Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

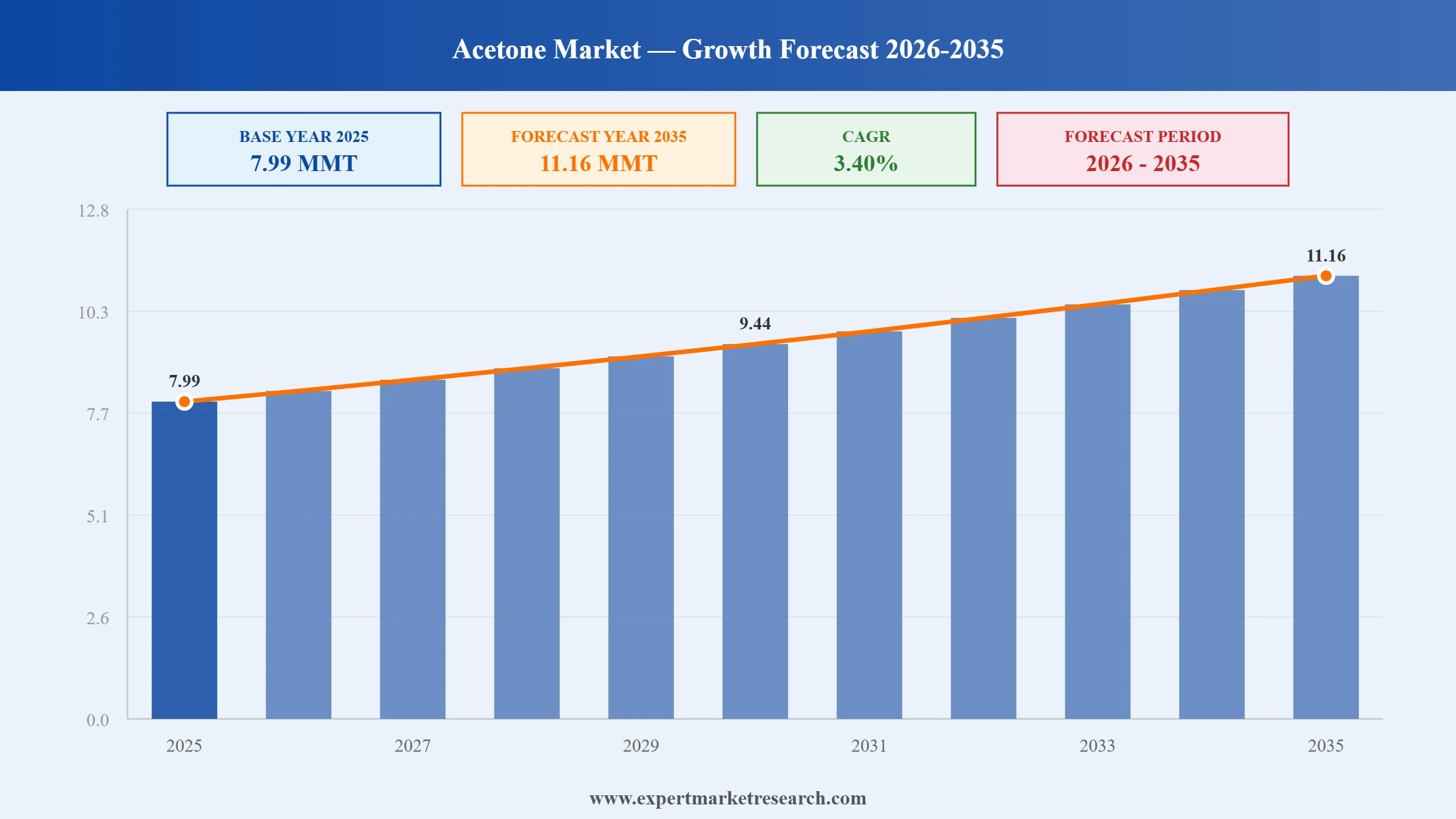

The Global Acetone Market reached a volume of 7.99 MMT at 2025 and is projected to expand at a CAGR of around 3.40% during the forecast period of 2026-2035. With sustained BPA and polycarbonate demand, accelerating MMA consumption from EV acrylic glazing, rising pharmaceutical and cosmetic solvent use, and large-scale phenol-acetone capacity additions in Asia, the market is expected to reach 11.16 MMT by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Acetone Market is being shaped by Chinese capacity expansions, EU regulatory tightening on BPA, accelerating MMA-led demand, and rising solvent volumes for pharmaceuticals and cosmetics.

