Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

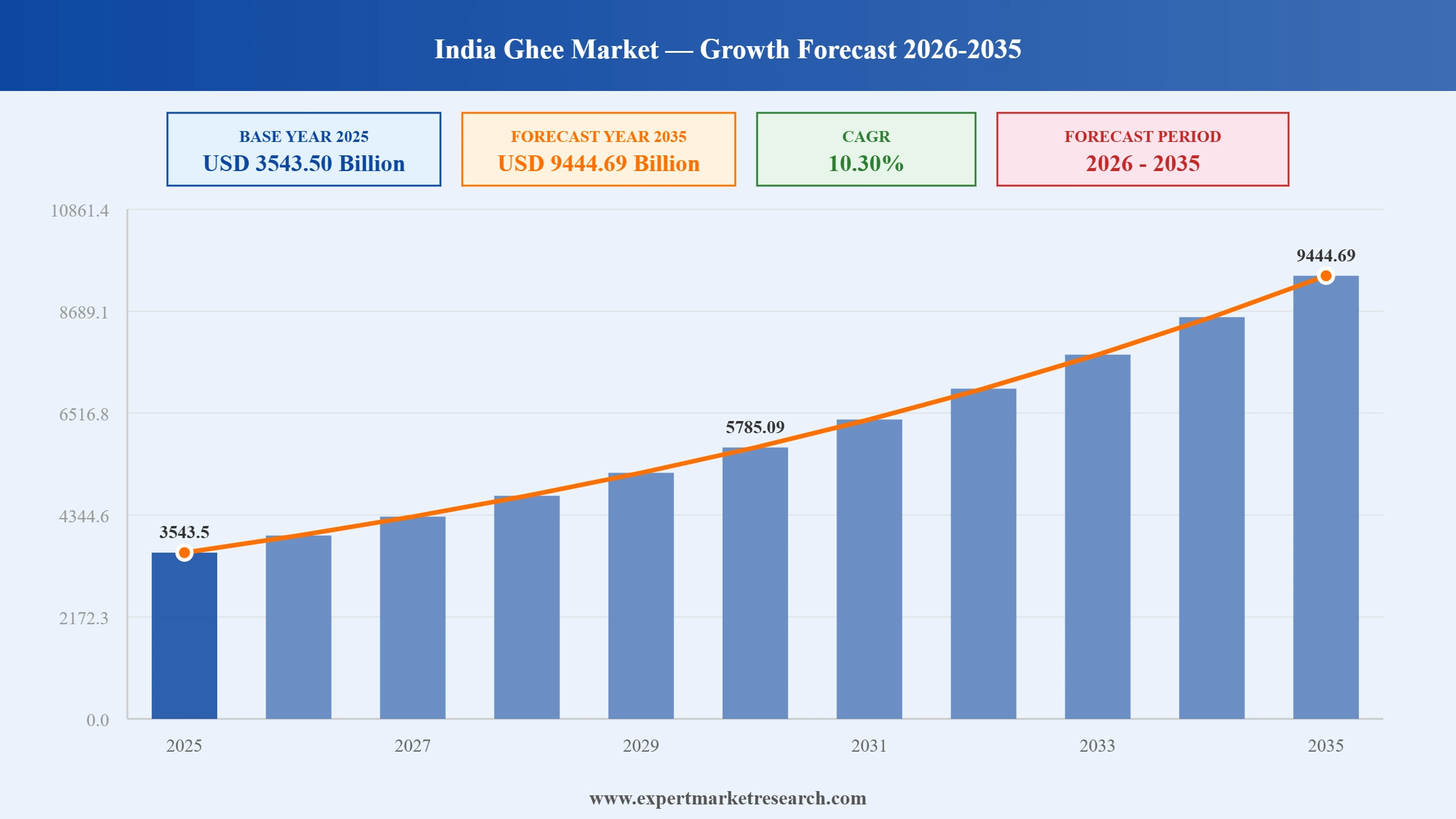

The India ghee market reached a value of USD 3543.50 Billion at 2025 and is projected to expand at a CAGR of around 10.30% during the forecast period of 2026-2035. With rising demand for Ayurveda-linked food products, a structural shift from the unorganised to the organised sector, growing premium and artisanal ghee consumption, and rapid e-commerce distribution expansion, the market is expected to reach USD 9444.69 Billion by 2035.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

| India Ghee Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 3543.50 |

| Market Size 2035 | USD Billion | 9444.69 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 10.30% |

| CAGR 2026-2035 - Market by Region | Karnataka | 13.3% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 11.7% |

| CAGR 2026-2035 - Market by End Use | Retail | 11.7% |

The India ghee market is undergoing a marked structural transformation, with consumer preferences shifting from loose, unbranded ghee to premium, packaged, and health-positioned variants. The rapid expansion of quick commerce and e-commerce channels, alongside growing interest in artisanal bilona ghee and A2 variants, is redefining how ghee is distributed and consumed across India. Major cooperatives and private players are accelerating product innovation and international market entry to capture demand across both domestic and export segments.

In November 2025, Milma, the Kerala cooperative dairy federation, launched five new premium products including Samridhi Ghee, signalling a strategic cooperative push into value-added dairy. The move targeted domestic and export consumers seeking quality-assured ghee, reinforcing the cooperative sector's active premiumisation strategy within the India ghee market.

In October 2025, GCMMF launched Amul Cow Ghee in Fiji through a distribution partnership with FMF Foods, marking Amul's entry into the Pacific market. The launch expanded India's ghee export footprint and strengthened bilateral dairy trade ties between the two countries.

