Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

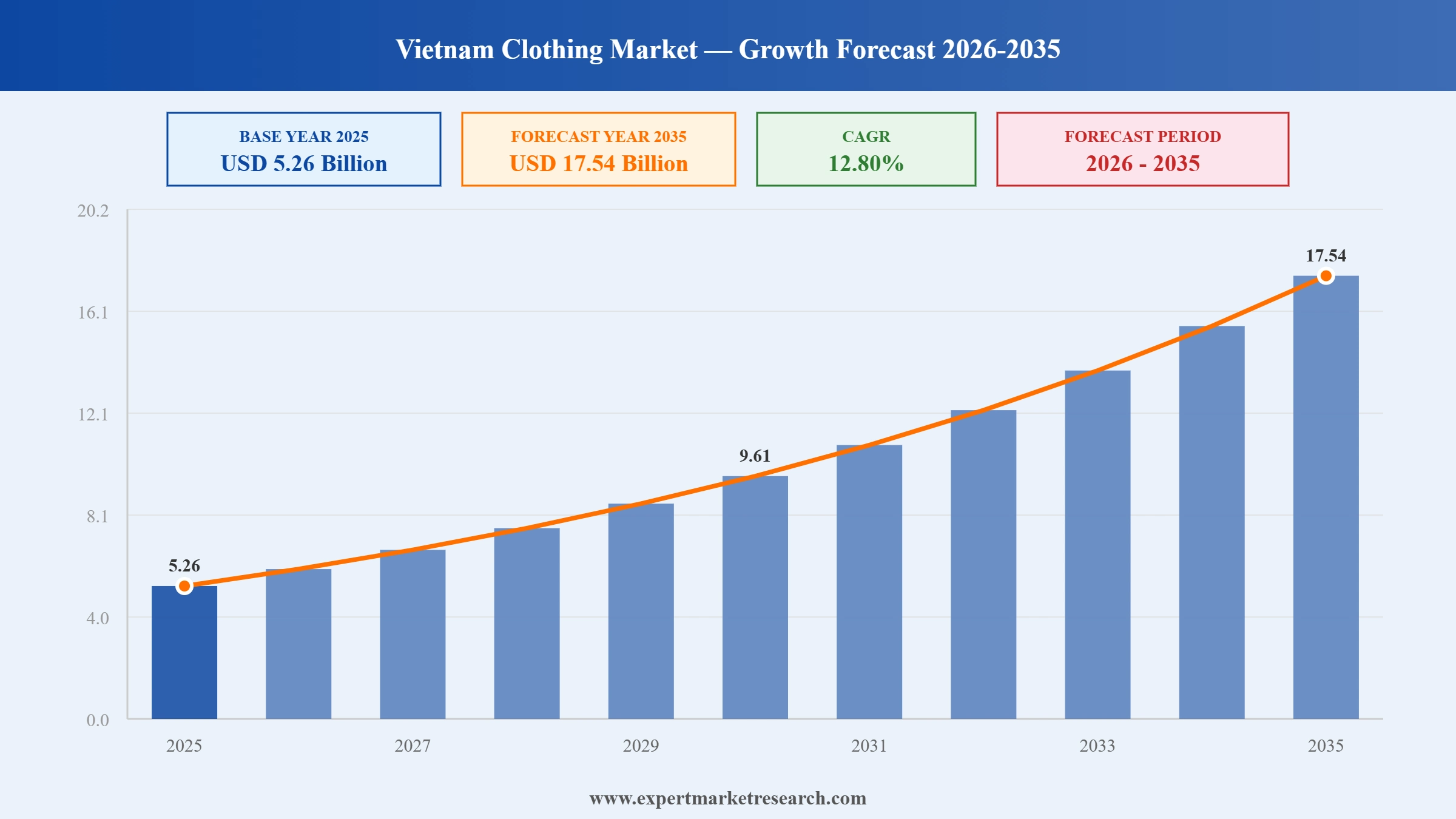

The Vietnam Clothing Market reached a value of USD 5.26 Billion at 2025 and is projected to expand at a CAGR of around 12.80% during the forecast period of 2026-2035 to reach USD 17.54 Billion by 2035. With accelerating nearshoring investment by global fashion brands, a rapidly digitalizing retail landscape, a growing domestic consumer base driven by middle-class expansion, and rising demand for premium and sustainable apparel.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Vietnam Clothing Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

5.26 |

|

Market Size 2035 |

USD Billion |

17.54 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

12.80% |

|

CAGR 2026-2035 - Market by Region |

Southeast |

14.5% |

|

CAGR 2026-2035 - Market by Region |

Red River Delta |

13.7% |

|

CAGR 2026-2035 - Market by Price Range |

Premium and Luxury |

14.4% |

|

CAGR 2026-2035 - Market by End Use |

Women |

13.6% |

|

2025 Market Share by Region |

Southeast |

29.1% |

Vietnam's clothing market is being reshaped by nearshoring dynamics, digital retail expansion, sustainability-led manufacturing, and rising premium consumption, each trend reinforcing the country's dual role as a global production powerhouse and a fast-maturing domestic consumer market.