Mitsui Chemicals Group decided to bring forward the shutdown of its phenol plant at Ichihara Works to October 2025, ahead of the originally planned schedule. The closure is part of a broader Japanese restructuring effort in response to over-supply from Chinese producers and weakening domestic phenol-acetone margins. The move follows the impairment-related transfer of Mitsui's equity interest in a Chinese phenol joint venture and reflects the structural shift of phenol-acetone production capacity toward Greater China.

Zhenhai Refining and Chemical, a Sinopec subsidiary, commissioned a large-scale phenol and acetone facility in China. The new unit adds significant volumes to an already long Chinese market and reinforces China's position as the world's leading phenol-acetone hub. The start-up follows Fuyu Petrochemical's 250,000 t/year phenol-ketone unit that began external sales in February 2025, underscoring an aggressive multi-year wave of Chinese capacity additions geared toward self-sufficiency in BPA, polycarbonate, and MMA chains.

Deepak Nitrite announced plans to invest approximately INR 3,500 crore (around USD 420 million) to add new petrochemical capacity in India, including 185 KTA of acetone, 300 KTA of phenol, and 100 KTA of isopropyl alcohol. The investment is aimed at consolidating India's import-substitution position in acetone and phenol and strengthening backward integration into BPA, polycarbonate, and specialty solvent applications. The project is among the largest single-site acetone capacity additions announced in South Asia and reflects rising domestic demand from automotive, construction, and pharmaceuticals.

Mitsui Chemicals Group and Mitsubishi Chemical Corporation jointly launched a study into stable supply of phenol-related products, covering phenol, acetone, alpha-methylstyrene, bisphenol A, and methyl isobutyl ketone. The collaboration explores joint operating practices during major turnarounds, optimisation of tank logistics, and reduction of GHG emissions. The alliance reflects rationalisation pressure across the Japanese phenol-acetone chain, where operators are managing oversupply from China and seeking cost and emissions efficiencies.

Cepsa Química, S.A. began construction of a new isopropyl alcohol plant at Palos de la Frontera, Huelva, with capacity of 80,000 tonnes per year and an investment of around €75 million. The plant, scheduled for completion at the end of 2025, will be supplied by acetone from Cepsa's adjacent chemical complex, increasing the value-add of its acetone output. The project supports rising European demand for isopropyl alcohol in pharmaceuticals, hand sanitiser, electronics, and cosmetics, and reinforces Cepsa's downstream integration strategy.

The European Union enforced broad bisphenol A restrictions for food-contact articles from January 2025, prompting polycarbonate and BPA producers to recalibrate volumes and re-route phenol-acetone outputs. The Global Acetone Market market growth in Europe is being tempered by reduced regional BPA demand, even as solvent and specialty applications continue to expand. Producers in the region are responding by deepening downstream integration into isopropyl alcohol, MIBK, and pharma-grade solvents, with Cepsa's new IPA plant at Palos de la Frontera as a marquee example.

China is in the middle of a multi-year phenol-acetone capacity build-out, with new units from Fuyu Petrochemical, Zhenhai Refining, and others adding hundreds of thousands of tonnes per year. The surge is targeting BPA, polycarbonate, and MMA self-sufficiency, but it is also pushing global acetone into structural oversupply and compressing margins for legacy producers in Japan, Korea, and Europe. In 2025, Mitsui Chemicals' early closure of its Ichihara plant illustrates the strategic re-allocation of capacity toward integrated, low-cost Chinese complexes.