In April 2025, Parag Milk Foods expanded its Gowardhan brand with Crunchy Chikki, a traditional Indian sweet snack made with 100% pure Gowardhan Ghee in sesame and peanut variants, broadening ghee-derived snack consumption among Indian households.

In March 2025, Amaya Milk Company introduced Havan Ghee, a 100% pure cow ghee prepared weekly under Vedic guidelines for religious rituals. The launch addressed growing consumer demand for ritual-grade, purity-certified ghee beyond commercial supermarket brands.

India's ghee market is shifting from loose, unbranded supply to packaged, quality-certified formats. Amul and state dairy federations are formalising procurement and distribution, while branded ghee steadily captures share from unorganised products, broadening the India ghee market across tiers.

Rising health awareness is driving demand for A2 cow ghee and bilona variants at significantly higher price points. India's A2 ghee sub-market is growing rapidly, attracting established brands and artisanal producers, accelerating India ghee market growth in the premium segment.

Recent Development Description 3: Online platforms and quick-commerce channels are creating new access points for packaged ghee among urban consumers valuing convenience and transparency. Branded ghee companies are using direct-to-consumer digital channels to improve margins, broadening their reach in the evolving India ghee segment.

Recent Development Description 4: Growing consumer adoption of Ayurvedic dietary principles is repositioning ghee as a functional wellness ingredient. Nutritionist and influencer endorsements highlighting ghee's butyric acid and fat-soluble vitamin profile are expanding consumption into health-conscious households, sustaining the long-term India ghee market trajectory.

Recent Development Description 5: India's position as the world's largest milk-producing nation underpins growing export momentum for ghee among diaspora communities globally. Amul's October 2025 Fiji launch through FMF Foods signals active international market-building, extending the India ghee market's reach into new export territories.

The Expert Market Research's report titled “India Ghee Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

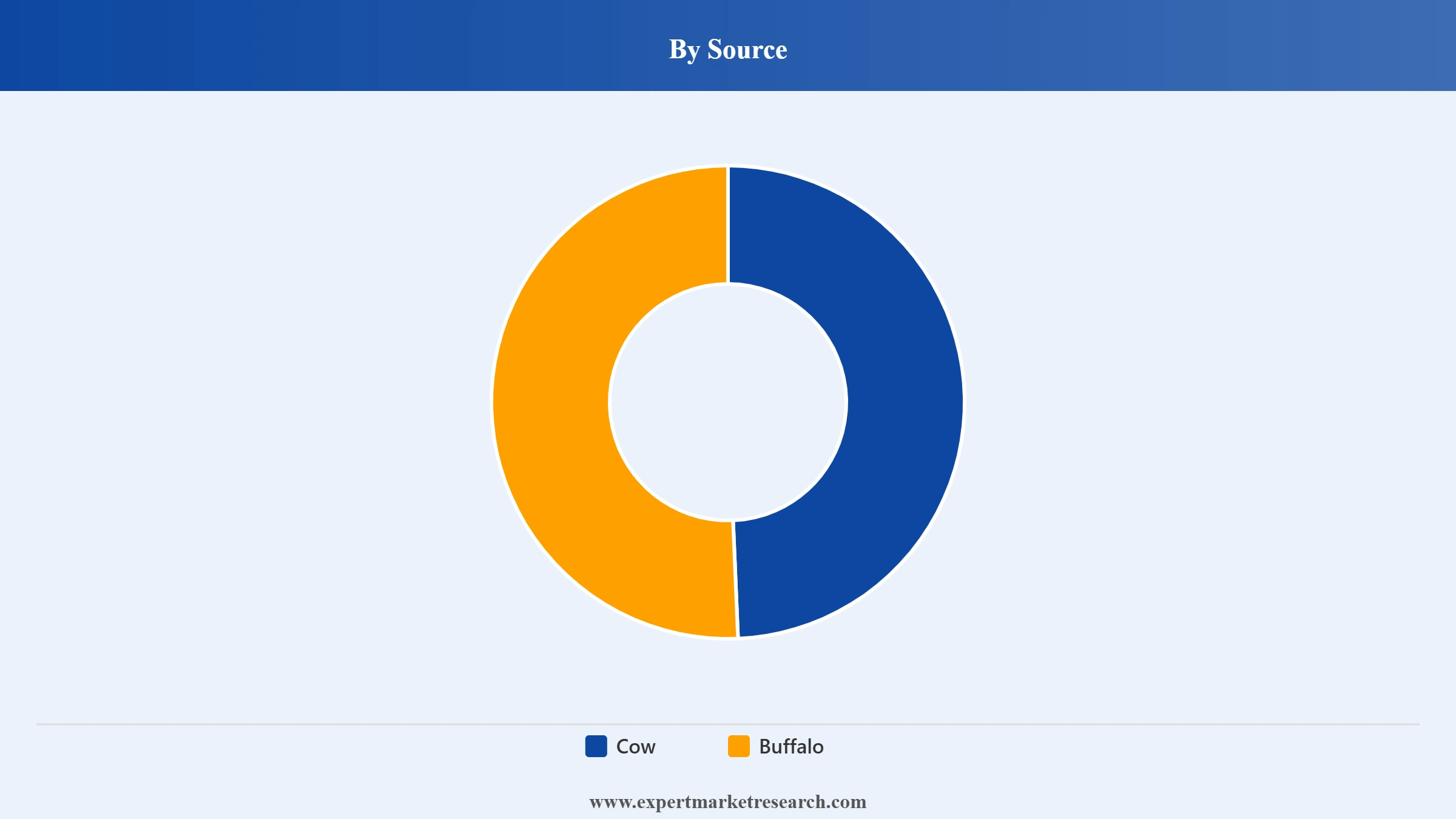

Market Breakup by Source

Key Insight: Cow ghee commands the dominant share of the India ghee market by source, underpinned by its central role in Ayurvedic practices and widespread consumer preference for cow-derived dairy. The rapidly growing premium A2 bilona segment is further reinforcing cow ghee's lead, as health-conscious urban consumers shift toward indigenous-breed, traditionally processed variants. Buffalo ghee addresses a distinct consumer segment, particularly within the HoReCa channel, where its richer fat profile suits commercial-scale cooking applications, providing producers clear differentiation across mass and premium tiers.

