Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The Europe beer processing market was valued at USD 281.28 Billion in 2025. The market is expected to grow at a CAGR of 4.20% during the forecast period of 2026-2035 to reach a value of USD 424.44 Billion by 2035. The market is undergoing a significant transformation driven by decarbonization of logistics, automation in supply chains, and sustainability-led production strategies adopted by leading brewers.

Increasing adoption of automation and digital process control systems is emerging as a key driving factor that is supporting efficiency improvements in brewing operations. Modern breweries are integrating advanced monitoring, fermentation control, and predictive maintenance technologies to optimize production cycles and reduce operational losses. At the same time, growing demand for diversified beer portfolios, including craft-inspired, flavored, and low-alcohol variants, is encouraging processors to upgrade brewing infrastructure with flexible processing equipment capable of handling varied ingredients and brewing techniques, thereby strengthening production adaptability and supporting long-term growth in the Europe beer processing market.

Companies across the region are increasingly integrating electric mobility solutions and smart logistics systems to reduce carbon intensity while improving operational efficiency across brewing and distribution networks. This shift is further supported by rising investments in renewable-powered transportation and digitally optimized fleet management, which are helping brewers streamline beer movement from production facilities to end markets. As a result, logistics is becoming a strategic extension of beer processing operations rather than a standalone function, enhancing overall value chain efficiency within the Europe beer processing market.

A strong illustration of this trend is Carlsberg’s continued push toward green logistics in Sweden. In April 2025, Carlsberg Sweden advanced its collaboration with Einride to expand electric freight operations, supporting a transition toward zero-emission beer transportation across its distribution network. The initiative also includes the launch of a limited “electric beer,” brewed and transported using renewable energy, showcasing the integration of sustainable production and logistics innovation.

Compound Annual Growth Rate

4.2%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Diageo expanded its brewing footprint with the EUR 300 million Newbridge brewery, strengthening large-scale production capabilities in the Europe beer processing market. The facility improved operational efficiency, modernized brewing infrastructure, and enhanced output scalability, supporting rising demand for premium and export-oriented beer production across European markets.

Heineken reaffirmed its Brew a Better World roadmap at its AGM, focusing on renewable thermal energy, water reduction, and increased low- and no-alcohol production. These initiatives strengthened investment flows into energy-efficient brewing systems, supporting long-term sustainable growth in the Europe beer processing industry.

Carlsberg advanced its Fiber Bottle rollout and energy efficiency initiatives across European breweries, integrating heat pumps, biogas, and CO₂ recovery systems. These developments supported emissions reduction targets and improved process efficiency, reinforcing modernization trends in the Europe beer processing market amid tightening EU climate regulations.

ABB launched a new cold-block process automation solution for beer production, enhancing fermentation control and operational efficiency. The system improved energy optimization and production consistency, contributing to digital transformation and higher productivity within the market.

Premiumization strategies continue to shape brewing dynamics across Europe as companies introduce globally recognized brands into new regional markets to capture evolving consumer preferences. Expanding premium beer portfolios allows brewers to strengthen presence in hospitality and retail channels while competing more effectively in high-value segments. These launches also stimulate brewing volumes and reinforce demand for advanced processing capabilities to maintain consistent product quality. Reflecting this trend, in January 2026, AB InBev introduced its premium lager Stella Artois into the Netherlands, first through restaurants and bars and later through major retailers such as Albert Heijn, Jumbo, and Plus, supporting expansion of the Europe beer processing market.

Changing consumption patterns, inflationary pressures, and rising energy costs are prompting brewers to reassess operational footprints across Europe. Producers increasingly consolidate production or close underperforming facilities while redirecting investments toward technologically advanced brewing plants capable of delivering higher efficiency and lower emissions. These structural shifts encourage modernization of brewing infrastructure and improved capacity utilization across regional production networks. This trend was highlighted in January 2026, when the European Beer Consumers Union discussed growing brewery closures and evolving market dynamics, reflecting broader operational transformation across the Europe beer processing market.

Brand development strategies are increasingly shaping production planning as brewers seek to strengthen global brand positioning and premium product visibility. Expanding marketing collaborations enables companies to execute coordinated campaigns across multiple markets, helping flagship labels reach wider audiences and maintain consistent brand narratives. Stronger brand engagement is supporting stable demand and reinforcing production volumes across brewing facilities. Demonstrating this trend, Heineken appointed new global marketing agencies in May 2026 to accelerate the next phase of brand growth, sustaining demand in the Europe beer processing market.

