Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

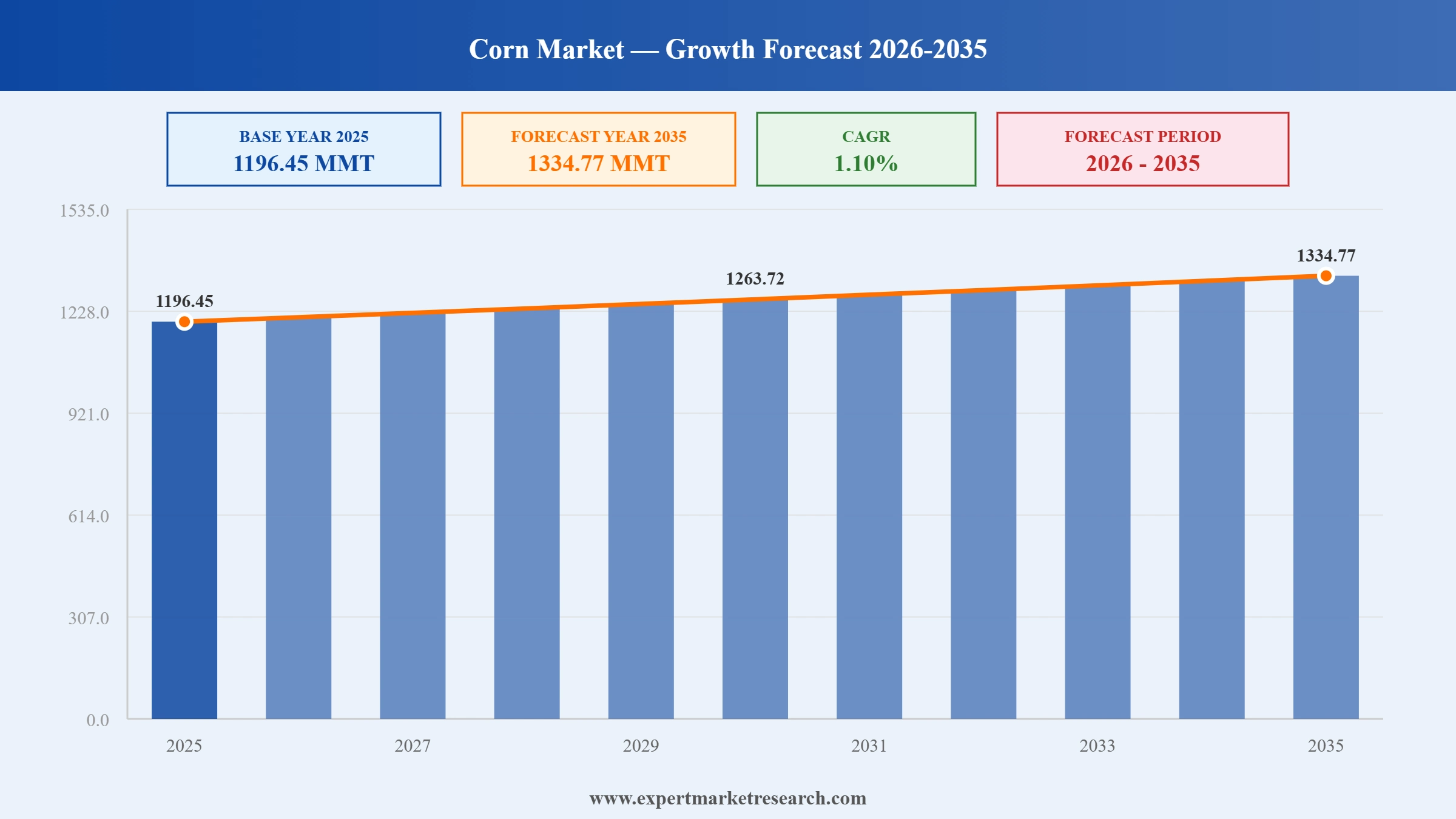

The Global Corn Market reached a volume of 1196.45 MMT at 2025 and is projected to expand at a CAGR of around 1.10% during the forecast period of 2026-2035. With record 2025/26 U.S. and global harvests, sustained animal-feed demand across Asia Pacific, stable U.S. ethanol mandates under the EPA's RFS Set 2 rule, and rising use of corn-based ingredients in food, beverage, and industrial applications, the market is expected to reach 1334.77 MMT by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Corn Market is being shaped by four mutually reinforcing shifts: record 2025/26 production from the United States and South America rebuilding global supply, a stable U.S. ethanol mandate at 15 billion gallons through 2027, the steady expansion of corn-based ingredients into food and beverage applications, and the gradual rise of organic and non-GMO corn varieties supported by clean-label consumer demand and farm-gate price premiums.

On 12 January 2026, USDA confirmed 2025 U.S. corn production at a record 17.02 billion bushels with yields at a record 186.5 bushels per acre across 91.3 million harvested acres-the largest area harvested since 1933. The bumper harvest lifted USDA's forecast for 2025/26 world corn production to roughly 1.265 billion tonnes and reinforced the United States' role in stabilising global corn supply against drought risks in parts of the EU and Black Sea region.

In its February 2026 WASDE report, USDA raised projected 2025/26 U.S. corn exports to a record 3.3 billion bushels, up nearly 27% from 2.6 billion bushels in 2024/25, as overseas demand-particularly from Mexico, Japan, Colombia, South Korea, and Egypt-accelerated against a record 17.02 billion-bushel U.S. harvest. The upgrade reinforced the United States' position as the world's top corn exporter and signalled robust trade momentum despite South American competition from Brazil's 131 MMT and Argentina's 53 MMT crops.

In October 2025, Corteva Agriscience confirmed plans to separate its seed and crop-protection businesses into two independent public companies, slated for completion in the second half of 2026. The split establishes "New Corteva" (crop protection, projected 2025 net sales of USD 7.8 Billion) and a SpinCo housing the Pioneer corn-seed brand (projected 2025 net sales of USD 9.9 Billion). The move sharpens strategic focus, reshapes competitive dynamics in corn genetics, and creates a pure-play corn-seed leader pivotal to global corn-supply economics.

