Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

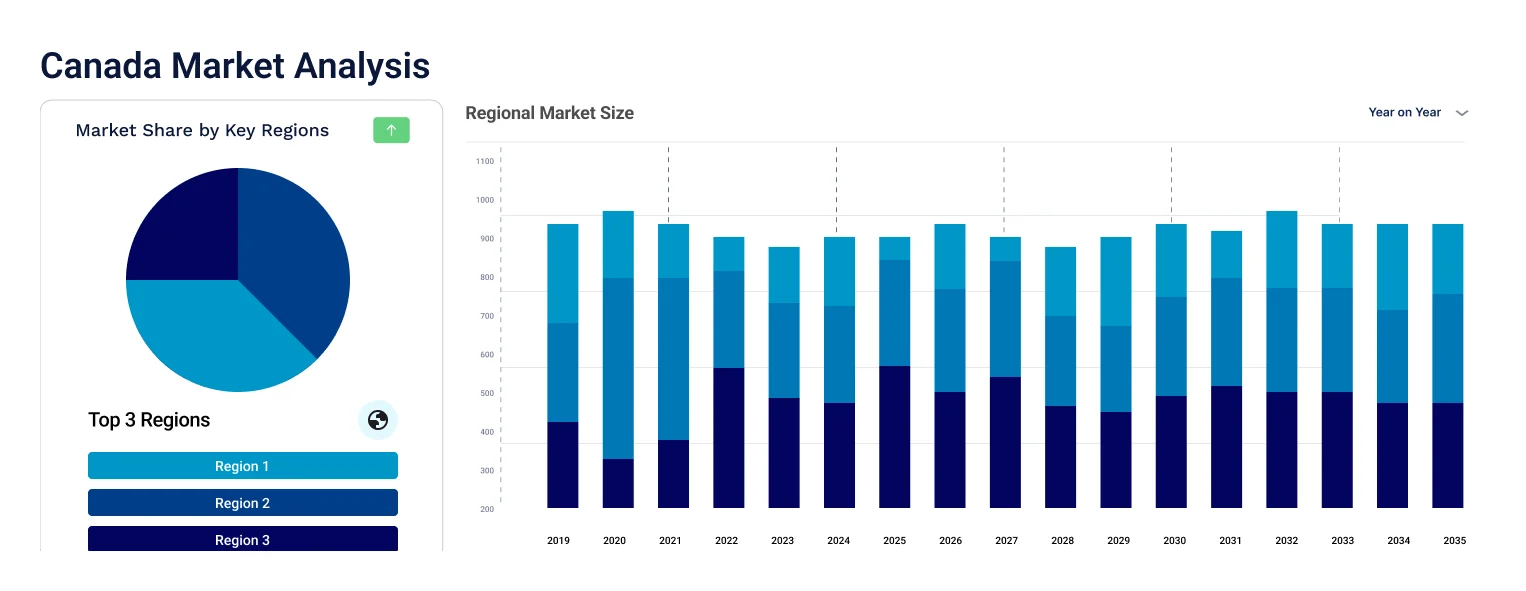

The Canada pet food market size was valued at USD 5.96 Billion in 2025. The market is further projected to grow at a CAGR of 4.40% between 2026 and 2035, reaching a value of USD 9.17 Billion by 2035.

Compound Annual Growth Rate

4.4%

Value in USD Billion

2026-2035

Read more about this report - Request a Free Sample

Pet food is a type of food specifically formulated and intended for consumption by pets. It is available in various forms such as dry kibble, wet food, and treats. Some brands in Canada pet food market offer organic, wild-caught, and GMO-free options for different consumer preference. The manufacture and distribution of pet food is regulated by federal guidelines and state laws, including nutritional requirements for food sold as a "complete and balanced meal".

In Canada, almost four out of every five households own a pet, where cats are the most popular, followed by dogs, fish, birds, and exotic animals. In 2020, there were about 27.93 million pets in Canada and by 2025, this number is predicted to rise to slightly over 28.5 million. Meanwhile, in 2022, there were 8.5 million pet cats and 2.51 million pet birds in the nation. Less than 1 percent of homes had any other kind of pet. Canada has a sizable pet industry due to the country's high pet ownership rate, which is leading to Canada pet food market growth.

