Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

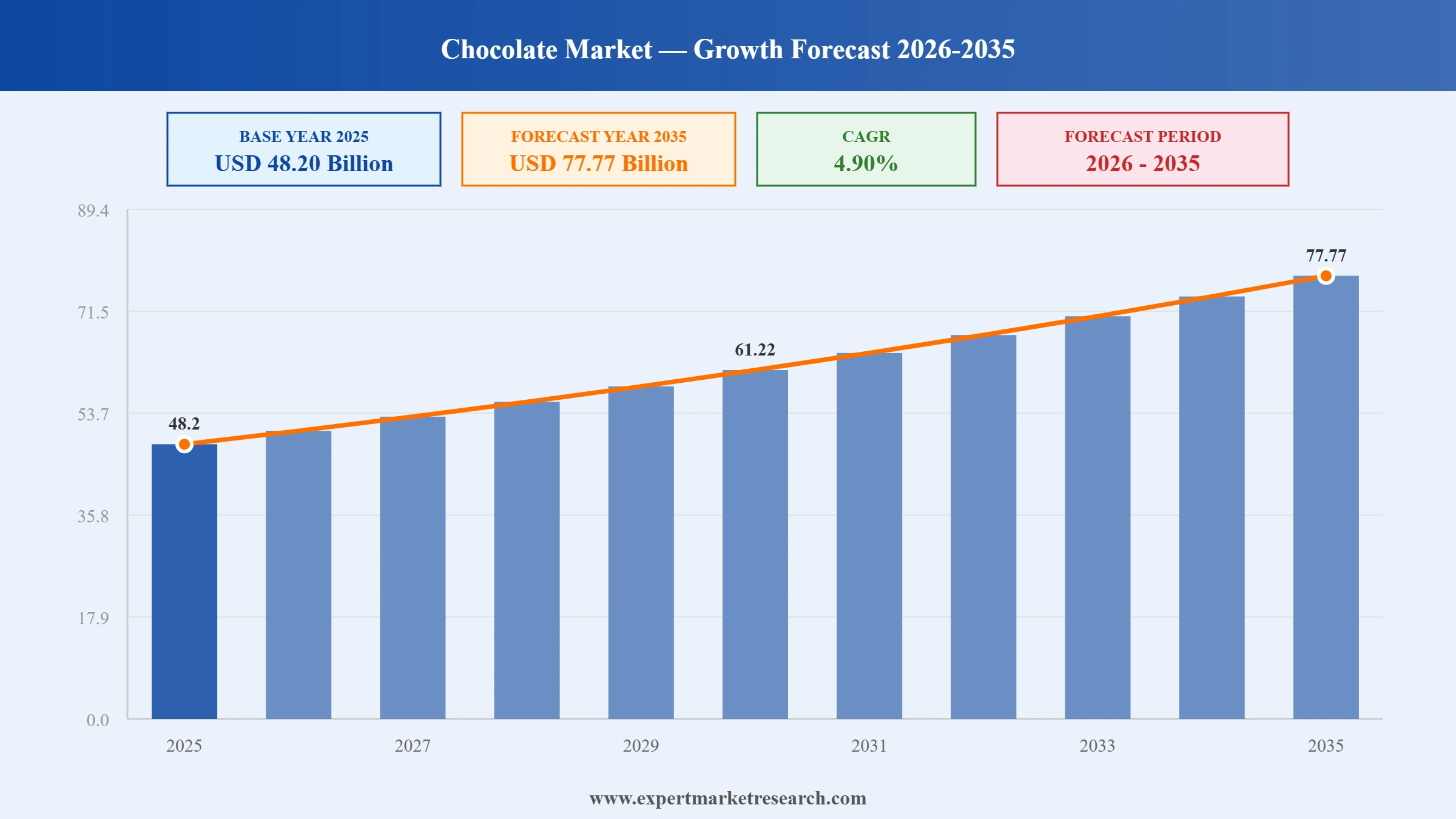

The global chocolate market attained a value of USD 48.20 Billion in 2025 and is projected to expand at a CAGR of 4.90% through 2035. The market is further expected to achieve USD 77.77 Billion by 2035. The rising interest in functional chocolates that contain botanicals, probiotics, and high cocoa content is motivating the producers to develop diversified premium lines of products and differentiate themselves at the retail level, enhancing consumer engagement across the globe.