Vietnam's fashion industry officially targeted USD 48 billion in textile and garment exports for 2026, with an ambitious strategy targeting USD 50 billion positioning the sector as a central pillar of Vietnam's overall USD 550 billion import-export target for the year, while domestic branded fashion retail reached USD 3.5 billion amid fierce competition between international fast fashion giants and rising local brands.

A US Supreme Court ruling restructured apparel sourcing economics, reducing Vietnam's effective tariff rate from 46% to 10% under Section 122 making Vietnamese factories competitive again almost overnight, with orders that had been redirected to Mexico and Central America now being reconsidered for Vietnam-based production.

Vietnam's textile and garment export sector entered 2026 targeting USD 48 billion in exports, but faced tightening profit margins due to a combination of rising wages (averaging USD 300/month three times higher than Bangladesh), input cost inflation, and residual US tariff pressures of 20–40% on Vietnamese apparel, signaling a structural shift from volume-based to value-added manufacturing.

Fast-fashion giant Shein took a major step in its "China + 1" strategy by leasing a 15-hectare warehouse near Ho Chi Minh City to consolidate garment inventory sourced from Vietnamese contractors before export, shielding the company from US-China tariff adjustments and signaling Vietnam's rising status as a global fast fashion manufacturing anchor.

Vietnam's clothing industry is a direct beneficiary of the global nearshoring trend, as international brands reduce dependence on China-based production due to geopolitical risk and rising tariff pressures. Vietnam offers a compelling alternative: competitive labour costs, a skilled garment workforce, and 16 operational free trade agreements covering major markets. This structural shift continues to attract significant inflows of new manufacturing capacity and sourcing contracts, supporting Vietnam clothing market growth well beyond domestic consumption levels. In May 2025, Shein formalised this trajectory by leasing a 15-hectare warehouse near Ho Chi Minh City, consolidating inventory from Vietnamese contract factories before international export.

Digital retail is fundamentally changing how Vietnamese consumers engage with clothing brands. By the end of 2024, e-commerce accounted for 27.5% of total apparel value sales in Vietnam, with platforms such as Shopee, Lazada, and cross-border options like Shein and Taobao gaining rapid traction among urban and youth demographics. This digital acceleration is pushing both domestic brands and international players to invest in social commerce, influencer-led marketing, and mobile-first shopping experiences. In February 2025, the VIATT trade fair in Ho Chi Minh City attracted over 463 exhibitors, partly reflecting accelerating demand for digitally integrated supply chain and fulfilment solutions within the clothing sector.

International buyers and Vietnamese manufacturers are jointly committing to greener production, driven by EU sustainability regulations, ESG mandates from global retail groups, and growing consumer awareness of environmental impact. Factories across Vietnam are investing in solar-powered production, closed-loop water systems, and certified eco-materials. In 2024, Vietnamese denim manufacturer Saitex opened a LEED-certified production facility operating on 98% recycled water, setting a new benchmark for sustainable garment manufacturing in Southeast Asia and reinforcing Vietnam's appeal to environmentally conscious international clothing brands.

Vietnam's rapidly expanding middle class and growing cohort of high-net-worth urban consumers are fuelling strong interest from global luxury and premium fashion houses. Rising incomes in Ho Chi Minh City and Hanoi are accelerating aspirational spending on branded clothing, with consumers trading up from mass-market products toward premium labels. In 2024, luxury brands including Hermes, Piaget, and Cartier made high-profile expansions across Vietnam's prime retail corridors, capitalising on a demographic transition that is expected to see Vietnam's middle class surpass 56 million people by 2030.

The Expert Market Research's report titled "Vietnam Clothing Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Casual wear holds the dominant position in Vietnam's clothing market, driven by a combination of shifting lifestyle preferences, work-from-home culture, and the country's central role as a sourcing hub for global casual apparel brands such as Zara and Uniqlo. Sports and functional wear is gaining rapidly as health awareness, gym culture, and demand for technical textiles grow among Vietnam's urban population, supported by brands like Adidas and Nike, both of which maintain extensive manufacturing operations in the country. Traditional and cultural wear, notably ao dai and festival clothing, retains consistent relevance around Tet and national events, supported by a cultural pride movement among younger Vietnamese designers. Fashion accessories and uniforms round out the segment, growing through e-commerce platforms and Vietnam's expanding hospitality and industrial workforce.