Methyl methacrylate, derived from acetone via the ACH route, is emerging as the fastest-growing application, with industry forecasts pointing to roughly 7% CAGR. Demand is being lifted by acrylic glazing and PMMA replacing glass in EV battery covers, automotive lighting, and large-format displays, plus growing use in construction and signage. In 2025, multiple Asian producers committed fresh MMA capacity, including Mitsui Chemicals and Sumitomo, increasing acetone intake from the petrochemical chain and tightening regional demand.

Pharmaceutical and cosmetic uses of acetone are growing on the back of rising API manufacturing in India and China, expanded hand-sanitiser and personal-care production, and steady demand for nail-care formulations. High-purity acetone grades are commanding premium pricing, prompting producers such as Cepsa to invest downstream in IPA and pharma-aligned products. In 2025, capacity additions in Spain, China, and India explicitly highlighted pharma and personal-care end markets as growth anchors.

“Acetone Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

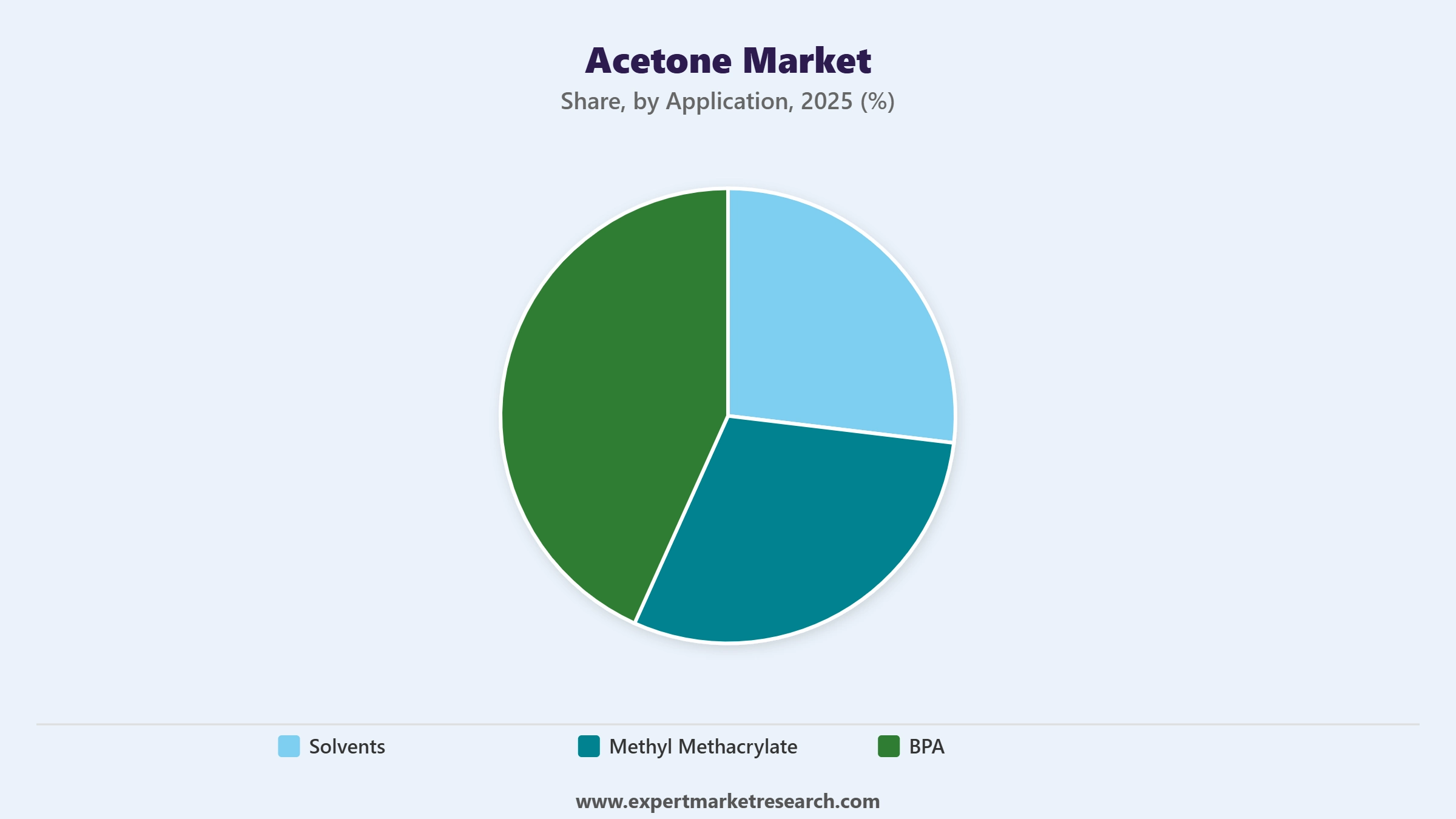

Market Breakup by Application

Key Insight: Solvents currently account for the largest application share of acetone, drawing on the molecule's strong solvency, low residue, and rapid evaporation rate. Demand spans pharmaceuticals, cosmetics, electronics cleaning, and surface coatings. BPA is the second-largest outlet via the phenol-acetone process route, although European demand has been tempered by the January 2025 EU food-contact restrictions. MMA is the fastest-growing application, projected at around 7% CAGR, lifted by EV-related acrylic glazing and large-format displays. Producers including Cepsa, INEOS, LG Chem, and Mitsui are recalibrating volumes across these end uses.

