Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

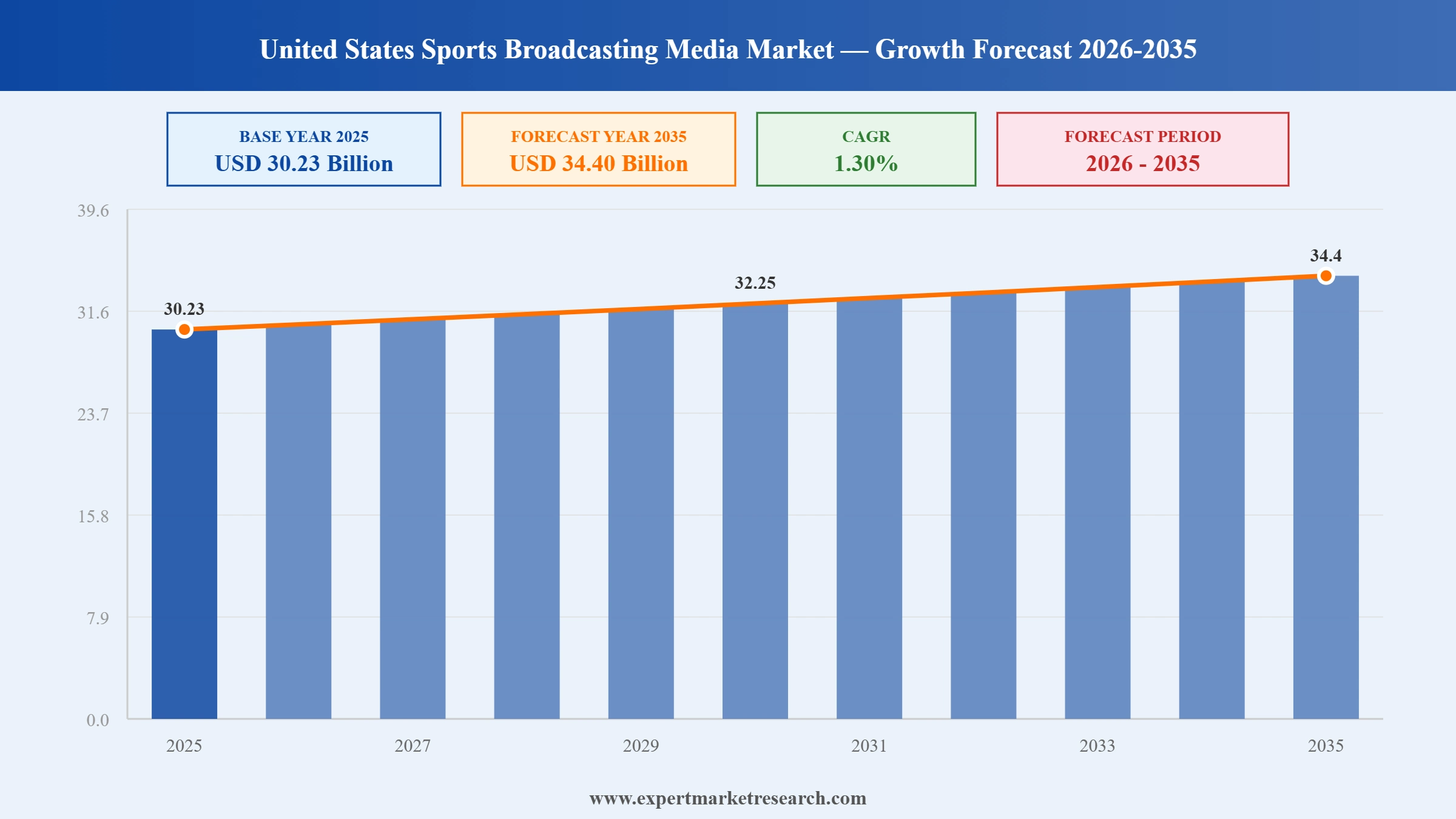

The United States Sports Broadcasting Media Market reached a value of USD 30.23 Billion at 2025 and is projected to expand at a CAGR of around 1.30% during the forecast period of 2026-2035. With rapid growth in online and mobile sports streaming, accelerating shift toward subscription-based revenue models, record-breaking media rights deals across major professional leagues, and rising viewership for women's sports and major international events, the market is expected to reach USD 34.40 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United States Sports Broadcasting Media Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 30.23 |

