Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

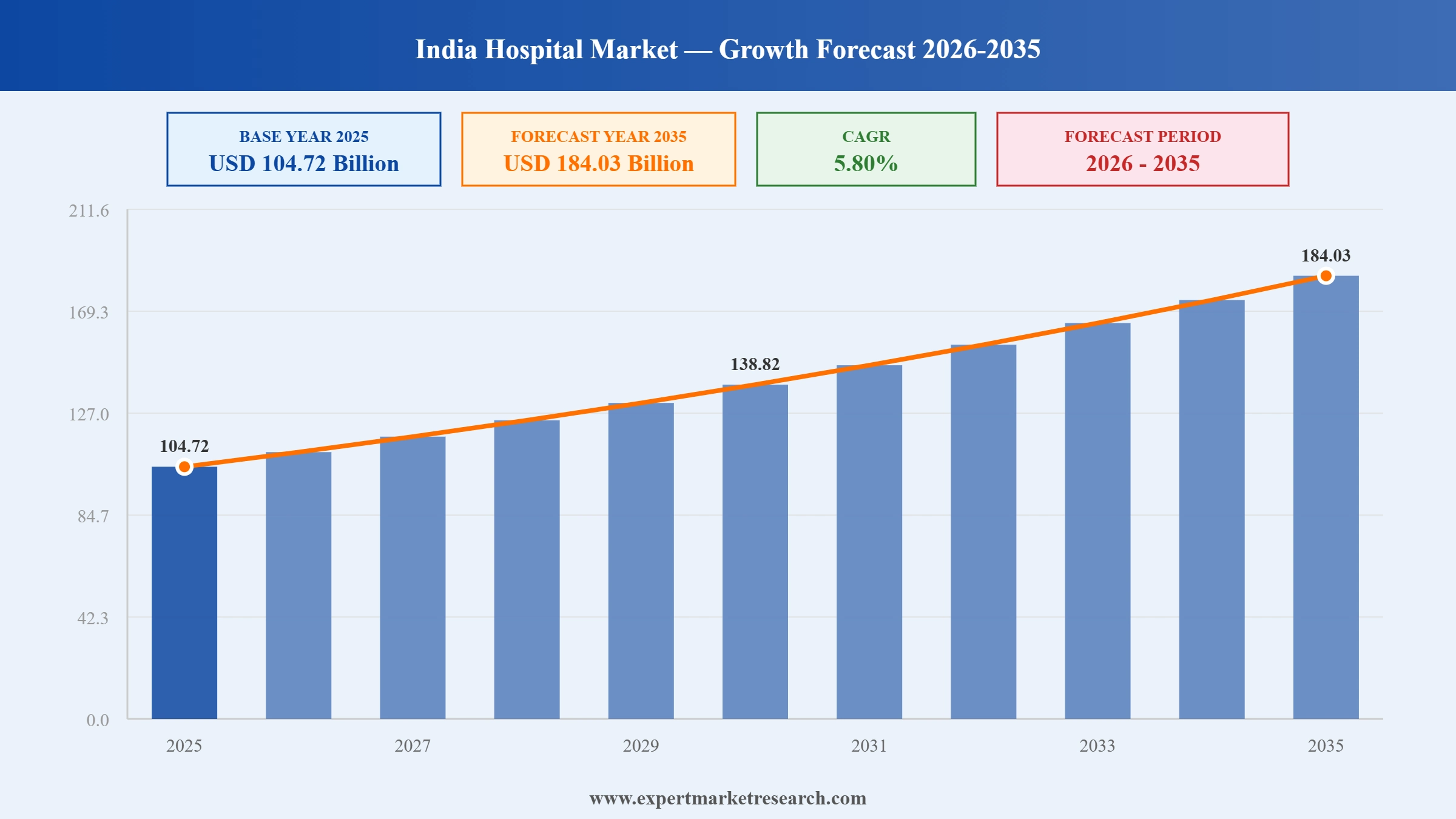

The India hospital market was valued at USD 104.72 Billion in 2025. It is poised to grow at a CAGR of 5.80% during the forecast period of 2026-2035, and reach USD 184.03 Billion by 2035. The market growth is driven by the increasing healthcare infrastructure development and rising patient admissions across public and private facilities. The growing adoption of advanced medical technologies and expansion of specialized healthcare services will contribute to the market growth in the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The hospitals in India are undergoing rapid transformation through infrastructure modernization, advanced medical technologies, and improved healthcare accessibility. The sector plays a critical role in addressing the growing burden of chronic and acute diseases across the country. The market is poised to grow at a CAGR of 5.80% during the forecast period of 2026-2035. The growth is driven by increasing patient volumes, healthcare investments, medical tourism, and the expansion of private healthcare networks.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market Breakup by Type

The market is segmented by type into public and private hospitals, with growth supported by expanding healthcare infrastructure, increasing patient admissions, rising government healthcare investments, and the growing presence of privately operated facilities offering advanced medical services.

Market Breakup by Specialization

The market is segmented by specialization into general, multi-specialty, specialty, super specialty, and others, driven by increasing demand for specialized treatments, higher disease burden, technological advancements, and expanding access to comprehensive healthcare services.

Market Breakup by Bed Capacity

The market is segmented by bed capacity into small hospitals, medium hospitals, and large hospitals, with demand influenced by population growth, rising hospitalization rates, healthcare accessibility initiatives, and capacity expansion to accommodate increasing patient volumes.

Market Breakup by Type of Care

The market is segmented by type of care into primary care, secondary care, and tertiary care, supported by growing emphasis on preventive healthcare, increasing referral-based treatments, and rising demand for advanced diagnostic and complex medical procedures.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Analysis Type | Factors | Example |

| Market Drivers | Increasing healthcare infrastructure development and integration of AI-enabled technologies improving hospital efficiency, treatment quality, and patient outcomes. | In July 2025, Pi Health launched a 30-bed AI-enabled cancer hospital in Hyderabad, enhancing clinical trials and treatment delivery. |

| Market Restraints | Shortage of skilled healthcare professionals and inadequate healthcare infrastructure across rural regions limiting service accessibility and expansion. | Rural areas continue facing shortages of hospital beds, advanced diagnostic equipment, and specialized care services, restricting healthcare access. |

