Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

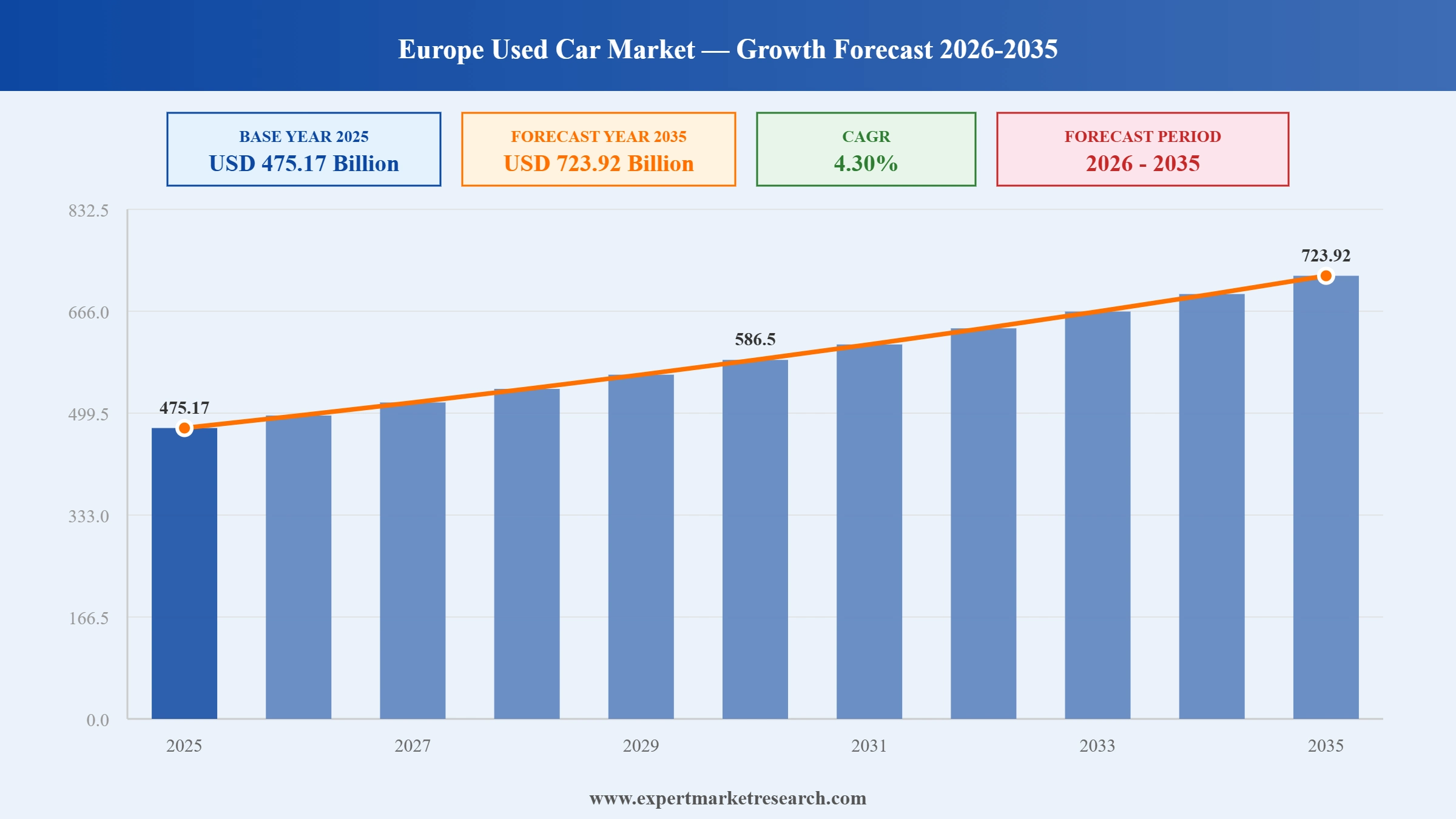

The Europe Used Car Market reached a value of USD 475.17 Billion at 2025 and is projected to expand at a CAGR of around 4.30% during the forecast period of 2026-2035. With rising new vehicle prices accelerating the shift to pre-owned alternatives, rapid digitalisation of used car retail, growing penetration of OEM-backed certified pre-owned programs, and increasing electrification of the used vehicle pool, the market is expected to reach USD 723.92 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Europe Used Car Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 475.17 |