An increase in premium gift-giving trends and demand for ethical chocolate is motivating product development among various manufacturers. In addition, technology investment in recycling solutions and advanced artificial intelligence manufacturing systems is improving production efficiency and compliance with changing sustainable regulations. Simultaneously, the growth of the direct-to-consumer sales channel and seasonal launches of products is assisting chocolate market players to increase sales and loyalty among customers.

In April 2026, Mars and ofi partnered to advance regenerative cocoa farming, reducing emissions while improving farmer resilience and productivity. It is yet another example of how leading manufacturers integrate innovative products and their sustainable impact into their premiumization strategy. According to the chocolate market analysis, global grindings of cocoa have gone beyond 4.50 million tonnes during the 2024-2025 season, which shows that despite high cocoa prices and interruptions in supply chains, the industrial demand remains strong. This drives manufacturers to reconsider their sourcing practices, launch new climate-friendly products, and ensure supply chain resilience while providing high-quality products to their customers.

The chocolate market is further undergoing changes as manufacturers focus on premiumization, functional ingredients, clean label formulations, and responsible cocoa sourcing. Growing investments in single-origin chocolate, sugar-reduced formulae, and cocoa substitutes allow manufacturers to respond to consumer demand and shield themselves from volatile prices of raw materials. In February 2026, Puratos partnered with California Cultured to launch the first professional cultured cocoa chocolate, advancing sustainable chocolate innovation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Chocolate Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 48.20 |

| Market Size 2035 | USD Billion | 77.77 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.90% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.52% |

| CAGR 2026-2035 - Market by Country | India | 7.77% |

| CAGR 2026-2035 - Market by Country | Brazil | 5.35% |

| CAGR 2026-2035 - Market by Sales Channel | B2C | 5.54% |

| CAGR 2026-2035 - Market by Category | Compound Chocolate | 5.58% |

| Market Share by Country 2025 | United States | 18.10% |

Marks & Spencer opened a special production line for its Chocolate Strawberry Pistachio Crème sandwich in order to increase production due to the rapidly growing demand for high-quality trend-based chocolate treats. Similarly, other firms can produce limited edition premium chocolate flavors along with setting up special production lines to capitalize on viral food trends and generate additional sales.

IHOP expanded its viral Dubai Chocolate Pancakes offering by introducing a new Dubai Chocolate Milkshake at participating restaurants nationwide, capitalizing on social media-driven flavor trends. Chocolate market firms can therefore partner with chain restaurants and coffee shops to create trend-based chocolates desserts to boost brand value.

Italian luxury chocolates and gelato brand Venchi was launched in India by CocoCart via a premium franchise-based retail strategy to capitalize on the increasing trend of artisanal chocolates and luxury chocolate gifting. Companies could grow via partnerships in premium retail stores based on experience, tapping into the increasing demand for imported chocolates and premium chocolates.

Three new products were launched by CAMPCO to add to their range of premium chocolates to offer innovative experience to consumers in terms of cocoa value-added products. Other manufacturers can also diversify their product range by launching chocolate variants with a premium and local twist, boosting the chocolate market value.

The demand for premium chocolate is increasing, as firms launch unique lines of chocolate based on single-origin cocoa, limited edition collections, and artisanal formulas. Manufacturers are placing more emphasis on sourcing transparency, higher content of cocoa, and regional flavor notes to cater to consumers who desire genuine products. For example, Lindt & Sprüngli keeps adding new lines to its portfolio of premium chocolates called Excellence by developing chocolates based on a specific origin, propelling demand in the chocolate industry. Such actions positively influence branding and enable firms to charge premium prices in the retail, hospitality, and gifting sectors. In April 2026, SMOOR unveiled single-origin chocolates using Andhra Pradesh's Eluru cacao, highlighting premium Indian-origin cocoa and artisanal bean-to-bar craftsmanship.

Major firms producing chocolates are making huge investments into regenerative agriculture and programs aimed at the development of cocoa farmers to ensure long-term availability of cocoa in compliance with increased sustainability requirements. Firms like Nestlé, Mars, and Mondelēz International are implementing traceability platforms, agroforestry projects, and initiatives to increase farmers' incomes in West Africa, reshaping the chocolate market dynamics. These changes make chocolate manufacturers collaborate more actively along the cocoa value chain and reduce supply risks. In June 2026, Lindt achieved 100% Rainforest Alliance-certified cocoa sourcing, strengthening sustainable, traceable supply chains, and responsible cocoa farming.

