Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

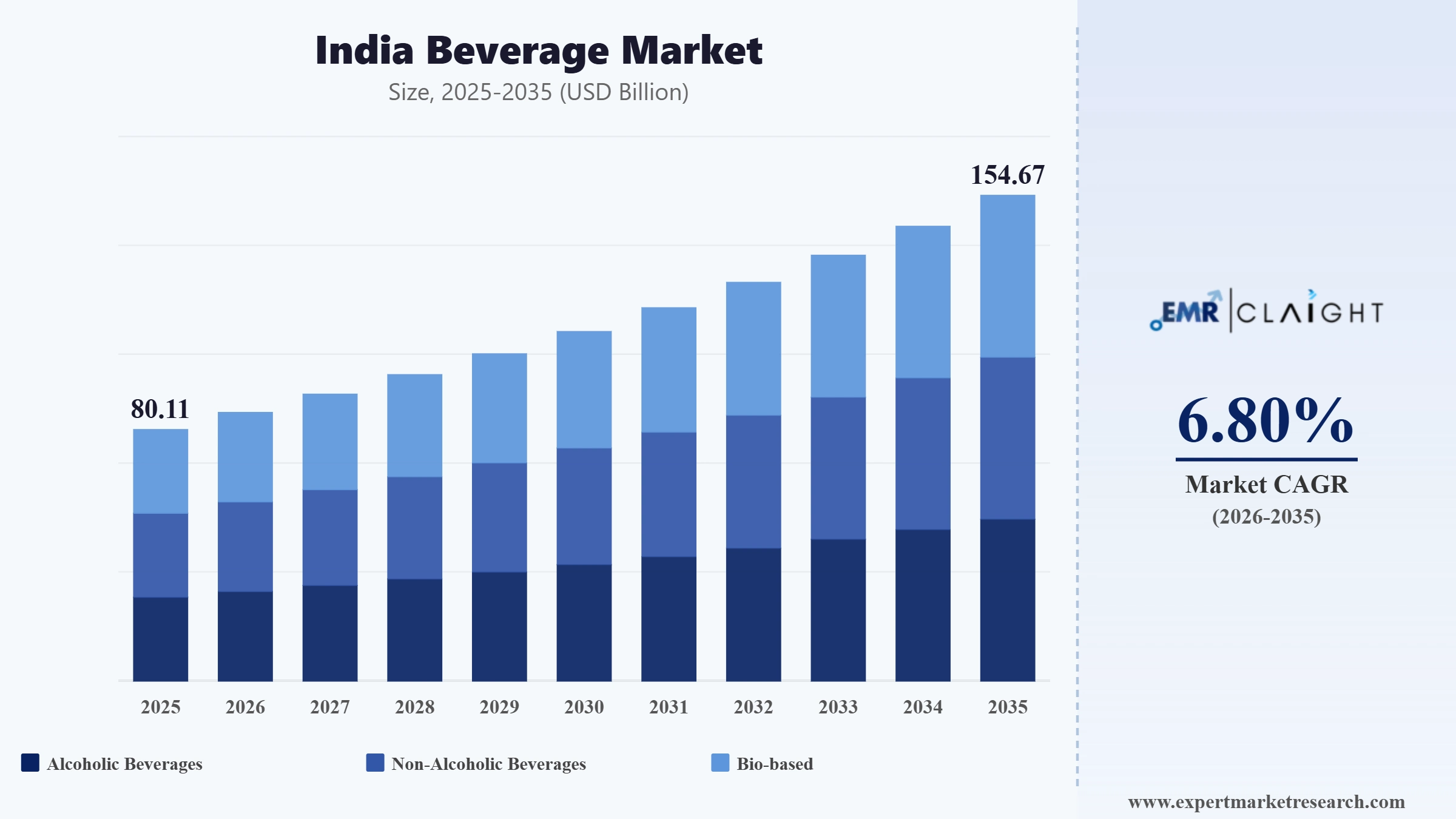

The India Beverage Market reached a value of USD 80.11 Billion at 2025 and is projected to expand at a CAGR of around 6.80% during the forecast period of 2026-2035. With the surging popularity of regional beverage brands, accelerating instant coffee consumption, expanding on-trade channels, and growing consumer appetite for functional, health-focused, and sustainably packaged drinks, the market is expected to reach USD 154.67 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| India Beverage Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 80.11 |

| Market Size 2035 | USD Billion | 154.67 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 6.80% |