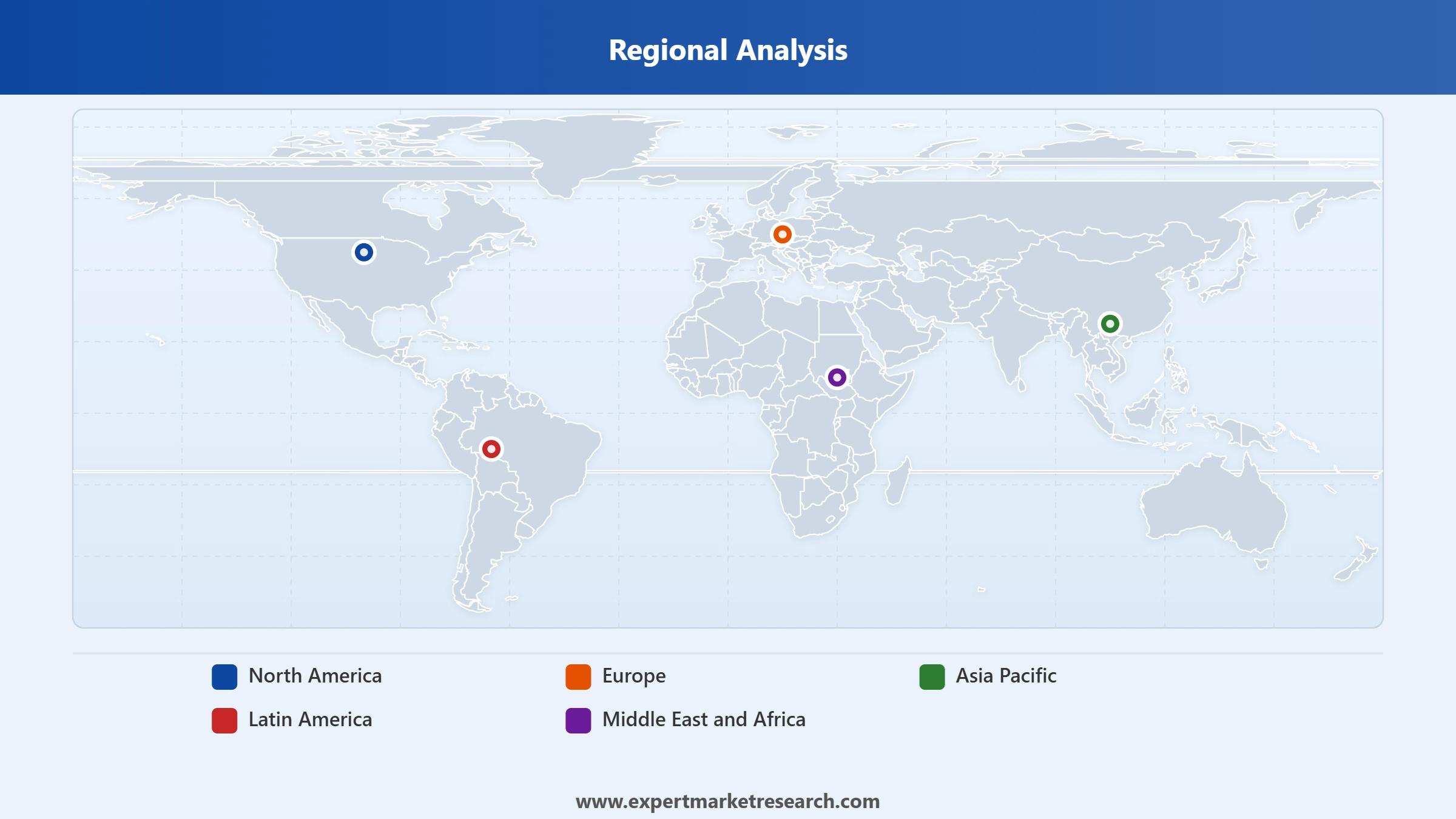

Market Breakup by Region

Key Insight: Asia Pacific dominates the global acetone market and is the fastest-growing region, anchored by China's vast phenol-acetone-BPA-polycarbonate value chain and India's downstream capacity additions led by Deepak Nitrite. Major commissioning's in 2025, including Fuyu Petrochemical and Zhenhai Refining, continue to lift regional supply. Europe is being reshaped by the EU's January 2025 BPA restrictions, with producers such as Cepsa pivoting into downstream IPA and pharma-grade solvents. North America remains a steady consumer with a focus on coatings, automotive, and specialty chemicals; Latin America and the Middle East and Africa serve as smaller but growing end markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Solvents lead the global acetone market, supported by broad use across pharmaceuticals, cosmetics, electronics, and industrial cleaning. High-purity grades are commanding premium pricing as pharma and personal-care customers tighten specifications, with capacity additions such as Cepsa's 80,000-tonne isopropyl alcohol plant directly tied to acetone feedstock. The segment benefits from steady, recurring demand and lower exposure to the BPA value-chain risks that dominate other outlets. Producers with downstream integration into IPA, MIBK, and pharma-aligned solvents are best positioned to capture margin in this category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

BPA, despite EU food-contact restrictions, continues to consume large volumes of acetone via the phenol-acetone route to feed polycarbonate and epoxy resin demand, with polycarbonate alone accounting for the majority of BPA end-use share. MMA is the fastest-growing application at around 7% CAGR as PMMA glazing displaces