Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

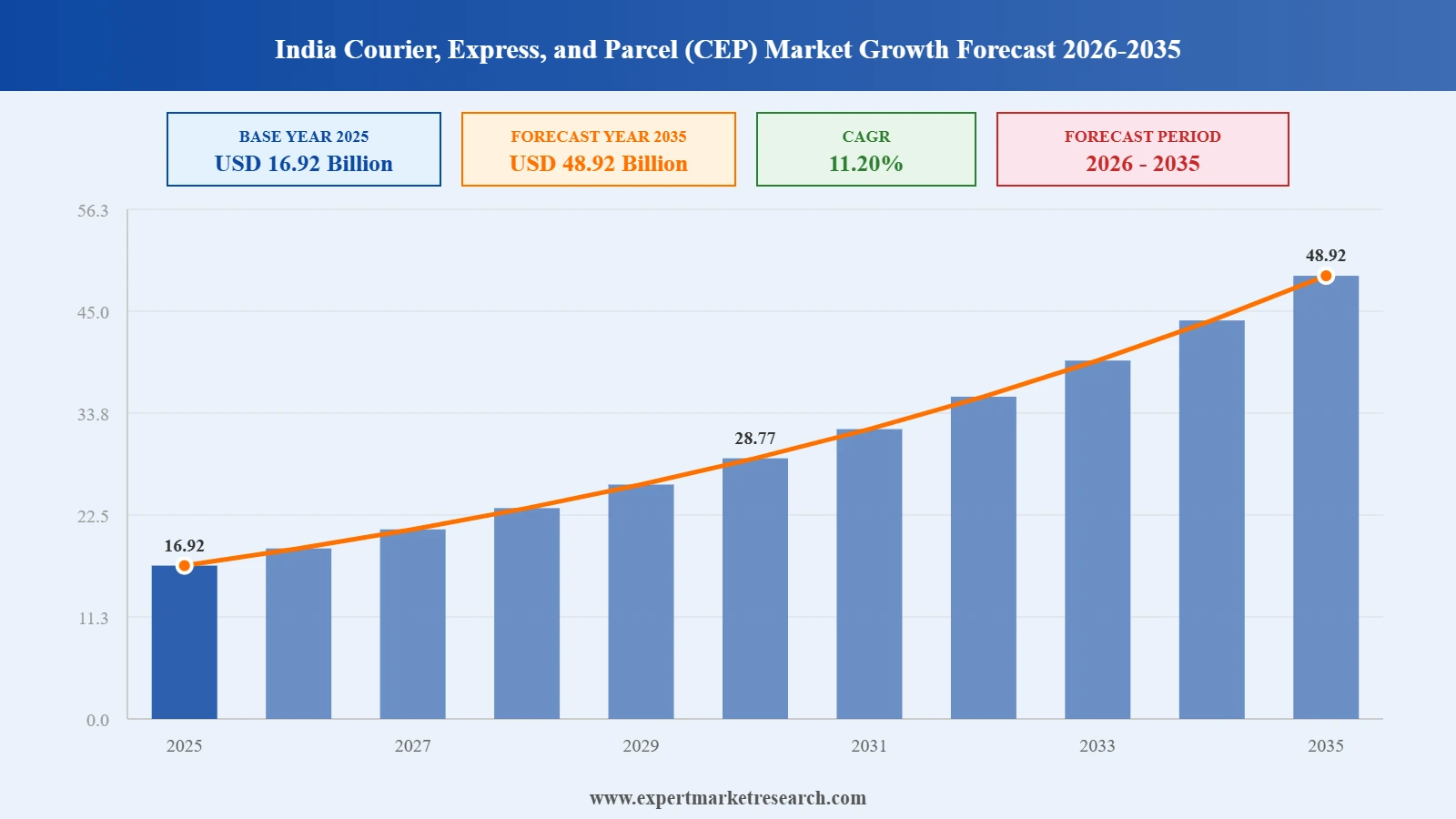

The India Courier, Express, and Parcel (CEP) Market reached a value of USD 16.92 Billion at 2025 and is projected to expand at a CAGR of around 11.20% during the forecast period of 2026-2035. With rapid e-commerce sector growth, the government's PM Gati Shakti logistics modernization program, growing consumer preference for same-day and quick commerce delivery, increasing electric vehicle adoption in last-mile operations, and expanding multimodal transport infrastructure across India, the market is expected to reach USD 48.92 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Courier, Express, and Parcel (CEP) Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