Manufacturers of chocolate products are diversifying their range of products to include those with high cocoa, low sugar, high protein, probiotic, botanical, and plant-based ingredients in response to changing dietary preferences. Firms like Barry Callebaut are developing chocolate formulations that have low sugar and better nutritional benefits for confectionery brands all over the world. Manufacturers are also innovating products while maintaining the taste without fail, thereby accelerating the chocolate market growth. For example, in February 2025, Mycopreneur launched MycoDay mushroom chocolate, combining functional mushrooms with dark chocolate for cognitive and immune health benefits. Such innovations help firms reach out to healthy consumers, develop premium positioning, and produce differentiated products for foodservice and retailers.

Artificial Intelligence, predictive maintenance, and digital factory technologies are changing the entire chocolate industry dynamics. This involves using advanced methods, inspection systems, smart packaging lines, and data analytics that lead to minimal waste and optimum energy usage. Mondelēz International, for instance, is working towards developing digital manufacturing operations in several manufacturing facilities. Industry 4.0 projects backed by the government all over Germany and other European manufacturing bases are helping firms to adopt production technologies. Similarly, in February 2026, Barry Callebaut launched an AI-powered Global Innovation Center in Singapore, accelerating chocolate innovation, predictive flavor development, and product customization.

Producers are redesigning their packaging to make it more environmentally friendly, convenient, and shelf attractive. Manufacturers are using wrappers made of paper, lighter packaging, and digital printing of their seasonal collections to leverage festive seasons all through the year. Firms like Ferrero are expanding its efforts towards sustainability through the launch of its premium seasonal products in various international chocolate markets. On the other hand, in January 2026, Amcor and Alter Eco introduced recyclable paper-based chocolate packaging, reducing material weight while advancing sustainable confectionery packaging solutions. The European Union Packaging and Packaging Waste Regulation is also encouraging manufacturers to quickly adopt packaging which is recyclable. These moves ensure better sustainability performance and generate more income through premium chocolates.

The Expert Market Research’s report titled “Global Chocolate Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