| Market Size 2035 | USD Billion | 723.92 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.30% |

| CAGR 2026-2035 - Market by Country | Germany | 4.9% |

| CAGR 2026-2035 - Market by Country | United Kingdom | 4.6% |

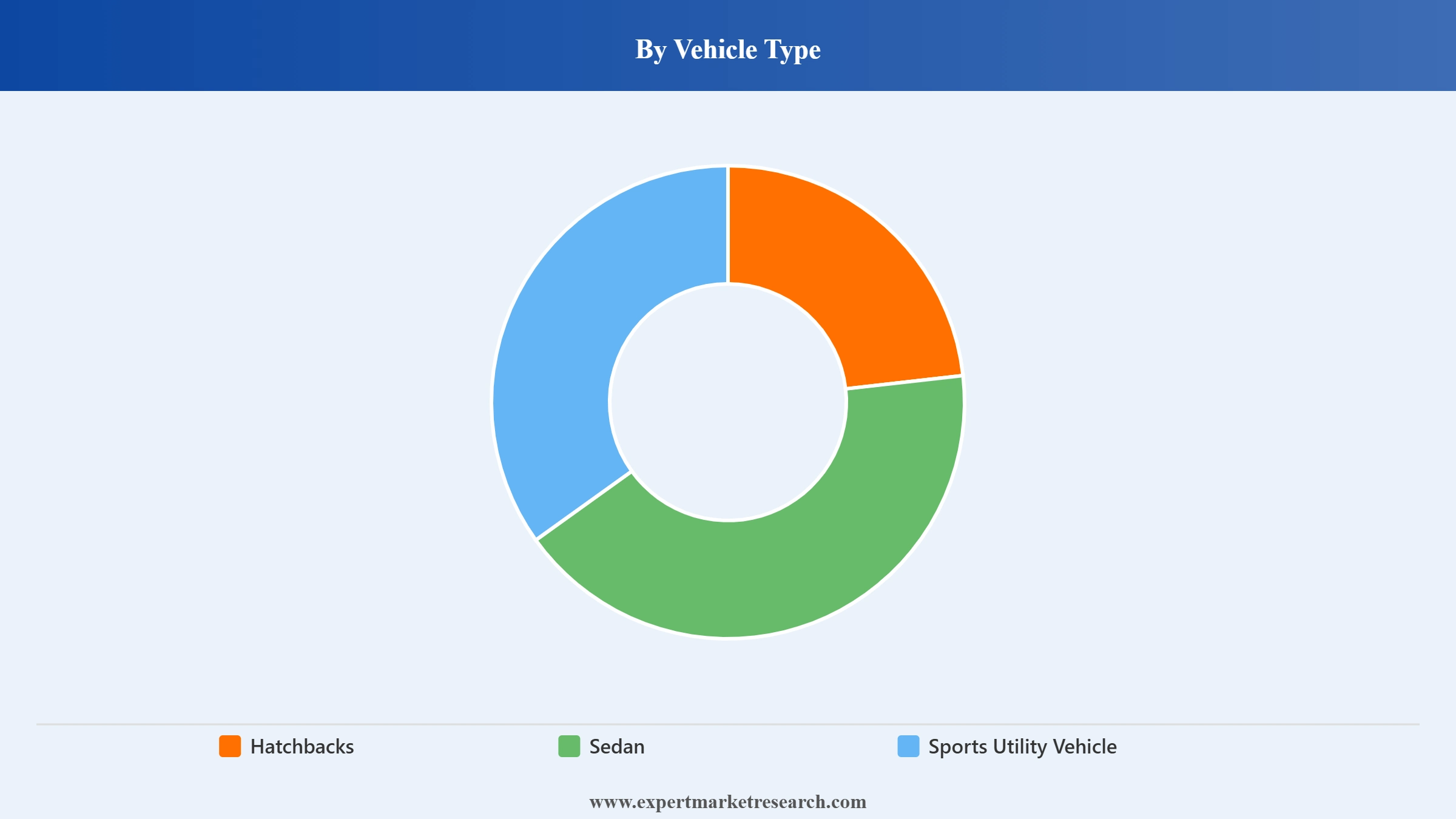

| CAGR 2026-2035 - Market by Vehicle Type | Sports Utility Vehicle (SUV) | 4.8% |

