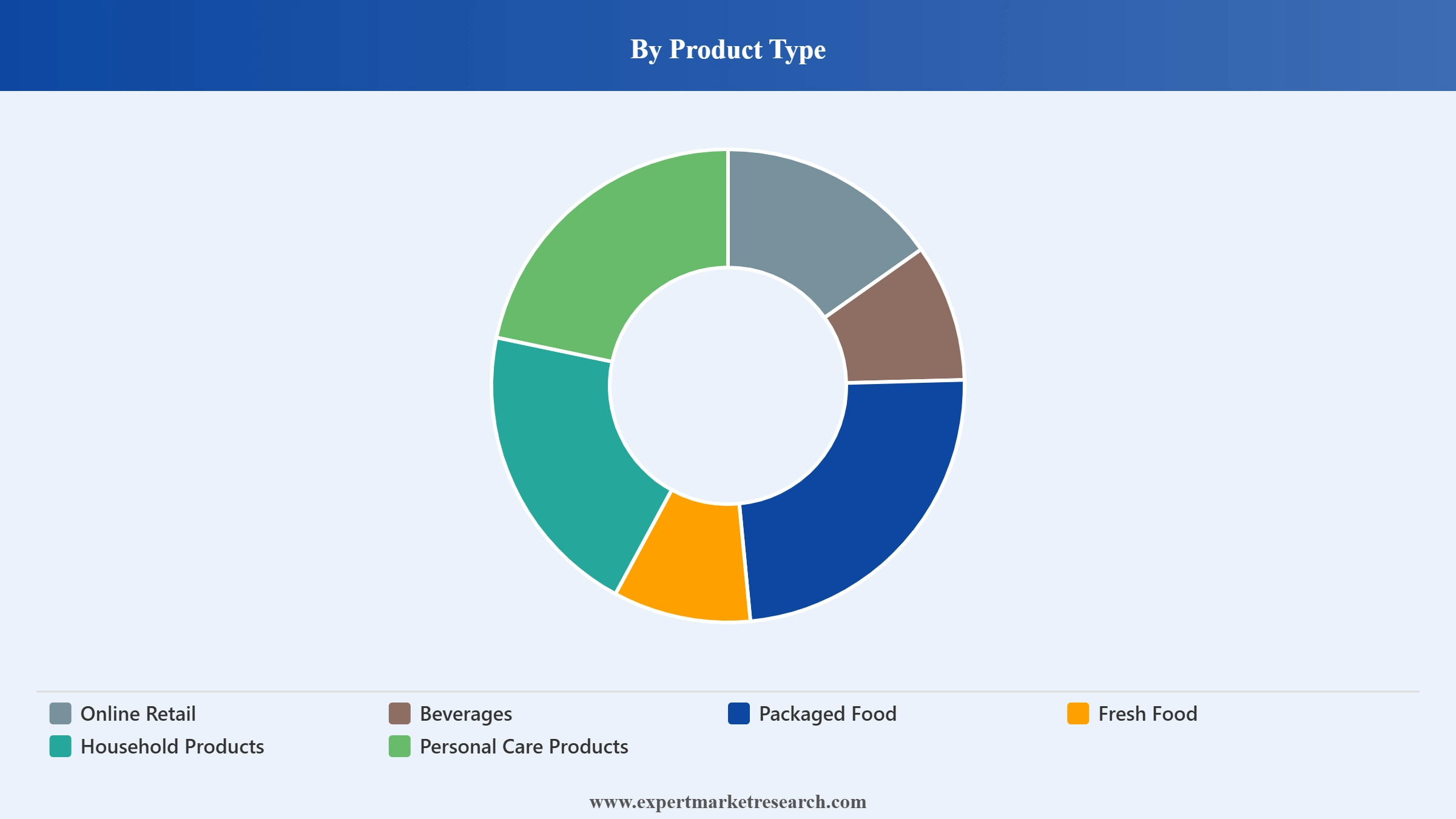

Market Breakup by Product Type

Key Insight: The Fresh Food segment holds the largest share of the US food and grocery retailing market by product type, capturing approximately 38% of revenues, underpinned by sustained consumer demand for fresh produce, meat, dairy, and bakery items across both supermarket and online channels. Online Retail is the fastest-growing product type at a CAGR of 3.8% through 2035, driven by the increasing convenience of digital platforms for non-perishable and packaged grocery purchases. Beverages follow with a 3.5% CAGR as online channels expand the consumer base for both alcoholic and non-alcoholic drink categories. Packaged Food maintains steady growth at 3.4%, supported by private label expansion and consumer demand for convenience meal solutions.