| CAGR 2026-2035 - Market by Region | West and Central India | 7.5% |

| CAGR 2026-2035 - Market by Region | East India | 7.1% |

| CAGR 2026-2035 - Market by Product Type | Bio-based | 10.3% |

| CAGR 2026-2035 - Market by Distribution Channel | On-Trade | 7.6% |

| Market Share by Region 2025 | North India | 31.2% |

As per the Agricultural and Processed Food Products Export Development Authority, India is currently the world’s 40th largest exporter of alcoholic beverages. The UAE, Tanzania, Angola, Singapore, the Netherlands, Rwanda, and Kenya are its major export destinations. According to the Confederation of Indian Alcoholic Beverage Companies (CIABC), government support for alcoholic beverage producers is expected to increase the nation’s exports to USD 1 billion in the coming years. In 2023-24, exports amounted to USD 389 million, and the country is aiming for a 14%-15% growth in production annually to meet the burgeoning demand for alcoholic beverages globally. Besides, the Indian government is expected to allow alcoholic beverage producers to produce packaging in flexible sizes, charge minimum charges for labour organisations, provide attractive incentives for participation in international exhibitions and fairs, and reimburse levies imposed on other inputs. Enabling alcoholic beverage producers to obtain timely permissions for branding and bottling of alcoholic beverages is expected to favourably shape the India beverage market dynamics. An increasing number of beverage consumers in India view coffee as a youthful and aspirational drink. It also provides a unique café-like experience at home, which is expected to further propel market growth in upcoming years.

Growing focus on reducing sugar consumption; the emergence of regional brands; increasing consumption of instant coffee; and the shift towards sustainable packaging are the major factors favouring the India beverage market expansion.

In March 2025, both Coca-Cola India and PepsiCo simultaneously launched zero-sugar and no-sugar variants of their flagship brands at an INR 10 price point, marking the first time either company had offered diet or light beverages at this highly competitive entry-level tier in India. Products included Thums Up X Force, Coke Zero, Sprite Zero from Coca-Cola, and Pepsi No-Sugar from PepsiCo, reflecting a concerted industry response to rapidly rising health consciousness among Indian consumers. The launches directly addressed the growing consumer preference for lower-calorie beverages without requiring consumers to pay a premium above the standard carbonated drink price, removing the historical barrier that had limited the reach of diet beverage formats in price-sensitive Indian markets. By introducing health-conscious alternatives at mass-market price points, both companies sought to defend volume share against the encroaching challenge from regional brands and domestically backed challengers while simultaneously repositioning their product ranges for the increasingly health-aware Gen Z and millennial consumer base. The coordinated pricing move also triggered a broader competitive response from emerging players and regional brands across the carbonated segment.

In June 2025, Heineken N.V. announced a landmark investment of INR 2,500 to 3,000 crore to establish its first Asia-Pacific Global Capability Center in Hyderabad, reflecting the company's growing confidence in India as a strategic hub for operational management and business intelligence across its Asia-Pacific operations. The Global Capability Center is designed to consolidate critical functions including supply chain management, data analytics, digital transformation, and market intelligence, strengthening Heineken's ability to manage its India and wider APAC operations with greater efficiency and speed. India has emerged as Heineken's most compelling emerging market for beer, driven by a rapidly urbanising population, a growing legal-drinking-age consumer base of approximately 15 to 20 million new entrants annually, and increasing premiumisation of alcoholic beverage choices among younger Indians. Heineken's India operations span multiple brewery partnerships including its strategic stake in United Breweries, and the Hyderabad investment signals a long-term structural commitment to India rather than an opportunistic play. The center positions Heineken to compete more effectively in one of the world's most strategically important long-term beer growth markets as on-trade expansion accelerates through the forecast period.

In January 2025, Reliance Consumer Products Limited launched RasKik Gluco Energy, a mass-market rehydration drink priced at INR 10, combining electrolytes, glucose, and real lemon juice in a convenient single-serve format. The launch followed the highly successful revival of Campa Cola and represented Reliance's deliberate strategy of targeting price-sensitive Indian consumers in Tier-II, Tier-III, and rural markets through high-volume, low-cost beverage offerings distributed via its extensive Reliance Retail network. The RasKik Gluco Energy product targets active individuals and working consumers seeking practical, affordable hydration solutions, positioning itself against established players in the functional hydration sub-segment. This launch underscores the intensifying competitive pressure on multinational beverage companies in India, where domestic and conglomerate-backed challengers are leveraging broad distribution networks and aggressive pricing to capture market share in the accessible price tier. Reliance's entry into the functional hydration space signals a further broadening of competition within India's non-alcoholic beverage category and its growing ambition to build a multi-product beverage portfolio that competes across both value and functional drink segments simultaneously.