| Market Size 2035 | USD Billion | 34.40 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 1.30% |

| CAGR 2026-2035 - Market by Region | Far West | 1.8% |

| CAGR 2026-2035 - Market by Region | Rocky Mountain | 1.6% |

| CAGR 2026-2035 - Market by Type | Mobile Streaming | 2.3% |

| CAGR 2026-2035 - Market by Revenue Model | Subscription-Based | 2.5% |

| 2025 Market Share by Region | Southeast | 15.0% |

The United States sports broadcasting media market is undergoing a structural transformation, driven by the rapid shift of audiences from traditional linear television to digital and mobile streaming platforms, the growing economic value of sports media rights, expanding women's sports viewership, and the integration of new technologies including AI-driven personalisation and immersive viewing experiences.

In February 2024, ESPN, Fox Corporation, and Warner Bros. Discovery announced a joint venture to launch a combined sports streaming service in the United States. The platform is designed to aggregate live sports content from all three companies' extensive media rights portfolios, covering the NFL, NBA, MLB, NHL, college sports, and international events. The announcement represents one of the most significant consolidation moves in US digital sports broadcasting, aiming to create a single destination for live sports streaming and counter the subscriber growth of general entertainment platforms by offering a comprehensive, sports-focused subscription product.

In 2024, Amazon's partnership with the National Football League for exclusive Thursday Night Football streaming rights continued to demonstrate the transformative shift of premium live sports content toward digital-first distribution. Amazon's Prime Video platform invested heavily in production quality and interactive features including real-time stats overlays and alternative viewing angles, attracting sports fans who have cut traditional cable subscriptions. The deal reinforced the NFL's broader strategy of diversifying its media rights across traditional broadcast, cable, and streaming channels to maximise total audience reach and advertising revenue.

In 2024, NBCUniversal generated record advertising revenues exceeding USD 1.25 billion from its coverage of the Paris Summer Olympics, streaming over 11,000 hours of content through its Peacock platform. Sponsorship revenues from the event reached USD 1.34 billion, reflecting the enormous commercial value of major international sports properties for US broadcasters. The Paris 2024 Olympics demonstrated Peacock's capability as a large-scale live sports streaming platform, reinforcing NBCUniversal's strategy of driving Peacock subscriber growth through exclusive premium sports broadcasting rights and multiplatform content delivery.

In 2024, the National Women's Soccer League secured a landmark four-year USD 240 million media rights deal, marking one of the most significant commercial milestones in US women's sports broadcasting history. The deal, encompassing rights distributed across multiple broadcast and streaming platforms, follows record NCAA Women's Basketball Championship viewership of 10 million for a single game. The transaction reflects a meaningful structural shift in sports broadcasting investment, with advertisers and rights-holders recognising the rapidly expanding audience and commercial potential of women's professional sports programming across the United States.

In 2022, the National Football League completed a landmark media rights package worth approximately USD 110 billion, distributing broadcasting rights across ABC/ESPN, CBS, Fox, NBC, and Amazon Prime Video for an 11-year term extending through 2033. The deal, the most valuable media rights agreement in US sports history, secured exclusive live game streaming rights for Amazon Prime Video for Thursday Night Football and established a framework for the continued migration of premium sports content to digital platforms. The agreement continues to underpin the financial structure of US sports broadcasting and shapes strategic investment decisions across all major broadcasting and streaming operators.