| CAGR 2026-2035 - Market by Sales Channel | Online | 6.0% |

| 2025 Market Share by Country | Germany | 21.4% |

The Europe used car market is undergoing a meaningful structural transformation, shaped by the accelerating electrification of the used vehicle pool, rapid digital adoption among buyers and sellers, consolidation among major dealer groups, and the EU's regulatory push toward zero-emission mobility. These forces are simultaneously disrupting established market dynamics and creating new growth avenues for well-positioned players.

In November 2025, Arnold Clark Automobiles was confirmed as the United Kingdom's most profitable car dealer for 2024, posting GBP 380 million in EBITDA as per the Car Dealer Top 100 report. The result underscores Arnold Clark's commanding market position in both new and used vehicle retail across its network of over 200 UK dealerships. The group attributed its performance to investments in digital systems and the expansion of its EV charging infrastructure under the Arnold Clark Charge initiative, as well as a broadening luxury vehicle portfolio, which together supported its resilience through a challenging year for the broader motor trade.

In September 2024, Van Mossel Automotive Group signed an agreement to acquire Nord-Ostsee Automobile SE and Co KG, a move that significantly expanded the group's dealership footprint across Germany. The deal is part of Van Mossel's broader strategy to grow its presence in one of Europe's most mature and competitive used car markets. Germany accounts for approximately 21.4% of the European used car market and is among the continent's most active cross-border vehicle trading hubs. The acquisition further illustrates the consolidation underway in the European automotive retail landscape, with major dealer groups aggressively pursuing buy-and-build strategies to achieve scale.

In July 2025, Penske Automotive Group completed the acquisition of a Ferrari dealership in Modena, Italy, a move expected to contribute approximately USD 40 million in annual revenue to the group's European operations. The acquisition extends Penske's luxury automotive footprint in continental Europe and positions the group to capture growing demand for premium pre-owned vehicles in the Italian market. The deal reflects broader consolidation trends across the European automotive retail sector, where large dealer groups are increasingly acquiring specialist and luxury franchises to diversify their brand portfolios and strengthen their geographic presence.

In June 2025, Athenaeum International Holdings agreed to acquire Johnsons Cars, a transaction that propelled the combined entity into the ranks of the United Kingdom's top ten automotive retail groups. The deal exemplifies the ongoing consolidation wave reshaping the European used car dealership landscape, as private equity-backed groups and strategic buyers compete to build scale in an increasingly competitive market. Johnsons Cars had operated a multi-brand dealership network across several UK regions, and its absorption into a larger retail group is expected to unlock operational efficiencies and expand access to digital used car retail capabilities.

In April 2024, used vehicle demand across Europe registered strong momentum, with Spain recording a 38.3% year-on-year increase in second-hand automotive demand and the United Kingdom posting a 9.1% monthly surge in used car transactions. France saw used car transactions climb by 10.4% in the same month, with the government-certified sustainable vehicle category posting a 64% demand increase. Italy recorded a 9% total transaction volume surge in the second quarter of 2024, reaching 1,350,123 units. These trends collectively reflect a structural shift in European consumer behaviour toward pre-owned vehicles, driven by elevated new car prices, persistent supply chain constraints, and growing environmental awareness.

Used vehicle demand across Europe accelerated notably during 2024, with multiple major markets posting strong transactional growth. In April 2024, Spain recorded a 38.3% year-on-year surge in second-hand automotive demand, while the UK saw monthly used car transactions climb by 9.1%. Italy's Q2 2024 transaction volume reached 1,350,123 units, a 9% increase over the prior period. France's government-certified sustainable vehicle category posted demand increases of 64% in April and 73% in June 2024. These regional data points reflect a continent-wide shift toward pre-owned vehicles as consumers navigate elevated new car pricing and supply constraints that continue to define Europe used car market growth.

