Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

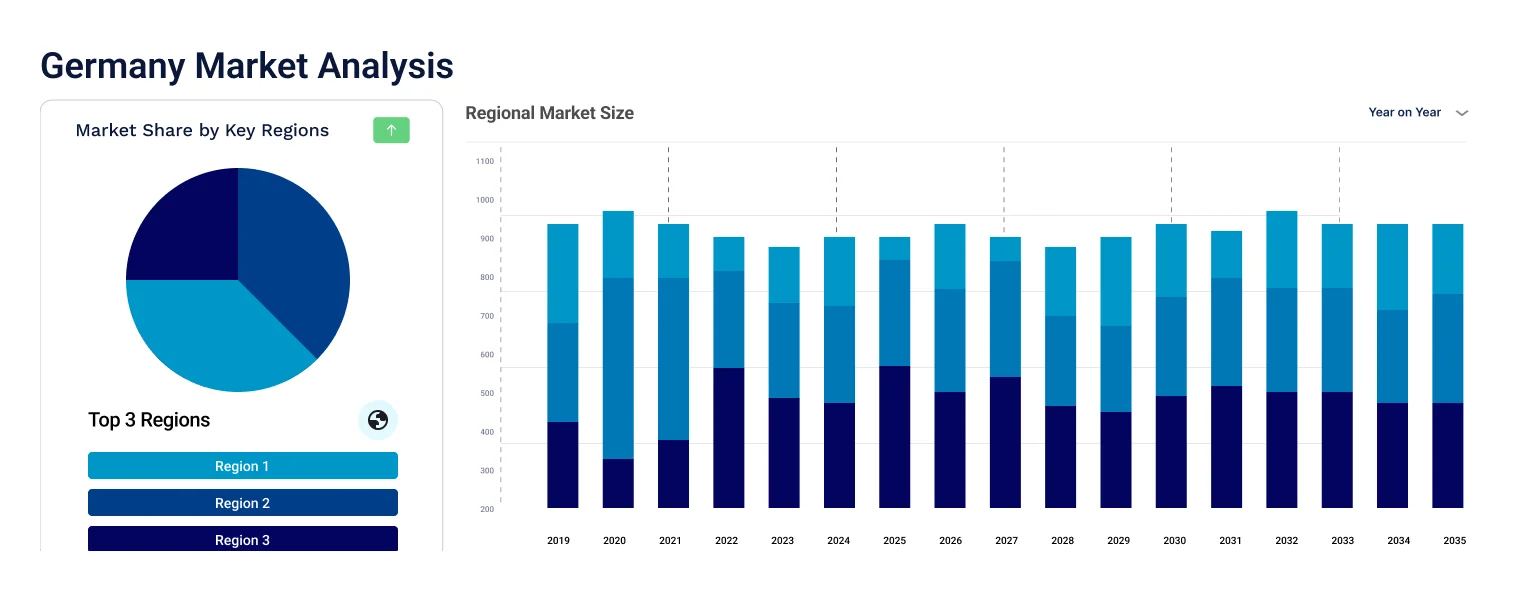

The Germany third-party logistics (3PL) market size was valued at USD 20.18 Billion in 2025. The market is further projected to grow at a CAGR of 3.30% between 2026 and 2035, reaching a value of USD 27.92 Billion by 2035.

Compound Annual Growth Rate

3.3%

Value in USD Billion

2026-2035

Third-party logistics (3PL) is the process of outsourcing some or all the supply chain functions, such as transportation, warehousing, distribution, and fulfillment, to a specialised service provider. The 3PL service providers offer inventory management services, door–to–door delivery, cross-docking, packaging services. The sole focus on shipment and storage activities allows 3PL providers to offer greater scalability, efficient operations, and improved customer experience.

The Germany third-party logistics (3PL) market outlook looks positive due to the increasing demand for e-commerce, the rising need for cost reduction and operational efficiency, the growing adoption of green logistics solutions, and the development of the cold chain sector in the country.