The migration of live sports content from traditional cable and broadcast television to digital streaming platforms is the most consequential structural trend reshaping the US sports broadcasting market. In 2024, online and mobile streaming channels each grew at a CAGR of 1.4%, outpacing linear television. Amazon's exclusive Thursday Night Football streaming, NBCUniversal's Peacock achieving record sports viewership during the Paris Olympics, and the joint ESPN-Fox-Warner Bros. Discovery streaming platform announcement all exemplify this fundamental shift. United States Sports Broadcasting Media Market growth is increasingly being driven by digital-first distribution strategies, as consumers expect live sports access across smartphones, connected TVs, and tablets on demand.

The subscription-based revenue model is the fastest-growing segment in the US sports broadcasting market, projected to grow at a CAGR of 1.5% through 2035. Consumer willingness to pay for ad-free, exclusive access to premium live sports content has fuelled the rapid subscriber growth of platforms including ESPN+, Peacock, and Paramount+ Sports. In 2024, NBCUniversal's Peacock streaming service used the Paris Olympics to drive subscription growth, while the planned ESPN-Fox-Warner Bros. Discovery joint streaming venture targets sports fans willing to consolidate their subscriptions. Ad-supported streaming tiers are also expanding, with major platforms introducing lower-cost ad-supported options to broaden their accessible audience.

Women's sports have emerged as one of the fastest-growing content categories in US sports broadcasting, with record-breaking viewership, rights deals, and sponsorship revenues transforming the economic model for women's leagues and events. The National Women's Soccer League's USD 240 million media rights deal in 2024 and peak viewership of 10 million for the NCAA Women's Basketball Championship signal a fundamental shift in how broadcasters and advertisers value women's sports content. Networks and streaming platforms are increasingly competing for exclusive women's sports rights, recognising the expanding demographic reach and strong advertiser demand for content targeting female audiences aged 18 to 49.

Artificial intelligence, augmented reality, and advanced data analytics are being deployed across US sports broadcasting to enhance production quality, personalise content delivery, and improve viewer engagement. In March 2024, DeepMind's TacticAI tool was deployed to analyse corner kick strategies for Liverpool FC, demonstrating AI's potential to transform sports analytics and broadcast commentary depth. US broadcasters are increasingly leveraging AI for automated highlight generation, real-time stat overlays, personalised content feeds, and second-screen experiences that deepen fan engagement and increase time spent on platform, creating new advertising and subscription revenue opportunities.

The Expert Market Research's report titled “United States Sports Broadcasting Media Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