The European used electric vehicle segment is emerging as one of the market's fastest-growing categories, underpinned by the growing volume of early-generation EVs entering the secondary market as original owners upgrade to newer models. Battery-electric vehicles posted a CAGR of approximately 17.95% in the used car segment through 2031, according to industry analysis. Countries including Norway, Germany, and the Netherlands lead in used EV availability due to earlier adoption cycles. The EU's mandate to ban new ICE vehicle sales from 2035 is accelerating consumer interest in used EVs, while manufacturers are extending warranties and battery health certifications to support buyer confidence in pre-owned electric vehicles.

Europe's automotive retail sector experienced significant ownership restructuring through 2024 and 2025, with approximately 9% of all franchise points changing hands between January 2022 and September 2025. Major acquisitions during this period included Lithia and Driveway's GBP 397 million purchase of Pendragon Plc's automotive dealership and leasing division, and Van Mossel's acquisition of Nord-Ostsee Automobile in Germany. This consolidation wave is being driven by private equity interest in automotive retail and the strategic imperative among large dealer groups to achieve the scale needed to invest in digital infrastructure, AI-driven inventory management, and omnichannel customer experience capabilities.

Digital platforms are fundamentally reshaping how Europeans buy and sell used vehicles. Approximately 16% of European consumers now prefer online channels for used car purchases, and this share is expected to rise materially through the forecast period, with online transactions projected to grow at a CAGR of 16.35% through 2031. Platforms such as AutoScout24, Autohero, and OEM-backed certified pre-owned digital portals are reducing information asymmetry between buyers and sellers. In January 2025, Cinch, owned by Volkswagen Financial Services, partnered with a major insurance provider to offer integrated coverage packages with every used car purchase, further simplifying the end-to-end digital ownership experience.

The Expert Market Research's report titled “Europe Used Car Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Vehicle Type

Key Insight: SUV and MUV models captured approximately 33.78% of the European used car market share in 2025, with consumer appetite for versatile, higher-seating vehicles proving resilient even amid fuel cost pressures. The SUV segment is projected to expand at a CAGR of approximately 9.7%, driven by the increasing volume of BEV-compatible SUVs exiting lease pools and entering the used vehicle market. Hatchbacks continue to hold significant share due to their affordability and fuel efficiency, particularly in urban environments. Sedans maintain relevance in markets such as Germany and France, where they remain popular among corporate and fleet buyers transitioning vehicles into the pre-owned channel.