In July 2025, Corteva Agriscience unveiled Lumidapt Valta LS, a biological seed treatment added to its LumiGEN corn package and positioned to deliver naturally derived nutrients that support uniform corn emergence and a measured 2.0 bu./acre yield advantage in multi-year testing. The launch underscores the industry's pivot toward biological inputs alongside genetically engineered traits, helping U.S. and Latin American growers improve early-season vigour while addressing rising consumer and regulatory pressure for reduced synthetic-chemistry footprints.

In 2025, the U.S. EPA finalised the Renewable Fuel Standard "Set 2" rule, holding the conventional biofuel volume requirement at 15 billion gallons for 2026 and 2027-preserving a major source of corn demand. USDA estimates that ethanol producers will use 5.5 billion bushels of corn in 2025/26, representing roughly 43% of total U.S. corn use. The rule provides a multi-year demand anchor for U.S. corn, underwrites Midwestern processing margins, and shapes the long-run supply-demand balance through 2035.

USDA confirmed 2025 U.S. corn production at a record 17.02 billion bushels with yields at a record 186.5 bushels per acre across 91.3 million harvested acres-the highest U.S. corn area since 1933-lifting projected 2025/26 world production to around 1.265 billion tonnes. Brazil's 131 MMT and Argentina's 53 MMT harvests reinforced South American supply, with U.S. exports projected at a record 3.3 billion bushels for 2025/26. The trend matters because it eases the post-2022 supply tightness, supports moderating corn prices, and underwrites Global Corn Market growth across feed, food, and ethanol end-uses worldwide.

The EPA's finalised Renewable Fuel Standard Set 2 rule holds the conventional biofuel volume at 15 billion gallons for 2026 and 2027-a multi-year demand anchor for U.S. corn-based ethanol. With ethanol producers projected to use 5.5 billion bushels of corn in 2025/26, around 43% of total U.S. use, the rule keeps a major buyer locked in even as electric-vehicle adoption rises. The trend also signals that, starting in 2028, foreign fuels and feedstocks will receive half the RFS compliance value of American-made products, sharpening the competitive moat for U.S. corn-ethanol producers.