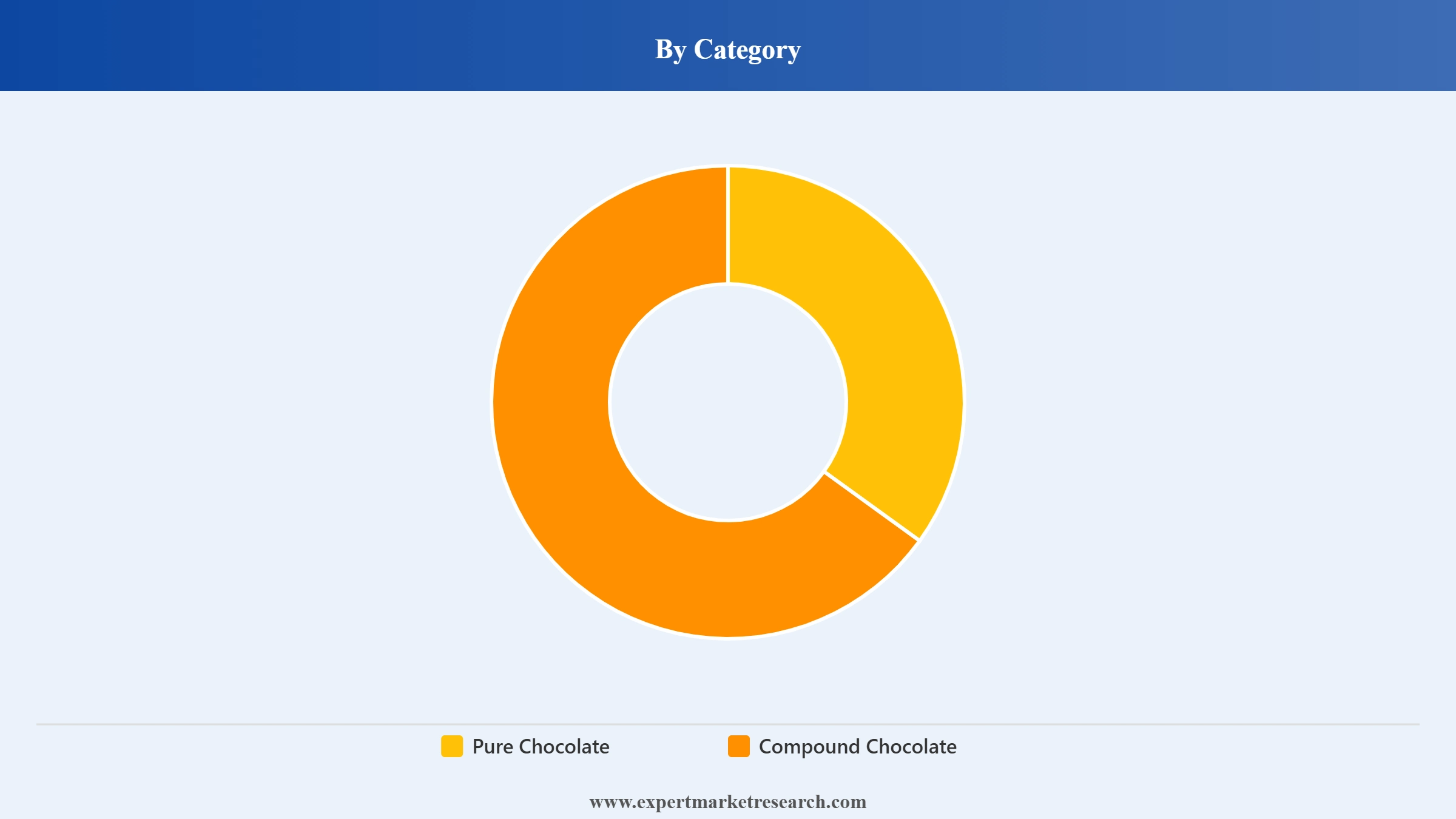

Market Breakup by Category

Key Insight: The chocolate market shows ample growth prospects within each of its segments. The pure chocolate segment remains dominant as the consumers perceive more cocoa content and higher-quality ingredients as indicative of the best product quality and gift-giving potential. At the same time, compound chocolate gains traction since it allows for improved formulation flexibility and process efficiency without sacrificing performance qualities. In May 2026, Barry Callebaut unveiled Cacao Max and ChoViva, expanding premium, sustainable chocolate innovations with cocoa-free confectionery alternatives. Both segments allow catering to the changing consumer needs while meeting the demands of premium retail and industrial manufacturing sectors. Continuous efforts in developing new flavors and optimizing formulations help improve competitiveness in different consumption environments.