16.92 |

|

Market Size 2035 |

USD Billion |

48.92 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

11.20% |

|

CAGR 2026-2035 - Market by Region |

West India |

12.8% |

|

CAGR 2026-2035 - Market by Region |

East Indi |

11.9% |

|

CAGR 2026-2035 - Market by Business |

B2C (Business-to-Consumer) |

13.1% |

|

CAGR 2026-2035 - Market by End Users |

Life Sciences / Healthcare |

13.2% |

|

2025 Market Share by Region |

West India |

29.4% |

The India CEP market is undergoing structural transformation driven by e-commerce-led volume growth, quick commerce demands compressing delivery windows, government logistics reforms, EV adoption, and sector consolidation as major players strengthen network coverage and technology capabilities.

In April 2025, Delhivery agreed to acquire Ecom Express for INR 1,400 crore (approximately USD 168 million), one of the largest consolidation moves in India's CEP sector in recent years. The acquisition is designed to deepen Delhivery's last-mile delivery reach and unify technology stacks across the two companies' logistics networks. Ecom Express, a major player in e-commerce parcel delivery, brings an additional network of delivery hubs, pin code coverage, and operational infrastructure that complements Delhivery's existing nationwide footprint. By Q3 FY2026, the Ecom Express integration was nearing completion, with Delhivery reporting express parcel shipment volumes surging 43% year-on-year to 295 million units, illustrating the scale benefits of the combined operation.

In April 2025, Ola Electric introduced HyperDelivery, a first-of-its-kind service offering same-day vehicle registration and delivery to customers. The service demonstrates how electric vehicle manufacturers in India are integrating logistics solutions directly into their consumer experience, bypassing traditional dealership models to deliver registered vehicles within 24 hours of purchase. While specific to the automotive category, the launch illustrates the broader trend of sector-specific express delivery innovations reshaping what Indian consumers expect from same-day service timelines, and it signals the growing overlap between electric mobility adoption and express last-mile logistics infrastructure in India's CEP market.

In February 2025, DTDC Express opened its first dark store in Bengaluru specifically designed to support 2-to-4-hour rapid commerce delivery for direct-to-consumer merchants. The facility represents a strategic pivot for DTDC from traditional hub-and-spoke logistics toward micro-fulfillment models that position inventory closer to demand clusters. The dark store enables same-day fulfillment by maintaining product inventory within approximately 3 kilometers of dense urban consumer zones, reducing the last-mile transit time significantly. The launch reflects the broader transformation underway in India's CEP market, where quick commerce platforms demanding sub-4-hour delivery windows are compelling established courier operators to develop new operational models beyond their traditional transport roles.

In January 2025, Blue Dart Express commissioned a 250,000 square-foot automated sorting hub in Delhi, significantly expanding its northern India processing capacity and reducing parcel sorting times. The facility uses advanced automation technology including conveyor-based sorting systems designed to handle higher parcel volumes with greater accuracy and faster throughput. The investment reflects Blue Dart's strategy of strengthening its premium express delivery capabilities as consumer expectations for reliable, time-definite delivery continue to rise across India's growing e-commerce and B2B sectors. North India, anchored by the National Capital Region, represents one of the highest-volume parcel origin and destination markets in the country, making Delhi hub capacity a strategic priority for major CEP operators.

In December 2024, the Asian Development Bank approved a USD 350 million policy-based loan to support the Indian Government's comprehensive reforms for strengthening and modernizing India's logistics sector. The loan is tied to policy conditions aligned with the National Logistics Policy and PM Gati Shakti initiative, targeting reductions in India's logistics costs as a share of GDP and improvements in multimodal freight connectivity. India's logistics costs as a percentage of GDP have already declined from approximately 16% to around 10%, but the country still trails global benchmarks. ADB's financing provides both capital and credibility to reforms that directly benefit the CEP sector by improving road, rail, and air freight infrastructure and reducing documentation-related delays at freight checkpoints.

