Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global application delivery controller market attained a value of USD 3.34 Billion in 2025 and is projected to expand at a CAGR of 10.90% through 2035. The market is further expected to achieve USD 9.40 Billion by 2035. The growing use of API-based solutions and real-time digital services by businesses is fueling the need for ADCs that can route traffic intelligently, provide automatic failover, and improve application-level security in their distributed deployments.

The adoption of edge computing is shaping up to be a critical factor driving growth in the market, as companies look to process information locally to minimize delays and boost application performance. Moreover, requirements for data security compliance are compelling businesses to install ADCs equipped with encryption and traffic monitoring features, especially in industries dealing with personal information, boosting the application delivery controller market value.

In November 2025, F5 introduced ADC 3.0, integrating security and delivery into a unified platform, which includes integration of AI-based traffic intelligence in its BIG-IP solution to enable dynamic tuning of applications in hybrid infrastructures. The introduction of this feature correlates with growing corporate demand for workloads requiring minimal latency since more than 65% of businesses have implemented hybrid cloud architecture for their mission-critical applications, as per the application delivery controller market analysis. The market is posed to experience rapid growth with increasing preference for secure and low-latency application delivery as companies continue to adopt more distributed infrastructures.

Enterprise IT infrastructure is undergoing significant structural transformation, driving corresponding shifts in demand within the application delivery controller market. The emergence of microservices and containers calls for advanced ADCs that can easily integrate into Kubernetes and other multi-cloudarchitectures. Key vendors are developing software-based and lightweight ADCs that can integrate into DevOps pipeline to ensure easy deployment. For example, in March 2024, NVIDIA launched generative AI microservices enabling healthcare firms to accelerate drug discovery, medtech innovation, and digital health using cloud-native AI tools. Additionally, there is a growing trend among vendors to develop ADCs with WAF and Zero Trust capabilities, particularly for the BFSI and healthcare segments.

Compound Annual Growth Rate

10.9%

Value in USD Billion

2026-2035

Mercury Security initiated the open controller application platform, offering third-party integration, customizability, and scalable security infrastructure setup. The market therefore presents more possibilities for ADC vendors to implement open and interoperable platforms that encourage innovation within an ecosystem of applications.

Rockwell Automation released ControlLogix 5590 controller, aimed at enhancing processing speed and scalability of real-time industrial automation systems. This development shows how providers in the application delivery controller market can improve their capability in implementing high performance computing and traffic handling solutions.

Omron announced the launch of highly sophisticated automation controllers that emphasize accuracy, energy savings, and interoperability within manufacturing systems. These technological developments open opportunities for ADC providers to offer smart and energy-efficient traffic management products that can be deployed in industrial and Internet-of-Things ecosystems.

F5 launched a unified application delivery and security platform capable of supporting AI-powered, multi-cloud, and hybrid environments. This indicates potential for vendors in the application delivery controller market to develop security and delivery capabilities that can help build AI-friendly architectures and application performance management systems.

ADC suppliers are now incorporating AI and machine learning algorithms into their offerings to optimize traffic routing and improve application performance. They leverage user behavior, traffic surges, and application statuses to predictively balance loads and resolve problems proactively. In line with this trend, in June 2025, A10 Networks launched AI-based analytics in its Thunder ADC line, designed for telecommunications companies handling traffic loads related to 5G services. The United States government's efforts in supporting the deployment of 5G networks through projects from the Federal Communications Commission indirectly boost demand in the application delivery controller market.

The emerging application delivery controller market trend towards containerization compels providers to revamp their products to meet the needs of Kubernetes-native infrastructures. Enterprises adopting microservices architectures need ADCs that are capable of scaling along with containerized applications. Government-led digital transformation strategies in the public sector, such as India's Digital Public Infrastructure strategy, promote container-based applications, thus generating ADC requirements. For example, in March 2026, Venn launched OpenClaw integration, enabling secure deployment of AI agents with permission-based controls, improved data access governance, and streamlined enterprise workflow integration.

The trend towards integration is expected to continue as ADC suppliers build their solutions based on Zero Trust principles, reshaping the entire application delivery controller market dynamics. Zero Trust security solutions provide ongoing authentication of user identities and application access, lowering risks from a security standpoint. In March 2025, Fortinet launched the latest version of its FortiADC with built-in support for Zero Trust Network Access (ZTNA) features designed primarily for businesses with remote workers. The implementation of GDPR by European Union regulators and other data privacy regulations around the world also requires ADC solutions for both performance improvement and strong security enforcement.