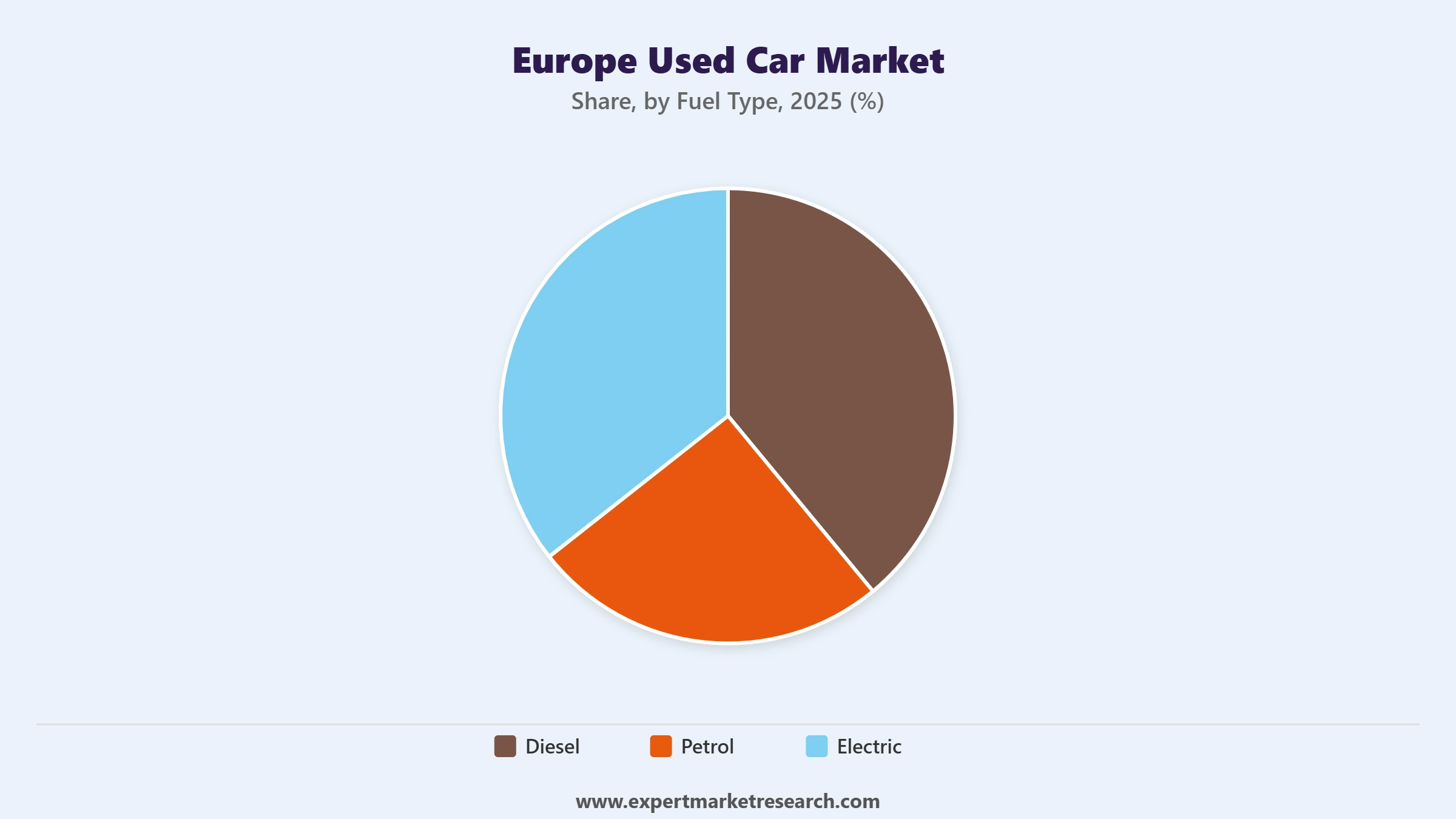

Market Breakup by Fuel Type

Key Insight: Diesel retained approximately 41.52% of the European used car market in 2025, reflecting the large existing stock of diesel-powered vehicles in the European fleet and continued demand from commercial and long-distance drivers. Petrol-powered vehicles account for a further substantial share, with petrol holding approximately 47.6% of the market in 2024 per some estimates. However, the electric vehicle segment is the most transformative, growing at a CAGR of approximately 17.95% through 2031 as early EV adopters cycle their vehicles into the used market. Battery health certification standards being developed at EU level are expected to further underpin buyer confidence in used electric vehicles through the forecast period.