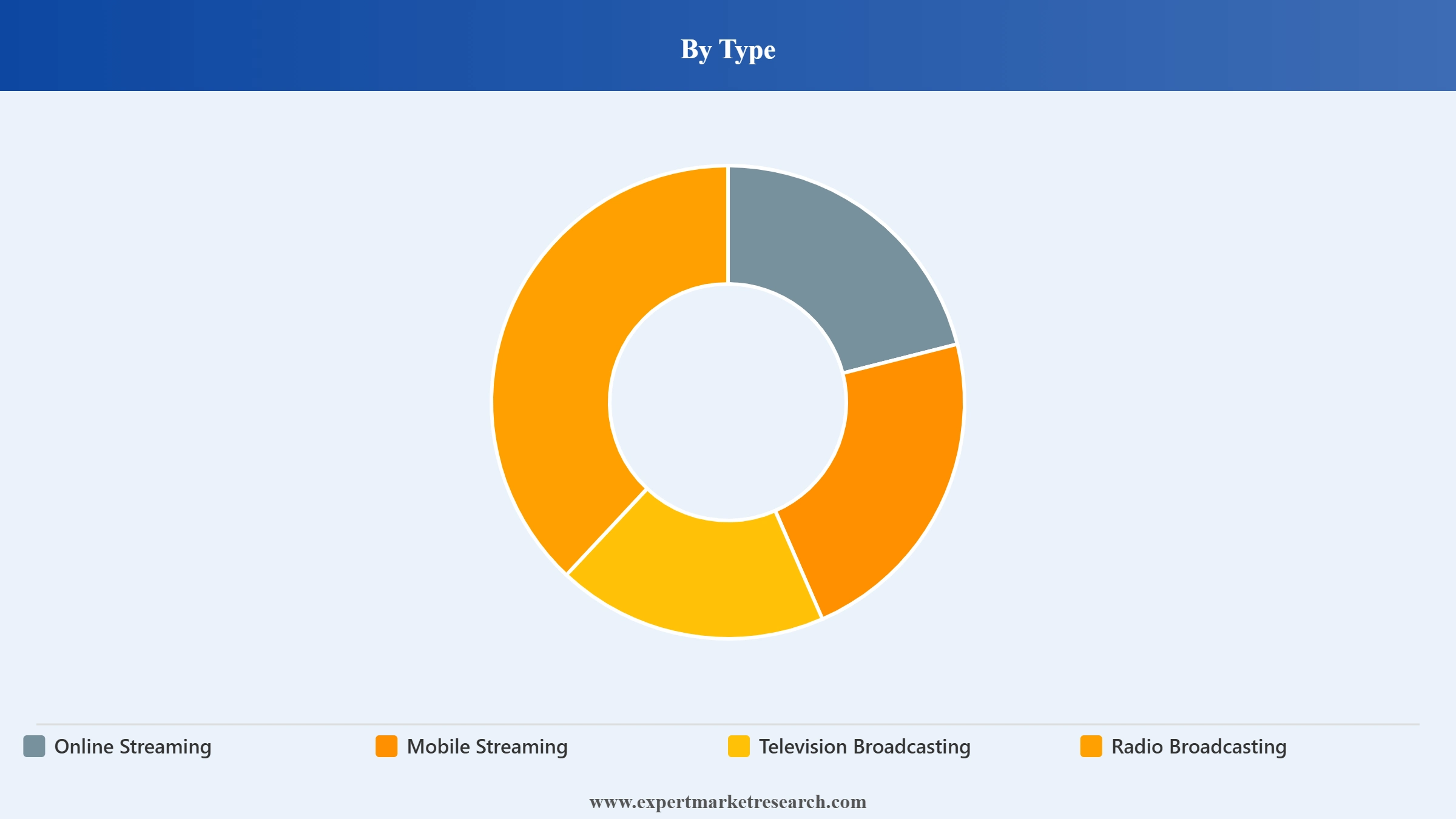

Market Breakup by Type

Key Insight: Television Broadcasting remains the largest broadcasting channel by revenue in the US sports media market, anchored by the dominance of the NFL, NBA, MLB, and NHL across major networks including ABC/ESPN, CBS, Fox, and NBC. However, Online Streaming and Mobile Streaming are both growing at a CAGR of 1.4%, reflecting accelerating consumer migration to digital-first viewing. Television and Radio Broadcasting both grow at approximately 1.2%, as they continue to serve important demographics, particularly older viewers and commuter audiences, while facing structural headwinds from cord-cutting and digital competition. The shift to multiplatform distribution is now a commercial imperative for all major US sports rights holders.