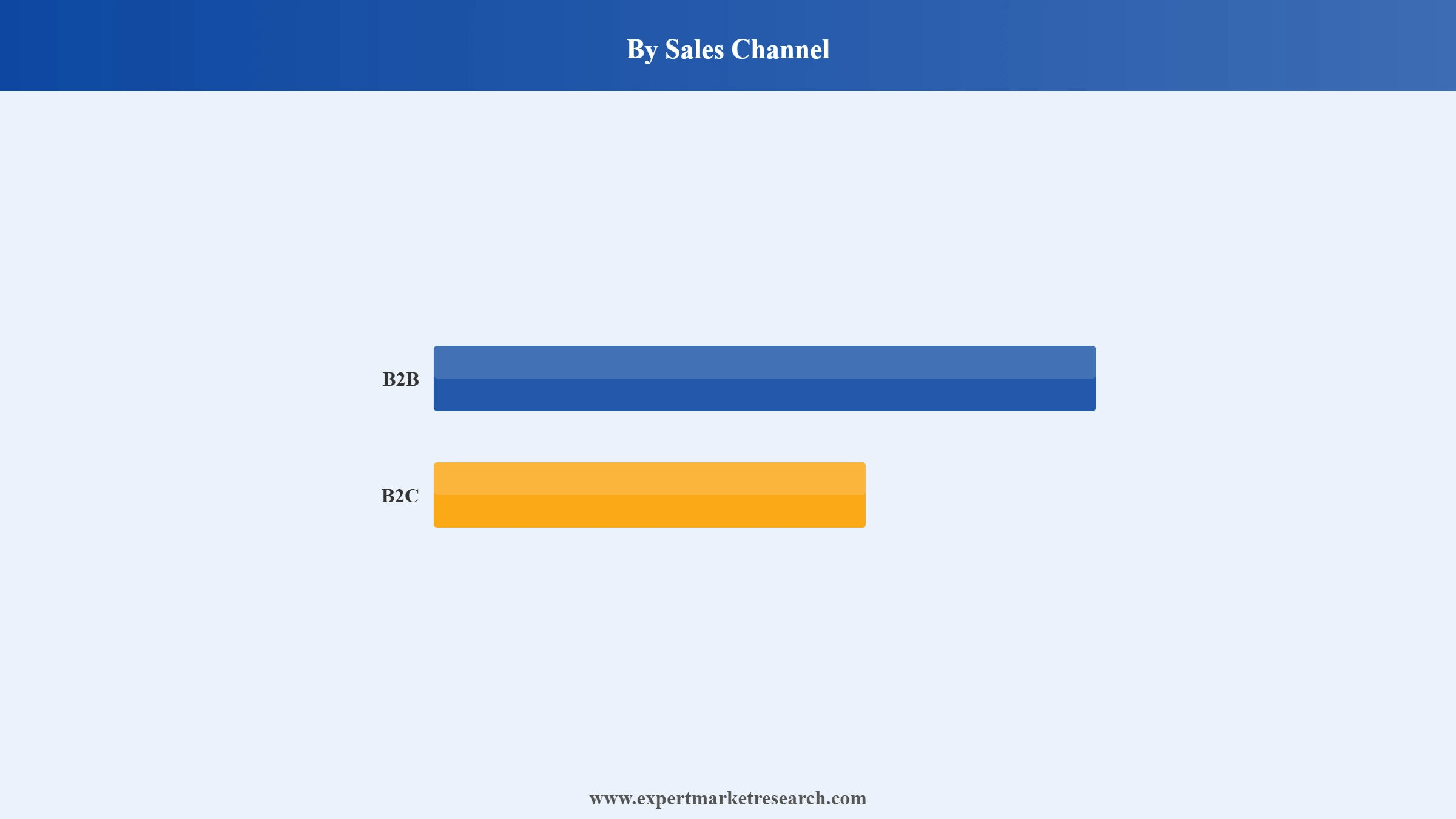

Market Breakup by Sales Channel

Key Insight: The two distribution modes have their own significance in forming the chocolate market scope. B2C continues to be the more prevalent distribution channel due to high levels of retail penetration, seasonal gift giving, premium branding, and increased usage of online shopping. More consumers are looking for personalized products with superior tastes, which is helping retailers grow in the coming years. On the other hand, the market witnesses an increasing demand for the B2B distribution mode as the food industry needs specific types of chocolates for bakery and beverages.

