Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

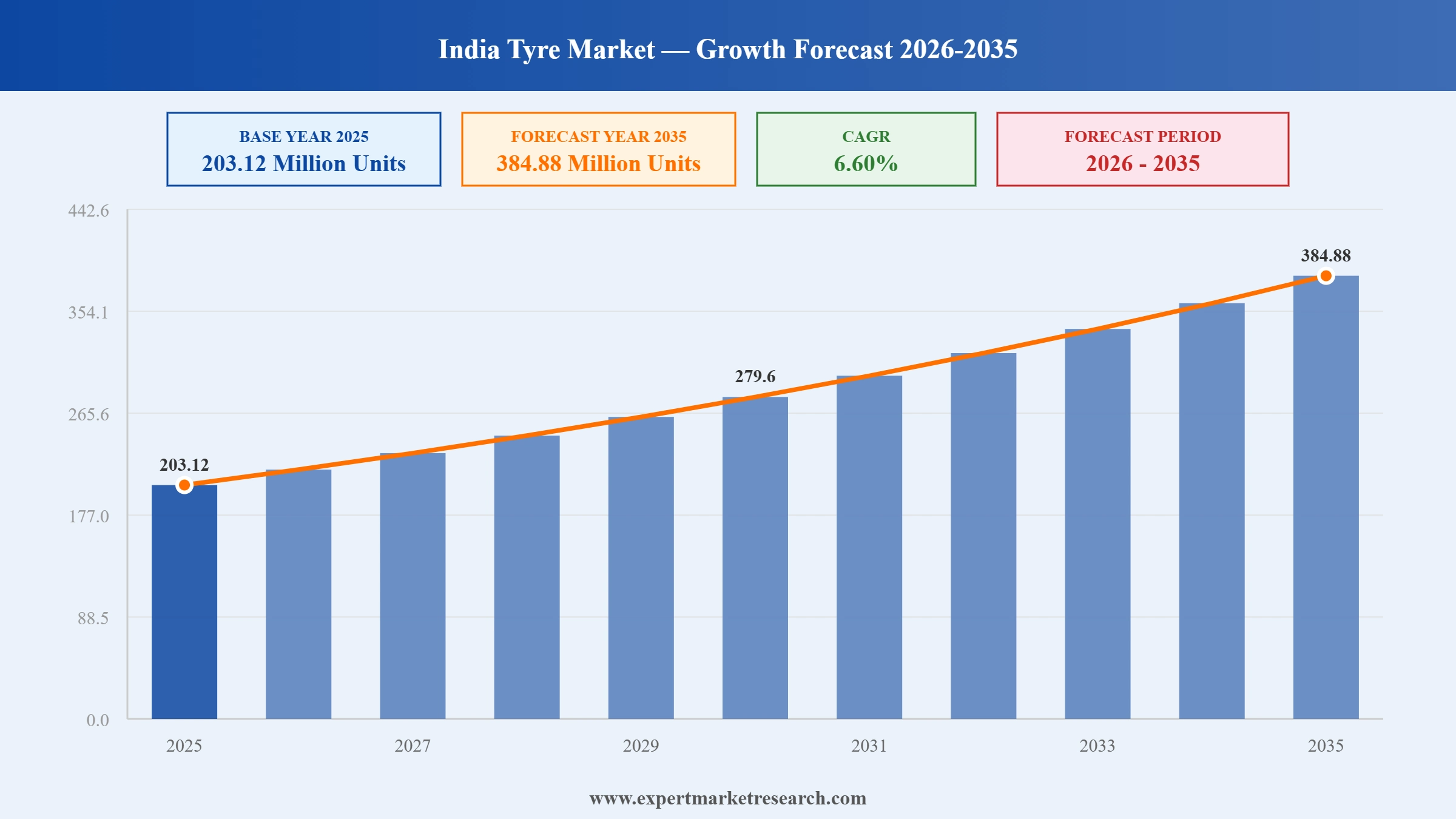

The India tyre market size attained a volume of 203.12 Million Units in 2025. The rising demand for electric two-wheelers and fleet-integrated electric buses is compelling tyre manufacturers to develop low-resistance, high-durability tyres tailored to EV-specific torque and load dynamics. As a result, the market is expected to grow at a CAGR of 6.60% during the forecast period of 2026-2035 to reach a volume of 384.88 Million Units by 2035.