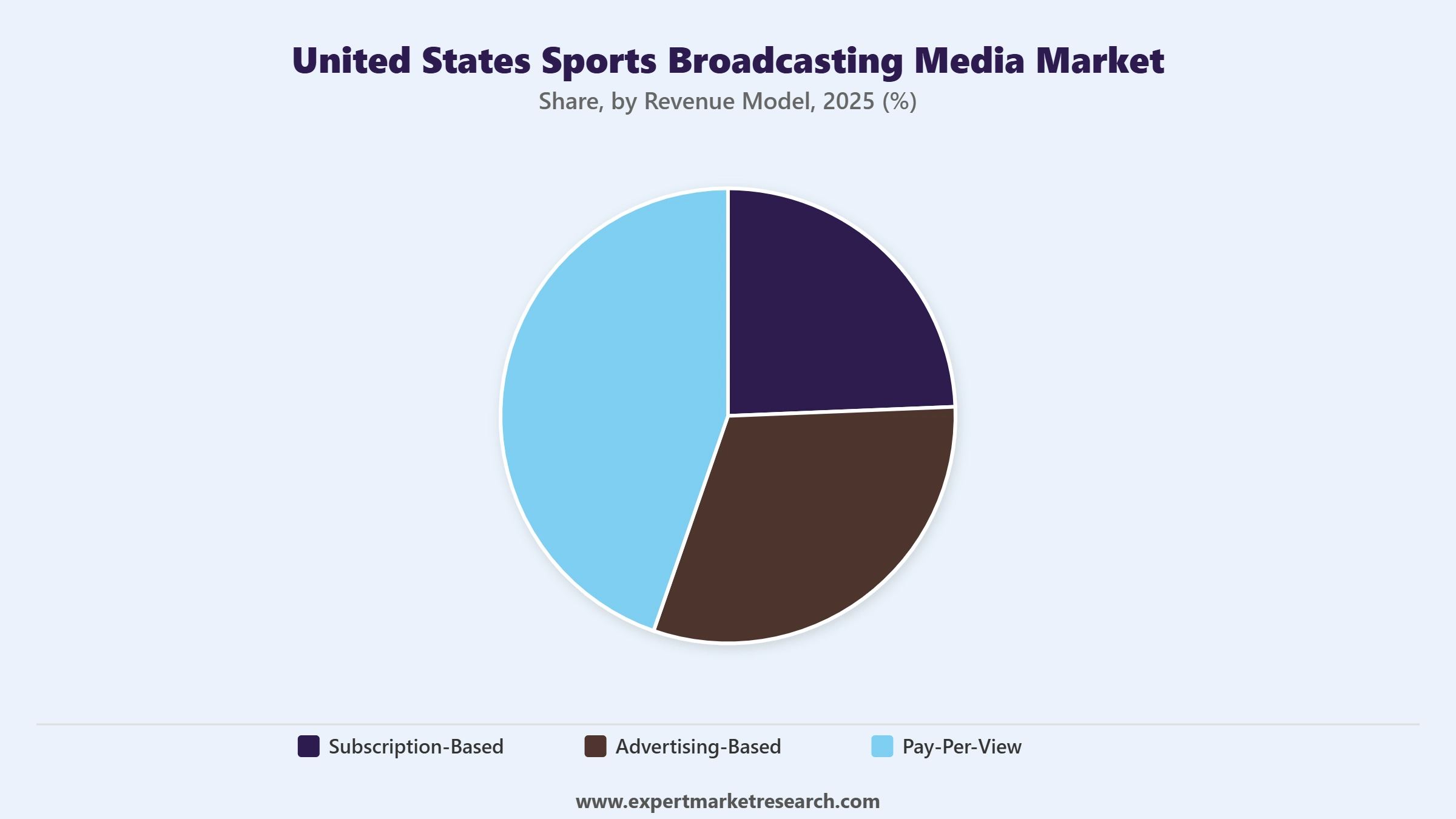

Market Breakup by Revenue Model

Key Insight: The Subscription-Based revenue model leads growth among US sports broadcasting revenue streams, projected at a CAGR of 1.5% through 2035. Consumer preference for premium, ad-free live sports content has driven ESPN+, Peacock, Paramount+, and DAZN to build dedicated sports subscription portfolios. Advertising-Based models grow at a CAGR of 1.4%, supported by continued demand from brands seeking live sports audiences, which remain among the most commercially valuable and hard-to-skip ad environments. Pay-Per-View grows more slowly at 1.2%, maintaining its niche appeal for premium combat sports events including boxing and mixed martial arts, where fans demonstrate strong willingness to pay for individual event access.