With the advent of multi-cloud environments, ADCs are expected to become centralized traffic management platforms. Suppliers are developing technologies that allow enterprises to distribute workloads between cloud service providers and optimize costs and performance levels. For example, AWS is upgrading its Elastic Load Balancer (ELB) solution with enhanced traffic management options. Government-led initiatives towards cloud computing use, such as national cloud policies in the Asia-Pacific region, encourage many companies deploy multi-cloud infrastructures, accelerating the application delivery controller market growth. In February 2026, Lumen launched Multi-Cloud Gateway and expanded metro connectivity, enabling high-speed, secure data movement across distributed AI environments while reducing network complexity.

Subscription- and software-as-a-service (SaaS)-based ADC services delivery reshape the revenue models of vendors and customers' preferences, boosting the overall application delivery controller market penetration. Enterprises prefer to opt for OPEX-based implementations rather than CAPEX-focused hardware-based solutions. For example, in March 2026, Radware introduced Alteon Protect, combining cloud-based threat detection with on-device enforcement to deliver scalable, low-latency security across hybrid applications and APIs. This trend is further bolstered by government schemes focused on digital transformation of SMEs in emerging markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global Application Delivery Controller Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

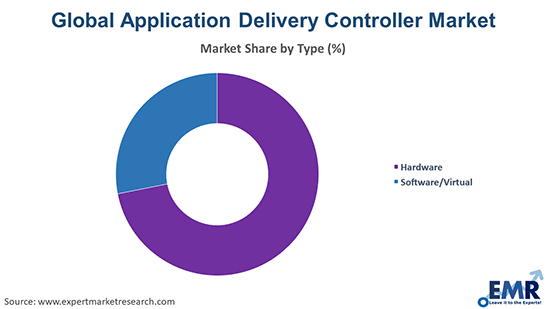

Market Breakup by Type

Key Insight: The application delivery controller market based on its type is witnessing a shift from high-performance hardware ADCs to agile software ADCs. The hardware segment holds dominance wherever there is a requirement for deterministic bandwidth, enforcement of security policies, and management of the IT infrastructure, especially in compliance-sensitive industries. The software ADC segment is growing at an accelerated rate owing to its applications across enterprise clouds, containerized computing, and programmable network traffic. Leading vendors are offering a balanced approach in terms of dual offerings.

Market Breakup by Enterprise

Key Insight: Enterprise segmentation as considered in the application delivery controller market report is characterized by the presence of a clear differentiation among companies with respect to the type of adoption. Large enterprises tend to be dominant because of their preference for application delivery frameworks that are reliable, fast, and secured, whereas small businesses are adopting the ADC technology via cloud computing owing to its reduced complexity and costs involved in the process. Vendors are offering feature-packed software for large enterprises and simpler solutions for SMEs. For example, in June 2024, ABB introduced OmniCore platform integrating AI, cloud, and edge computing, enabling faster, precise, and energy-efficient robotic automation across scalable industrial applications.

Market Breakup by Service

Key Insight: The issue of service segmentation highlights the relevance of both deployment skills and continuous support within the application delivery controller market. The provision of integration and implementation services is prevalent as it is challenging to deploy an ADC into hybrid and multivendor cloud infrastructures; therefore, technical skills are becoming vital. On the other hand, training, support, and maintenance services are becoming increasingly prominent, especially when organizations seek to improve ADCs' performance. In February 2023, Yokogawa introduced reinforcement learning-based autonomous control AI for edge controllers, improving productivity, optimizing operations, and enabling energy-efficient, self-learning industrial control systems.

Market Breakup by Application

Key Insight: Segmentation of applications shows different factors driving adoption in various sectors. The BFSI sector is positioned at the forefront of the application delivery controller market because of its requirements for transaction-processing infrastructure that is secure, compliant, and fast. On the other hand, the sector of IT and telecom is experiencing rapid growth as a result of modernizing their networks and increased data flows. Aligning with this trend, in April 2026, Appdome introduced identity-first mobile API protection, enabling verified app, device, and session authentication with real-time risk signals to prevent API abuse. Other sectors using ADCs include retail, health care, energy, and media, each with unique challenges.

Market Breakup by Region

Key Insight: Regional dynamics in the application delivery controller market mirror different levels of maturity and growth potential. North America leads in this regard because of its highly developed IT infrastructure and vendor base, along with early adoption of cloud technologies. Europe takes the second spot owing to consistent demand based on regulatory requirements and enterprise transformation initiatives. The fastest growth is observed in Asia-Pacific because of ongoing initiatives and expansion in telecom infrastructure. Latin America and the Middle East and Africa regions are slowly implementing ADCs with IT modernization in enterprises.