| Market Opportunities | Rising adoption of digital healthcare solutions supporting telemedicine, patient data management, and technology-driven healthcare delivery models. | By February 2026, over 78 crore digital health IDs and 37.2 crore teleconsultations under ABDM strengthened healthcare accessibility. |

The following section outlines the key factors influencing market growth, including major drivers, restraints, and emerging opportunities.

Increasing Healthcare Infrastructure Development and Technology Integration Supporting Market Expansion

The continuous expansion of healthcare infrastructure, coupled with the adoption of advanced digital technologies, is playing a significant role in the growth of the market. Hospitals are increasingly investing in modern facilities, specialized treatment centers, and technology-driven healthcare services to improve patient outcomes and operational efficiency. For instance, in July 2025, Forbes reported that Pi Health established a 30-bed AI-enabled cancer hospital in Hyderabad to accelerate clinical trials and enhance treatment delivery through advanced digital solutions. The successful implementation of AI-supported hospital operations highlights the growing focus on technologically advanced healthcare infrastructure, which is strengthening hospital capabilities, improving access to quality care, and supporting the expansion of the hospital market across India.

Shortage of Skilled Healthcare Professionals and Uneven Resource Distribution to Limit the Market Expansion

Limited healthcare infrastructure across rural and remote regions remains a major challenge for the market. Many areas continue to face shortages of hospital beds, advanced medical equipment, diagnostic facilities, and specialized care services. This disparity restricts access to quality healthcare, delays treatment, and increases the burden on urban hospitals. As a result, hospitals encounter difficulties in expanding service coverage and meeting the rising demand for healthcare, thereby constraining the overall growth and development of the market.

Growing Adoption of Digital Healthcare Solutions Accelerate the Market Growth

The increasing adoption of digital healthcare technologies is transforming healthcare delivery by improving access to medical services, enhancing patient data management, and supporting efficient clinical decision-making. According to the India Brand Equity Foundation (IBEF), in February 2026, India had generated more than 78 crore digital health IDs under the Ayushman Bharat Digital Mission (ABDM), while the eSanjeevani platform had facilitated approximately 37.2 crore teleconsultations by mid-2025. This growing digital health infrastructure is expected to strengthen healthcare accessibility, promote technology-driven care models, and contribute to the sustained growth of the market in the coming years.