In February 2025, Nestle announced its plans to launch Starbucks-branded ready-to-drink coffee in India, building on its long-standing global licensing partnership with Starbucks. The move directly targets the rapidly expanding premium coffee consumer base in urban India, where rising disposable incomes, lifestyle changes, and growing familiarity with international coffee culture have driven extraordinary demand for convenient, on-the-go coffee formats. India's urban coffee market has been one of the fastest-evolving segments within the broader non-alcoholic beverage space, with Starbucks Corporation itself having announced plans to open 1,000 additional stores across the country under its long-term India expansion strategy by 2028. Nestle's RTD entry complements this trajectory by bringing premium branded coffee into the off-trade channel, enabling wider household penetration beyond coffee chain outlets. The launch reflects Nestle's strategy of deepening its India beverage portfolio well beyond its legacy Nescafe instant coffee position, targeting both modern trade and e-commerce channels for distribution and capturing the growing cohort of urban Indians who want barista-quality coffee experiences at home.

In January 2024, Epigamia launched what is widely regarded as India's first ready-to-drink protein milkshake range offering 25 grams of protein per serving, with zero added sugar, zero fat, and zero preservatives. Available in Vanilla Caramel and Cookies and Cream variants in a 250ml format under the Turbo product line, the launch directly addressed the growing demand among fitness-conscious Indian consumers for high-protein, convenient nutrition options suited to pre- or post-workout consumption. The product positioned Epigamia at the forefront of India's emerging functional beverage space, where protein drinks, probiotic beverages, and immunity-boosting formulations have been gaining rapid traction among urban millennials and Gen Z consumers. The range also benefited from the rapid expansion of quick commerce infrastructure across Indian metros, which has significantly reduced the last-mile delivery window for perishable and refrigerated RTD beverages and effectively expanded the accessible market for premium functional drinks beyond traditional cold chain retail. Epigamia's launch reflected a broader industry trend of blurring the traditional boundaries between food, nutrition, and beverage products as Indian consumers increasingly seek drinks that function simultaneously as refreshment and daily nutritional supplementation.

One of the most consequential shifts reshaping the India beverage market is the rapid ascent of regional brands that are challenging the decades-long dominance of global multinationals in carbonated soft drinks and of national FMCG conglomerates across other beverage categories. During summer 2024, brands including Dailee from Tamil Nadu, Lahori from Punjab, Davat from Gujarat, and Mala Fruit Products from Maharashtra posted extraordinary demand growth, with Dailee alone recording a 2x sales volume increase within its target consumer base. These brands have succeeded by combining deep regional flavour knowledge, competitive pricing structures, and effective last-mile distribution in Tier-II, Tier-III, and rural markets where multinational distribution networks remain comparatively thin. The Reliance-backed revival of Campa Cola amplified this dynamic further, with regional and challenger brands collectively capturing approximately 15% of the carbonated beverage market from Coca-Cola and PepsiCo by early 2025, a structural disruption that analysts are drawing comparisons to the Jio moment in Indian telecommunications. This ongoing shift is forcing established players to accelerate distribution penetration, sharpen pricing strategies, and intensify regional marketing investment to protect volume share through the forecast period.

India's consumer relationship with coffee is evolving at a pace that is surprising even experienced beverage market observers. While India has historically been a tea-dominant market, rapid urbanisation, rising disposable incomes, and strong exposure to global coffee culture through international chains and social media are collectively driving swift adoption of instant coffee and ready-to-drink coffee products among younger consumers. Expert Market Research explicitly identifies increasing instant coffee consumption as one of the three major trends shaping the India Beverage Market during the forecast period. Starbucks Corporation's plan to expand its India retail footprint to 1,000 stores by 2028, and Nestle's February 2025 announcement of Starbucks-branded RTD coffee entering the India off-trade channel, both illustrate how global players are aggressively positioning for this structural shift. The trend is most pronounced in urban centres including Bengaluru, Mumbai, Hyderabad, and Pune, but it is spreading to Tier-II cities with notable speed. For beverage companies, the instant and RTD coffee opportunity is particularly attractive because premium pricing is far more accepted by Indian consumers in this category than in the intensely competitive carbonated drinks segment, offering meaningfully higher margin profiles alongside strong volume growth potential.