Market Breakdown by Region

Key Insight: The Far West region leads growth expectations with a CAGR of 1.5% through 2035, supported by California's dominant role in digital media consumption, high broadband and 5G penetration, and a strong base of sports fans across professional franchises in Los Angeles, San Francisco, and Seattle. New England and the Mideast register moderate growth at CAGRs of 1.2% and 1.1%, reflecting stable but slower adoption of newer streaming formats compared to leading regions. The Plains and Great Lakes regions grow at 1.0%, with smaller populations and less mature digital sports streaming infrastructure moderating growth. The Southeast and Southwest are growing regions as digital infrastructure investment expands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Broadcasting Channel

Television Broadcasting commands the dominant channel share of the US sports broadcasting media market, reflecting the enduring commercial strength of major league rights deals that continue to anchor the largest annual broadcast audiences in American media. The NFL's USD 110 billion broadcast package, signed in 2022 and extending through 2033, underpins the revenue floors for ABC/ESPN, CBS, Fox, and NBC, all of which generate significant affiliate fee and advertising income from sports programming. While television's share is gradually being eroded by digital migration, live sports remain the most resilient programming category for traditional broadcast, as they continue to deliver the mass simultaneous audiences that premium advertisers value most highly.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Revenue Model

The Subscription-Based model is the fastest-growing revenue segment in the US sports broadcasting market, with platforms including ESPN+, Peacock Sports, and Paramount+ Sports investing heavily in exclusive content to drive and retain subscribers. The Paris 2024 Olympics catalysed significant Peacock subscriber gains, demonstrating the power of marquee sports events to acquire new paying subscribers at scale. Advertising-Based models maintain broad reach and remain essential for mid-tier sports programming and regional coverage, while Pay-Per-View models retain their premium positioning in combat sports, where boxing and UFC events consistently demonstrate strong consumer willingness to pay for individual event access at premium price points.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Region

The Southeast region commands the largest share of US sports broadcasting media consumption by region, driven by its large population base, high cable television penetration, and intense regional sports loyalty across NFL, NBA, MLB, and college football markets. The Southeast accounts for a disproportionate share of major league sports viewership in states including Florida, Texas, Georgia, and Tennessee. The Far West region, anchored by California’s large metropolitan media markets, is the second-most significant region by advertising revenue, with Los Angeles and San Francisco serving as major centres for both sports media production and high-value sports advertising consumption. New England and the Mideast maintain strong per-capita sports viewership intensity driven by concentrated fanbases around marquee franchises.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Far West region leads the US sports broadcasting media market in digital growth terms, driven by California's outsized role in technology adoption, streaming platform headquarters, and sports franchise density. Los Angeles, home to the Rams, Chargers, Lakers, Clippers, Dodgers, and Angels among others, generates year-round sports broadcasting demand across both traditional and digital channels. The region's high-income consumer base and advanced digital infrastructure support above-average subscription rates for premium sports streaming platforms. Silicon Valley's concentration of technology companies also drives innovation in sports broadcast technology, including AI-driven personalisation and interactive viewing features that are shaping the future of sports media consumption nationally.

The Southeast is emerging as a high-growth region for digital sports broadcasting adoption, supported by rapid population growth across Florida, Georgia, the Carolinas, and Tennessee, and expanding digital infrastructure investment driven by major telecommunications and broadband providers. The region's growing base of professional sports franchises, including NFL teams in Tampa Bay, Miami, Atlanta, and Charlotte, and NBA teams in Miami and Atlanta, generates sustained sports media demand. College sports, particularly the SEC football conference, command exceptionally strong regional viewership and sponsorship revenues across the Southeast, maintaining high demand for both linear television and digital sports content among highly engaged fan bases.