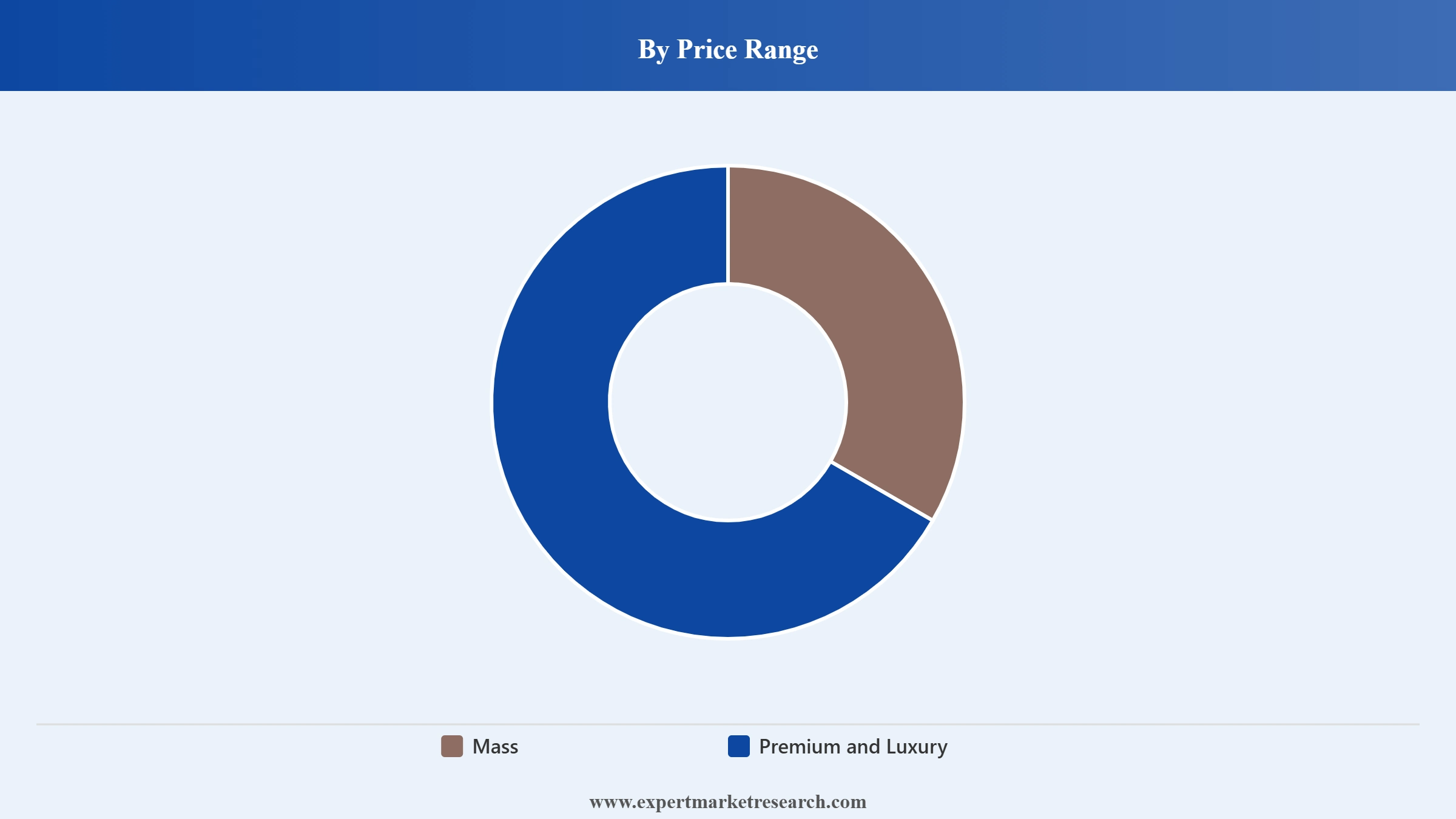

Market Breakup by Price Range

Key Insight: The Mass segment commands the overwhelming share of Vietnam's clothing market, consistent with the country's large base of price-conscious consumers and its role as a production centre for affordable global fast-fashion brands. However, the Premium and Luxury segment is the fastest growing in this segmentation, projected to expand at a CAGR of 14.4% through 2035 as Vietnam's middle class expands and urban consumers increasingly aspire to branded fashion. The Vietnamese luxury goods market reached USD 2.3 Billion in 2024, with clothing being a key component, as international houses such as Louis Vuitton, Hermes, and Chanel deepen their retail presence across Ho Chi Minh City and Hanoi's premium mall corridors.