Adoption of automation in logistics, growing focus on sustainability and green logistics, and rising e-commerce sales are driving the Germany third-party logistics (3PL) market growth.

DHL Group introduced hydrogen-powered trucks in Germany as part of its efforts to reduce transport emissions and strengthen its sustainable logistics operations.

DB Schenker rolled out customised logistics solutions at its new contract logistics warehouse in the Czech Republic, integrating advanced automation and robotisation technologies to enhance operational efficiency.

CEVA Logistics deployed 57 Skypod robots across two facilities in Venray, Netherlands, significantly improving warehouse efficiency and enabling the sites to manage up to three times peak-season volumes.

APL Logistics Ltd launched Logistics SuperSuite Plus (LSS+), a next-generation visibility and reporting platform designed to deliver seamless end-to-end integration across the supply chain.

Boosts the need for warehousing in Germany and for distribution services, especially in urban areas and near consumer hubs

Enhances the efficiency, accuracy, and transparency of 3PL services, as well as reduces costs and errors

Encourages the use of alternative fuels, low-emission vehicles, and eco-friendly packaging by 3PL providers, as well as the optimisation of routes and loads

Enables 3PL providers to offer end-to-end solutions that cover all aspects of the supply chain, from sourcing to delivery

Supportive ecosystems, favourable government policies, and healthy regional trade have allowed the exponential growth of new and established manufacturing sectors in Germany. This has created lucrative opportunities for the Germany third-party logistics (3PL) market growth.

The growth of the e-commerce sector is a major factor supporting the demand for third-party logistics in Germany. E-commerce retailers, attempting to provide their customers greater convenience, control, and choice, are rapidly adopting third-party logistics services that are reliable, fast, and cost-effective to enhance customer experience. The utilisation of advanced technologies such as AI, data analytics, and machine learning by service providers is promoting the Germany third-party logistics (3PL) market development. Such technologies allow greater client control over the supply chain and delivery by offering services like tracking, real-time query resolution, and optimisation of delivery time to enhance and streamline logistics services.

Germany Third-Party Logistics (3PL) Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Breakup by Service

Breakup by Transport

Breakup by End Use

Roadways transportations are expected to hold significant market share as they provide better connectivity to domestic regions of the country

According to the Federal Statistical Office of Germany, road transport accounted for 71.2% of the total freight transport in 2019, followed by railways (18.1%), waterways (8.4%), and airways (1.1%). Roadways are expected to hold a significant portion of the Germany third-party logistics (3PL) market share over the forecast period. The growing demand for goods by the domestic regions of Germany increases the demand for roadways as they provide greater connectivity, reliability, and enhanced penetration into remote areas.

Railways are the second-largest mode of 3PL in Germany, offering advantages such as low emissions, high capacity, and safety. Railways are mainly used for transporting bulk goods, such as coal, iron ore, and chemicals. Further, waterways are the third-largest mode of 3PL in Germany, mainly serving the international trade through ports such as Hamburg, Bremen, and Duisburg. Waterways are suitable for transporting large volumes of goods over long distances, such as containers, oil, and gas.

According to Germany third-party logistics (3PL) market report, airways is expected to witness a robust growth due to the increased cross-border trade among European countries. Airways are mainly used for transporting high-value and time-sensitive goods, such as pharmaceuticals, electronics, and perishables. Airways offer fast delivery, security, and global connectivity.

Healthcare sector leads the market due to the increasing demand for specialised logistics services such as cold chain, clinical trials, and biopharma distribution

The manufacturing segment accounts for the largest share of the Germany third-party logistics (3PL) market as it benefits from the outsourcing of logistics services such as transportation, warehousing, distribution, and inventory management, which help reduce costs and improve efficiency. The manufacturing sector in Germany is highly diversified and competitive, with a strong presence of industries such as machinery, chemicals, pharmaceuticals, electronics, and automotive. These industries require reliable and flexible 3PL solutions to cope with the changing market conditions and customer expectations.