glass in EV battery covers, automotive lighting, and architectural panels. Asian producers continue to add MMA capacity in 2025, tightening regional acetone demand. Specialty applications and methyl isobutyl ketone (MIBK) round out the mix, with growing pharma- and agrochemical-linked offtake.

Asia Pacific dominates the global acetone market, with China at the centre of an aggressive phenol-acetone-BPA-polycarbonate-MMA build-out. Fuyu Petrochemical's 250,000 t/year phenol-ketone unit began external sales in early 2025, and Zhenhai Refining commissioned new phenol-acetone capacity in July 2025, lifting regional supply materially. India is also scaling rapidly, with Deepak Nitrite committing INR 3,500 crore to add 185 KTA of acetone, 300 KTA of phenol, and 100 KTA of isopropyl alcohol. Demand drivers span EV-linked MMA, polycarbonate for automotive and electronics, and pharma- and cosmetic-grade solvents. Regional players are increasingly integrating downstream to capture value as bulk acetone margins compress.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe's acetone market is being reshaped by the January 2025 EU BPA restrictions on food-contact articles, which have softened regional polycarbonate-linked demand. Producers including Cepsa Química and INEOS are re-routing volumes into downstream isopropyl alcohol, MIBK, and pharmaceutical-grade solvents. Cepsa's new 80,000-tonne IPA plant at Palos de la Frontera, scheduled for completion at the end of 2025, exemplifies this pivot. North America remains a steady but slower-growing market, focused on coatings, specialty chemicals, and pharmaceuticals, while Latin America and the Middle East and Africa serve as smaller, gradually expanding consumers led by industrial coatings, oilfield solvents, and personal-care formulations.