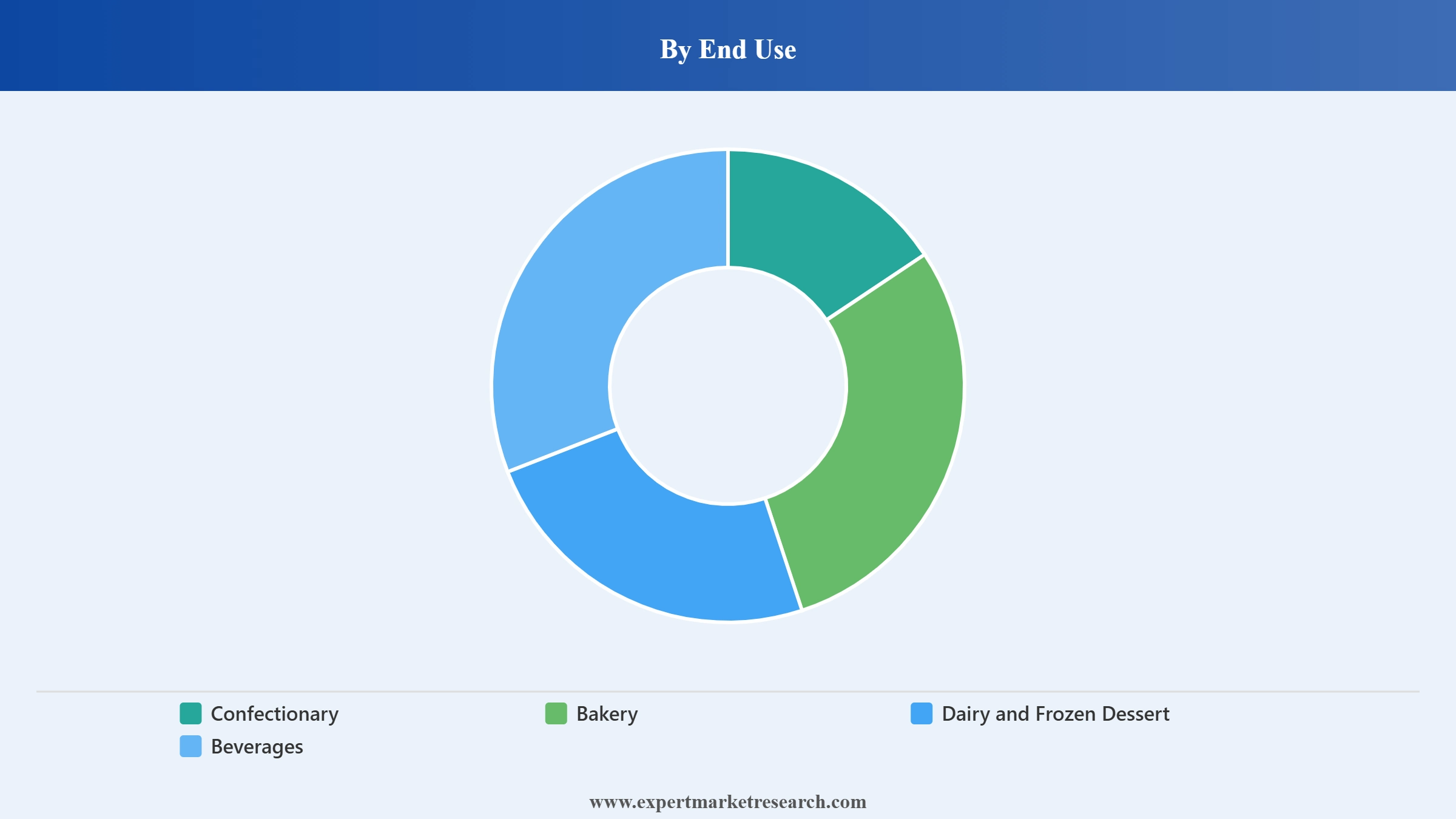

Market Breakup by End Use

Key Insight: End-uses are constantly becoming more varied, with manufacturers developing products designed for many different industrial uses. The confectionery industry is the major market segment as chocolate is often applied as its main component. Chocolate is also being used by bakery manufacturers to add more value to pastries, cakes, cookies, and fillings. Manufacturers of dairy and frozen desserts apply chocolate in order to add value to their products. Beverage manufacturers develop new products with the help of cocoa beverages, boosting demand in the chocolate market. In June 2029, Britannia launched Dubai Kunafa Croissant, capitalizing on viral flavor trends to attract young consumers seeking premium indulgent snacks.

Market Breakup by Region

Key Insight: The demand trends vary regionally due to the differing levels of market maturity and customer preferences. Europe holds its lead position in the global chocolate industry due to the quality chocolate manufacturing skills, innovative abilities, and strong brand loyalty. The region of North America keeps reaping the advantages of product innovation, premium snacking, and seasonal consumption. The Asia Pacific region exhibits high growth potential due to increased disposable incomes that encourage the consumption of chocolate. Latin America is contributing through increased manufacturing investments and consumption, while the regions of Middle East and Africa have potential growth factors such as premium gifting, tourism, and modern retailing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By category, pure chocolate dominates the market through premium quality, authenticity, and broader consumer preference

Pure chocolates occupy the largest share in the chocolate market because of their high percentage of cocoa, premium positioning, and extensive applications in confectionery, bakery, gifting, and food service industries. Chocolate makers are launching darker, milk, and single-origin chocolates in the market with the aim of maximizing profits from such segments. Additionally, consumers' increasing demand for organic and authentic cocoa taste makes this chocolate type gain more popularity. Chocolate manufacturers can strengthen traceability and adopt sustainable cocoa sourcing practices to develop premium chocolate brands that meet growing consumer demand for responsibly produced chocolate products. For example, in June 2026, Havmor launched Belgian Silky Chocolate Cone, delivering premium indulgence through molten chocolate filling and rich Belgian chocolate flavors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Compound chocolates are emerging as the fastest-growing segment in the chocolate market as they are relatively cheaper, easy-to-process, and more consistent when used in manufacturing processes. Vegetable fats replace cocoa butter in chocolate manufacturing, making such products cheaper without compromising quality and consistency. This type of chocolate finds wide applications in bakery fillings, coatings, molded chocolates, ice creams, and quick-service restaurants. Improvements in formulations help companies to launch new products while controlling volatile cocoa costs and manufacturing processes.