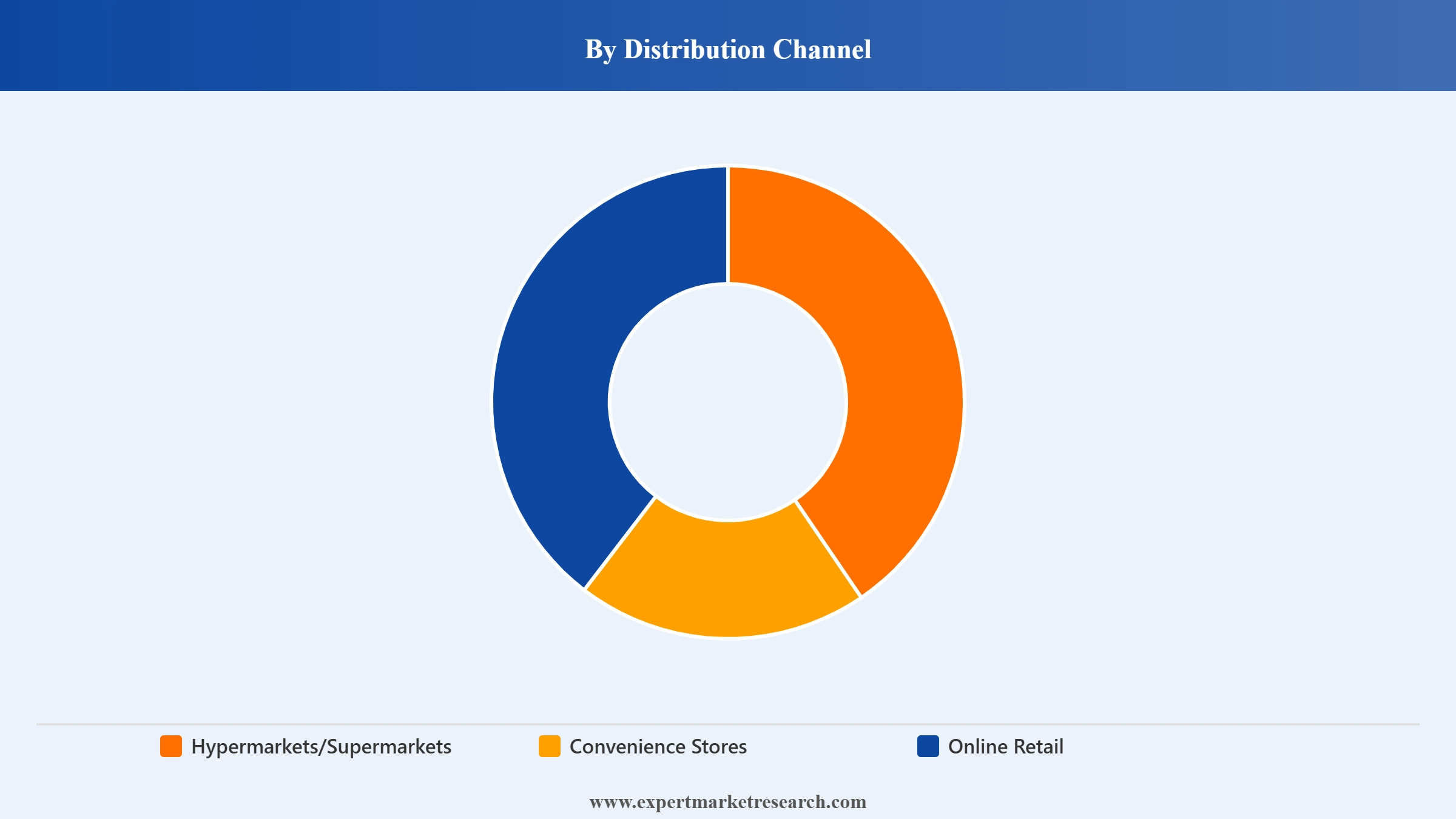

Market Breakup by Distribution Channel

Key Insight: Hypermarkets and Supermarkets dominate the US food and grocery retail distribution landscape, accounting for the majority of revenues in 2025. Walmart, Kroger, and Costco anchor this segment, leveraging scale, private label penetration, and omnichannel integration to maintain consumer loyalty. Online Retail is the fastest-growing distribution channel at an estimated CAGR of 3.6% through 2035, supported by investments from Amazon, Walmart, and Instacart in delivery infrastructure and app-based ordering. Convenience Stores are growing at a CAGR of 3.2% as operators expand their fresh food and prepared meal offerings to capture time-pressed urban consumers seeking fast, accessible grocery alternatives.

Market Breakup by Region

Key Insight: The Far West region is expected to lead the US food and grocery retailing market with the highest CAGR of 3.8% through 2035, driven by high urbanisation rates in California, strong e-commerce infrastructure, and consumer preference for premium, organic, and sustainably sourced grocery products. The Southeast region is the largest in total market size, reflecting its large and growing population base and the strong presence of major grocery chains. New England and the Mideast exhibit moderate growth at CAGRs of 3.1% and 2.8% respectively, while the Plains and Great Lakes regions grow more slowly at CAGRs of 2.6% and 2.5% due to lower population density and less mature digital grocery infrastructure.

By Product Type

Within the Product Type segmentation, the Fresh Food category commands the dominant share of the US food and grocery retailing market at approximately 38% of revenues in 2025. This reflects the enduring importance of fresh produce, meat, bakery, and dairy across US supermarket formats, where freshness is a primary store-selection driver for consumers. Major retailers including Kroger and Albertsons have invested significantly in fresh department expansions, local sourcing programmes, and reduced-waste initiatives to capitalise on growing consumer preference for quality fresh foods. Online Retail is the fastest-growing product type, with retailers like Amazon Fresh and Walmart Grocery extending fresh food delivery capabilities