India's CEP market is undergoing meaningful consolidation as major players pursue acquisitions to extend network reach, achieve technology synergies, and build the scale required to compete profitably in an increasingly cost-competitive market. Delhivery's USD 168 million acquisition of Ecom Express in April 2025 is the most prominent recent example of this trend, bringing together two significant e-commerce parcel delivery networks under a unified brand and technology stack. Delhivery's Q3 FY2026 results showed express parcel volumes rising 43% year-on-year following the integration, demonstrating how strategic consolidation can unlock rapid volume gains. The India CEP market growth trajectory depends heavily on how effectively the emerging tier of large, technology-enabled national networks can consolidate the fragmented mid-market and serve the rising expectations of e-commerce and quick commerce clients.

Quick commerce platforms demanding delivery windows of 10 to 30 minutes have fundamentally altered the operational model requirements for last-mile logistics providers in India's metropolitan markets. Rather than managing purely transport-based delivery from central hubs, CEP players are now establishing dark stores, micro-warehouses, and fulfillment nodes within dense urban zones to position inventory close enough to consumers for ultra-fast delivery. In February 2025, DTDC opened its first dark store in Bengaluru to support 2-to-4-hour fulfillment for D2C merchants, signaling that even established traditional courier operators are adapting their models for the quick commerce era. Quick commerce platforms now collectively operate in 92 non-metro cities, extending ultra-fast delivery beyond metro markets and creating new infrastructure demands across India's CEP sector.

India's leading CEP operators are investing heavily in automated sorting facilities, AI-driven route optimization, and IoT-enabled tracking infrastructure to improve delivery reliability, reduce per-shipment costs, and handle surging parcel volumes generated by e-commerce growth. Blue Dart's commissioning of a 250,000 square-foot automated hub in Delhi in January 2025 is a clear indicator of the capital commitment required to compete in the premium express delivery segment. AI-based demand forecasting helps operators pre-position vehicles and sorting capacity ahead of demand spikes, while real-time tracking capabilities have become a consumer expectation rather than a premium feature. Technology investment is also reducing logistics costs as a share of GDP, which has declined from approximately 16% to around 10%, according to industry data, though meaningful further reduction remains achievable.

The Indian government's sustained investment in logistics infrastructure under PM Gati Shakti and the National Logistics Policy is creating durable long-term tailwinds for the CEP market. The PM Gati Shakti digital platform integrates 16 ministries to streamline multimodal freight movement, cutting transit times and reducing documentation delays. Dedicated freight corridors have reduced the Delhi-Mumbai road haul time by up to 40%, directly improving asset utilization and delivery timelines for express operators. In December 2024, the Asian Development Bank approved a USD 350 million policy-based loan for India's logistics modernization, adding multilateral financial support to domestic policy ambitions. These structural improvements in logistics infrastructure are expanding the addressable market for CEP operators by making express delivery economically viable in geographies previously inaccessible due to poor connectivity.

The Expert Market Research's report titled "India Courier, Express, and Parcel (CEP) Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