By sales channel, the B2C category occupies a substantial share of the market through extensive retail and gifting demand

The B2C sales mode leads the chocolate market revenue owing to its wide availability via supermarket, convenience stores, specialty retailers, online portals, and brands' own store networks. Premium gifting, seasonal editions, and personalized products continue gaining traction from customers who are in search of differentiated products. Manufacturers enhance their omnichannel retail approach, loyalty programs, and direct-to-customer offerings to boost brand engagement. Innovations in products, appealing packaging, and premiumization also drive repeat purchases, making B2C the main channel of revenues in both developed and developing countries' chocolate markets. In April 2026, ITC announced plans to double Fabelle's manufacturing capacity and retail footprint, expanding India's premium luxury chocolate market presence.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The B2B market is growing fast as food producers, bakeries, beverages manufacturers, hotels, and quick-service restaurants continue buying specialized chocolate ingredients. The demand for customized solutions, compound coatings, cocoa inclusions, and premium couverture products continues to grow. Manufacturers are enhancing technical expertise, development cooperation, and application-driven portfolios for commercial clients, widening the chocolate market scope. Increased investments into premium bakery products, frozen desserts, and ready-to-eat products create additional opportunities in the channels of food manufacturing businesses globally.

By end use, confectionery sustains its market leadership through continuous premium chocolate product innovation

Confectionery is the dominant end-use category that is accelerating the chocolate market penetration due to steady consumer demand for chocolate bars, pralines, filled chocolates, gifting items, and luxury assortments. Innovation in terms of flavor, improved formulations, and premium cocoa blends helps differentiate the products. Special packaging, limited editions, and sustainable sourcing enhance the consumer appeal. Increasing urban consumption trends and impulse buying continue fueling demand via supermarkets, specialized stores, and even e-commerce channels. In March 2026, Nestlé launched cocoa-free Choco Crossies Snack Vibes with ChoViva, addressing cocoa shortages through sustainable confectionery innovation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The demand for chocolate-based beverages is growing due to consumer preference for premium hot chocolate, coffee drinks, protein drinks, and functional cocoa beverages. The chocolate market observes an increasing inclination towards reduced sugar, vegan, and premium cocoa beverages by manufacturers in response to changing consumer needs. Ingredients from chocolate are also becoming popular at cafes and food service establishments looking for premium beverages. For instance, in June 2026, Hotel Chocolat launched Coconut Macaroon iced drinking chocolate, expanding premium café beverages with indulgent, coconut-inspired seasonal chocolate experiences.

Europe dominates the market through premium chocolate heritage, innovation, and sustainable cocoa sourcing leadership

Europe retains the position of the largest regional chocolate market due to its developed market for chocolate products, premium consumer preferences, and globally known brands. Countries like Switzerland, Germany, Belgium, and France continue to innovate in premium, organic, and single-origin chocolates. Companies make efforts toward the use of sustainable cocoa supply, recyclable packaging, and more innovative production technology to enhance competitiveness. The presence of well-developed infrastructure for retail, gifting, and exporting ensures Europe’s superiority in the entire global value chain of the market. In October 2025, Foreverland expanded Choruba cocoa-free chocolate production, enabling scalable, sustainable alternatives that reduce cocoa supply chain dependence.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The fastest growing chocolate market is represented by the Asia Pacific region owing to increasing disposable income, growing urbanization, premiumization, and consumption trends similar to those of Western countries. International producers of chocolate continue to expand their manufacturing capacity, work on portfolio localization, and digital strategy of retailing in China, India, Southeast Asia, and Japan. Growing demand for premium gifting products, new flavors, and healthier chocolate alternatives inspires producers to localize manufacturing operations and increase collaborations with retailers and e-commerce businesses.

The competition within the global market is expected to intensify as the emphasis of the chocolate companies are being laid on using high-quality cocoa products, sustainability of sourcing, functionality of chocolate, and state-of-the-art technologies for processing. Chocolate makers are planning on building stronger ties with cocoa farmers, using regenerative agricultural practices, and using digital tracking technology for the sake of meeting the needs of customers and regulations.