Growing consumer interest in healthier beverage choices is accelerating investment in alcohol-free and low-alcohol beer innovation across Europe. Brewers and beverage companies are pursuing acquisitions to rapidly strengthen their presence in this expanding segment while leveraging existing brewing infrastructure. These developments also stimulate adoption of advanced dealcoholization and flavor preservation technologies within production systems. Illustrating this trend, Sunrise Beverages acquired a leading zero-alcohol beer brand in May 2026, reinforcing diversification strategies shaping the Europe beer processing market dynamics.

Partnership-driven expansion is becoming an effective strategy for craft beer brands seeking broader international reach without establishing new production facilities. By collaborating with established brewers that possess large-scale brewing capacity and distribution networks, small-scale brands are gaining access to wider markets while maintaining product authenticity. Such collaborations also expand the diversity of beer offerings available to European consumers. A notable example occurred in March 2024, when Bavarian craft brand Starnberger partnered with Krombacher for its European launch, highlighting how cooperative growth strategies contribute to the development of the Europe beer processing market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research’s report titled “Europe Beer Processing Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

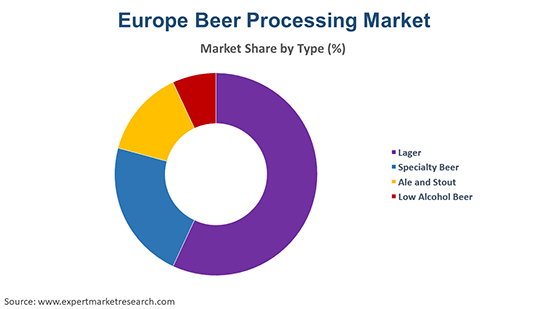

Market Breakup by Type

Key Insight: Product diversification across lager, speciality beer, ale and stout, and low alcohol beer continues to shape production strategies within the Europe beer processing market. Lager remains the dominant segment due to high consumer familiarity and large-scale brewing efficiency, while speciality beer gains traction through craft innovation and flavored variants. Ale and stout maintain steady demand in premium and heritage-driven markets, whereas low alcohol beer expands rapidly amid health-conscious consumption trends. Reflecting innovation in speciality beer, Molson Coors launched Madri Excepcional Limón fruit beer in April 2026, illustrating how brewers are introducing new flavors to stimulate category growth and broaden product portfolios.

Market Breakup by Distribution Channel

Key Insight: Distribution across hypermarkets and supermarkets, liquor stores, convenience stores, and other channels continue to influence purchasing patterns, thereby impacting the Europe beer processing market value. Hypermarkets and supermarkets dominate due to wide product availability and competitive pricing, while liquor stores play a key role in premium and craft beer sales. Convenience stores support impulse purchases and urban consumption trends, whereas other channels such as online retail and on-trade venues expand accessibility. Major brewers including Heineken, Carlsberg, and AB InBev are strengthening retail partnerships and expanding shelf presence across these channels to improve market penetration and maintain steady product circulation.

Market Breakup by Region

Key Insight: Regional dynamics across Germany, the United Kingdom, France, Russia, and other European markets collectively shape the Europe beer processing market trends through varying consumption habits and brewing traditions. Germany remains a production powerhouse driven by strong brewing heritage, while the United Kingdom supports growth through craft beer innovation. France is expanding premium beer demand, and Russia contributes to the market development through large-scale production volumes. Other markets continue to grow through new product experimentation and sustainability initiatives. For instance, Carlsberg and Brooklyn Brewery introduced a lager brewed with drought-resistant fonio grain in July 2024, highlighting innovation supporting sustainable brewing across European regions.

By type, lager beer witnesses high demand supported by premium brand expansion and localized brewing

Lager continues to dominate brewing volumes due to its widespread consumer acceptance, scalable production processes, and strong presence across retail and hospitality channels. Brewers are increasingly introducing new lager variants and expanding localized production to strengthen regional demand. Product innovation and brand extensions help maintain competitiveness while appealing to evolving taste preferences.

Meanwhile, low alcohol beer is emerging as one of the fastest-growing segments as consumers increasingly seek healthier beverage alternatives without compromising taste. Brewers are investing in advanced dealcoholization technologies and refined brewing methods to retain flavor while reducing alcohol content. The segment is further supported by regulatory encouragement and expanding availability in mainstream retail. Demonstrating this momentum, Heineken 0.0 introduced the first zero-alcohol, zero-calorie, and zero-sugar beer in March 2026, highlighting how product innovation is strengthening the low alcohol beer segment in the Europe beer processing market.

By distribution channel, hypermarkets & supermarkets are strengthening large-scale retail beer distribution

Hypermarkets and supermarkets remain the dominant retail channel for beer sales due to wide product assortment, competitive pricing, and strong consumer footfall. Brewers actively collaborate with major retail chains to launch seasonal and exclusive products that drive in-store demand and enhance brand visibility. Large-scale retail networks also enable efficient distribution of both mainstream and craft beer offerings. For example, Wold Top Brewery launched new seasonal beers through Asda in May 2026, demonstrating how partnerships with large supermarket chains continue to support distribution expansion within the Europe beer processing market.