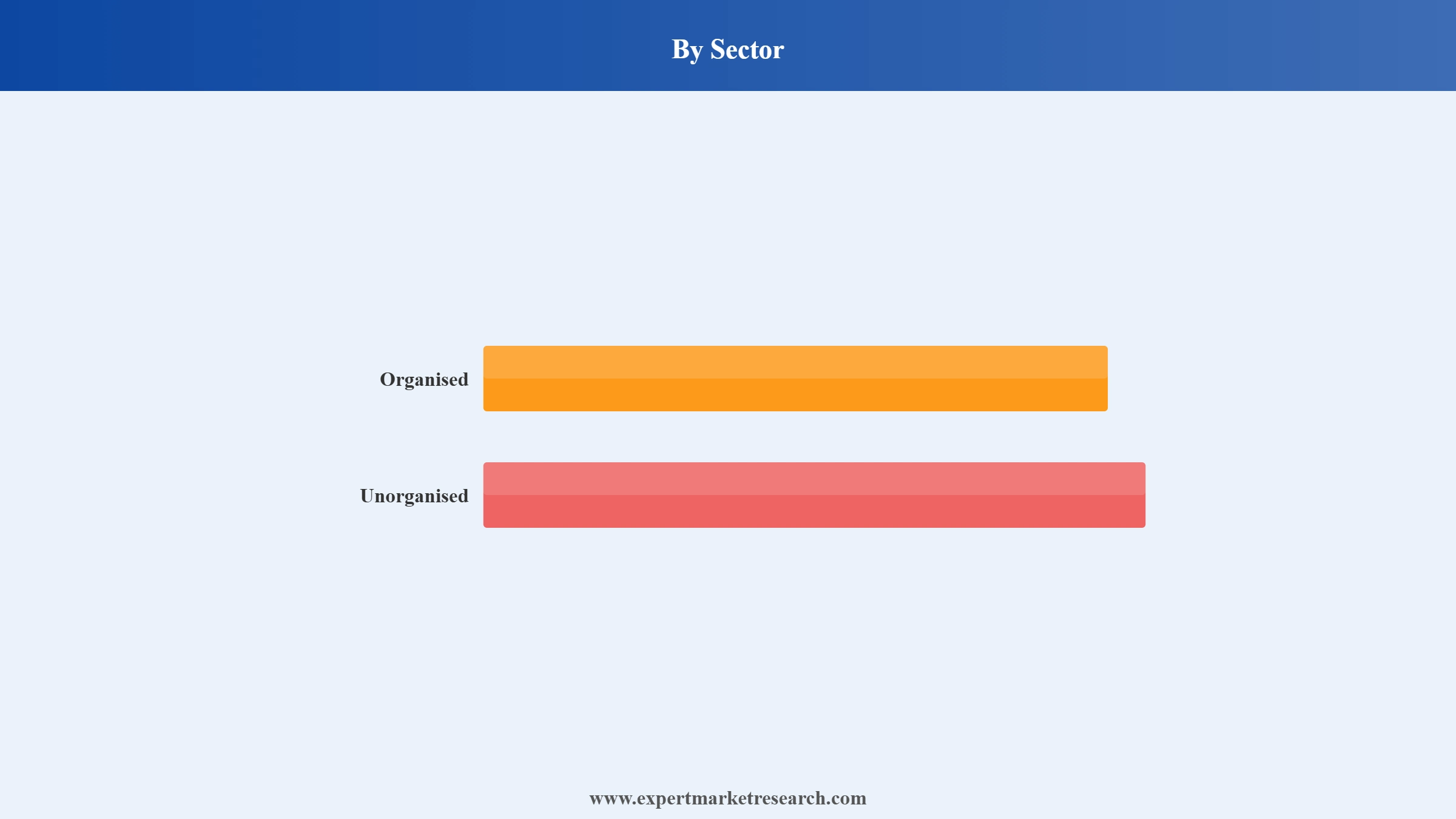

Market Breakup by Sector

Key Insight: The organised sector is gaining market share rapidly as consumers shift toward quality-assured, packaged, branded ghee. Led by national cooperatives such as Amul and Mother Dairy and large private players, organised ghee maintains consistent quality standards, AGMARK certification compliance, and transparent labelling. While the unorganised sector retains a large portion of rural and semi-urban consumption through local dairy outlets, urbanisation and rising income levels are systematically channelling purchasing behaviour toward the organised channel, a structural transition directly expanding the addressable market for established brands.