to capture digital demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Hypermarkets and Supermarkets hold the dominant distribution channel share in the US food and grocery retailing market, anchored by Walmart's position as the largest grocery retailer in the country and Kroger's extensive network of nearly 2,800 stores across 35 states. These large-format operators benefit from scale purchasing advantages, comprehensive private label portfolios, and the increasing integration of online ordering and curbside pickup services. Online Retail is the fastest-growing distribution channel at an estimated CAGR of 3.6% through 2035, as consumers shift towards digital-first grocery engagement and retailers invest in same-day and next-day fulfilment infrastructure to meet rising convenience expectations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Region

The Far West region leads growth expectations in the US food and grocery retail landscape, benefiting from California's large urban consumer base, high rates of health and organic product adoption, and well-developed e-commerce delivery infrastructure. The Southeast represents the largest regional market by absolute value, underpinned by rapid population growth, rising disposable incomes, and sustained expansion of both traditional supermarket chains and discount grocery operators into markets across Florida, Texas, and the Carolinas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Far West region is the fastest-growing market for food and grocery retailing in the United States, led by California and the Pacific Northwest where consumer spending on premium, organic, and specialty grocery products significantly exceeds the national average. California's large and diverse urban population, combined with advanced logistics infrastructure and high smartphone penetration, makes it a natural leader in online grocery adoption. Major retailers including Amazon Fresh, Walmart, and Kroger have concentrated digital grocery investment in the Far West, and regional specialty chains like Sprouts Farmers Market and Trader Joe's maintain particularly strong presences here. The region's regulatory emphasis on sustainable food systems and reduced plastic packaging is also driving innovation in eco-friendly grocery formats.