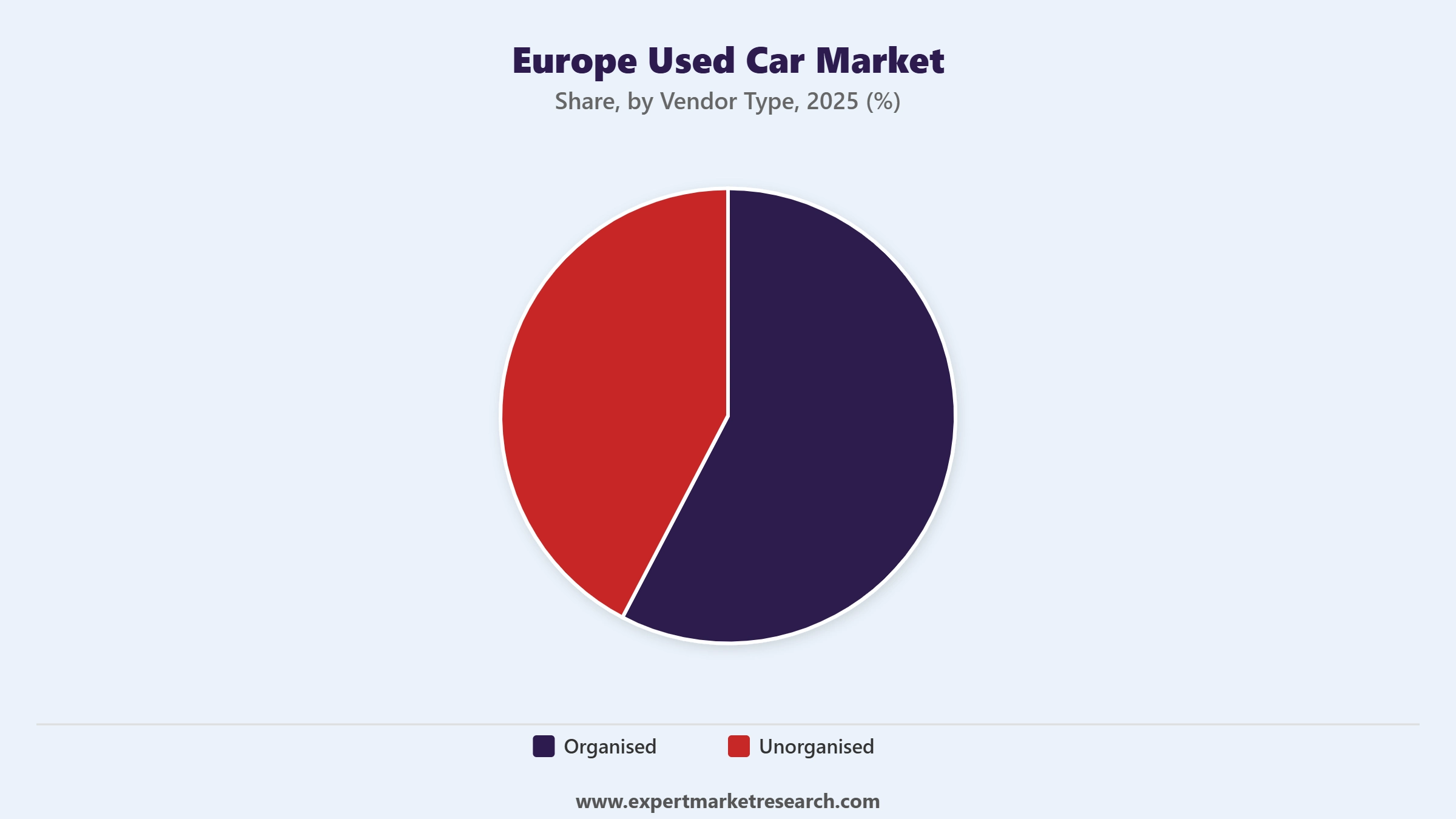

Market Breakup by Vendor Type

Key Insight: Unorganised channels retained approximately 54.60% of the European used car market in 2025, reflecting the continued prevalence of private sales and independent dealers outside formalised retail structures. However, the organised segment is growing at a notably faster pace, with a CAGR of approximately 6.18% projected through 2031. OEM-backed certified pre-owned programs and large dealer group networks are driving this formalisation, offering buyers warranty coverage, multi-point inspections, and integrated financing that private sellers cannot match. Emil Frey AG, Arnold Clark, and Penske Automotive Group represent the organised segment's most prominent players.

Market Breakup by Application

Key Insight: Offline channels accounted for approximately 87.35% of European used car sales in 2025, reflecting persistent consumer preference for physical vehicle inspection before purchase. However, the online segment is the clear growth driver within this segmentation, posting a CAGR of approximately 16.35% through 2031. Digital classifieds, end-to-end transactional marketplaces, and OEM-backed online CPO platforms are collectively driving this shift. Research conducted by industry sources shows approximately 16% of European consumers already prefer online channels for used car purchases, a figure expected to rise materially as digital infrastructure improves and consumer confidence in online transactions grows.