Sustainability in beverage packaging has rapidly moved from a voluntary brand aspiration to a hard commercial and regulatory requirement across the India beverage industry. The Indian government's Plastic Waste Management Rules amendments, effective June 2025, mandate that beverage manufacturers ensure a minimum of 30% of their plastic packaging is derived from recycled materials. Tetra Pak responded in February 2025 by announcing it would integrate 5% certified recycled polymers into its cartons for the Indian market from April 2025, sourcing these materials locally from its Pune manufacturing facility. Coca-Cola India, working with bottling partners SLMG Beverages and Moon Beverages, launched 100% recycled PET packaging bottles for its carbonated beverage range in 250ml and 750ml formats, featuring a "Recycle Me Again" consumer call-to-action message. These initiatives reflect both regulatory compliance obligations and a strategic brand-building response to the fact that younger Indian consumers are placing increasing weight on the environmental credentials of the brands they choose. Companies that invest ahead of regulatory timelines are also building procurement advantages in recycled material supply chains that slower-moving competitors will find difficult to replicate, making sustainability investment a source of genuine competitive differentiation in the India beverage market through the forecast period.

Indian consumers, particularly in urban and semi-urban markets, are increasingly demanding beverages that deliver meaningful benefits beyond basic thirst quenching. The functional beverage segment, encompassing protein drinks, probiotic beverages, energy drinks, immunity-boosting formulations, and plant-based hydration products, has emerged as one of the fastest-growing sub-categories within India's broader beverage market. India's functional drinks market generated approximately USD 3.79 billion in revenue in 2024 and is projected to reach USD 7.36 billion by 2030, representing a CAGR of 11.7%. Brands including Epigamia, Raw Pressery, and Storia Foods have built loyal urban consumer bases by offering clean-label, protein-rich, and minimally processed drink options that align strongly with rising health consciousness. The rapid expansion of quick commerce platforms has further accelerated functional beverage adoption by dramatically reducing the friction associated with purchasing refrigerated and premium-priced health drinks. Larger corporations including Hindustan Coca-Cola Beverages have responded by investing in health-focused and plant-based product development, incorporating local functional ingredients such as ginger, turmeric, and mint to resonate with Indian wellness preferences while maintaining broad consumer appeal. This intersection of global functional drink trends with Indian ingredient heritage is creating a distinctive and fast-evolving category within the India beverage market.

Shift towards sustainable packaging

Sustainable packaging is playing a significant role in the growth of the market by aligning with growing consumer demand for environmentally responsible products. As consumer awareness of various environmental issues increases, they are seeking recyclable, biodegradable, or reusable packaging solutions for beverages. This has prompted companies to switch to paper-based cartons, plant-based plastics, and glass bottles, among other eco-friendly packaging solutions, to reduce waste and attract eco-conscious buyers. This has built consumer trust in different brands and is driving younger generations towards more environmentally responsible brands, hence creating a favourable India beverage market outlook.

Rise of regional brands

Growing incidences of heatwaves and rising temperature levels in the country have prompted beverage companies to introduce innovative flavours. Between March and May 2024, the penetration rate of regional beverage brands across India rose to 7%, a year-on-year surge from 5% in 2023. Based on market analysis, the consumer reach of regional beverage brands in urban and rural areas increased to 10% and 5.3% respectively, thereby facilitating the India beverage market development. For instance, the demand for Dailee, a regional beverage brand of Tamil Nadu, witnessed a 2x growth among consumers in 2024.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research's report titled “India Beverage Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Breakup by Product Type

