Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The United States e-cigarette and vape market reached a value of USD 31.25 Billion at 2025 and is projected to expand at a CAGR of around 25.00% during the forecast period of 2026-2035. With expanding FDA product authorisations, accelerating adoption of closed-pod systems, growing momentum behind synthetic nicotine, and tightening state-level disposable regulations, the market is expected to reach USD 291.04 Billion by 2035.

Compound Annual Growth Rate

25%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United States E-Cigarette and Vape Market growth is being shaped by an evolving FDA framework, the rapid spread of state-level disposable controls, the rise of synthetic nicotine, and the migration of consumers from open-system devices to closed-pod systems with embedded age-assurance technology.

In April 2026, Philip Morris International announced that the U.S. Food and Drug Administration had renewed Modified Risk Tobacco Product orders covering the IQOS 2.4 and IQOS 3.0 system holders and chargers, alongside the HEETS Amber, Green Menthol and Blue Menthol consumables. The reauthorisation continues PMI's ability to communicate reduced-exposure messaging to adult consumers and reinforces the regulatory legitimacy of heated-tobacco platforms within the broader US e-cigarette and vape ecosystem, supporting category expansion alongside ENDS products.

R.J. Reynolds Vapor Company, a subsidiary of Reynolds American, began a regional pilot of the Vuse One disposable vape across South Carolina, Florida and Georgia in the fourth quarter of 2025. The product extends the Vuse portfolio – which already leads US closed-system pod share – into the disposable segment, with broader flavour variety and laboratory-produced synthetic nicotine. A Premarket Tobacco Product Application is pending with the FDA, positioning Reynolds to compete with illicit imported disposables on convenience while pursuing federal authorisation.

In October 2025, JUUL Labs disclosed plans to bring its second-generation JUUL2 device to the United States, pending FDA marketing authorisation. JUUL2 introduces a dual-layer security architecture combining app-based identity verification – including facial recognition on compatible smartphones – with a Bluetooth-paired chip embedded in each pod that locks devices to verified adult accounts. The development positions age-assurance technology as a strategic lever for restoring the brand's regulatory standing and differentiating premium pod systems from illicit disposables.

On 17 July 2025, the U.S. Food and Drug Administration granted marketing orders to JUUL Labs for the JUUL device along with Virginia tobacco-flavoured and menthol-flavoured JUULpods at 3% and 5% nicotine concentrations. This was only the third time the FDA had authorised menthol-flavoured electronic nicotine delivery systems through the PMTA pathway, restoring legal access for one of the country's most recognised closed-pod brands and tightening competitive dynamics versus Vuse and NJOY in the regulated channel.

Philip Morris International began rolling out its heated-tobacco IQOS device in the United States from May 2025, with initial commercial launches in Austin, Texas, followed by Fort Lauderdale, Florida. The launch was supported by experiential brand activations and positioned IQOS as a smoke-free harm-reduction alternative to combustible cigarettes. The pilot represents PMI's most significant US push for the device since regaining commercial control of the IQOS franchise from Altria, with the company eyeing 2026 as a tipping point for smoke-free products.

On 9 March 2026, the FDA released draft guidance establishing a risk-based evidentiary framework for flavoured electronic nicotine delivery system applications. Lower-youth-appeal flavours such as menthol, mint, coffee and spice face a more workable threshold, while fruit, candy and dessert flavours must clear the highest evidentiary bar. The framework is widely viewed as a pivot from a near-blanket flavour ban toward a structured pathway that could enable legal market re-entry for compliant adult-focused products, accelerating United States E-Cigarette and Vape Market growth across regulated channels.

Texas Senate Bill 2024, effective 1 September 2025, banned the sale of pre-filled disposable e-cigarettes manufactured in China, including via vending machines. Tennessee's SB 763 (1 July 2025) introduced mandatory product registration, ID verification and steep penalties for underage sales, while North Carolina restricted retail to FDA-authorised products. Combined with Chinese disposable exports exceeding USD 10.6 billion in 2025, these moves are reshaping competitive dynamics in favour of domestically marketed, PMTA-compliant brands.