Market Breakup by End Use

Key Insight: The Women's segment leads clothing consumption in Vietnam, consistent with regional patterns where women drive a disproportionate share of household apparel purchasing decisions and are more actively engaged with fashion trends and brand experimentation. Data from local browser Coc Coc confirms that clothing is the top fashion search category among Vietnamese women, with essential wardrobe staples accounting for over 84% of women's fashion searches. The Men's segment is the second largest, supported by rising professional and casual wear demand, while the Kids and Unisex segments are growing through social media influence and expanding e-commerce options for family fashion shopping.

Market Breakup by Region

Key Insight: The Southeast region, anchored by Ho Chi Minh City, is Vietnam's largest and most dynamic clothing market zone. The city functions as the country's primary garment manufacturing and retail hub, home to hundreds of export-oriented factories and a dense retail environment featuring international and domestic fashion brands. The Red River Delta, centred on Hanoi, is the second-largest region, with strong garment and textile manufacturing infrastructure, skilled labour availability, and a sophisticated retail consumer base. In February 2025, the VIATT trade fair in Ho Chi Minh City attracted over 19,000 industry visitors and 463 exhibitors from 24 countries, confirming the Southeast's central role in driving trade flows, international sourcing relationships, and supply chain investment for the Vietnamese clothing sector.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Casual Wear subsegment accounts for the largest share within the product type segmentation, driven by its alignment with the lifestyles of Vietnam's young, urban, and growing middle-class consumers. The proliferation of remote and hybrid working arrangements, the influence of fast-fashion platforms, and Vietnam's role as a global production centre for everyday apparel all reinforce casual wear's dominance. Globally recognised brands, including Zara, Uniqlo, and H&M, prioritise Vietnam as a sourcing and retail market specifically for casual collections. Uniqlo had expanded to 29 stores nationwide by the end of 2024, a clear indicator of how much consumer appetite for accessible, versatile casual clothing has deepened across Vietnamese urban centres. Sports and Functional Wear is the fastest-growing product type, with rising fitness culture, organised sports participation, and corporate investment in performance apparel driving demand beyond traditional casual categories.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the price range segmentation, the Mass segment holds the dominant share of consumer spending, consistent with Vietnam's per capita income levels and the market's structure as a high-volume production and retail environment for affordable clothing. International fast-fashion brands operating in Vietnam price aggressively, offering discounts of up to 90%, keeping the Mass segment the undisputed volume leader. At the same time, the Premium and Luxury segment is expanding at the highest growth rate, with a projected CAGR of 14.4% through 2035. High-profile retail expansions by Hermes, Louis Vuitton, and Cartier in 2024 across Ho Chi Minh City and Hanoi reflect genuine commercial confidence in the segment's trajectory as Vietnam's high-income urban cohort grows.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the end-use segmentation, Women represent the leading consumer group for clothing in Vietnam, both by volume of purchases and by brand diversity. Vietnamese women demonstrate high engagement with fashion trends, driven by social media, influencer culture, and the growing availability of both international labels and local "made-in-Vietnam" brands. The Men's segment holds the second-largest share, with casual and professional clothing categories driving steady demand as Vietnam's white-collar workforce expands. Kids and Unisex segments are the fastest-growing end-use categories, fuelled by increasing parental spending on children's branded apparel and youth-driven demand for gender-neutral styling, particularly in urban areas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Southeast region, led by Ho Chi Minh City, is Vietnam's undisputed clothing market epicentre. Its concentration of garment manufacturing facilities, international brand partnerships, and retail infrastructure makes it the region with the largest market share and fastest commercial activity. Over 450 million garment items were exported from Vietnam in 2024, with the Southeast accounting for the bulk of this output. Key global brands, including Nike, Adidas, H&M, and Zara, source heavily from factories in Ho Chi Minh City, Binh Duong, and Dong Nai. The region's port connectivity and proximity to raw material suppliers further cement its position as the primary driver of Vietnam's clothing market revenues. The VIATT 2025 trade fair in Ho Chi Minh City drew nearly 13% more exhibitors than the prior year, reflecting continued investment interest in the region's clothing supply chain infrastructure.