Hardware-based ADCs dominate the market the market due to high-performance processing and security control needs

Application delivery controller solutions based on hardware appliances retain their significance for large-scale implementations, especially for businesses dealing with delay-intolerant applications or services subjected to government compliance regulations. Companies in the application delivery controller market are improving hardware solutions with the use of ASIC chips to provide higher speeds and reliable performance, which is essential for financial trading systems or core telecom networks. ADC appliances are being used as combined security devices that include SSL offload, deep-packet inspection, and DDoS protection capabilities. For companies running their own data centers, hardware ADCs remain the preferred choice due to consistent performance and fine-tuned traffic management capabilities. For example, in April 2026, Microchip introduced new dsPIC33A digital signal controllers featuring real-time control, integrated analog capabilities, and post-quantum security.

Software and virtual application delivery controllers gain increasing popularity within the application delivery controller market scope, along with the growing trend to develop applications natively for the cloud environment. Businesses are turning to vendors such as NGINX Inc. providing software solutions focused on light-weight, API-driven ADCs. This approach offers flexible and seamless implementation into CI/CD processes and integration with Kubernetes clusters. Subscription-based pricing model is also being introduced to support broader adoption of virtual ADCs in mid-sized companies.

Large enterprises account for the dominant share of the market due to complex multi-cloud infrastructure and high traffic volumes

The large enterprises are considered as the leading adopter group owing to the need for traffic orchestration and robust application ecosystem. The companies operating in BFSI, telecommunications, and healthcare industries are implementing ADC platforms to handle higher volume traffic while ensuring application reliability, boosting the overall application delivery controller market development. ADC solution providers like Citrix are building enterprise-class solutions with inbuilt analytics and zero-trust capability. The multi-cloud strategy adopted by prominent companies mandates centralized traffic control. Furthermore, lengthy purchase cycle and collaboration among vendors are other factors that add to the prominence of this category. In July 2025, Advantech introduced the AMAX platform integrating PLC, HMI, and IoT into unified architecture, enabling deterministic real-time control and simplified automation system integration.

In contrast, small and medium-sized enterprises are anticipated to exhibit the highest adoption rate for ADC solutions owing to the availability of cloud-based services and subscription-based offerings. Enterprises like Radware are offering ADC solutions with ease of deployment along with security features to the SME sector. The increased adoption of digitization by SMEs necessitates efficient traffic management without any huge investment. The software-as-a-service (SaaS)-based ADCs enable SMEs to adapt to changing business dynamics. Moreover, digitalization programs for SMEs undertaken by governments are driving ADC implementation.

Integration services continue to capture a sizeable market share due to complex deployment across hybrid and multi-cloud environments

Integration and implementation services occupy the largest application delivery controller market share as enterprises need the custom implementation of ADC solutions. Companies like A10 Networks provide custom integration services in order to integrate ADC capabilities with enterprise’s infrastructure and security measures, and with cloud platforms. This is becoming necessary due to the high complexity of deployment processes of ADCs in complex infrastructures that involve both legacy and cloud technologies. For instance, in April 2026, Tieto Caretech, x-tention, and Better partnered to launch open, modular clinical data platforms, enabling interoperable, patient-centric healthcare systems across the DACH region.

The training, support, and maintenance services segment observes significant growth in the application delivery controller market since enterprises aim at optimizing their utilization of ADCs and benefitting from the investment. Ongoing support is required due to frequent product updates, constant emergence of cyber threats, as well as AI-based innovations. The support service offerings of vendors like Fortinet are expected to grow popular as they add automation to the process and expand the scope of customer support services.

By application, the BFSI sector dominates the market due to stringent security compliance and high transaction processing needs

The BFSI segment continues to be the leading user of ADC technology owing to its reliance on secure and high-end application delivery needs. Financial institutions are utilizing ADC technology to handle encryption in their transactions and protect themselves from cyber fraud while guaranteeing uninterrupted online banking applications. Some of the vendors that offer ADC technologies include F5 Inc. which provides an integrated solution that includes the Web Application Firewall (WAF), traffic analysis, and other capabilities that can handle all financial environment needs. In April 2026, CARD91 introduced VerifyIQ, an AI-powered platform integrating verification, fraud detection, and real-time confidence scoring to streamline faster, policy-aligned onboarding decisions.

The fastest growth in the application delivery controller market is witnessed in the IT and telecommunication sector owing to the development of 5G and cloud services. Telecommunications firms need to provide ADC solutions to handle vast amounts of data traffic while guaranteeing smooth and uninterrupted delivery of services. Some of the vendors providing ADC solutions include A10 Networks, which is focused on developing high-end ADC products that can handle telecom-grade data traffic.