Closed-pod systems are gaining share over open-system mods, with manufacturers leaning into synthetic nicotine to navigate tobacco-derived nicotine restrictions and supply uncertainty. Reynolds' Vuse One disposable, launched in late 2025, uses laboratory-produced synthetic nicotine, while major brands continue to invest in mesh-coil atomisers, dual-coil architectures and higher-capacity batteries. The shift reflects consumer preference for consistent dosing, simpler maintenance and validated nicotine quality, and underpins premium-tier growth across regulated retail channels.

Manufacturers are embedding hardware- and software-based age-assurance features in next-generation devices to address regulatory and public-health concerns. JUUL2's Bluetooth-paired pods and biometric app verification, disclosed in October 2025 ahead of an FDA filing, exemplify a broader industry pivot toward identity-bound activation. Reynolds' Vuse Pro PMTA submission similarly relies on age-gating to differentiate from disposable substitutes. These features are emerging as a strategic pathway to re-establish legitimacy with adult consumers while supporting future FDA authorisations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research’s report titled “United States E-Cigarette and Vape Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

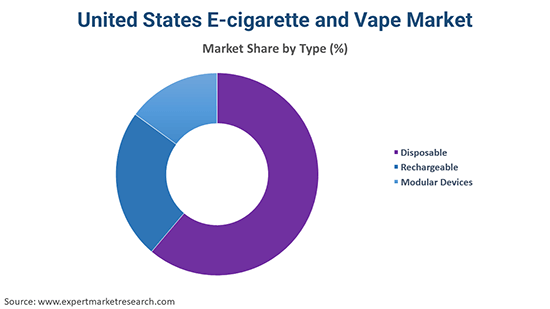

Market Breakup by Type

Key Insight: Disposables dominate the United States e-cigarette and vape landscape, supported by the lowest entry price among all formats, no-maintenance design and rapid flavour rotation that resonates with adult smokers transitioning away from combustibles. Brands such as Vuse, NJOY and recent entrants leveraging synthetic nicotine have intensified competition, while state-level disposable bans on Chinese-manufactured units (Texas SB 2024) are reshaping which products legally reach shelves. Rechargeables and modular systems remain anchored among value-conscious and enthusiast users respectively, with mesh-coil atomisers, longer batteries and larger e-liquid capacity supporting premium positioning.

Market Breakup by Component

Key Insight: E-liquids represent the highest-frequency consumable in the US market, with refill formats supporting strong recurring revenue across rechargeable and modular platforms. Atomisers continue to gain share on the back of mesh-coil upgrades, dual-coil architectures and improved compatibility across closed-pod systems, while vape mods remain the technology backbone of the enthusiast segment. Cartomizers, although a more mature sub-segment, retain relevance in cig-a-like devices and certain entry-level pods. Component innovation – particularly around coil longevity, flavour fidelity and battery efficiency – is a critical lever for brands competing in PMTA-compliant retail.

Market Breakup by Composition

Key Insight: Tobacco and menthol compositions hold privileged status under the FDA's PMTA framework, with all currently authorised ENDS products falling within these categories. The March 2026 risk-based flavour guidance creates a structured pathway for additional non-tobacco compositions to reach the market, with sweeter profiles facing the highest evidentiary bar. Nicotine-free formulations are gaining traction with consumers seeking sensory rituals without dependence, supported by synthetic ingredient innovation. Flavour diversity remains a critical battleground, balancing adult preference for variety with the FDA's continued focus on minimising youth appeal.

Market Breakup by Battery Mode

Key Insight: Automatic battery-mode devices dominate the closed-pod and disposable categories, where draw-activated firing simplifies the consumer experience and aligns with the convenience-led purchase patterns of adult smokers transitioning from combustibles. Manual battery devices retain a strong position in modular systems used by enthusiast consumers who value firing-button control, variable wattage and customised performance.