Corn-derived ingredients-starches, sweeteners, maltodextrin, fibre, and protein concentrates-are the fastest-growing slice of corn-end-use demand. The corn-based ingredients market is projected to reach USD 64.1 Billion by 2035 at a 3.32% CAGR; corn maltodextrin reached USD 1,337.8 Million in 2025, with more than 540 new global food products in 2024 using maltodextrin as a stabiliser, bulking agent, or sweetener substitute. The trend matters because it tilts incremental corn demand toward higher-value applications, supporting wet-milling capacity expansions and CPG-led innovation across bakery, beverages, and snacks.

U.S. organic corn acreage has grown approximately 18% between 2021 and 2025, supported by farm-gate premiums of 10-25% above conventional corn and identity-preserved premiums of USD 0.50-1.20 per bushel for non-GMO varieties. North America accounted for around 38.5% of global non-GMO corn-seed revenues in 2025 (~USD 2.6 Billion) as the broader USD 230 Billion-plus organic food and beverage market expands at roughly 9.5% CAGR. The trend reshapes part of the corn-supply chain toward identity-preserved channels, separate handling logistics, and premium-priced contracts that incentivise selective grower adoption.

The Expert Market Research’s report titled “Corn Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

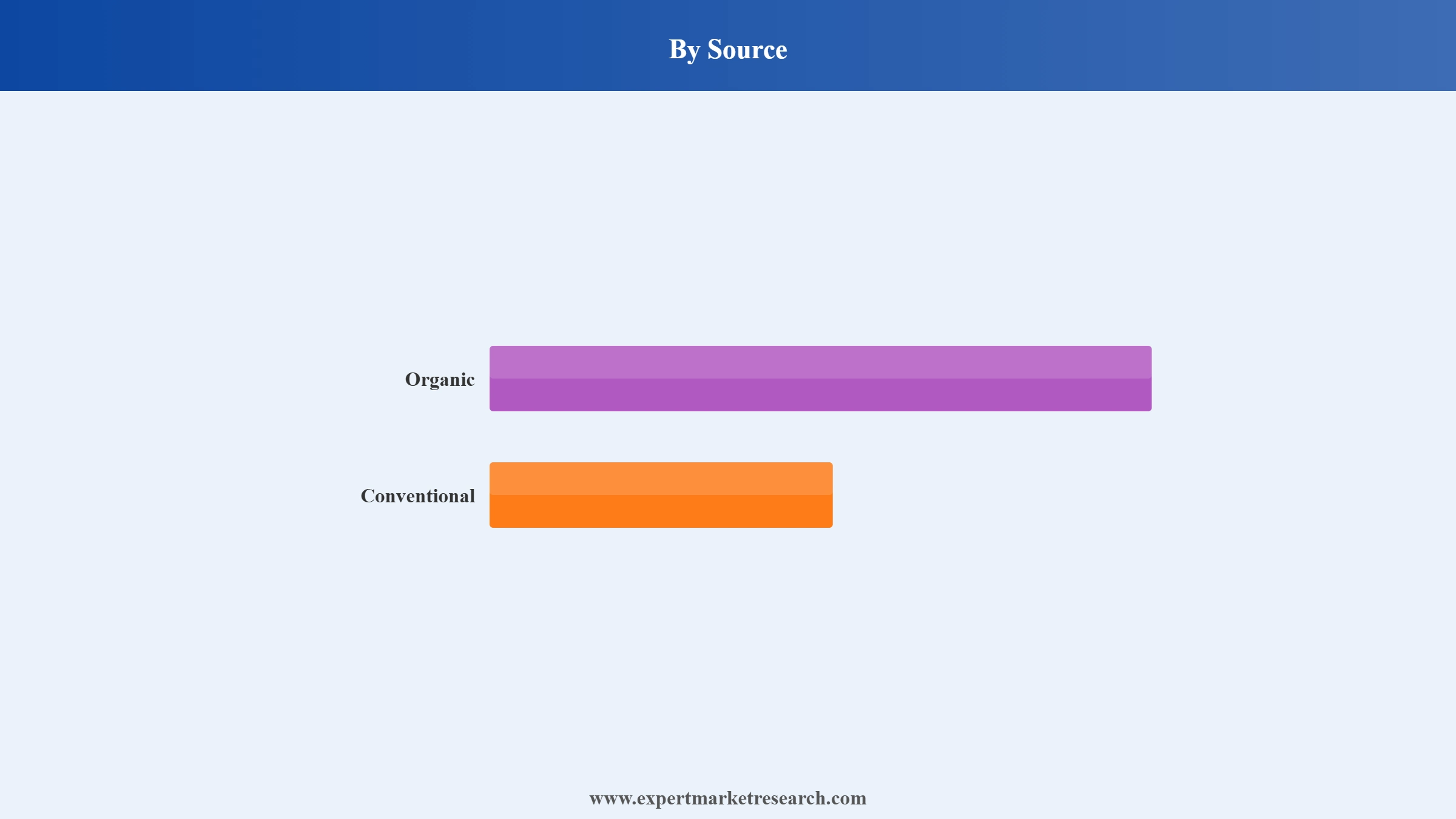

Market Breakup By Source

Key Insight: Conventional corn dominates the global market, accounting for the vast majority of the 1,196.45 MMT 2025 production, anchored by genetically engineered traits, scaled mechanised farming in the U.S., Brazil, Argentina, and Ukraine, and well-established input ecosystems from Bayer, Corteva (Pioneer), Syngenta, and BASF. Organic corn is a smaller but faster-growing slice-the global organic corn market reached around USD 1,084 Million in 2025 with a 3.1% CAGR-propelled by the broader USD 230 Billion-plus organic food and beverage market growing at 9.5% CAGR. U.S. organic corn acreage has grown roughly 18% from 2021 to 2025 on the back of premium pricing and clean-label demand.