Market Breakup by Country

Key Insight: Germany dominates the European used car market with approximately 21.4% market share, supported by a professional dealership network and robust cross-border vehicle trading infrastructure. The UK's used car market demonstrated strong resilience in 2024, with monthly transaction volumes climbing 9.1% in April. France recorded double-digit used car transaction growth through Q2 2024 and leads European demand for certified sustainable pre-owned vehicles. Italy posted a 9% transaction volume surge in Q2 2024. Spain emerged as one of Europe's fastest-growing markets, with used car demand rising 7.5% in H1 2024, particularly for one-to-three-year-old vehicles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Vehicle Type

SUVs hold the largest and fastest-growing share of the European used car market by vehicle type in 2025, having captured approximately 33.78% of the market. Consumer preferences for elevated seating positions, higher cargo capacity, and all-terrain versatility, combined with the growing volume of used SUVs becoming available as ex-lease stock, are driving this dominance. Hatchbacks maintain their position as a popular choice for budget-conscious urban buyers, particularly in the UK, France, and Spain, where compact models are well-suited to city driving conditions and parking constraints.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Fuel Type

Diesel retains the single largest fuel type share in the European used car market at approximately 41.52% of 2025 volumes, supported by the high proportion of diesel vehicles in the existing European fleet and their continued appeal for commercial and long-distance use. Petrol vehicles account for a significant secondary share. However, the electric vehicle segment is undergoing the most dynamic growth, driven by increasing supply of used EVs from early adopters and government mandates restricting future ICE vehicle sales. Countries such as Norway, Germany, and the Netherlands are leading this transition, supplying the highest volumes of quality used EVs into the secondary market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Vendor Type

While unorganised channels continue to represent the majority of European used car transactions by volume, the organised segment is gaining share at an accelerating rate. Large dealer groups such as Emil Frey AG, Arnold Clark, and Penske Automotive Group are investing heavily in digital capabilities, certified pre-owned programs, and integrated financing to attract buyers who prioritise transparency, warranty cover, and post-sale support. Germany and the UK lead in organised dealer penetration, with professional dealerships accounting for over 56% of used car purchases in Germany in 2021, a figure that has continued to grow since.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Germany

Germany is Europe's largest and most sophisticated used car market, commanding approximately 21.4% of the regional market share and projected to grow at a CAGR of 4.9% through 2035. The country's deep network of professional dealerships, its position as a major vehicle exporter, and the strong digital infrastructure supporting online used car transactions are core strengths. In September 2024, Van Mossel Automotive Group's acquisition of Nord-Ostsee Automobile SE further consolidated the German used car dealer landscape. Germany's role as both a major generator and recipient of cross-border used car flows within the EU positions it as the fulcrum of the continental pre-owned vehicle trade.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

United Kingdom

The United Kingdom remains one of Europe's most active used car markets, with used vehicle transactions in April 2024 surging 9.1% on a monthly basis. Arnold Clark Automobiles, with over 200 UK dealerships and GBP 380 million in EBITDA for 2024, exemplifies the scale of organised retail in the country. The UK market is also at the forefront of digital used car retail innovation, with platforms such as Cazoo and Cinch having invested heavily in end-to-end digital purchase experiences. The ongoing consolidation of UK dealer groups, including the Athenaeum International Holdings acquisition of Johnsons Cars in June 2025, reflects continued investor confidence in the UK used car sector's long-term growth potential.

The Europe used car market features a competitive landscape that is simultaneously fragmented at the local and regional level and increasingly concentrated among large national and pan-European dealer groups. No single player commands a dominant market share, but the top ten dealer groups by turnover collectively represent a growing proportion of organised retail activity. Market competition is centred on certified pre-owned program quality, digital platform investment, financing accessibility, and aftersales service capability.

Emil Frey AG leads the European dealer group rankings by turnover at approximately GBP 15.3 billion, followed by Penske Automotive Group's Sytner and Carshop operations in the UK. Arnold Clark tops the UK profitability rankings. The sector is attracting increasing private equity interest and cross-border M&A activity as investors recognise the structural growth dynamics of the European used car market.