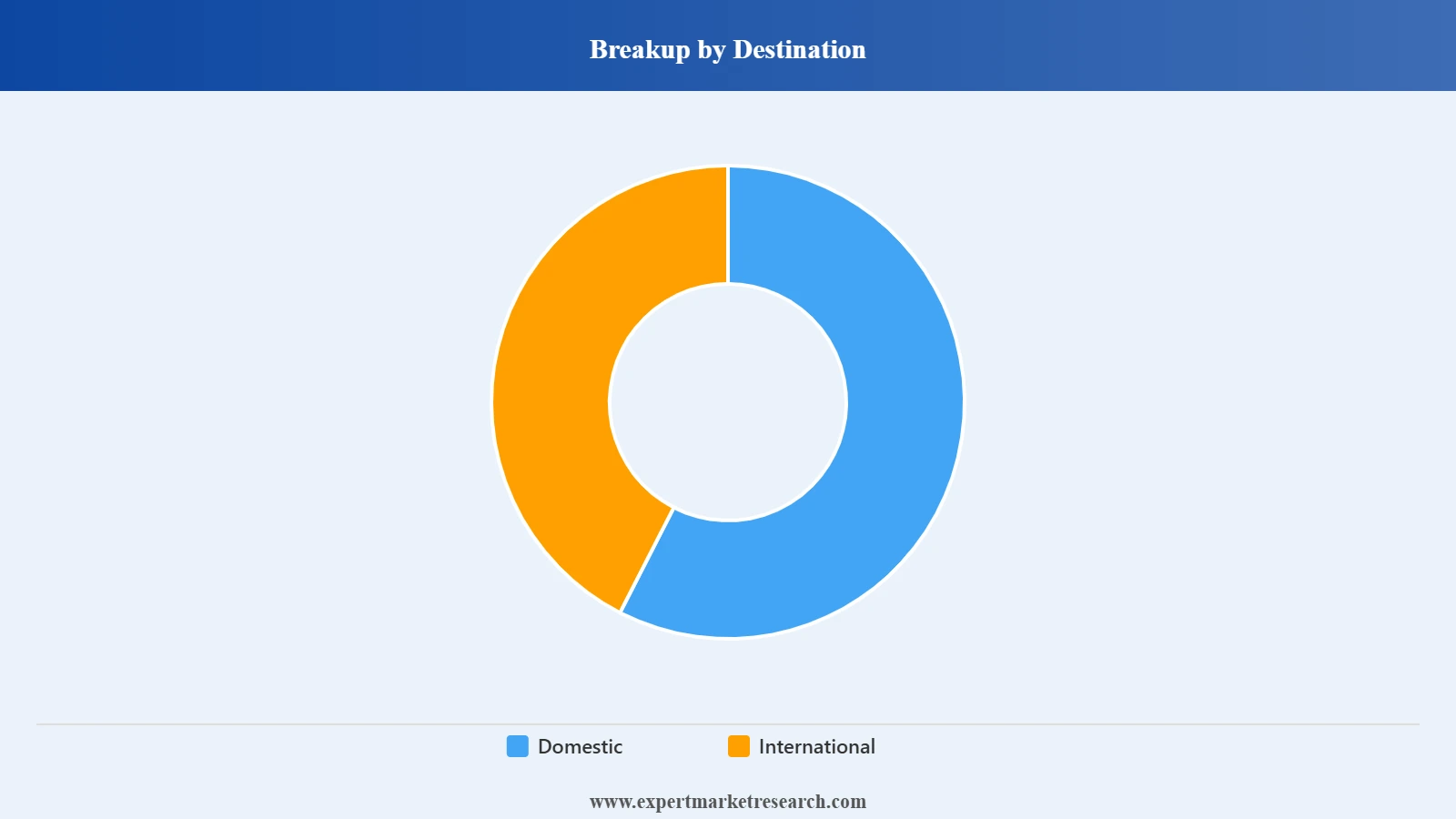

Market Breakup by Destination

Key Insight: Domestic parcels dominate the India CEP market by destination, accounting for approximately 59% of total market revenue in 2025. The segment's leadership is rooted in India's rapidly expanding domestic e-commerce market, which generates massive parcel volumes across B2C and B2B channels. Tier-2 and tier-3 cities now contribute more than 60% of new online shoppers, driving parcel density beyond major metropolitan centers. International shipments, while smaller in absolute share, represent the faster-growing segment at a CAGR of approximately 11.8% over the forecast period, fueled by MSME exports tripling to INR 12.39 lakh crore (USD 149.3 billion) in FY2024-25 after ONDC provided small sellers with digital storefronts and simplified customs processing. Free Trade Agreements are further expanding India's cross-border commerce corridors with key partner nations.