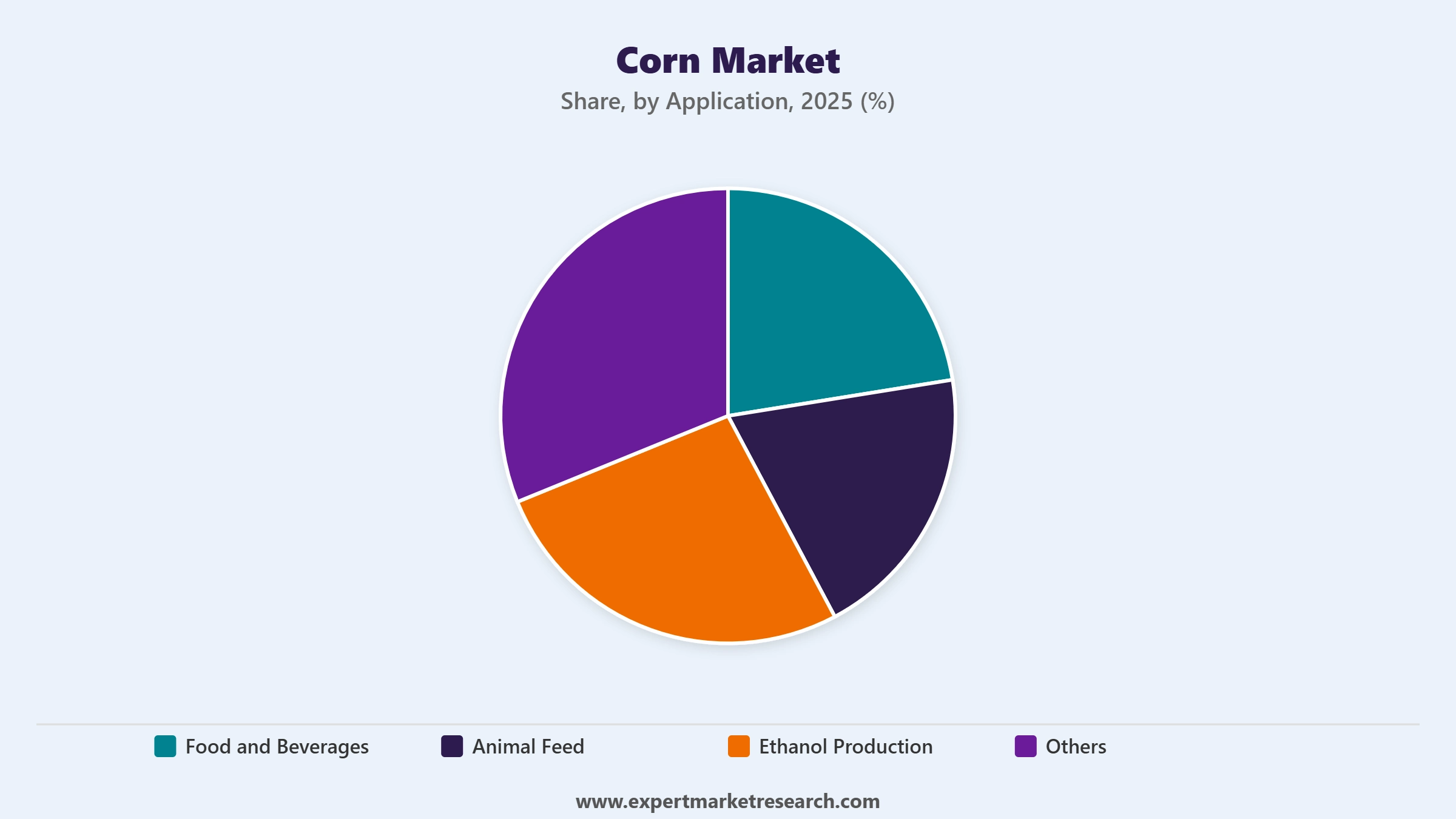

Market Breakup by Applications

Key Insight: Animal Feed anchors the largest share of global corn consumption, supported by sustained livestock and poultry production across Asia Pacific, Latin America, and Sub-Saharan Africa, alongside structural demand from Brazil and the United States as the two largest meat producers. Ethanol Production is the largest single end-use of U.S. corn at around 43% of domestic use, underpinned by the EPA's Renewable Fuel Standard at 15 billion gallons through 2027. Food and Beverages, while a smaller share, is the most strategically dynamic application, with corn starches, sweeteners, maltodextrin, fibre and protein concentrates expanding across bakery, beverage, snack, and pharmaceutical formulations. Others include industrial applications such as bioplastics, paper, and personal care.