The market dynamics is shaped by a wave of innovation and supportive government policies. As per industry reports, the Indian tyre exports recorded a turnover of over INR 23,073 crore in FY24, with a strong push from OEM and replacement demand. Government schemes like the Production Linked Incentive (PLI) for the auto sector and the National Electric Mobility Mission have invested major funds for tyre makers, especially those investing in smart manufacturing and EV-compatible tyres. The Ministry of Road Transport & Highways’ push to upgrade highways under the Bharatmala project is also increasing the demand for high-performance tyres.

A major trend in the India tyre market is the adoption of sustainable and smart tyre technologies. JK Tyre, for instance, offers 'Smart Tyre' with Treel sensors, offering real-time data on pressure, temperature and movement, positioning itself as a pioneer in connected mobility solutions. This tech-forward focus is vital, especially as fleet owners seek higher efficiency and data-driven performance from their tyre solutions.

Moreover, the country’s surge in automotive exports, especially to Africa and Southeast Asia, is contributing to rising demand for locally manufactured tyres. With rubber prices relatively stable and automation picking pace in domestic plants, tyre manufacturers in India are better placed to meet global quality benchmarks.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| India Tyre Market Report Summary | Description | Value |

| Base Year | Million Units | 2025 |

| Historical period | Million Units | 2019-2025 |

| Forecast Period | Million Units | 2026-2035 |

| Market Size 2025 | Million Units | 203.12 |

| Market Size 2035 | Million Units | 384.88 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 6.60% |

| CAGR 2026-2035 - Market by Region | West Region | 7.3% |

| CAGR 2026-2035 - Market by Region | North Region | 7.0% |

| CAGR 2026-2035 - Market by Price Segment | High | 7.4% |

| CAGR 2026-2035 - Market by Distribution Channel | Replacement | 7.3% |

| Market Share by Region | North Region | 31.4% |

The Expert Market Research's report titled “India Tyre Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