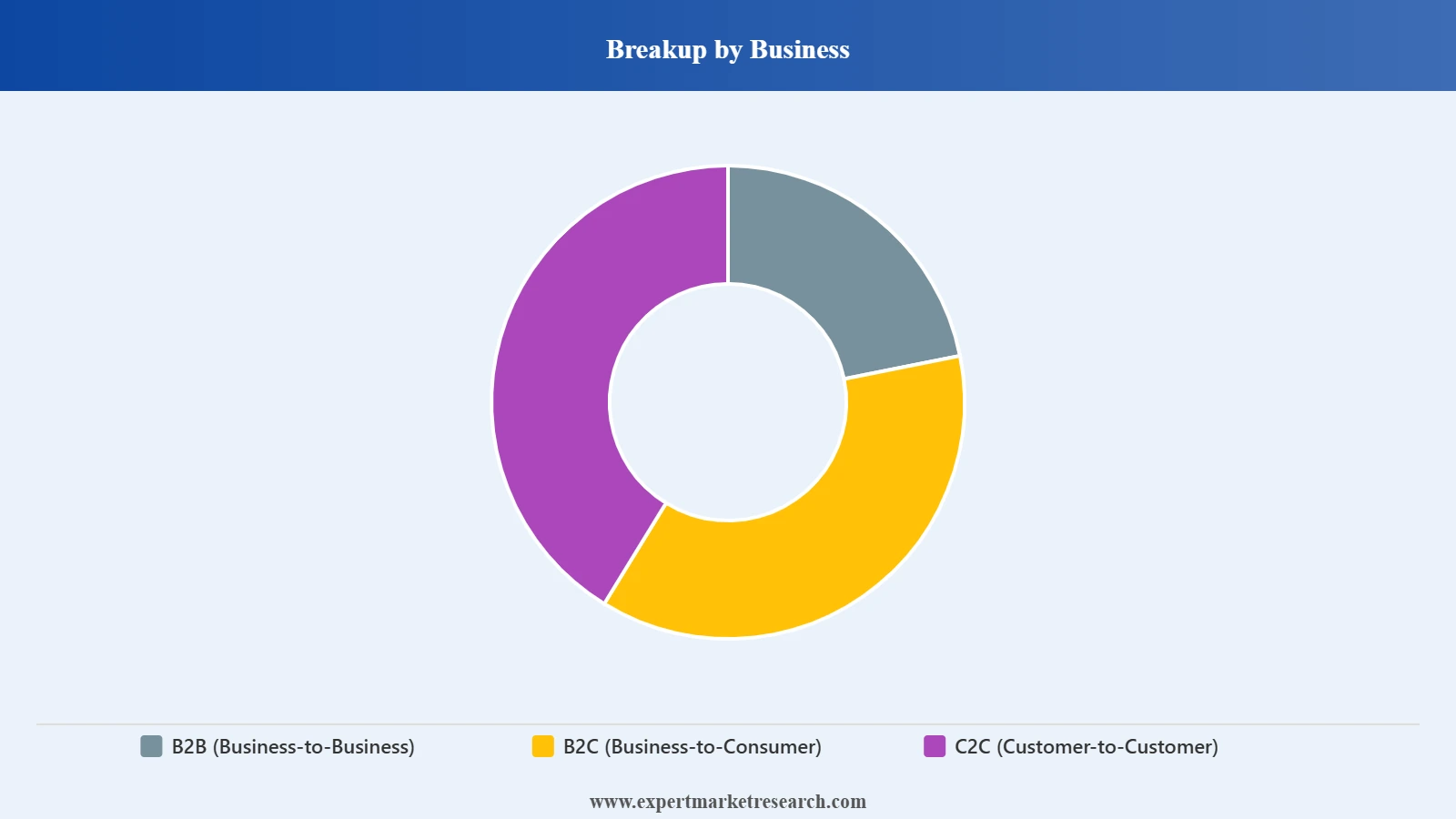

Market Breakup by Business

Key Insight: B2C is the dominant business type in the India CEP market, commanding approximately 56.7% of revenue in 2025 and growing at a CAGR of 12.61%, the fastest among all business type segments. The segment's dominance reflects India's booming D2C brand ecosystem, social commerce adoption, and the deep integration of digital wallets and UPI payments that compress the online purchase lifecycle. B2B shipments sustain significant volume in industrial and manufacturing supply chains, though growth is more measured compared to B2C. C2C parcels are a growing category driven by peer-to-peer resale platforms, with operators experimenting with automated parcel lockers in gated communities to manage last-mile costs as residential parcel density increases.