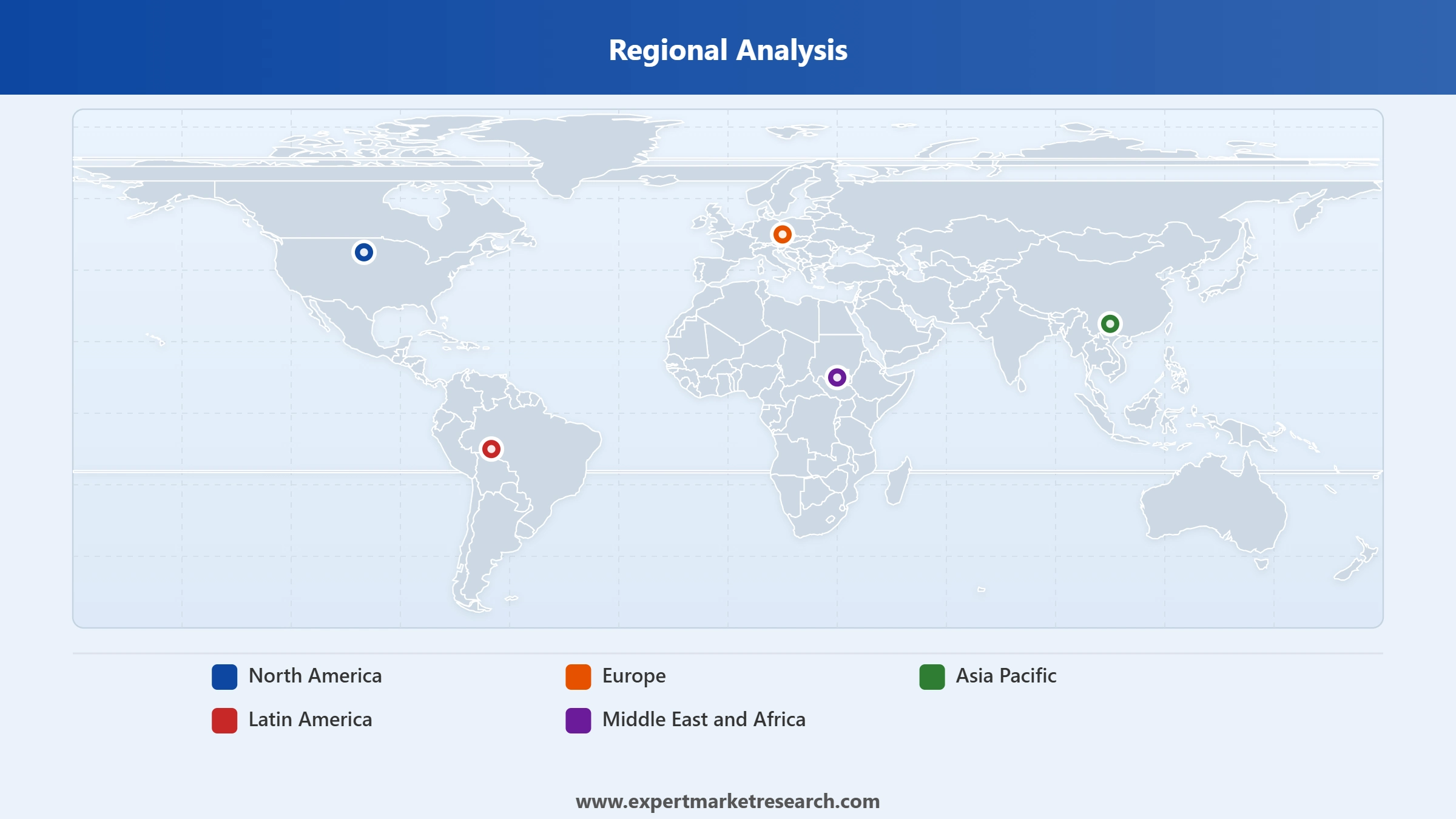

Market Breakup by Region

Key Insight: North America anchors global corn supply with the United States producing a record 17.02 billion bushels (around 419 MMT) in 2025 across 91.3 million harvested acres, paired with Canada's growing crop. Latin America is the second-largest production region, led by Brazil at 131 MMT and Argentina at 53 MMT for 2025/26, both major exporters to China, the European Union, Egypt, and ASEAN. Asia Pacific is the largest consumption region, anchored by China's deep livestock-feed demand, Indian and Indonesian feed-and-food use, and Vietnamese poultry expansion. Europe is a structural net importer with Romania, France, Hungary, and Bulgaria as key producers. Middle East and Africa are net-import dependent, led by Egypt and Sub-Saharan Africa.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Source, Conventional corn dominates the market with the overwhelming majority of the 1,196.45 MMT 2025 global production, anchored by genetically engineered varieties, mechanised farming, and well-established global trading systems. Conventional corn benefits from scale economics across the U.S. Corn Belt, Brazilian Cerrado, and Argentine Pampas, with the world's largest seed companies (Bayer, Corteva/Pioneer, Syngenta, BASF) supplying traited hybrids that drive yield gains-evidenced by U.S. yields hitting a record 186.5 bushels per acre in 2025. Organic corn is the faster-growing source, supported by 18% U.S. acreage growth between 2021 and 2025 and farm-gate premiums of 10-25% above conventional, but it remains a small share of total volume.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Animal Feed dominates the application share, anchored by the world's largest livestock and poultry production complexes in China, the United States, Brazil, the European Union, India, and Mexico. Ethanol Production is the second-largest application globally and the largest single end-use of U.S. corn at around 43% of domestic use, with EPA's RFS Set 2 rule preserving 15 billion gallons of conventional biofuel volume for 2026 and 2027 and providing a multi-year demand anchor. Food and Beverages is a smaller share but the most innovation-led slice, with corn-based ingredients (sweeteners, starches, maltodextrin, fibre, protein) projected to reach USD 64.1 Billion by 2035 at 3.32% CAGR thanks to expanding bakery, beverage, and snack applications.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America anchors global corn supply and is the largest single regional contributor to the Global Corn Market. The United States produced a record 17.02 billion bushels (around 419 MMT) in 2025 with record yields of 186.5 bushels per acre across 91.3 million harvested acres-the largest U.S. corn area since 1933-and 2025/26 exports projected at a record 3.3 billion bushels. The region benefits from deep wet-milling capacity (ADM, Cargill, Tate & Lyle), the world's largest ethanol industry locked in by EPA's 15-billion-gallon Renewable Fuel Standard through 2027, and ongoing seed innovation from Corteva (Pioneer) and Bayer that lifts yields and disease resistance. Mexico is the United States' largest corn export destination and a critical livestock-feed demand pillar.