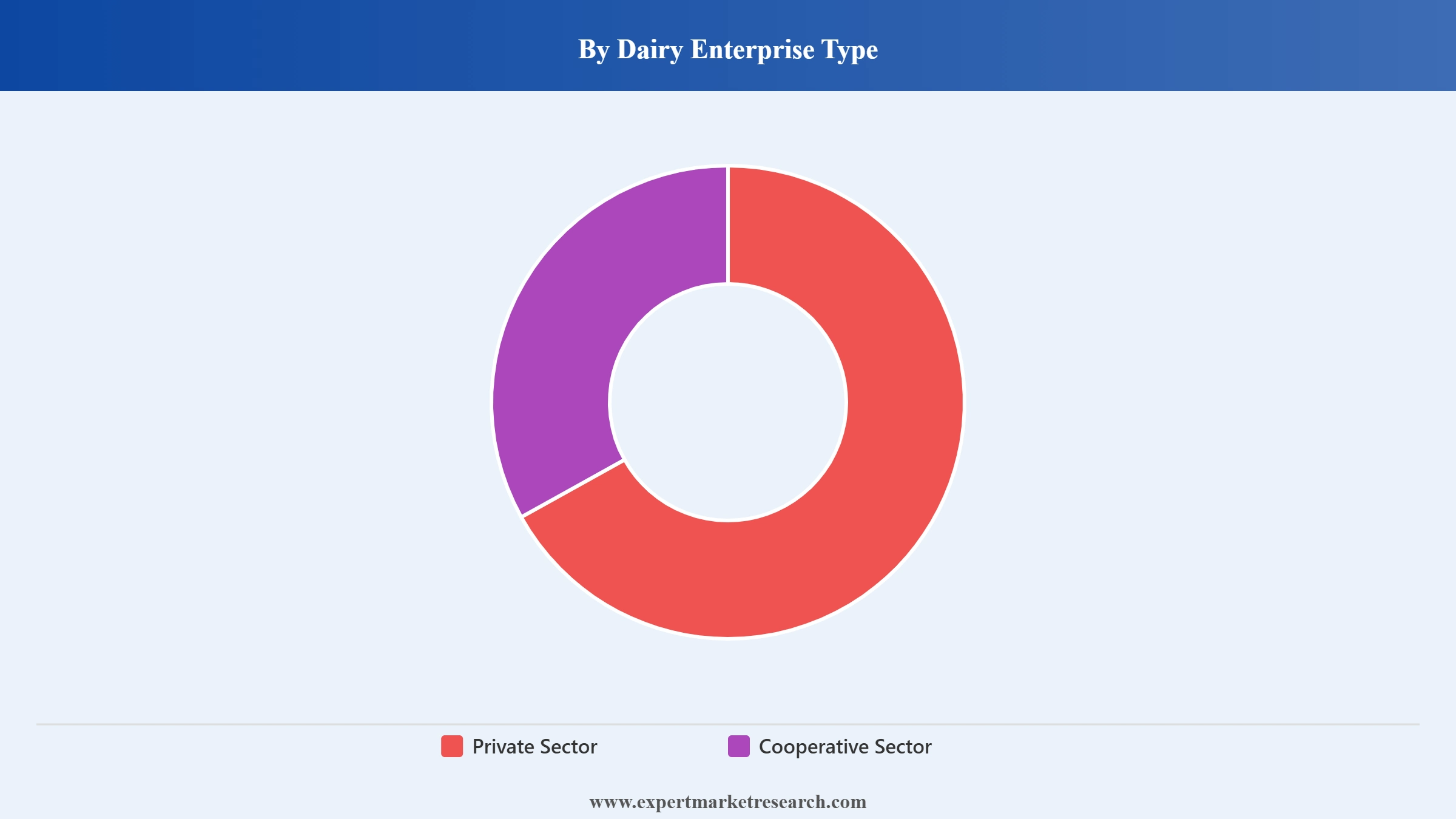

Market Breakup by Dairy Enterprise Type

Key Insight: Cooperative dairies, including GCMMF (Amul), Rajasthan Cooperative Dairy Federation (Saras), and Punjab Milkfed (Verka), hold strong positions through farmer-linked procurement networks and government backing. Private sector players including Parag Milk Foods (Gowardhan) and Anik Milk Products are driving premiumisation and national distribution expansion. The two enterprise types serve complementary price tiers, with cooperatives anchoring the mid-market and private enterprises leading premium and value-added ghee growth, resulting in a well-structured competitive dynamic across the India ghee market.