Market Breakup by Distribution Channels

Key Insight: Offline channels – convenience stores, vape specialty retailers and tobacco outlets – continue to anchor United States e-cigarette and vape volumes, supported by impulse purchase behaviour and the regulatory requirement for in-person age verification. Online channels are increasingly constrained by state-level restrictions on flavoured product e-commerce and tightened shipping rules, but remain critical for refill consumables, accessories and modular hardware. The interplay between in-store availability of FDA-authorised SKUs and digital discovery is reshaping omnichannel strategies.

Market Breakup by Region

Key Insight: Regional dynamics are highly differentiated. California combines a large adult smoker population with a strict flavoured-product framework, channelling demand toward FDA-authorised tobacco and menthol pods. Florida benefits from dense convenience retailing and was selected by Reynolds for its Vuse One disposable pilot. Texas, post-SB 2024, has effectively reset its disposable shelf set toward domestic and PMTA-pending products, while also hosting Philip Morris' IQOS launch in Austin. New York's regulatory environment skews demand toward closed-pod and heated-tobacco categories. Investment, company expansions and PMTA filings are increasingly concentrated in these four states.

By Type: The disposable category is the dominant sub-segment, capturing the largest share of US e-cigarette unit volumes through 2025. Affordability, no-maintenance use and rapid flavour rotation explain its lead, with brands such as Vuse, NJOY and emerging synthetic-nicotine entrants intensifying competition. The Reynolds Vuse One disposable pilot launched in Q4 2025 across South Carolina, Florida and Georgia underscores how legacy players are aggressively repositioning toward this format to recapture share previously concentrated in unauthorised Chinese disposables, particularly following Texas SB 2024.

By Composition: Tobacco and menthol formulations hold the leading market share within the FDA-authorised universe, given that all currently legal ENDS products fall within these profiles. Adoption is highest among adult former smokers seeking familiar sensory experiences and consistent dosing. The July 2025 FDA authorisation of JUUL Virginia tobacco and menthol pods – only the third menthol ENDS authorisation – reinforces this dominance, while the March 2026 risk-based flavour framework signals a measured opening for additional compositions over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

California is the leading state-level market, supported by a large adult-smoker base, dense urban retail networks and a regulatory framework that pushes demand toward FDA-authorised tobacco and menthol pods. Major players including Reynolds (Vuse), JUUL Labs and Altria-owned NJOY operate dense distribution footprints across the state, while specialty vape retailers anchor adult-focused premium platforms. Investments in synthetic nicotine and closed-pod manufacturing increasingly target California's regulated channels, with company expansions concentrated around Los Angeles and the Bay Area. Demand drivers include high disposable income, strong harm-reduction awareness and a steady migration of adult smokers from combustibles toward heated-tobacco and ENDS alternatives.

Florida is a close second, combining a fast-growing population with permissive convenience-store distribution that favours disposable and closed-pod formats. Reynolds American selected Florida – alongside South Carolina and Georgia – for its Q4 2025 Vuse One disposable pilot, while Philip Morris included Fort Lauderdale among its early IQOS rollout cities. The state also hosts substantial NJOY distribution under Altria, and convenience-led demand is being reinforced by tourism flows. Demand drivers include warm-weather lifestyle factors, expanding multicultural consumer bases and a relatively flexible state regulatory regime that has accelerated company expansions and category trial.

The United States e-cigarette and vape market is moderately consolidated at the top of the FDA-authorised channel, with Vuse (Reynolds American), NJOY (Altria) and JUUL accounting for the bulk of legally compliant pod and disposable volumes. Outside this regulated core, an extensive grey-market segment of imported disposables continues to compete on price and flavour, prompting both legislative and corporate responses.

Competitive priorities now centre on PMTA pipeline depth, age-assurance technology, synthetic nicotine integration and harm-reduction positioning. Heated-tobacco entrants such as Philip Morris (IQOS) and adjacent nicotine-pouch leaders are expanding the smoke-free category alongside traditional ENDS, while M&A activity – exemplified by Altria's USD 2.75 billion NJOY acquisition – continues to reshape the addressable share opportunity for the leading players profiled below.