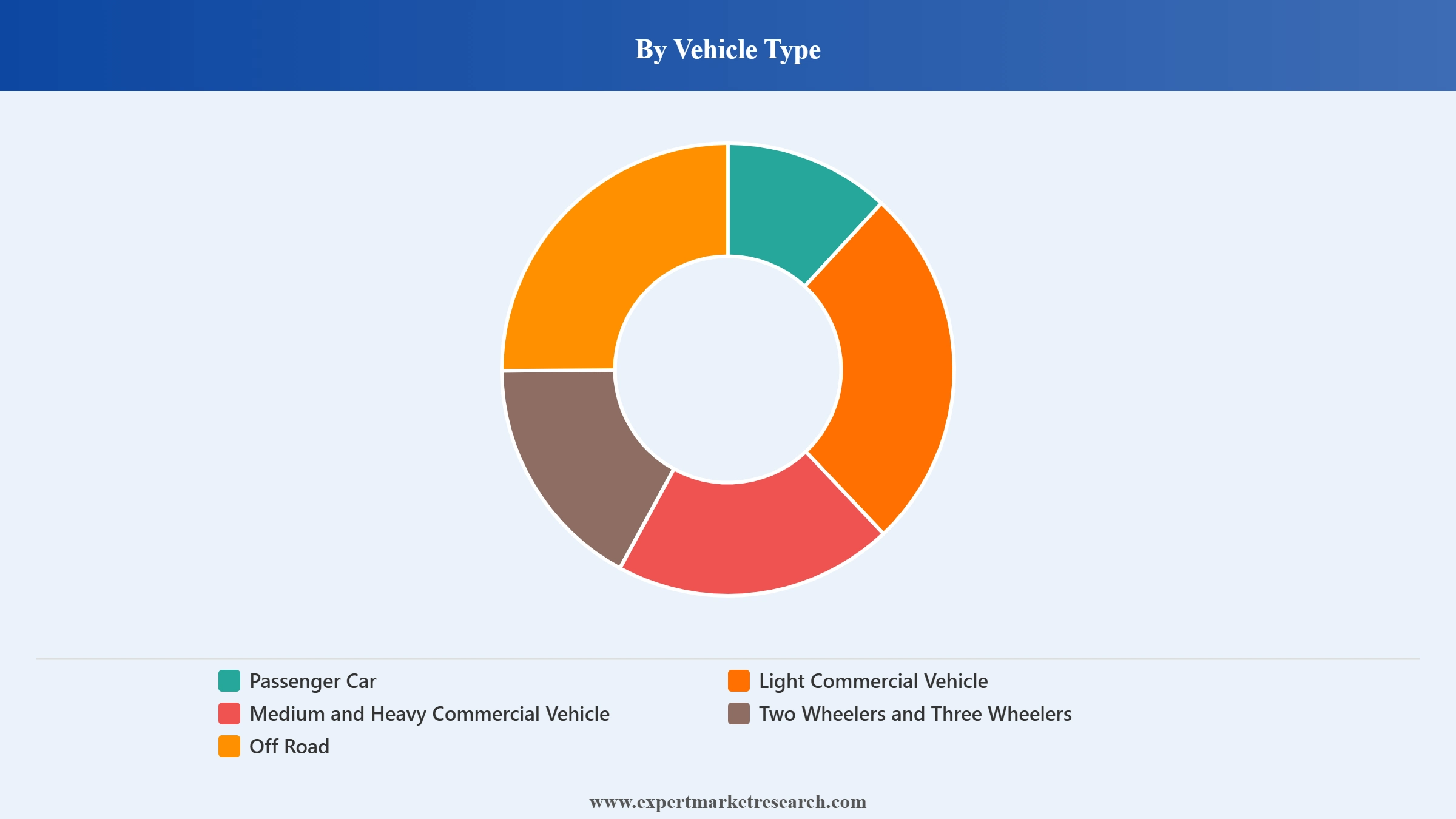

Market Breakup by Vehicle Type

Key Insight: Passenger cars dominate the industry due to mass ownership and replacement cycles. LCVs are surging in demand owing to the e-commerce boom. Medium and heavy commercial vehicles stay crucial for long-haul logistics, requiring high-durability tyres. Two- and three-wheelers lead in volume, especially across tier-II cities and rural zones. Off-road tyres, though niche, are gaining ground in mining and agricultural applications.