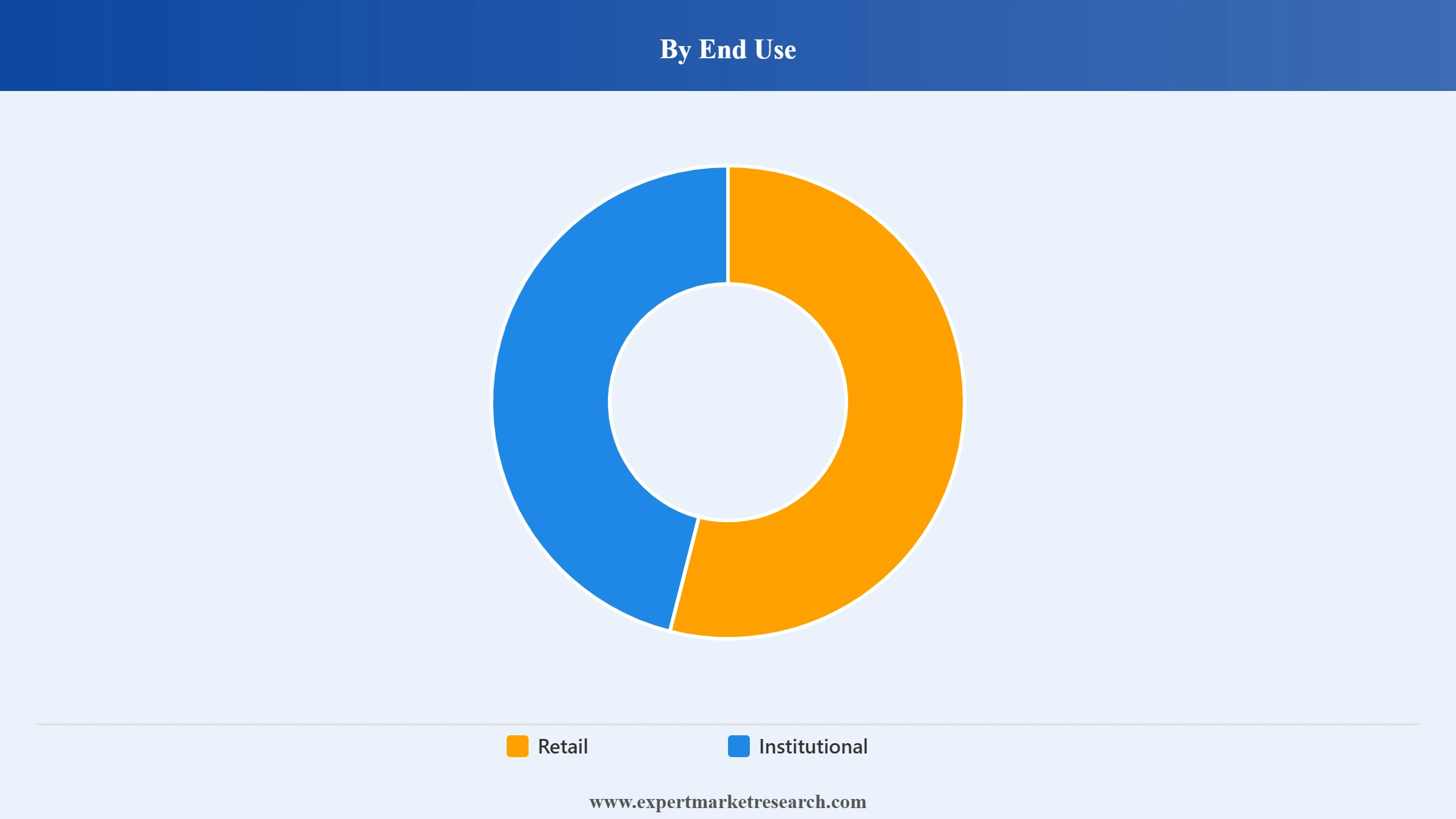

Market Breakup by End Use

Key Insight: The retail segment dominates end use, reflecting ghee's indispensable role in Indian household cooking, religious rituals, and traditional medicine. Retail demand is supported across all income brackets, with mass-market brands serving price-sensitive households and premium variants targeting health-conscious urban buyers. The institutional segment, covering food service, confectionery manufacturing, and Ayurvedic product formulation, is growing steadily as demand from quick-service restaurants, sweet manufacturers, and nutraceutical producers expands, creating a complementary growth layer alongside the dominant retail channel.