Breakup by Distribution Channel

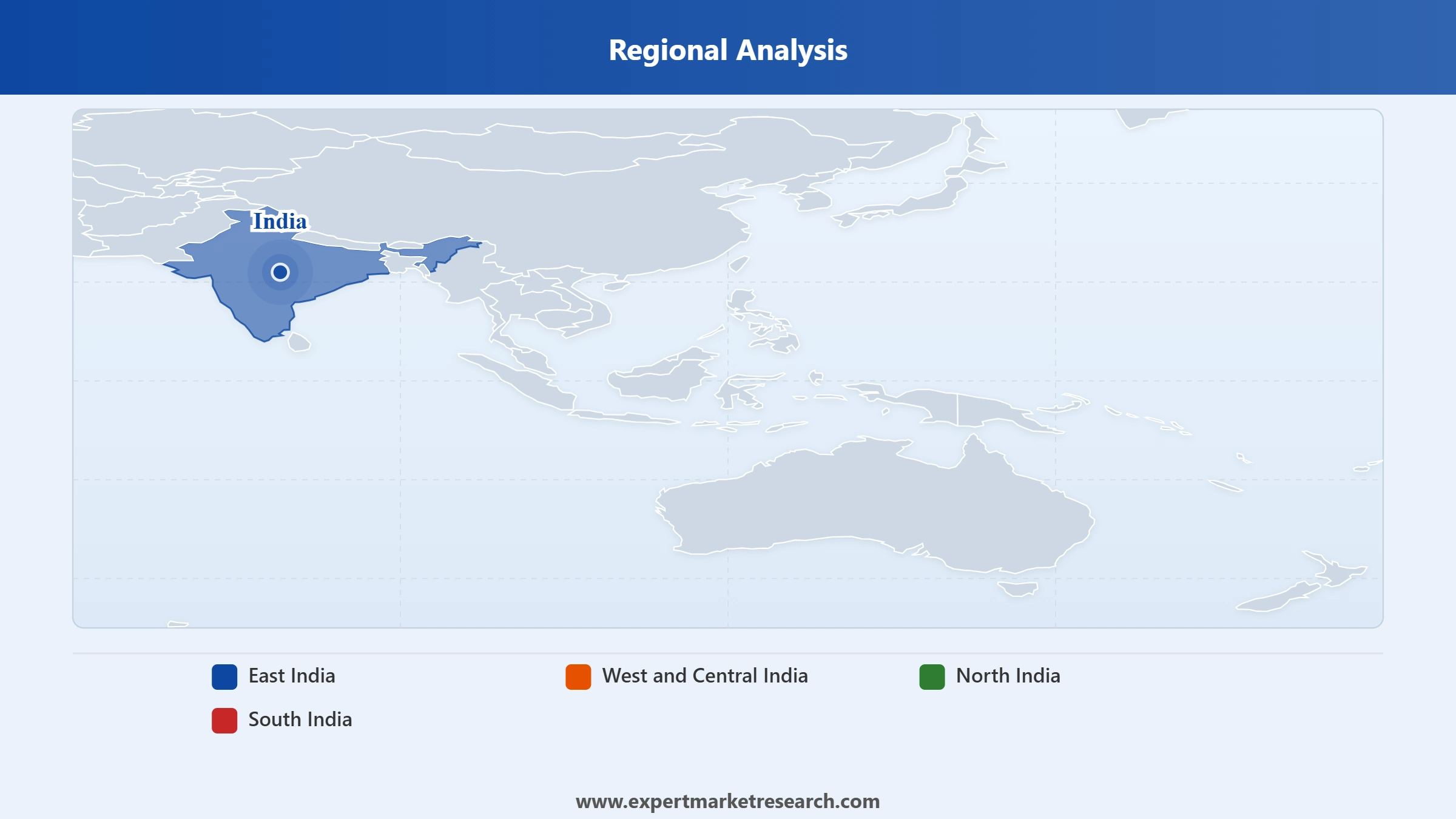

Breakup by Region

Based on region, the market is segmented into East India, West and Central India, North India, and South India. Over the forecast period of 2026-2035, the market for beverages in West and Central India is expected to grow at a CAGR of 7.5% due to the growth of regional beverage brands. East India is expected to grow at a CAGR of 7.1% between 2026 and 2035 due to the rising consumption of ready-to-drink tea and coffee products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