The United States sports broadcasting media market is dominated by a small number of large media conglomerates that hold the majority of premium sports rights across major professional and collegiate leagues. The Walt Disney Company through ESPN and ESPN+, NBCUniversal through NBC Sports and Peacock, Fox Corporation through Fox Sports, and Paramount Global through CBS Sports collectively control the majority of broadcast and cable sports rights. Amazon Prime Video has emerged as a significant digital-native rights holder following its exclusive Thursday Night Football agreement, while Warner Bros. Discovery holds NBA and NHL rights through TNT Sports.

Competitive dynamics are shifting as streaming platforms challenge cable incumbents for both audience share and rights acquisition, driving rights fee inflation and increasing content investment requirements across all market participants. The announced ESPN-Fox-Warner Bros. Discovery joint streaming service reflects the industry's recognition that consolidating digital sports content on single, sports-focused platforms is necessary to retain subscribers in an increasingly fragmented media landscape. Regional sports networks face particular pressure as regional sports rights deals come up for renegotiation in an environment of declining traditional pay-TV subscribers.

Founded in 1923 and headquartered in Burbank, California, The Walt Disney Company operates ESPN as the dominant US cable sports network. ESPN holds extensive rights across the NFL, NBA, MLB, college football, and international sports. ESPN+ serves as its direct-to-consumer streaming product with over 24 million subscribers. Disney is building toward a standalone ESPN flagship streaming service targeting cord-cutters and is a partner in the announced joint sports streaming venture with Fox and Warner Bros. Discovery.

Founded in 2019 and headquartered in New York City, Fox Corporation operates Fox Sports as a major US sports broadcasting network holding rights to the NFL's NFC package, the UEFA Champions League, NASCAR, MLB, and college football. Fox Sports 1 and Fox Sports 2 anchor its cable portfolio. Fox is a co-founder of the ESPN-Fox-Warner Bros. Discovery joint sports streaming service and has positioned itself as a sports-first media company following the sale of its entertainment assets to Disney in 2019.

Founded in 1926 and headquartered in New York City, NBCUniversal is a subsidiary of Comcast Corporation operating NBC Sports and Peacock. NBCUniversal holds rights to the NFL's AFC Sunday package, the Olympics, Premier League soccer, PGA Tour golf, NASCAR, and NHL. Its Paris 2024 Olympics coverage generated record advertising revenues exceeding USD 1.25 billion. Peacock is its primary sports streaming vehicle, having demonstrated meaningful subscriber acquisition capacity through live sports simulcasting and exclusive content.

Founded in 2006 and headquartered in New York City, Paramount Global operates CBS Sports as a leading broadcast and streaming sports platform. CBS Sports holds the NFL's AFC package and major college football and basketball rights. Paramount+ serves as its streaming platform offering live CBS Sports events. The company competes for sports rights alongside established broadcast networks and streaming challengers, leveraging its CBS broadcast reach and Paramount+ subscriber base to maintain competitive positioning in live NFL and NCAA coverage.

Other key players in the market are Warner Bros. Discovery (TNT Sports), Amazon (Prime Video), and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a strategic edge in the United States Sports Broadcasting Media Market 2026 with our comprehensive research report. Access detailed analysis on digital migration trends, subscription model growth, record-breaking media rights dynamics, and regional market opportunities shaping the future of sports content delivery in America. Whether you are a broadcaster negotiating rights, a streaming platform investing in sports content, or an advertiser optimising media spend, our report delivers the clarity and intelligence to sharpen your competitive positioning. Download your complimentary sample today.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 30.23 Billion.

The market is projected to grow at a CAGR of 1.30% between 2026 and 2035.

The market is projected to grow during the forecast period 2026-2035 to reach USD 34.40 Billion for 2035.

The key players in the market include The Walt Disney Company (ESPN/ESPN+), Fox Corporation (Fox Sports), NBCUniversal (Comcast Corporation), Paramount Global (CBS Sports), Warner Bros. Discovery (TNT Sports), Amazon (Prime Video), and Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Revenue Model |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.