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Latin America is the fastest-growing major corn region by export volume, anchored by Brazil's 131 MMT and Argentina's 53 MMT 2025/26 harvests and rising export flows of around 43 MMT (Brazil) and 37 MMT (Argentina) to China, the European Union, Egypt, and ASEAN economies. Brazilian safrinha (second-crop) corn has materially shifted global supply seasonality, with Mato Grosso, Paraná, and Goiás as key producing states, while Argentina's Pampas pampers Mercosur supply. Latin American competitiveness has been further reinforced by infrastructure investment in northern Brazilian export corridors (Northern Arc), competitive logistics costs, and a steadily improving operating environment for international grain traders such as Cargill, ADM, Bunge, and Cofco.

The Global Corn Market is structurally fragmented at the production layer-anchored by millions of growers across the U.S. Corn Belt, Brazilian Cerrado, Argentine Pampas, Ukrainian and EU farmlands, and the Chinese Northeast Plain-but more concentrated at the seed, crop-protection, trading, and processing layers. Bayer, Corteva (Pioneer), Syngenta, and BASF lead seed and crop-protection economics, while ADM, Cargill, Bunge, COFCO, Louis Dreyfus, and Glencore Agriculture dominate global corn trading.

Strategic priorities cluster around yield-lifting genetics, biological seed treatments, identity-preserved organic and non-GMO supply chains, vertical integration with ethanol and wet-milling assets, and exposure to South American export growth. Major moves-Corteva's October 2025 announcement to spin off its seed business as a Pioneer-anchored pure-play, the EPA's RFS Set 2 finalisation, and Brazil's continued safrinha investment-are reshaping competitive positions across breeders, traders, processors, and ethanol producers through 2035.

Discover the latest insights on the Global Corn Market 2026 with our comprehensive report. Stay ahead of the curve with detailed data on global production and consumption, HS Code 1005 trade flows, regional pricing, ethanol policy, and the seed and processing innovations reshaping corn supply through 2035. Whether you are a trader, ethanol producer, food manufacturer, or investor sizing the agricultural supercycle, this report provides the clarity you need. Download your free sample now and unlock the key opportunities in the thriving Global Corn industry.

Corn Demand and Investment Expansion Trends

Corn Innovation And Product Strategy Analysis

Corn Pricing And Demand Cycle Industry Trends

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the corn market reached an approximate volume of 1196.45 MMT.

The market is projected to grow at a CAGR of 1.10% between 2026 and 2035.

The market is being driven by the growing demand for sorbitol and the rising use of corn in end-use industries, such as personal care and pharmaceuticals, among others.

The key trends guiding the market include the rising demand for corn in the animal feed sector and the growing uses of corn as ethanol fuel.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The significant applications of corn include food and beverages, animal feed, and ethanol production, among others.

The major sources of corn are organic and conventional.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a volume of around 1334.77 MMT by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| Report Features | Details |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Source |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.