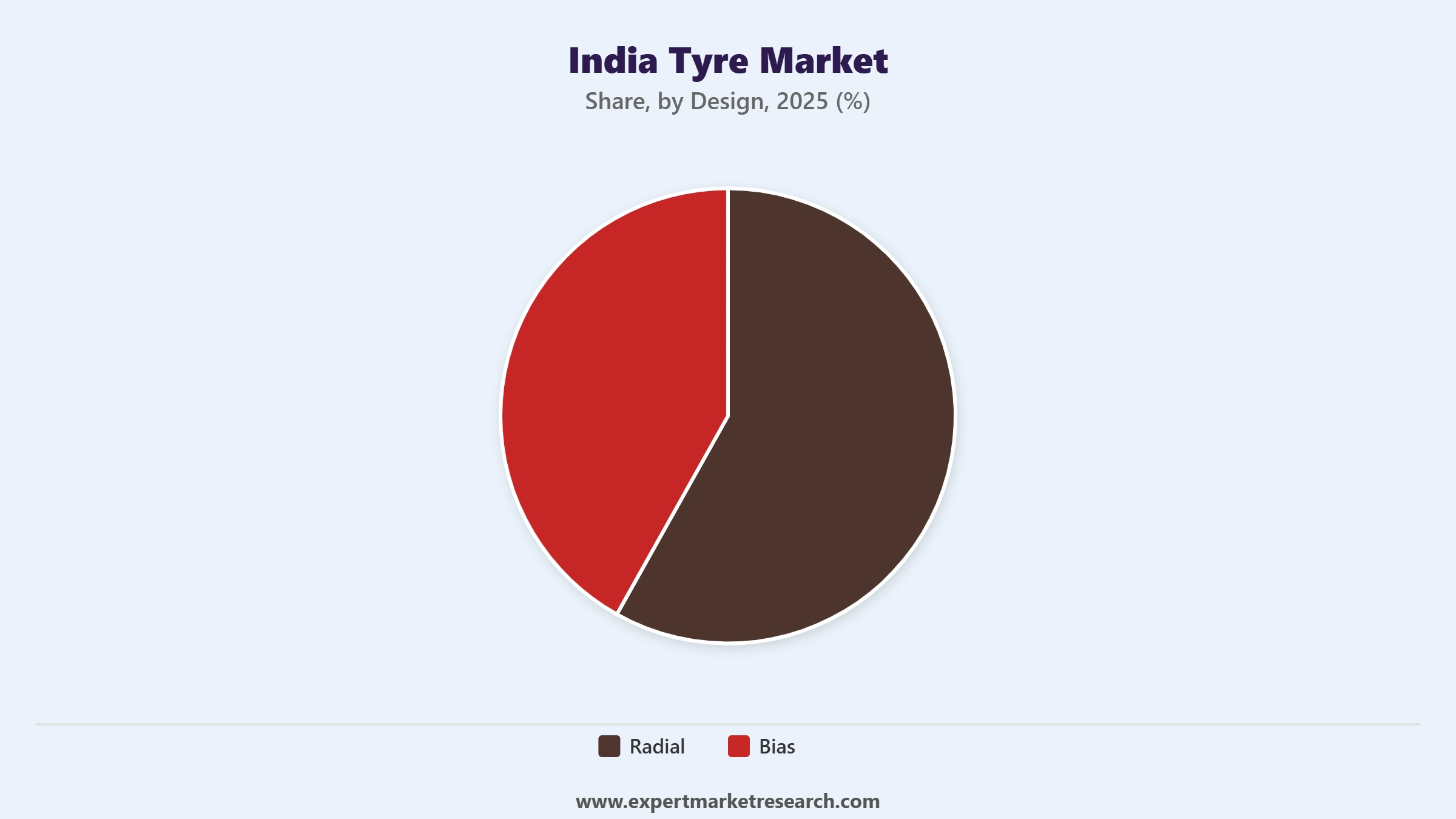

Market Breakup by Design

Key Insight: The tyre market in India is divided primarily between radial and bias designs. Radial tyres dominate on-road applications, owing to their performance, efficiency, and regulatory support. Bias tyres, find stronghold in niche, rugged terrains like construction, mining, and farm use. While radial tyres are common across cities and highways, the bias category is gaining ground in tough-operating conditions. For B2B buyers, the design choice is less about trend and more about operational ROI, driving tailored procurement depending on load patterns, road conditions, and frequency of usage.