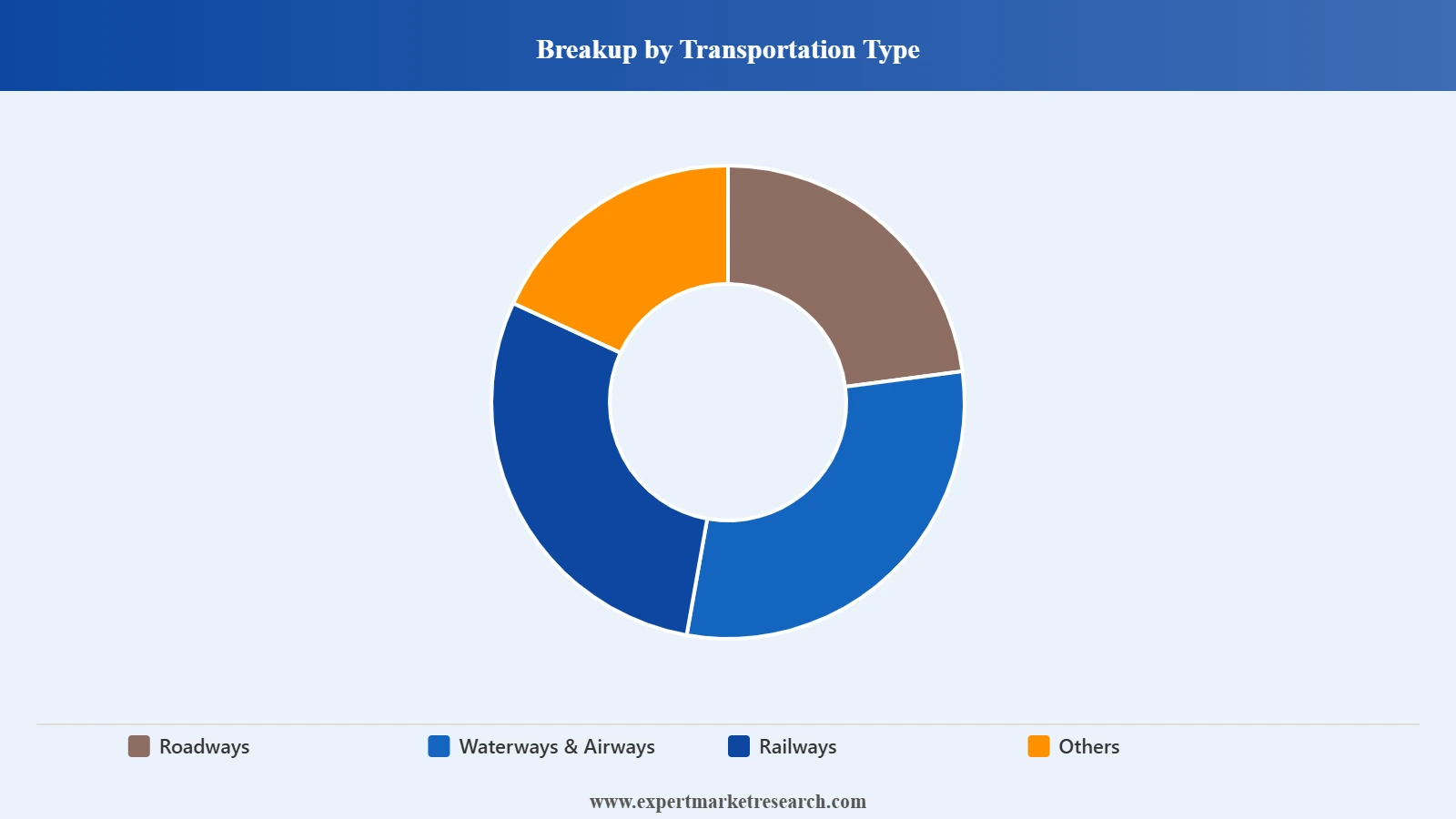

Market Breakup by Transportation Type

Key Insight: Roadways is the dominant transportation mode in India's CEP market, accounting for approximately 56 to 71% of total shipment volume and revenue depending on the segment. Road transport's leadership reflects India's road network coverage, flexibility for last-mile delivery, and the rapid adoption of electric two-wheelers and three-wheelers by delivery operators that reduce per-kilometer operating costs. Airways, while accounting for a smaller share, is the fastest-growing transport mode at approximately 8.9 to 10.9% CAGR, driven by expanding consumer expectations for same-day and next-day delivery that require air freight over long-distance routes. Railways represent a structurally important mode for bulk freight under PM Gati Shakti's dedicated freight corridor program, which is expected to reduce road congestion and improve delivery times on key national trade corridors.

Market Breakup by End User

Key Insight: Retail is the dominant end-user segment in the India CEP market, driven primarily by e-commerce parcel flows generated by platforms including Flipkart, Amazon India, Meesho, and a growing ecosystem of D2C brands. According to available research, e-commerce logistics is projected to grow at an 11.32% CAGR, the fastest among all end-user industries. Industrial Manufacturing is the second-largest end-user segment, contributing approximately 32 to 33% of total CEP revenue, reflecting India's growth as a global production hub requiring synchronized inbound and outbound logistics. Life Sciences and Healthcare is a strategically important segment requiring temperature-controlled and time-definite delivery capabilities, where specialized operators like Safexpress have built differentiated competitive positions. Financial Institutes use CEP services for document and secure item delivery, particularly relevant for the BFSI sector's distributed branch network.