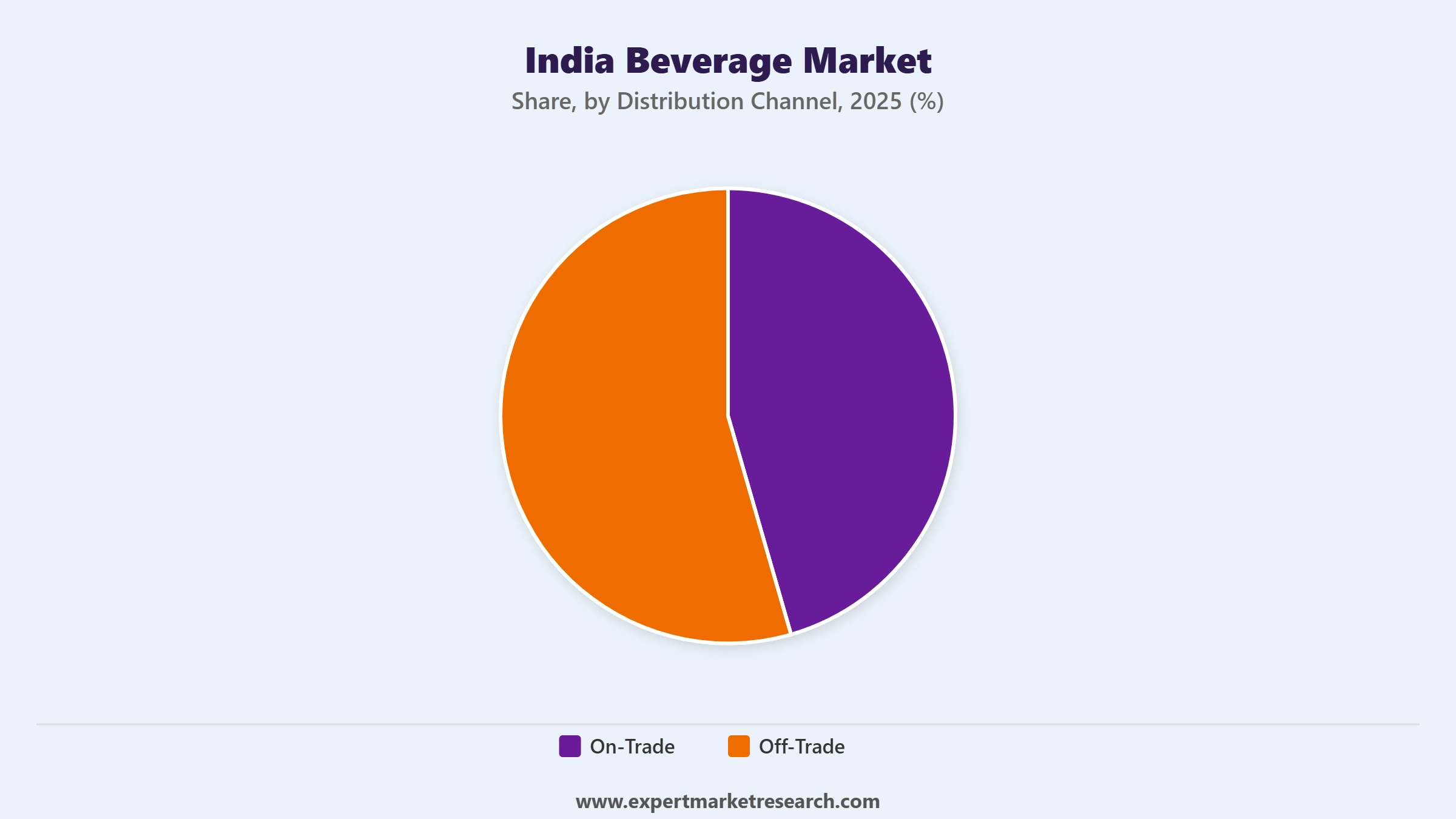

Based on distribution channel, the market is categorised into on-trade and off-trade. The India beverage market analysis suggests that on-trade consumption is expected to grow at a CAGR of 7.6% between 2026 and 2035 due to the rising consumption of alcoholic beverages, while off-trade consumption is expected to grow steadily with the shift towards home-entertainment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India beverage market is characterised by intense competition among global multinationals, large domestic conglomerates, and a rapidly expanding cohort of regional challengers. Leading players are deploying strategies centred on pricing innovation, distribution expansion into Tier-II and Tier-III cities, product diversification into functional and health-focused categories, and sustainability-led packaging upgrades. Regional brands have meaningfully disrupted market share dynamics in the carbonated segment, while the on-trade alcoholic beverage channel continues to attract substantial investment from global spirits and beer companies that view India as one of the world's most important long-term growth markets for premium alcoholic beverages.