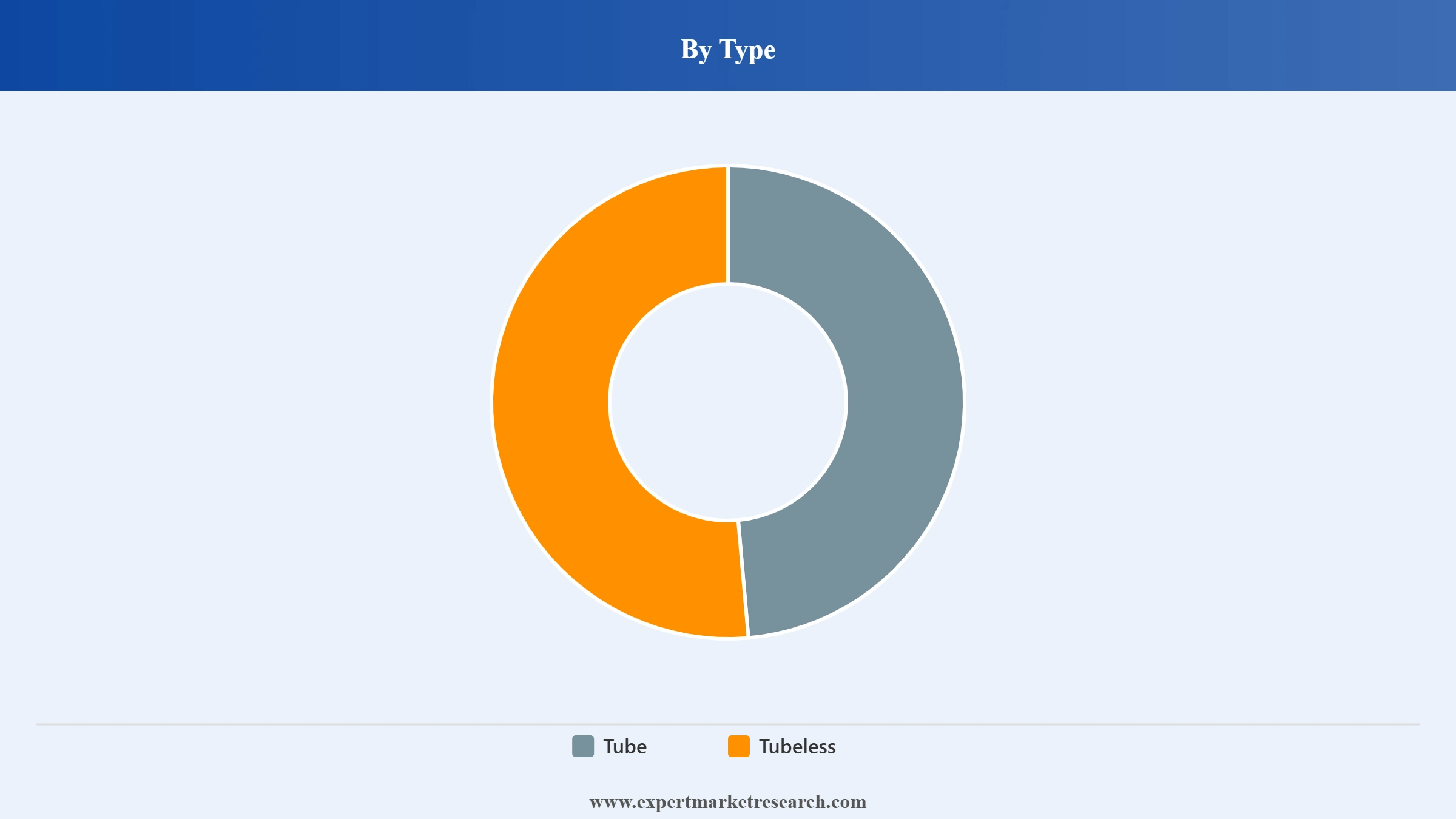

Market Breakup by Type

Key Insight: Tyre types in India are split across tubeless and tube variants, each with distinct B2B appeal. Tubeless tyres lead in performance, safety, and fleet reliability, especially in highway and urban operations. Tube tyres persist in cost-sensitive and rural markets, where ruggedness and affordability matter more than features. While the broader trend favours tubeless technology, tube tyres have remained relevant in the India tyre industry. For bulk buyers, the choice often hinges on road conditions, servicing infrastructure, and vehicle age.