North America registers the leading market share due to early cloud adoption and strong vendor presence

North America is at the forefront of the application delivery controller market owing to early adoption of cloud computing services and an active presence of prominent vendors in the region. Citrix Systems Inc., F5 Inc., and other firms that are based in North America have been instrumental in the development of ADCs and their adoption in organizations. In this region, organizations are making heavy investments in a multi-cloud strategy, which requires efficient traffic management systems. Regulatory measures concerning data protection are also prompting companies to implement better ADCs. In January 2026, Emerson introduced DeltaV v16 LTS, enabling software-defined control, improved data visibility, enhanced cybersecurity, and scalable automation for enterprise-wide industrial operations.

On the other hand, Asia Pacific is expected to be the fastest growing regional application delivery controller market over the forecast period, due to the ongoing transformation to a digital economy coupled with telecom infrastructure development. The region is witnessing an increased adoption of cloud computing technology as well as growth in mobile application usage. The regional presence of Amazon Web Services and initiatives to build a digital economy are contributing to growth in this market.

There has been heightened competition in the market as vendors increasingly focus on incorporating AI-driven automation, API protection and security, and multi-cloud orchestration features into their product lines. Platform consolidation has become common as application delivery controller market players offer consolidated ADC, WAF, and Zero Trust platforms to simplify operations for the enterprise customer base. The growing adoption of a subscription or SaaS model by vendors in the market offers recurring revenues and also helps companies to tap mid-market customers.

Partnering with hyperscalers and telecom companies is creating lucrative revenue opportunities as they leverage 5G and edge computing platforms. The trend of development of lightweight, Kubernetes-native ADCs is expected to see increased traction owing to the rising demand for such solutions from microservice environments. Analytics is another area in which application delivery controller companies are focusing, offering advanced predictive analytics to optimize traffic.

Founded in 1996 and operating from Seattle, United States, F5 Inc. specializes in implementing the use of AI-enabled traffic intelligence and security within its BIG-IP and NGINX solutions. It aims to further develop distributed cloud services allowing companies to effectively control their apps within hybrid and multi-cloud architectures through increased visibility, automation, and security.

Founded in 1997 and based in the United States of America, Radware Ltd. is expanding its ADC-as-a-Service suite by adding bot and API security. It caters to enterprises looking for cloud-native subscription-based solutions.

Citrix Systems Inc. was founded in 1989 and operates from its headquarters in Fort Lauderdale, United States. Citrix Systems Inc. provides NetScaler ADC products that include Zero Trust security and adaptive authentication capabilities. Citrix Systems Inc. has identified secure application delivery in hybrid work models as its key focus area in which it aims to support businesses by providing them secure application delivery in distributed end-user access environments.

A10 Networks Inc. was established in 2004 and operates from its headquarters in San Jose, United States. A10 Networks Inc. specializes in offering high-end ADC products with high traffic load management capabilities for telecom companies and 5G applications.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Barracuda Networks, Inc., and Array Networks, Inc., among others.

Unlock the latest insights with our application delivery controller market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 3.34 Billion.

The market is projected to grow at a CAGR of 10.90% between 2026 and 2035.

The market is estimated to grow in the forecast period of 2026-2035 to reach about USD 9.40 Billion by 2035.

Focusing on expanding SaaS-based offerings, strengthening AI-driven analytics, targeting regulated industries, forming hyperscaler partnerships, and enhancing managed services portfolios while optimizing pricing models to attract mid-sized enterprises globally.

The growing technological advancements and increasing virtualisation and internet penetration, are the key trends guiding the growth of the application delivery controller market.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Hardware and software/virtual are the leading application delivery controller types in the market.

By enterprise, the market for application delivery controllers is segmented into small and medium enterprise and large enterprise.

Integration and implementation, and training, support, and maintenance are the significant services of the product in the market.

The major applications of the product include banking finance service, and insurance, retail, IT and telecom, health and life science, energy and utilities, and media and entertainment, among others.

The key players in the market include F5, Inc., Radware Ltd., Citrix Systems, Inc., A10 Networks, Inc., Barracuda Networks, Inc., and Array Networks, Inc., among others.

Rising complexity of multi-cloud environments, integration with legacy systems, increasing cybersecurity threats, high deployment costs, and shortage of skilled professionals are limiting seamless ADC implementation across enterprises globally.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Enterprise |

|

| Breakup by Service |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.