Increase in pet humanisation, easy availability of pet food via online store, and rising adoption of dogs are boosting the market demand

Hill's Pet Nutrition unveiled its new line of MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. These products are rich in antioxidants, omega-3 fatty acids, and vitamins.

Mars Incorporated introduced its high-end cat brand SHEBA to the Canadian market, providing cat parents with wet food formulas.

Nestle Purina introduced a new line of cat treats called "Friskies Playfuls". These round treats come in flavours like chicken and liver as well as salmon and shrimp are specifically made for adult cats.

Simmons Pet Food invested USD 100 million for canned pet food operation in Dubuque. This investment is aimed at meeting the strong demand for high-quality nutrition and pet parent preferences.

General Mills acquired Tyson Foods' pet treats business for USD 1.2 billion, which includes the Nudges, Top Chews, and True Chews brands. The acquisition strengthened General Mills' position in the fast-growing North American pet food market.

The increase in pet humanisation is one of the key Canada pet food market trends. The high demand for companionship has led to an increase in adoption of pets.

The nation's millennial population is increasingly adopting pets, especially dogs. 58.0% of Canadians owned a dog as of 2020 and saw them as essential members of their families, which is contributing to Canada pet food market demand.

The demand for wet and dry pet food products has increased due to their easy availability via online stores. In 2020, Amazon’s pet food sales reached USD 9 billion, and the number is expected to grow, which will likely increase the Canada pet food market size in future.

The demand for organic pet food is experiencing growth as it offers better digestion, promote energy levels, and has higher levels of nutrients. Due to increased pet adoption and greater awareness of health issues via campaigns, this Canada pet food market trend is expected to continue in the forecast period.

The Canada pet food market share have grown as nearly three million people adopted pets, particularly dogs and cats in 2023, which has thereby increased the sales of pet food. There are more than 2,000 pet stores in Canada and in 2023, sales from pet stores alone were expected to surpass USD 7 billion.

Some popular pet stores in Canada that sell pet food include PetSmart, PetValu, Mondou, and Petland Canada. These well-known chains offer a variety of pet food options, including both wet and dry food, as well as treats and other pet supplies. In addition to physical stores, online retailers such as Chewy, Rover, Homes Alive Pets, and Critters Pet Health Store also deliver pet food and supplies to Canada. Whether shopping in-store or online, Canadian pet owners have a range of options for purchasing quality pet food for their furry friends, which thereby promotes Canada pet food market development.

Canada Pet Food Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Pet Type

Market Breakup by Form

Market Breakup by Ingredient Type

Market Breakup by Pricing Type

Market Breakup by Distribution Channel

Market Breakup by Region

Read more about this report - Request a Free Sample

Dogs lead the pet food market due to their high food consumption levels

According to Canada pet food market analysis, dogs are expected to account for a significant portion of the market. Even though there are fewer dogs than cats in Canada, dogs still lead the pet food industry, which was valued worth USD 1.67 billion in 2022. This is because they eat more commercial food than cats do. The pet food market for dogs is expected to grow at the fastest rate during the forecast period due to pet owners' growing interest in high-end products like vegan and grain-free dog food.

Meanwhile, there has been a rising adoption of cats as pets in Canada, which can lead to increased market share of cats in Canada pet food market segmentation. As of 2022, the Canadian cities with the highest adoption rates for cats were Toronto, Calgary, and Quebec, with Toronto contributing 5% of all adoptions nationwide, while the other two states accounted for 4% and 1%, respectively.

Premium pet food holds a significant market share because of its higher protein content and nutritional values

According to the Canada pet food market report, the premium price segment is expected to dominate, since pet owners' top priorities are providing their animals with proper healthcare and nutrition. They frequently look for premium dry foods from pet food brands that provides specialised nutrition for managing pet weight and skin. This rising demand from pet owners for premium dry pet foods to support the health of their animals is anticipated to further boost the pet food market growth.