The Red River Delta, anchored by Hanoi, represents the second-largest regional clothing market in Vietnam. The region combines a mature garment manufacturing base with a large, income-diversified urban consumer population. Hanoi's retail environment has seen significant expansion from international brands seeking to capture demand from Vietnam's northern economic corridor. Government-backed industrial zones in the Red River Delta provide favourable conditions for garment manufacturers, including tax incentives and streamlined export logistics. Consumer spending in this region reflects growing aspirations toward premium and branded clothing, particularly among Hanoi's expanding professional class. The region also benefits from Vietnam's broader textile and apparel export surge, with total sector export revenue reaching approximately USD 46 billion in 2025, positioning the Red River Delta as a critical contributor to this trajectory.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vietnam's clothing market features a competitive mix of globally recognised brands and emerging domestic labels, with international players commanding the premium and mid-market segments while local manufacturers capitalise on production cost advantages and cultural affinity. The market's competitive intensity has increased sharply as luxury houses deepen their retail footprints and fast-fashion giants scale their sourcing and logistics networks in the country. Companies compete on product innovation, supply chain efficiency, sustainability credentials, and digital marketing investment.

Leading competitors maintain competitive advantage through integrated manufacturing and retail strategies, trade agreement leverage, and growing ESG commitments to attract both local consumers and international brand partnerships. Smaller domestic brands such as Yody, An Phuoc, and Coolmate are carving out meaningful niches by combining local design sensibility with digital-first distribution and accessible pricing.

Founded in 1964 and headquartered in Beaverton, Oregon, Nike is one of the world's largest sports and casual clothing brands. In Vietnam, Nike maintains an extensive supplier network, with approximately 167 factories across the country producing footwear, apparel, and accessories as of 2025. Nike's Vietnam presence spans both production and retail, with flagship stores in Ho Chi Minh City and Hanoi. The brand's strength in performance and lifestyle apparel, combined with deep manufacturing integration, makes it a dominant force in Vietnam's sportswear and casual clothing segments.

Founded in 1854 and headquartered in Paris, France, Louis Vuitton is a flagship brand of the LVMH luxury conglomerate. In Vietnam, Louis Vuitton targets the premium urban consumer segment, with dedicated boutiques in Ho Chi Minh City and Hanoi's luxury retail districts. The brand's ready-to-wear collections, accessories, and leather goods are positioned at Vietnam's growing high-net-worth demographic, and its retail expansion in the country reflects confidence in the long-term trajectory of luxury clothing demand among Vietnamese consumers.

Founded in 1949 and headquartered in Herzogenaurach, Germany, Adidas operates one of the most extensive supplier networks in Vietnam, engaging around 167 factories across the country for footwear, apparel, and accessories production. Adidas's Vietnam operations form a core part of its global supply chain, with approximately 40% of its footwear historically produced in the country. Adidas competes in both performance and streetwear segments within Vietnam's domestic retail market, leveraging brand recognition, product innovation, and strong retail distribution across urban shopping centres.

Founded in 1837 and headquartered in Paris, France, Hermes is one of the world's most recognised luxury fashion houses. In Vietnam, Hermes caters to the ultra-premium segment, offering ready-to-wear clothing, leather accessories, and lifestyle products through select boutiques in Ho Chi Minh City. Hermes was among the luxury brands that expanded its Vietnam retail presence in 2024, reflecting the brand's strategic assessment of Vietnam as an emerging luxury market driven by growing high-income consumer density and rising aspirational spending among Vietnamese affluent consumers.

Other key players in the market are PUMA SE, H & M Hennes and Mauritz AB, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore in-depth insights into the Vietnam Clothing Market from 2026 with our comprehensive industry report. Access verified data on shifting consumer preferences, manufacturing investment trends, product innovation, and the regions driving the strongest growth. Whether you're an apparel brand planning market entry, a retailer refining your sourcing strategy, or an investor assessing opportunities in Vietnam's fashion sector, this report delivers the clarity you need. Download a free sample today and uncover the strategic opportunities shaping Vietnam's dynamic clothing industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 5.26 Billion.

The market is projected to grow at a CAGR of 12.80% between 2026 and 2035.

The key players in the market include Nike, Inc., Louis Vuitton Malletier SAS, Adidas Vietnam Company Limited, Hermes International S.A., PUMA SE, and H & M Hennes and Mauritz AB, among others.

Major strategies propelling the Vietnam clothing market are increasing manufacturing capacity, embracing sustainable practices, taking advantage of e-commerce, improving export competitiveness, investing in technology, and establishing global partnerships to address changing consumer and market needs.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 17.54 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Price Range |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.