Market Breakup by Region

Key Insight: North India is the largest regional CEP market, anchored by the National Capital Region, which is home to major distribution hubs for e-commerce platforms, Blue Dart's new 250,000 square-foot automated hub, and the industrial manufacturing corridors of the Delhi-NCR region. West India is the second-largest region, driven by Maharashtra's dense consumer markets and the manufacturing clusters of Gujarat. South India is the fastest-growing region, powered by Bengaluru's technology startup and e-commerce ecosystem, Chennai's manufacturing base, and Hyderabad's rapidly expanding urban consumer market. East India, anchored by Kolkata and parts of Odisha and West Bengal, is an emerging growth market as smartphone penetration and e-commerce adoption increase in previously underserved states.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Destination

Domestic shipments hold the dominant position in India's CEP market at approximately 59% of total revenue in 2025, reflecting the market's primary driver of domestic e-commerce growth. The domestic segment is expanding rapidly as tier-2 and tier-3 city consumers increasingly shop online, with quick-commerce platforms operating in 92 non-metro cities and smartphone affordability bringing first-time online shoppers onto e-commerce platforms in smaller towns. International shipments represent the faster-growing segment at 11.8% CAGR over the forecast period, as government policy through ONDC, Free Trade Agreements, and export incentive schemes meaningfully expand the volume of goods flowing through India's international CEP corridors. MSME exporters in particular are generating new international parcel demand as they gain access to global customers through digital storefronts previously unavailable to small businesses.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Business

B2C is the leading and fastest-growing business type segment in the India CEP market, holding approximately 56.7% of revenue in 2025 and growing at 12.61% CAGR. D2C brands, social commerce platforms, and quick-commerce operators are collectively generating an unprecedented volume of residential parcel deliveries that define the modern India CEP market's growth profile. B2B remains the largest by shipment value in industrial-heavy segments, supporting supply chain flows across manufacturing, BFSI, and healthcare industries. C2C is growing from a smaller base, driven by peer-to-peer resale platforms that are creating new delivery use cases as more Indian consumers participate in the circular economy for pre-owned goods, electronics, and fashion items.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India is the largest regional contributor to the India CEP market, with the National Capital Region forming the most active parcel origin and destination hub in the country. Blue Dart's January 2025 commissioning of a 250,000 square-foot automated hub in Delhi reflects the region's strategic importance and the scale of investment being directed at northern India's logistics capacity. The NCR's dense consumer population, concentration of manufacturing industries in surrounding states, and status as India's largest metropolitan economy creates consistently high parcel volumes across B2B, B2C, and government-linked delivery channels. Government infrastructure projects including the Western Dedicated Freight Corridor, which has reduced Delhi-Mumbai road haul times by up to 40%, are improving the speed and cost economics of north-to-south freight flows, benefiting CEP operators operating national hub-and-spoke networks.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the fastest-growing regional market for CEP services, driven by Bengaluru's role as India's technology capital and the high density of e-commerce startups, quick-commerce platforms, and D2C brands based in the region. Quick-commerce operators including Swiggy Instamart and Zepto have established some of their densest delivery networks in Bengaluru and Hyderabad, creating large parcel volumes with demanding delivery time requirements. Chennai's manufacturing base, particularly in automotive and electronics, generates significant B2B industrial parcel flows. DTDC's dark store launch in Bengaluru in February 2025 directly targets the South India quick-commerce opportunity. The region's high smartphone penetration, above-average consumer spending power, and large technology workforce create a sustained foundation for above-market-average CEP growth over the forecast period.

The India Courier, Express, and Parcel (CEP) Market is moderately consolidated, with a small number of large network operators commanding significant market share alongside a competitive mid-tier of specialized regional and segment-specific service providers. The competitive landscape is defined by network coverage breadth, last-mile delivery density, technology investment quality, and the ability to serve the growing quick commerce and D2C brand segments with reliable, trackable, time-definite delivery. Market consolidation is accelerating through acquisitions as operators seek network scale and technology synergies to compete on cost and service reliability simultaneously.

Blue Dart, with DHL group backing, leads the premium express air segment. Delhivery has emerged as the technology-forward national network challenger, amplified by its April 2025 acquisition of Ecom Express. FedEx India remains a critical player in international shipments through its commercial alliance with Delhivery. EV adoption is increasingly a competitive differentiator for last-mile operators, with PM E-DRIVE incentives accelerating the transition from petrol two-wheelers to electric alternatives that reduce per-delivery fuel costs and support corporate sustainability commitments to large e-commerce clients.