Founded in 2004 (current form) and headquartered in Winston-Salem, North Carolina, Reynolds American is the BAT-owned subsidiary behind the Vuse pod system, the Vuse One disposable and the age-gated Vuse Pro platform. Vuse holds the leading FDA-authorised pod share in the United States, supported by a deep PMTA pipeline, mesh-coil innovation and synthetic nicotine integration in newer SKUs.

Founded in 1822 and headquartered in Richmond, Virginia, Altria entered the ENDS category as a portfolio anchor through its USD 2.75 billion acquisition of NJOY in 2023. The group's competitive priorities span FDA-authorised pod and disposable products, oral nicotine pouches and harm-reduction messaging, with NJOY positioned as the regulated alternative to Vuse and JUUL.

Founded in 2008 (post-spin-off) and headquartered in Stamford, Connecticut, Philip Morris International is rolling out IQOS heated-tobacco devices across the United States, having begun in Austin in 2025. IQOS holds Modified Risk Tobacco Product status reauthorised by the FDA in April 2026, anchoring PMI's smoke-free strategy alongside the rapidly expanding ZYN pouch franchise.

Founded in 1996 and headquartered in Bristol, United Kingdom, Imperial Brands operates in the United States across mass-market combustibles, the blu e-cigarette franchise and adjacent next-generation product trials. Its US capabilities span manufacturing, distribution and retail trade marketing, with a strategic focus on disciplined capital allocation in next-generation nicotine categories.

Other key players in the market are British American Tobacco, Turning Point Brands, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The United States e-cigarette and vape market operates within a complex and shifting regulatory environment that poses significant challenges for manufacturers. Every product requires FDA marketing authorization before legal sale, yet the agency has cleared only a limited number of devices, leaving most products in regulatory limbo. Fruit, candy, and dessert flavors continue to face a heightened evidentiary burden due to documented youth appeal, while persistent state-level opposition adds further compliance complexity for companies operating nationally.

Several factors restrain market expansion. A vast majority of disposable vapes from popular brands lack FDA authorization, exposing retailers to enforcement risk and constraining legitimate channel growth. Sustained public health scrutiny, youth-access concerns, and the unresolved status of countless pending applications create planning uncertainty, while declining teen vaping rates intensify pressure on companies to demonstrate population-level benefit.

Meaningful opportunities are nonetheless emerging. The first-ever authorization of fruit-flavored products using rigorous age-verification technology signals a potential pathway for compliant flavor innovation. Positioning devices as smoking-cessation alternatives for adult smokers, alongside investment in device access restriction technology and harm-reduction messaging, offers manufacturers durable avenues for differentiated, regulation-aligned growth.

Discover the latest insights on the United States E-Cigarette and Vape Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on product innovations, consumer demand and top growth regions across PMTA-authorised pods, disposables and heated-tobacco platforms. Whether you are launching a new ENDS device, expanding a synthetic-nicotine portfolio or evaluating M&A, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving United States E-Cigarette and Vape industry.

United States Heated Tobacco Products Adoption

United States Nicotine Replacement Therapy Challenges

United States E-Liquid Market Trends

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 31.25 Billion.

The market is projected to grow at a CAGR of 25.00% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035 to reach USD 291.04 Billion by 2035.

Key drivers include the migration of adult smokers from combustibles to harm-reduction products, the maturing FDA PMTA framework, the rise of synthetic nicotine, accelerating adoption of closed-pod and disposable formats, and the introduction of age-assurance technology in next-generation devices such as JUUL2 and Vuse Pro.

By type, the market is segmented into disposable, rechargeable and modular devices. Disposables currently lead the market, propelled by ease of use, low entry price and rapid flavour rotation, with rechargeables anchoring the value-tier and modular systems serving the enthusiast segment.

Key trends include the FDA's risk-based flavour PMTA framework (March 2026), state-level disposable bans on Chinese-made products, the migration toward closed-pod systems and synthetic nicotine, and the embedding of age-assurance technology in next-generation devices.

The key players in the market include Reynolds American Inc., Imperial Brands PLC, Altria Group, Inc., Philip Morris International Inc., British American Tobacco, Turning Point Brands and Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Component |

|

| Breakup by Composition |

|

| Breakup by Battery Mode |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.