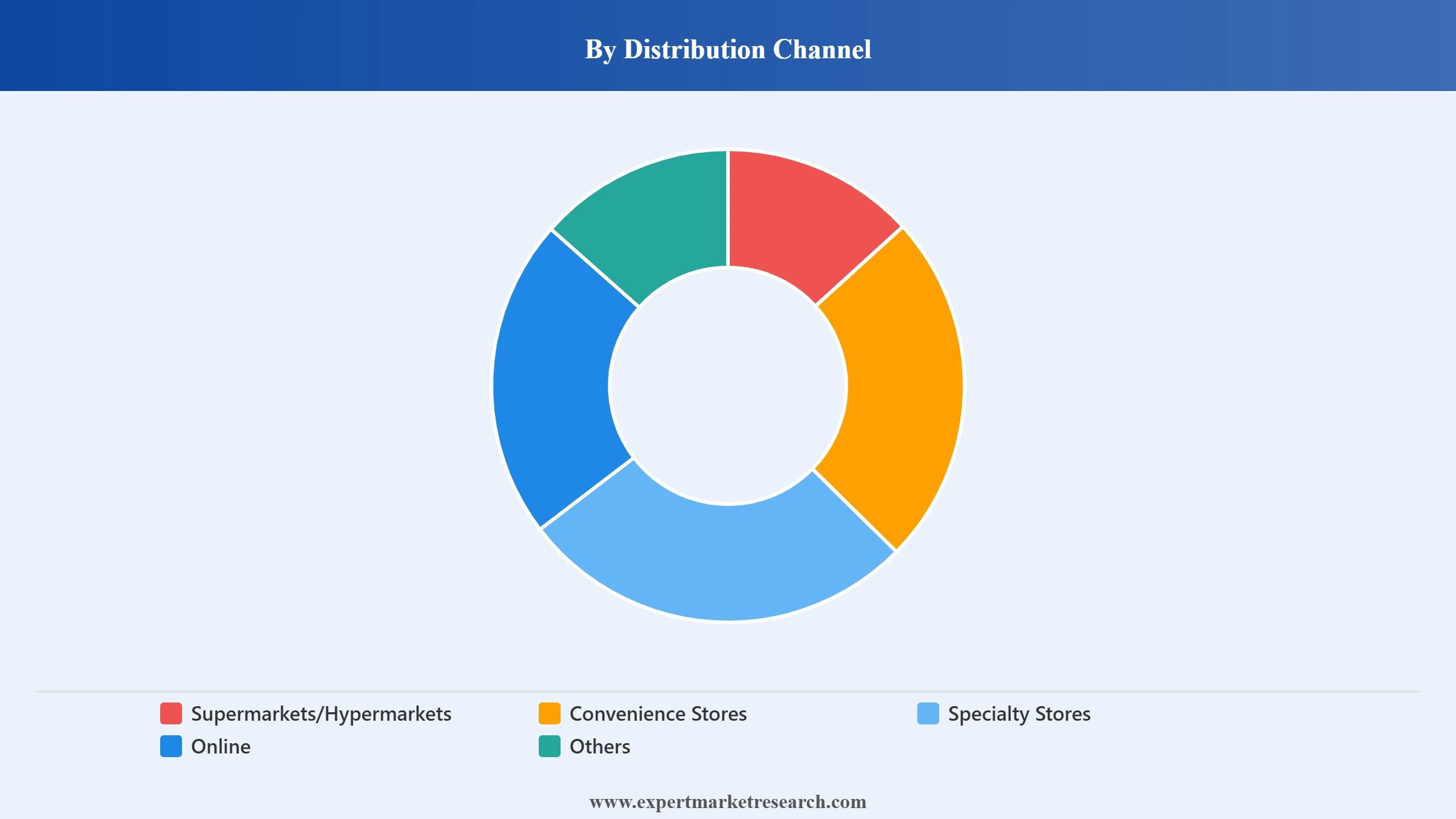

Market Breakup by Distribution Channel

Key Insight: Supermarkets and hypermarkets remain the dominant distribution channel for packaged ghee, offering consumers a wide range of SKUs and promotional access across national and regional brands. The online channel is the fastest-growing, driven by quick-commerce platforms enabling same-day delivery for premium brands. Specialty stores catering to organic, A2, and artisanal ghee are emerging as a differentiated channel for health-conscious buyers, while convenience stores continue to serve habitual, repeat purchases in urban and peri-urban markets.

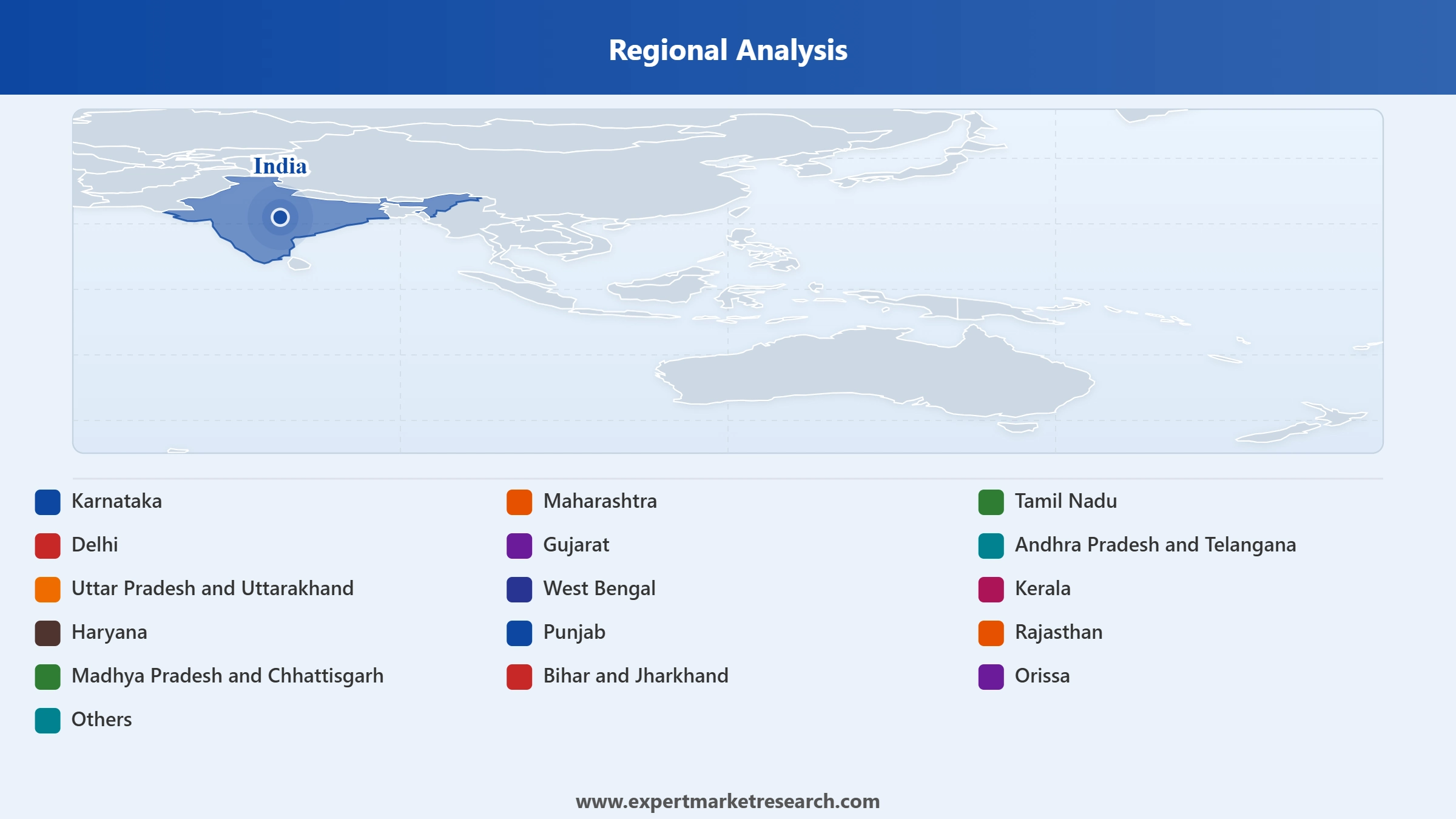

Market Breakup by Region

Key Insight: Uttar Pradesh and Uttarakhand is the largest regional market, driven by India's highest dairy cattle population, extensive ghee production infrastructure, and deeply embedded consumption traditions across religious and culinary practices. Rajasthan leads in per-capita ghee consumption nationally, reflecting its rich culinary culture and the strong network of Rajasthan Cooperative Dairy Federation (Saras). Gujarat anchors cooperative dairy scale through GCMMF (Amul), while Karnataka, Maharashtra, and Tamil Nadu drive urban premiumisation and organised retail growth in the India ghee market.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