However, the mass-priced pet food segment in Canada is also experiencing growth due to an increase in e-commerce sales for pet food. Online channels allow consumers to purchase pet food products on discounts, offering convenience and accessibility. In addition, supermarkets and hypermarkets also offer consumers an abundance of choices in terms of brands and prices, which has contributed to increasing share of mass-priced pet food segment, thus impacting the pet food market in Canada.

The competitive landscape of the market is characterised by market players expanding their product portfolio to cater to the growing demand for pet care products and services.

Mars Inc. was founded in 1911 and is based in United States. It is an international conglomerate that owns ‘PEDIGREE’ among other pet care brands. With its 100,000 veterinary care professionals, Mars Inc. focuses on offering complete veterinary care, nutrition, and pet welfare services.

Nestlé S.A. also known as Purina was founded in 1866 and is based in Switzerland. It is a significant participant in the pet food market and provides a selection of goods for dogs, cats, and other household animals. The business is renowned for both its dedication to animal welfare and its premium ingredients.

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.) was founded in 1948 and is headquartered in United States. The company specialises in creating premium pet food products, such as prescription diets for animals with medical requirements. Simmons Foods, Inc. is a leading supplier of meat products, including poultry, pet, and ingredient products, and serves customers in North America. The company was founded in 1949 and is based in Arkansas, United States. Simmons Foods works with farmers, communities, and employees to provide quality food products and services.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players included in the Canada pet food market analysis are Archer-Daniels-Midland Co., General Mills Inc., The J.M. Smucker Company, FirstMate Pet Foods, PLB International (1st Choice Nutrition), and Rolf C. Hagen Inc. (Nutrience), among others.

Central Canada is one of the prominent regions in Canada due to its high pet adoption levels

The pet food market in Central Canada is a booming industry, with the country being home to hundreds of pet stores across the nation.

As of December 2022, Ontario was home to most number of pets and pet supplies stores across the country, with 845 such stores in the province. This can increase the Canadian pet food market share in the future. Meanwhile, Quebec had 544 pet stores, followed by British Columbia with 375 pet stores. These pet stores facilitate a wide availability of pet food varieties, including wet and dry treats, biscuits, cereals, organic, and non-GMO items.

In addition, Canadian pet food manufacturers have been developing high-quality, human-grade, and innovative pet foods to supply in all Canadian regions through store-based retail channels, e-commerce sector, and veterinary clinics. The availability of a wide range of pet food options reflects the growing demand for pet food products in the Canadian market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Canada pet food market reached an approximate value of USD 5.96 Billion.

The market is expected to grow at a CAGR of 4.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 9.17 Billion by 2035.

Canada pet food market is experiencing significant growth, driven by factors such as pet humanisation, premiumisation of pet food, and the increasing demand for high-quality pet foods.

The key trends aiding the market expansion include the launch of different type of pet foods, high sales of nutraceuticals for animals, and increasing adoption rate among millennials.

Major regions in the market are Northern Canada, British Columbia, Alberta, The Prairies, Central Canada, and Atlantic Canada.

Dogs, cats, and birds are studied in the market report.

Dry pet food is a type of pet food that is made up of dry, hard kibble or pellets. It is a popular choice among pet owners due to its long shelf-life, convenience, and variety of flavours and textures.

Pet snacks are treats or small portions of food that are given to pets, such as dogs and cats, as a supplement to their regular diet. They are designed to provide additional nutrition, flavour, and enjoyment for pets.

Pet snacks can be made from a variety of ingredients, including real meat, seafood, grains, vegetables, and fruits.

The key players in the market are Mars Inc., Nestlé S.A., Archer-Daniels-Midland Co., General Mills Inc., Colgate - Palmolive Company (Hill's Pet Nutrition, Inc.), The J.M. Smucker Company, FirstMate Pet Foods, PLB International (1st Choice Nutrition), Rolf C. Hagen Inc. (Nutrience), and Simmons Foods, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Pet Type |

|

| Breakup by Form |

|

| Breakup by Ingredient Type |

|

| Breakup by Pricing Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.