Innovation within the industry is now focused on developing formulas of chocolate products that contain less sugar content, as well as plant-based chocolates and specialized ingredients for the use of bakery, dairy, and beverages manufacturers. Several chocolate market players are also expanding their local processing plants in order to increase the resilience of supply chains and reduce risks associated with cocoa sourcing from countries where the crop is produced. In addition, they are developing low-carbon cocoa products, recyclable packaging, and AI technology-based quality management.

Founded in 1996, and based out of Zurich, Switzerland, Barry Callebaut AG is one of the world's leading chocolate and cocoa ingredient producers. The company manufactures customized chocolate products for food companies and food services along with developing low carbon chocolate, cocoa traceability systems, and reduced sugar formulations.

Based in Singapore, established in 2020, Olam Food Ingredients is a producer of sustainable cocoa ingredients and customized chocolate products for global food manufacturers. The company keeps on expanding its AtSource digital traceability platform along with regenerative agriculture, premium cocoa processing, and transparent sourcing programs.

Founded in 1865 and based in Minnesota, United States, Cargill Incorporated provides cocoa powders, chocolate ingredients, and unique formulas for confectionary, bakery, and dairy industries. It concentrates on sophisticated technologies, sustainable sourcing of cocoa beans, innovative cocoa formulas, and collaboration to ensure better quality of ingredients and production processes across international chocolate industries.

Founded in 2004 and based in Johor, Malaysia, Guan Chong Berhad is one of the leading cocoa processors offering cocoa butter, cocoa liquor, cocoa powder, and chocolate ingredients across the world. The company continues to grow through increased processing capacity, sustainable sourcing methods, and development of superior cocoa ingredients for confectionary producers and industrial food processors across international chocolate markets.

Other key players in the market include Fuji Oil Co., Ltd., Mars, Incorporated, Mondelēz International, Inc., Ferrero International S.A., The Hershey Company, Nestlé S.A., Chocoladefabriken Lindt & Sprüngli AG, August Storck KG, United Confectionary, S.L.U., pladis Foods Ltd., Meiji Holdings Co., Ltd., LOTTE Corporation, and Arcor Group, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our chocolate market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2999 $2699

$4399 $3959

$5599 $4759

$6659 $5660

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 48.20 Billion.

The market is projected to grow at a CAGR of 4.90% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035 to reach USD 77.77 Billion by 2035.

Growth is driven by sustained premiumisation, expanding compound-chocolate use across bakery and confectionery, large-scale capex by Barry Callebaut (EUR 250 million Wieze, EUR 125 million Halle, USD 50 million Hershey supply pact), Ferrero's USD 214 million Kinder Bueno plant, the launch of TogetherCocoa to stabilise cocoa supply, and the commercial debut of cocoa-alternative ingredients such as Nestlé's ChoViva.

Compound Chocolate holds the largest share of the market, supported by affordability, ease of use, and broad applicability across bakery, confectionery coatings, and moulded confectionery. Pure Chocolate captures the higher-margin, brand-led segment and is dominated by Lindt, Ferrero, Hershey, Mars, and Mondelēz, with continued growth driven by premiumisation, dark-chocolate health positioning, and seasonal gifting.

Key trends include cross-industry cocoa-supply restructuring (TogetherCocoa launched February 2026), the mainstream commercial debut of cocoa-alternative chocolate (Nestlé ChoViva, March 2026), heavy manufacturing capex (Barry Callebaut's EUR 250 million Wieze, EUR 125 million Halle, Hershey USD 50 million pact, Ferrero USD 214 million Kinder Bueno plant), and accelerating premiumisation with dark-chocolate, plant-based, and functional propositions.

The key players in the market include Barry Callebaut AG, Olam Food Ingredients (OFI), Cargill Incorporated, Mars Incorporated, Mondelēz International, Inc., Ferrero International S.A., The Hershey Company, Nestlé S.A., Chocoladefabriken Lindt & Sprüngli AG, Guan Chong Berhad, Fuji Oil Co., Ltd., August Storck KG, United Confectionary, S.L.U, pladis Foods Ltd., Meiji Holdings Co., Ltd., LOTTE Corporation, Arcor Group and Others.

North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa are the major regions covered in the market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Category |

|

| Breakup by Sales Channel |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,399

USD 3,959

tax inclusive*

Five User License

Five User

USD 5,599

USD 4,759

tax inclusive*

Corporate License

Unlimited Users

USD 6,659

USD 5,660

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.