By Source, Cow ghee dominates the market due to its Ayurvedic endorsement and widespread consumer preference

Cow ghee holds the dominant share of the India ghee market by source. Its deep cultural and Ayurvedic association positions it as the default choice for household and institutional buyers. Brands including Amul Cow Ghee, Gowardhan, and Patanjali Cow Ghee anchor the mass market, while premium sub-categories, including bilona and A2 ghee, have created a fast-growing upper tier that is pulling more health-conscious urban consumers into the branded ghee segment. India's growing preference for indigenous cow breeds such as Gir and Sahiwal underpins the A2 cow ghee premium segment, which is growing well above the overall market rate.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

Buffalo ghee represents the second-largest source segment, supported by India's large buffalo dairy base in states such as Uttar Pradesh, Madhya Pradesh, and Rajasthan. Buffalo ghee's higher fat content makes it well-suited for the HoReCa sector and certain regional cuisines. New product entries in the buffalo dairy segment, including expanded offerings from Mother Dairy in early 2025, signal renewed commercial attention toward buffalo-derived dairy products, which could further expand this segment's contribution to the India ghee market through the forecast period.

By Sector, the Organised segment leads the market due to rising consumer trust in branded, quality-certified products

The organised sector commands a growing and increasingly dominant share of the India ghee market, driven by post-pandemic consumer trust in branded dairy, FSSAI-mandated quality standards, and the expansion of modern trade and quick-commerce channels. Cooperative giants such as Amul, Saras, and Milma, alongside private players such as Parag Milk Foods and Anik, have invested significantly in production capacity, cold-chain logistics, and digital marketing to consolidate their positions within the India ghee market.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

The unorganised sector retains a substantial share in rural and semi-urban markets where loose ghee from local dairies remains price-competitive. However, the structural shift toward packaged formats is accelerating as middle-class consumers in Tier 2 and Tier 3 cities upgrade from loose to branded ghee. Government initiatives such as the National Dairy Development Board's quality certification drives are adding further momentum to this transition, directly supporting organised sector growth throughout the forecast period.

By Dairy Enterprise Type, the Cooperative sector anchors the market through farmer-linked supply chains and national distribution

The cooperative sector, led by GCMMF (Amul), Rajasthan Cooperative Dairy Federation (Saras), and Punjab Milkfed (Verka), holds a dominant value share of the India ghee market by enterprise type. These federations benefit from assured raw milk procurement through farmer member networks, government-backed pricing stability, and decades of brand trust. Amul's ghee alone commands the highest single-brand market share in India, distributed across over one million retail outlets nationwide, providing it unmatched geographic reach.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

The private sector is the faster-growing enterprise type, as companies like Parag Milk Foods, Heritage Foods, and Anik Milk Products expand premium product lines, invest in modern processing infrastructure, and build direct-to-consumer digital channels. Parag Milk Foods outlined plans in January 2026 to scale its premium and new-age dairy businesses, with Gowardhan Ghee remaining central to its India ghee market growth strategy through the forecast period.

By End Use, the Retail segment dominates due to ghee's role as an everyday household cooking and wellness ingredient

The retail segment accounts for the dominant share of the India ghee market by end use, reflecting ghee's indispensable role in Indian daily cooking, religious rituals, and traditional medicine. Retail demand is supported across all income brackets, from mass-market brands serving price-sensitive households to premium variants targeting health-conscious urban buyers. The supermarket and hypermarket channel amplifies retail access for national brands, while quick-commerce platforms are enabling convenience-driven repurchase cycles among urban consumers.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

The institutional end-use segment is growing steadily, driven by expansion in the food service industry, confectionery manufacturing, and Ayurvedic product formulation. Quick-service restaurant chains and sweet manufacturers in Gujarat, Rajasthan, and Uttar Pradesh are among the largest institutional ghee consumers, sourcing directly from cooperatives and large private players. The pharmaceutical and nutraceutical segment also contributes incremental demand as formulations incorporating ghee-based lipid carriers gain traction in Ayurvedic wellness products.

By Distribution Channel, Supermarkets/Hypermarkets lead by volume while Online is the fastest-growing channel

Supermarkets and hypermarkets command the dominant distribution channel share for packaged ghee in India, providing high footfall, promotional visibility, and extensive shelf space for both national and regional brands. Chains such as Reliance Smart, D-Mart, and Big Bazaar are key retail partners for cooperatives and private dairy companies seeking volume throughput. This channel's dominance reflects India's growing organised retail penetration, particularly in Tier 1 and Tier 2 cities where supermarkets have replaced traditional wholesale channels for routine ghee purchases.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

The online channel, comprising e-commerce platforms and quick-commerce players such as Blinkit, Zepto, and Swiggy Instamart, is the fastest-growing distribution channel within the India ghee market. These platforms enable premium brands to reach health-conscious, urban consumers who prioritise quality, traceability, and convenience. Parag Milk Foods' multi-channel expansion in 2025, spanning general trade, modern trade, and quick commerce, directly reflects this structural shift in ghee purchasing behaviour across India.