Some of the notable trends in the market are rising medical value tourism and cross-border healthcare demand.

Rising Medical Value Tourism is Likely to Enhance Market Landscape

The growing prominence of medical value tourism is emerging as a significant trend in the market, driven by India’s combination of advanced healthcare infrastructure, skilled medical professionals, and cost-effective treatment options. For instance, according to PIB Research, India recorded 507,244 foreign arrivals for medical treatment in 2025, while medical tourism accounted for approximately 5.5% of total foreign tourist arrivals. The increasing inflow of international patients is strengthening hospital utilization rates, expanding healthcare service revenues, and supporting sustained growth in the market.

Multi-Specialty Expected to Lead the Market Share by Specialization

The market is segmented by specialization into general, multi-specialty, specialty, super specialty, and others. Among these, multi-specialty hospitals are expected to lead the market owing to their ability to provide a broad range of medical services under one roof, including diagnostics, emergency care, surgical procedures such as robotic surgical procedures, and specialized treatments. Their integrated healthcare model improves patient convenience, treatment coordination, and operational efficiency, making them the preferred choice for a growing patient population. Rising demand for comprehensive healthcare services, expanding hospital infrastructure, and increasing adoption of advanced healthcare and medical cleanroom technology are further strengthening their position. As healthcare delivery continues to evolve, multi-specialty hospitals are expected to remain the primary contributors to market growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The key features of the market report comprise funding and investment analysis and strategic initiatives by the leading players. The major companies in the market are as follows:

Apollo Hospitals Enterprise Limited is one of the largest private hospital networks, operating multispecialty and super-specialty hospitals supported by advanced healthcare technologies. Its services include cardiac sciences, oncology, neurosciences, organ transplantation, robotic surgery, proton therapy, AI-enabled diagnostics, and preventive healthcare programs. Through its extensive hospital, clinic, pharmacy, and diagnostic center network, Apollo plays a significant role in expanding access to advanced healthcare services in the market.

Max Healthcare Institute Limited is a leading healthcare provider with a network of super-specialty hospitals offering advanced medical services. Its key offerings include robotic surgery, oncology, cardiac sciences, neurosciences, organ transplantation, orthopedics, and home healthcare solutions. The company continues to strengthen its presence through hospital expansion and specialized care programs, supporting the growth and modernization of the market with technology-driven and patient-centric healthcare services.

Fortis Healthcare Limited is a prominent healthcare organization providing comprehensive tertiary and quaternary care services across multiple specialties. Its healthcare portfolio includes bone marrow transplantation, CAR-T cell therapy, robotic surgery, cancer care, genomic medicine, ECMO, and advanced surgical procedures. By delivering specialized treatments through its network of hospitals and centers of excellence, Fortis contributes significantly to the advancement of quality healthcare infrastructure within the India hospital market.

Narayana Health is a major healthcare provider known for delivering affordable and specialized medical care through its multispecialty hospital network. The company offers advanced services in cardiac sciences, cancer care, neurosciences, gastro sciences, orthopedics, and health insurance solutions. Through its focus on accessible healthcare, clinical excellence, and large-scale hospital operations, Narayana Health remains an important participant in the market, supporting increased healthcare accessibility and patient care delivery.

Other key players in the market are Aster DM Healthcare Limited, Shalby Limited, Medanta The Medicity Global Health Pvt Ltd., Tata Memorial Centre (TMC), All India Institute of Medical Sciences (AIIMS), Kokilaben Dhirubhai Ambani Hospital & Medical Research Institute, Sir Ganga Ram Hospital, and Lilavati Hospital & Research Centre.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

This report is developed through a robust mixed-methods research framework combining:

Upto 15% Off

USD

$3099 $2789

$1999 $1799

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Specialization |

|

| Breakup by Bed Capacity |

|

| Breakup by Type of Care |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.