Nestle S.A. is a Swiss multinational food and beverage corporation headquartered in Vevey, Switzerland, operating in more than 190 countries. In India, Nestle operates through Nestle India Limited and commands one of the strongest beverage portfolios in the country, anchored by the Nescafe instant coffee brand, Milo nutritional drinks, and the Milkmaid dairy-based beverage range. The company has pioneered the India ready-to-drink and instant beverage space through decades of deep retail penetration and brand investment. In February 2025, Nestle announced plans to extend its global licensing partnership with Starbucks into India's RTD coffee segment, signalling a clear ambition to capture the rapidly expanding premium coffee market beyond its traditional instant coffee leadership. Nestle India also committed an investment of INR 4,200 crore to enhance manufacturing capacity, including the establishment of a new production facility in Odisha, reflecting the company's structural commitment to scaling India operations in line with rising consumer demand across both urban and rural beverage categories.

PepsiCo Inc. is an American multinational food, snack, and beverage corporation headquartered in Purchase, New York, and one of the largest beverage companies operating in India. Through its India operations, PepsiCo markets a broad and well-recognised portfolio spanning Pepsi, Mirinda, 7UP, Mountain Dew, Sting energy drink, Tropicana juice, and Gatorade sports beverages, alongside its leading snacks range. The company operates through a franchise bottling model and has invested significantly in expanding distribution reach into Tier-II and Tier-III cities to defend volume share against the growing challenge from regional brands and domestic competitors. In March 2025, PepsiCo launched zero-sugar variants of its flagship carbonated brands at the INR 10 price point alongside Coca-Cola, a strategic move to address rising health consciousness without abandoning the mass market. PepsiCo has been investing in supply chain management enhancements and strategic distribution partnerships to strengthen India beverage market revenue, while its local management teams leverage deep regional consumer knowledge to navigate India's exceptionally diverse taste preferences across geographies.

The Coca-Cola Company is an American multinational beverage corporation headquartered in Atlanta, Georgia, and among the most widely distributed beverage brands in India through Hindustan Coca-Cola Beverages and its bottling partner network. Coca-Cola's India portfolio spans carbonated beverages including Coca-Cola, Thums Up, Limca, Sprite, Fanta, and Maaza, alongside Kinley packaged drinking water and the Honest Tea ready-to-drink range. The company operates approximately 4 to 5 million retail touchpoints across India and has prioritised brand building and volume expansion over premium pricing strategy since the post-pandemic recovery. In collaboration with bottling partners SLMG Beverages and Moon Beverages, Coca-Cola India launched 100% recycled PET packaging bottles for its carbonated beverage range with a "Recycle Me Again" consumer message, advancing its sustainability agenda. In March 2025, Coca-Cola simultaneously introduced Thums Up X Force and Coke Zero at the INR 10 price point alongside PepsiCo, reflecting the competitive intensity of Indian carbonated beverages and the shared imperative to introduce health-oriented options at accessible price levels for India's mass consumer base.

Heineken N.V. is a Dutch multinational brewing corporation headquartered in Amsterdam, Netherlands, and one of the world's largest beer producers with a strategically important and expanding presence in India. Heineken operates in India principally through its stake in United Breweries, the company behind the iconic Kingfisher beer brand, which commands the largest share of the Indian beer market. In June 2025, Heineken announced a major investment of INR 2,500 to 3,000 crore to establish its first Asia-Pacific Global Capability Center in Hyderabad, consolidating supply chain management, digital transformation, data analytics, and regional intelligence functions across its APAC operations. The investment reflects Heineken's conviction that India will be a central growth driver within its global portfolio, consistent with market projections showing Indian total beverage alcohol volumes growing at an 8% CAGR between 2024 and 2029. The company continues to invest in brewery capacity expansion, premiumisation strategies, and on-trade channel development to capture the growing urban middle-class consumer base that is driving demand for international and premium beer formats across India's expanding foodservice and hospitality landscape.

Other Key Players Red Bull GmbH, Diageo plc, Anheuser-Busch N.V., Suntory Holdings Limited, Reliance Retail Limited, Prime Hydration LLC.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 80.11 Billion.

The market is projected to grow at a CAGR of 6.80% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 154.67 Billion by 2035.

The different regions considered in the market report include East India, West and Central India, North India, and South India.

The different types of products include alcoholic beverages, non-alcoholic beverages, and bio-based beverages.

The different distribution channels are on-trade and off-trade.

The major market trends include the emergence of regional brands, increasing consumption of instant coffee, and the shift towards sustainable packaging.

Key players in the market are Nestle S.A., Pepsico Inc., The Coca-Cola Company, Heineken N.V., Red Bull GmbH, Diageo plc, Anheuser-Busch N.V., Suntory Holdings Limited, Reliance Retail Limited, and Prime Hydration LLC, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.