Founded in 1954 and headquartered in Glasgow, Scotland, Arnold Clark Automobiles is one of Europe's largest independent car dealer groups, operating over 200 dealerships across the United Kingdom. The company sells in excess of 300,000 vehicles annually across more than 30 brands and is a major player in both new and used vehicle retail. Arnold Clark topped the Car Dealer Top 100 profitability rankings in 2024 with GBP 380 million in EBITDA. The group's investment in digital retailing systems and its Arnold Clark Charge EV infrastructure initiative position it strongly for the accelerating transition toward electrified used vehicles.

Founded in 1924 and headquartered in Zurich, Switzerland, Emil Frey AG is Europe's largest automotive retailer by turnover, generating approximately GBP 15.3 billion annually. The group operates across France, Germany, the Netherlands, Belgium, and Eastern Europe, with a broad multi-brand used and new vehicle portfolio. Emil Frey deploys centralised data analytics to optimise service bay utilisation and inventory planning, positioning it as a technology leader among European dealer groups. Its scale enables it to maintain certified pre-owned programs across multiple brands, underpinning its competitive position in the organised used car segment.

Founded in 1990 and headquartered in Bloomfield Hills, Michigan, USA, Penske Automotive Group is a global automotive retailer with substantial European operations through its ownership of Sytner and Carshop in the UK. Sytner is the UK's largest premium car retailer, while Carshop operates a multi-brand used car superstore model. In July 2025, Penske completed the acquisition of a Ferrari dealership in Modena, Italy, extending its luxury brand presence in continental Europe. Penske's European operations are at the forefront of digital retailing and certified pre-owned programming, with strong aftersales and financing capabilities.

Headquartered in Manchester, United Kingdom, Lookers Motor Group is one of the UK's largest automotive retail groups, operating a broad network of franchised dealerships across the country. Owned by Global Auto Holdings since its acquisition, Lookers posted GBP 43.7 million in profits in 2024, a significant turnaround from the prior year. The group has expanded its franchise portfolio, adding Cupra and Geely dealerships in 2025, and is investing in digital retailing capabilities and omnichannel customer experience initiatives. Lookers represents multiple brands including premium and volume marques, offering buyers access to a wide range of certified pre-owned vehicles.

Other key players in the market are Auto Empire Trading GmbH, AVAG Holding SE, DAT AUTOHUS AG, Gottfried Schultz Automobilhandels SE, Pendragon Plc, WELLER Holding SE and Co. KG, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Europe's used car market is at an inflection point, shaped by regulatory change, digital disruption, and the growing electrification of the pre-owned vehicle pool. Our comprehensive Europe Used Car Market report for 2035 provides the depth of analysis you need to navigate this transformation, covering country-level demand trends, segment growth dynamics, dealer group competitive positioning, and the emerging role of used EVs in reshaping buyer preferences. Whether you are a dealership group, investor, OEM, or digital platform operator, this report delivers the clarity to make informed decisions. Download your free sample today and start uncovering Europe's pre-owned vehicle opportunities.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 475.17 Billion.

The market is projected to grow at a CAGR of 4.30% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 723.92 Billion by 2035.

The different countries considered in the Europe used car market report include Germany, the United Kingdom, France, and Italy, among others.

The different types of vehicles in the market are hatchbacks, sedans, and SUVs, among others.

The different vehicles based on fuel type include diesel, petrol, and electric, among others.

The different sales channels in the market are online and offline.

Key players in the market are Arnold Clark Automobiles Limited, Auto Empire Trading GmbH, AVAG Holding SE, DAT AUTOHUS AG, Emil Frey AG, Gottfried Schultz Automobilhandels SE, Lookers Motor Group Limited, Pendragon Plc, Penske Automotive Group, and WELLER Holding SE & Co. KG, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Vehicle Type |

|

| Breakup by Fuel Type |

|

| Breakup by Vendor Type |

|

| Breakup by Sales Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.