The retail segment in third-party logistics (3PL) market in Germany also relies on 3PL providers for timely delivery, order fulfillment, and reverse logistics, especially in the e-commerce sector. The e-commerce industry in Germany is one of the largest and fastest growing in Europe, with a high penetration of online shoppers and a diverse product range. The e-commerce retailers need 3PL partners to handle the complex and dynamic logistics processes, such as order processing, packaging, shipping, tracking, returns, and refunds. The 3PL providers also help the retailers to optimise their logistics network, reduce operational costs, and enhance customer satisfaction.

The healthcare segment of Germany third-party logistics (3PL) market is expected to expand at a faster rate in the coming years due to the growing demand for specialised logistics services such as cold chain, clinical trials, and biopharma distribution. The healthcare sector in Germany is one of the most advanced in the world, with a high expenditure on research and development, large number of patents, and a strong export orientation. The 3PL providers offer customised and value-added services to healthcare clients, such as temperature-controlled transportation and storage, real-time monitoring and tracking, quality assurance, and risk management.

According to the Germany third-party logistics (3PL) market analysis, the automotive sector also utilises 3PL services for the transportation and storage of raw materials, spare parts, and finished vehicles. As Germany is one of the world's largest automotive sectors with superior quality vehicle engineering, German vehicles are extensively exported across the globe. Additionally, increasing investments by vehicle manufacturers aimed at developing electric and hydrogen vehicles are expected to aid the market growth. The 3PL providers support the automotive clients in streamlining their logistics operations, reducing their inventory and transportation costs, improving their delivery performance, and enhancing their customer loyalty.

Market players are committed to changing the world of logistics by introducing new logistics solutions and deploying sustainable fleet, further strengthening their position in the market.

Deutsche Post AG (DHL), founded in 1995 and headquartered in Bonn, Germany, is a leading global logistics provider offering parcel services, express delivery, e-commerce solutions, freight transportation, and end-to-end supply chain management.

Established in 1980 with operations based in Singapore and the United States, APL Logistics Ltd specialises in ocean and air freight forwarding, customs brokerage, contract logistics, distribution management, order fulfilment, and transportation management solutions.

Founded in 2006 and headquartered in Geneva, Switzerland, CEVA Logistics SA provides comprehensive logistics services, including transportation across land, air, and sea routes, along with contract logistics, warehousing, and distribution support.

Nippon Express Co., Ltd. established in 1937 and headquartered in Tokyo, Japan, delivers a wide range of logistics services such as air, ocean, and land transport, warehousing, distribution, customs clearance, heavy haulage, construction logistics, and consulting.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other players included in the Germany third-party logistics 3PL market are Schenker AG, WemoveBW GmbH, GEODIS, and Rhenus Group, among others.

Third-Party Logistics (3PL) Market

Middle East and Africa Third-Party Logistics (3PL) Market

United States Third-Party Logistics (3PL) Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Germany third-party logistics (3PL) market reached an approximate value of USD 20.18 Billion.

The Germany third-party logistics (3PL) market is expected to grow at a CAGR of 3.30% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 27.92 Billion by 2035.

A third-party logistics (3PL) provider offers companies with supply chain management and outsourced logistics services, such as inventory management, order fulfilment, transportation, and warehousing.

The main benefits of using a 3PL include cost savings, improved supply chain efficiency, and the ability to focus on core competencies. Businesses can cut expenses and improve efficiency by contracting out supply chain management and logistics tasks to outside service providers.

The major drivers of the market are the robust growth of the e-commerce sector along with globalisation and liberalisation supporting international trade.

Key trends aiding market expansion include the rising export of vehicles from the country and the incorporation of advanced technologies in third-party logistics.

Based on transport, the market segmentations are roadways, railways, waterways, and airways.

Based on end use, the market is divided into manufacturing, retail, healthcare, and automotive, among others.

Key players in the market are Deutsche Post AG (DHL), Schenker AG, WemoveBW GmbH, APL Logistics Ltd, CEVA Logistics SA, Nippon Express Co., Ltd., GEODIS, and Rhenus Group, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Service |

|

| Breakup by Transport |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.