On the other hand, convenience stores play a critical role in urban beer consumption by offering quick access to single-serve and ready-to-drink products. The channel increasingly supports the expansion of alcohol-free and low-alcohol variants that appeal to on-the-go consumers seeking lighter beverage options. Brewers are introducing compact packaging and accessible product formats to strengthen this retail segment. Reflecting this shift, a Belgian beer producer introduced a new alcohol-free beer offering in February 2026, highlighting how product launches aligned with convenience retail formats are reinforcing growth in the Europe beer processing market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By region, United Kingdom dominates the market growth driven by premium brand launches and local brewing expansion

The United Kingdom remains a significant brewing hub characterized by strong demand for premium, craft, and international beer brands. Breweries are expanding local production of globally recognized labels while introducing new products tailored to domestic tastes. Strategic brand launches and localized brewing help companies strengthen supply chains and improve responsiveness to market demand. Illustrating this trend, AB InBev launched Via Roma lager and introduced locally brewed Leffe in the United Kingdom in December 2023, highlighting ongoing investment and product diversification supporting the Europe beer processing market.

Besides, Germany continues to be one of Europe’s most influential beer markets due to its strong brewing heritage and high per-capita consumption. The market is experiencing notable growth in non-alcoholic beer as health-conscious consumers increasingly shift toward lighter beverage alternatives. Brewers are expanding alcohol-free production lines and investing in improved dealcoholization technologies to meet rising demand.

Leading Europe beer processing market players are increasingly prioritizing process optimization and sustainability-driven modernization to strengthen operational efficiency and meet evolving regulatory expectations. Investments in energy-efficient brewing equipment, heat recovery systems, and advanced automation technologies are helping processors reduce production costs while improving consistency and output quality. At the same time, producers are upgrading fermentation, filtration, and packaging lines to support diversified product portfolios including flavored, craft, and alcohol-free variants.

Beer processing companies in Europe are also focusing on portfolio diversification, distribution expansion, and consumer-centric innovation to maintain competitive positioning. Companies are introducing new flavor profiles, functional beers, and low-alcohol alternatives while aligning production with changing consumer preferences. In parallel, stronger collaboration with retail chains and hospitality networks is improving product accessibility across major distribution channels. Investments in digital supply chain management, smart logistics, and localized brewing capacity are further strengthening market reach.

Established in 2008 and headquartered in Leuven, Belgium, Anheuser-Busch InBev SA/NV is one of the world’s largest brewing companies with an extensive portfolio of global and regional beer brands. The company focuses on large-scale brewing operations, premium brand development, and continuous investments in brewing technology and sustainability initiatives.

Established in 1864 and headquartered in Amsterdam, Netherlands, Heineken N.V. operates a vast network of breweries across multiple international markets. The company emphasizes premium beer production, product innovation, and expansion in low- and no-alcohol beer segments to strengthen its global brewing presence.

Established in 1847 and headquartered in Copenhagen, Denmark, the Carlsberg Group is a major global brewer recognized for its strong European brewing footprint. The company invests in sustainable brewing practices, advanced processing technologies, and product diversification to enhance its beer portfolio worldwide.

Established in 1883 and headquartered in Skælskør, Denmark, Harboes Bryggeri A/S produces a range of beer, malt beverages, and soft drinks for international markets. The company focuses on efficient brewing processes and export-oriented production to support its presence across Europe and other global regions.

Other key players in the market include Oettinger Brauerei Gmbh, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest trends shaping the Europe beer processing market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on Europe beer processing market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The Europe beer processing market is expected to grow at a CAGR of 4.20% in the forecast period of 2026-2035.

The major drivers of the market include the growing number of micro-breweries and small and medium-sized companies in the area.

Supermarkets and restaurants extending their ranges to include items from local brewers and craft beer and increasing preference for beer as an alcoholic beverage are the key trends in the market.

The major countries in the Europe beer processing market are Germany, the United Kingdom, France, and Russia, among others.

The leading types of beer processing in the market are lager, speciality beer, ale and stout, and low alcohol beer.

The major distribution channels in the market are hypermarkets and supermarkets, liquor stores, and convenience stores, among others.

The key players in the market are Anheuser-Busch InBev SA/NV, Heineken N.V., Carlsberg Group, Harboes Bryggeri A/S, and Oettinger Brauerei Gmbh, among others.

In 2025, the Europe beer processing market reached an approximate value of USD 281.28 Billion.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.