Founded in 1983 and headquartered in Mumbai, India, Blue Dart Express Limited is South Asia's leading premium express air and integrated transportation and distribution company, operating as a DHL Group company. Blue Dart operates one of India's most comprehensive domestic express delivery networks, covering thousands of pin codes with a combination of air and surface delivery capabilities. In January 2025, the company commissioned a 250,000 square-foot automated sorting hub in Delhi to strengthen its northern India capacity and reduce sorting times. Blue Dart is known for its reliable, time-definite delivery standards, strong presence in the premium B2B and healthcare sectors, and its consistent investment in automation and operational excellence.

Founded in 1995 and headquartered in Bonn, Germany, Deutsche Post AG is the parent company of DHL, one of the world's leading logistics groups with substantial operations in India. In India, DHL operates across express, supply chain, and e-commerce logistics segments through its DHL Express, DHL Supply Chain, and DHL eCommerce divisions. Deutsche Post AG holds a strategic stake in Blue Dart Express Limited, leveraging Blue Dart's domestic network for last-mile delivery while deploying DHL's global capabilities for international express shipments. The company's investment of EUR 500 million in India in 2022, focused on warehousing, workforce development, and sustainability, underscores its long-term commitment to India's logistics growth story.

FedEx India operates as part of FedEx Corporation, founded in 1971 and headquartered in Memphis, USA, one of the world's largest express transportation companies. In India, FedEx focuses on international import and export services through its global network, leveraging a long-term commercial partnership with Delhivery for domestic pick-up and last-mile delivery. FedEx made a USD 100 million equity investment in Delhivery to deepen this strategic alliance, which combines FedEx's international network strength with Delhivery's pan-India domestic infrastructure spanning over 18,700 pin codes. FedEx India is positioned as a primary gateway for Indian exporters and multinational corporations requiring reliable cross-border express shipment services into and out of India.

Founded in 2015 and headquartered in Bengaluru, India, Busybees Logistics Solutions, which operates under the brand Xpressbees, is one of India's fastest-growing end-to-end logistics companies. Xpressbees provides express parcel delivery, surface express, B2B freight, and international logistics services, with a tech-driven approach to network management and real-time delivery tracking. The company has been backed by marquee investors and has expanded its automated sortation hub network significantly over recent years. Xpressbees has built a particularly strong presence in tier-2 and tier-3 cities, making it a preferred logistics partner for D2C brands and e-commerce platforms seeking to extend their delivery reach beyond major metropolitan markets.

Other key players in the market are Ecom Express Private Limited, DTDC Express Limited, Delhivery Limited, Atlantic International Express, EKart Logistics, Safexpress Private Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Discover the latest insights on the India Courier, Express, and Parcel (CEP) Market 2026 with our comprehensive report. Stay ahead with verified data on e-commerce delivery growth, quick commerce innovation, government logistics reform impacts, and the regions recording the strongest parcel volume expansion. Whether you are a logistics operator planning network investment, an e-commerce company evaluating delivery partners, or an investor assessing India's logistics sector growth potential, this report provides the strategic intelligence you need. Download your free sample today and explore the key opportunities within India's thriving CEP market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 16.92 Billion.

The market is projected to grow at a CAGR of 11.20% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 48.92 Billion by 2035.

The major drivers of the market are the demand for green mobility, growth of ecommerce, focus on automation, and surging government support.

The key trends of the market include use of electric vehicles, technological integration, preference for quick deliveries and adoption of drone technology.

The major regions in the market are North India, South India, East India and West India.

The various types of destinations considered in the market report are domestic and international.

The various types of business studies in the market report are B2B (business-to-business), B2C (business-to-consumer), and C2C (customer-to-customer).

The transportation types considered in the market report are roadways, waterways & airways, railways, and others

The major players in the market are Blue Dart Express Limited, Deutsche Post AG, FedEx India, Busybees Logistics Solutions Pvt. Ltd., Ecom Express Private Limited, DTDC Express Limited, Delhivery Limited, Atlantic International Express, EKart Logistics, Safexpress Private Limited, and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Destination |

|

| Breakup by Business |

|

| Breakup by Transportation Type |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.