The Global Acetone Market is moderately consolidated, dominated by integrated phenol-acetone producers including Shell Chemicals, INEOS Group Holdings, Cepsa Química, LG Chem, Mitsui Chemicals, Honeywell, Versalis, and Formosa Chemicals, who control most of global cumene-route capacity. Regional specialists such as Hindustan Organic Chemicals, Altivia, and SI Group serve focused downstream and specialty markets.

Competitive priorities centre on backward integration into propylene and phenol, downstream extension into BPA, polycarbonate, MMA, IPA, and MIBK, and capacity rationalisation in response to Chinese oversupply. Leaders are investing in scale, energy efficiency, and pharma- and personal-care-grade specialty acetone to defend margins in a long market.

Founded in 1929 and headquartered in The Hague, Netherlands, Shell Chemicals is the petrochemicals arm of Shell plc and one of the world's largest phenol-acetone producers via the cumene process. Capabilities span phenol, acetone, alpha-methylstyrene, and downstream solvents. The company supplies acetone for BPA, MMA, and solvent applications across the Americas, Europe, and Asia, with notable strengths in integrated feedstock and global logistics.

Founded in 1998 and headquartered in London, UK, INEOS Group is one of the world's largest privately held chemical companies. INEOS Phenol is among the leading global producers of phenol and acetone, supplying BPA, MMA, and solvent customers across Europe, North America, and Asia. The company's strengths include large integrated cumene-phenol-acetone complexes, deep downstream integration, and a track record of selective acquisitions to expand capacity and geographies.

Founded in 1929 and headquartered in Madrid, Spain, Cepsa Química is the petrochemicals subsidiary of Moeve (formerly Cepsa). It is among the world's leading producers of LAB, phenol, and acetone, with a strong footprint in Europe and the Middle East. In 2025, Cepsa began construction of a new 80,000-tonne IPA plant in Spain that will use its own acetone as feedstock, deepening downstream integration into pharmaceutical and cosmetic-grade solvents.

Founded in 1947 and headquartered in Seoul, South Korea, LG Chem is one of Asia's largest chemical companies with a leading position in phenol, acetone, and bisphenol A. The company's acetone output supports its broader downstream portfolio in BPA, polycarbonate, and MMA, with strong demand from electronics, automotive, and packaging clients across Asia. LG Chem invests in process upgrades and energy efficiency to defend margins amid Chinese oversupply.

Other key players in the market are Honeywell International Inc., Versalis S.p.A., Mitsui Chemicals Group, Formosa Chemicals and Fibre Corporation, Altivia, Hindustan Organic Chemicals Limited, and SI Group, Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Acetone Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on phenol-acetone capacity additions, BPA and MMA demand shifts, regulatory impacts, and top growth regions. Whether you are launching a new specialty solvent or expanding your petrochemicals portfolio, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Acetone.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate volume of nearly 7.99 MMT.

The market is estimated to grow at a CAGR of 3.40% between 2026 and 2035.

The major drivers of the industry, such as the rising disposable incomes, increasing hygiene awareness, rapidly growing cosmetic market, and the growing end-use industries, are expected to aid the market growth.

The key trends aiding the market include the growing applications of acetone in the pharmaceutical sector, the growth of the personal care and cosmetic sectors, advancements in the acetone production process, and regulations guiding the use of acetone.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific, with the Asia Pacific accounting for the largest share in the market.

Solvents, methyl methacrylate (MMA), and BPA, among others are the leading applications of acetone in the industry.

The major players in the market are Shell Chemicals, INEOS Group Holdings S.A., Cepsa Química, S.A., LG Chem, Honeywell International Inc., Versalis S.p.A., Mitsui Chemicals Group, Formosa Chemicals and Fibre Corporation, Altivia, Hindustan Organic Chemicals Limited, and SI Group, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.