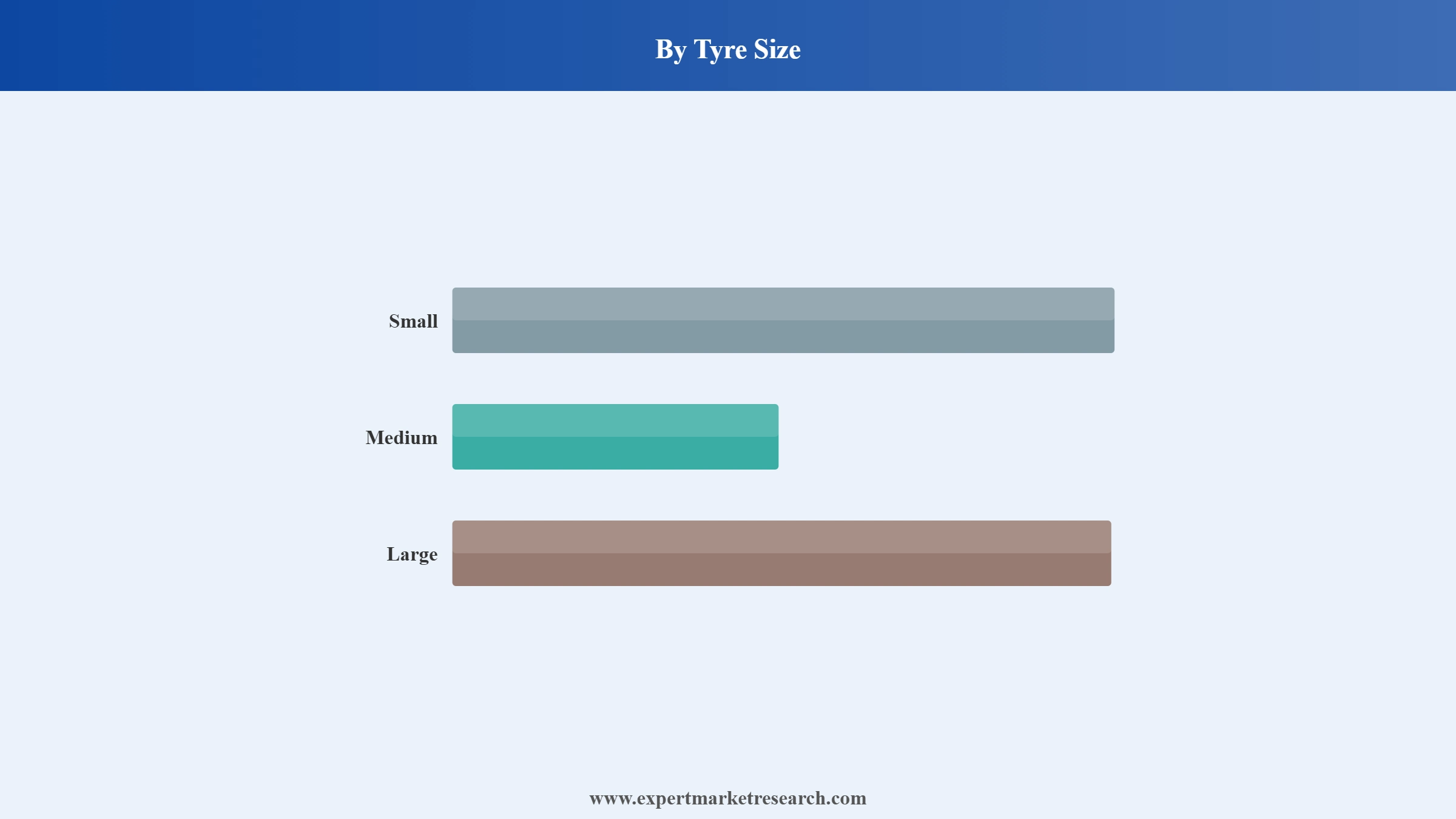

Market Breakup by Tyre Size

Key Insight: As far as the size dynamics is concerned, the market observes application-specific demand rising across categories. Small tyres have continued to be relevant due to mass two-wheeler and budget-car usage, mostly in rural belts and low-income urban zones. Medium-sized tyres dominate commercial transport due to balance between durability and cost, making them ideal for logistics and mid-load applications. Large sizes are expanding fast in terms of tyre market share in India, owing to the increased demand from construction, mining, and industrial fleets. Their enhanced builds, including smart and self-cooling variants, are becoming attractive for B2B buyers facing rugged terrain conditions.