Uttar Pradesh and Uttarakhand dominates the market due to the highest cattle population and deeply embedded ghee consumption traditions

Uttar Pradesh and Uttarakhand represents the largest regional market for ghee in India, underpinned by the country's highest dairy cattle population and a per-household ghee consumption culture rooted in North Indian cuisine, religious observance, and Ayurvedic practice. The region's extensive cooperative dairy infrastructure supports both local production and outbound supply to national distribution networks. The organised sector is expanding steadily into smaller UP towns as income levels and consumer aspirations for branded, quality-assured products continue to rise.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

Rajasthan is among the fastest-growing states in the India ghee market, driven by the highest per-capita ghee consumption in India and the well-established network of Rajasthan Cooperative Dairy Federation (Saras). The state's food culture, which incorporates ghee extensively into traditional cuisine including dal baati churma and regional sweets, sustains consistent year-round demand. Urbanisation in Jaipur, Jodhpur, and Kota is channelling consumption toward packaged organised formats, while Gujarat, home to Amul, continues to anchor cooperative scale, and Southern states including Karnataka and Tamil Nadu are emerging as premium ghee consumption markets amid rising disposable incomes.

The India ghee market is characterised by a dual competitive structure, with government-backed dairy cooperatives and large private sector players operating at national scale alongside a fragmented base of regional brands and unorganised producers. Cooperatives such as Amul (GCMMF), Saras (RCDF), and Milma benefit from farmer-linked procurement infrastructure, extensive distribution networks, and strong legacy brand equity, making them formidable incumbents across price tiers. Private sector companies including Parag Milk Foods and Anik Milk Products are competing aggressively in premium and value-added ghee segments, investing in product innovation, digital marketing, and e-commerce expansion.

The competitive landscape is undergoing consolidation, with organised players systematically capturing share from unbranded loose ghee. Key competitive priorities include quality certification, packaging innovation, e-commerce penetration, and health-linked product differentiation such as A2, bilona, and organic ghee variants. Companies are also leveraging cultural marketing and Ayurvedic endorsements to strengthen brand recall and expand into export markets, intensifying competition at both the volume and value ends of the India ghee market.

Established in 1946 and headquartered in Anand, Gujarat, GCMMF operates under the Amul brand as India's largest food products marketing cooperative. With a presence across over one million retail outlets and exports to more than 50 countries, Amul's ghee portfolio commands the highest single-brand market share in the India ghee market. The federation's farmer-owned procurement model, AGMARK-certified manufacturing, and decades of consumer trust give it a structural competitive advantage across mass, mid, and premium tiers.

Incorporated in 1959 and headquartered in Gurugram, Haryana, Nestlé India is the Indian subsidiary of global food and beverage company Nestlé S.A. Known for its wide portfolio spanning MAGGI, KitKat, and everyday dairy products, Nestlé India markets ghee under its everyday dairy range. The company leverages ISO-certified production facilities, an extensive national distribution network, and the parent group's R&D capabilities to serve organised retail and institutional buyers with consistently high quality-standard dairy products.

Founded in 1974 and headquartered in New Delhi, Mother Dairy is a wholly owned subsidiary of the National Dairy Development Board, operating as one of India's leading organised dairy brands. Mother Dairy's ghee is distributed through its extensive retail booth network, modern trade channels, and e-commerce platforms, with particular strength in Delhi-NCR and North Indian urban markets. The company's government-backed quality mandate and affordable pricing position it as a trusted household brand, competing directly with Amul across mass-market and mid-tier ghee segments.

Founded in 2006 and headquartered in Haridwar, Uttarakhand, Patanjali Ayurved is a consumer goods company built on Ayurvedic and natural product positioning. Patanjali's cow ghee is among the top-selling SKUs within its dairy range, marketed on Ayurvedic authenticity, natural processing, and competitive pricing. With a pan-India distribution network reaching over 15,000 stores and a growing e-commerce presence, Patanjali competes effectively across urban and rural markets, particularly among health-conscious and religiously oriented consumer segments.

Other key players in the market are Britannia Industries Limited, Anik Milk Products Pvt Ltd., SMC Foods Limited, The Punjab State Cooperative Milk Producers' Federation Ltd., Milk Food Ltd., Parag Milk Foods Ltd., Rajasthan Cooperative Dairy Federation Ltd, Gopaljee Dairy Foods Pvt Ltd, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the full scope of India's ghee market with our detailed forecast report for 2026-2035. Whether you are a dairy cooperative assessing state-level production opportunities, a private label brand evaluating premiumisation potential, a retail chain tracking channel shifts, or an investor seeking exposure to one of India's fastest-growing packaged food segments, this report delivers the granular intelligence you need. Download your free sample today and tap into the opportunities shaping the India ghee market through 2035.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India market for ghee attained a value of nearly USD 3543.50 Billion.

The market is assessed to grow at a CAGR of 10.30% between 2026 and 2035.

The India ghee market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 9444.69 Billion by 2035.

The major market drivers are the increasing demand for ghee in cooking and growing awareness about the health benefits of ghee.

The key market trends for ghee in India include the growing utilisation of ghee in Ayurveda and the rising demand for the product in traditional restaurants.

The various sources of ghee include cow and buffalo.

The different sectors of ghee include organised and unorganised.

The enterprise types for ghee include the private sector and cooperative sector.

The primary end uses of ghee include retail and institutional.

The various distribution channels for ghee include supermarkets/hypermarkets, convenience stores, specialty stores, and online, among others.

The major players in the market are Gujarat Co-operative Milk Marketing Federation Ltd, Nestlé India Limited, Britannia Industries Limited, Mother Dairy Fruits and Vegetables Pvt. Ltd., Anik Milk Products Pvt Ltd., Patanjali Ayurved Limited, SMC Foods Limited, The Punjab State Cooperative Milk Producers' Federation Ltd., Milk Food Ltd., Parag Milk Foods Ltd., Rajasthan Cooperative Dairy Federation Ltd, and Gopaljee Dairy Foods Pvt Ltd, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Source |

|

| Breakup by Sector |

|

| Breakup by Dairy Enterprise Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.