The Southeast is the largest regional food and grocery retail market in the United States by total revenue, reflecting sustained population growth across states including Florida, Texas, Georgia, and North Carolina. The region's expanding suburban communities and rising median household incomes are generating strong demand for both traditional full-service supermarkets and value-oriented grocery formats. Walmart and Kroger maintain dense store networks throughout the Southeast, while discount operators including Aldi and Grocery Outlet are aggressively expanding their footprints to capture price-conscious consumers. The Southeast was also the focus of Grocery Outlet's 2024 acquisition of United Grocery Outlet, which added 40 stores across six states and highlighted the region's strategic attractiveness for grocers seeking growth.

The United States food and grocery retailing market is highly competitive and moderately consolidated at the national level, with a handful of large-scale operators capturing the majority of total market revenues. Walmart commands the leading position with approximately 37% of online grocery sales and an unrivalled physical store network, while Kroger operates the largest traditional supermarket chain in the country. Costco continues to expand its membership-based warehouse model, and Amazon has deepened its physical and digital grocery integration through Amazon Fresh and Whole Foods Market. Regional and independent grocers face increasing pressure from these scaled national players and discount channel operators, prompting M&A activity to build competitive scale.

Technology investment, private label development, and supply chain efficiency are the primary competitive levers across the sector. Retailers investing in AI-powered personalisation, app-based loyalty programmes, and seamless omnichannel shopping experiences are seeing measurable gains in basket size and visit frequency. The FTC's blocking of the Kroger-Albertsons merger in late 2024 reinforced the competitive fragmentation at the top tier, ensuring that no single traditional supermarket operator gains outsized national dominance in the near term.

Founded in 1962 and headquartered in Bentonville, Arkansas, Walmart is the world's largest retailer and the dominant force in US food and grocery retailing. Its grocery operations span more than 4,600 US locations and account for approximately 56% of total Walmart US revenues. Walmart's strong investments in digital grocery, Walmart Plus membership, curbside pickup, and its Microsoft Azure cloud collaboration are reinforcing its position across both physical and online channels.

Founded in 1883 and headquartered in Cincinnati, Ohio, Kroger operates nearly 2,800 supermarkets under multiple banners across 35 states. It is the largest traditional supermarket chain in the United States by store count and revenue. Kroger competes through its extensive private label portfolio, customer loyalty programme, and investments in digital ordering and delivery capabilities through partnerships with Ocado and Instacart.

Founded in 1983 and headquartered in Issaquah, Washington, Costco operates a membership-based warehouse retail model across the United States. Its food and grocery operations, anchored by Kirkland Signature private label products, generate significant revenue from bulk purchasers. Costco's value proposition, high membership renewal rates exceeding 90%, and expansion of e-commerce capabilities position it as a durable and growing force in US food retailing.

Founded in 1939 and headquartered in Boise, Idaho, Albertsons Companies operates more than 2,200 supermarkets and pharmacies across 34 states under banners including Safeway, Vons, Jewel-Osco, and Shaw's. Following the failed Kroger merger in December 2024, Albertsons is pursuing an independent growth strategy focused on digital capabilities, private label expansion, and its Sincerely Health wellness platform to drive customer engagement.

Other key players in the market are Amazon, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead of the competition in the United States Food and Grocery Retailing Market 2026 with our comprehensive research report. Explore the latest findings on digital grocery adoption, product innovation trends, regional demand dynamics, and the competitive strategies reshaping America's food retail sector. Whether you are a retailer seeking expansion opportunities, an investor evaluating market entry, or a brand assessing shelf positioning, our report delivers the clarity you need. Download your complimentary sample now and explore the key opportunities defining US grocery retailing through 2035.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 1.80 Billion.

The market is projected to grow at a CAGR of 3.30% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026-2035 to reach USD 2.49 Billion for 2035.

The key players in the market include Walmart Inc., The Kroger Co., Costco Wholesale Corporation, Albertsons Companies, Amazon, and Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.