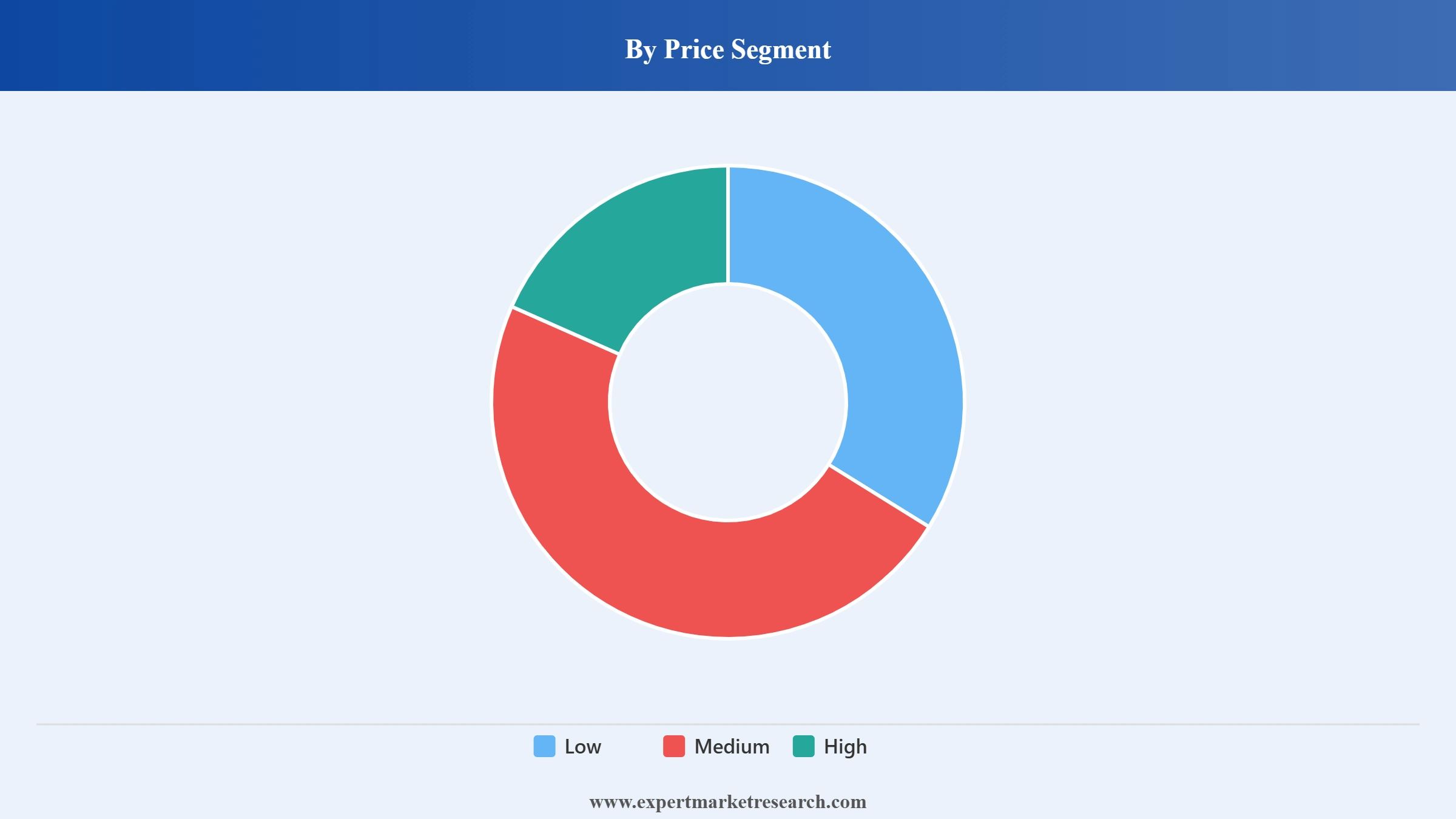

Market Breakup by Price Segment

Key Insight: By price is the market clearly segmented by value perception and end-use purpose. Low-price tyres continue serving cost-sensitive markets, particularly in rural transport and legacy fleet operators where basic utility is preferred to longevity. Medium-priced category accelerate majority of the tyre consumption in India as they provide the right balance of reliability, warranty support, and evolving technology integration without straining budgets. Meanwhile, high-priced tyres are scaling fast, led by electric mobility, long-haul fleet operations, and government-driven performance mandates.

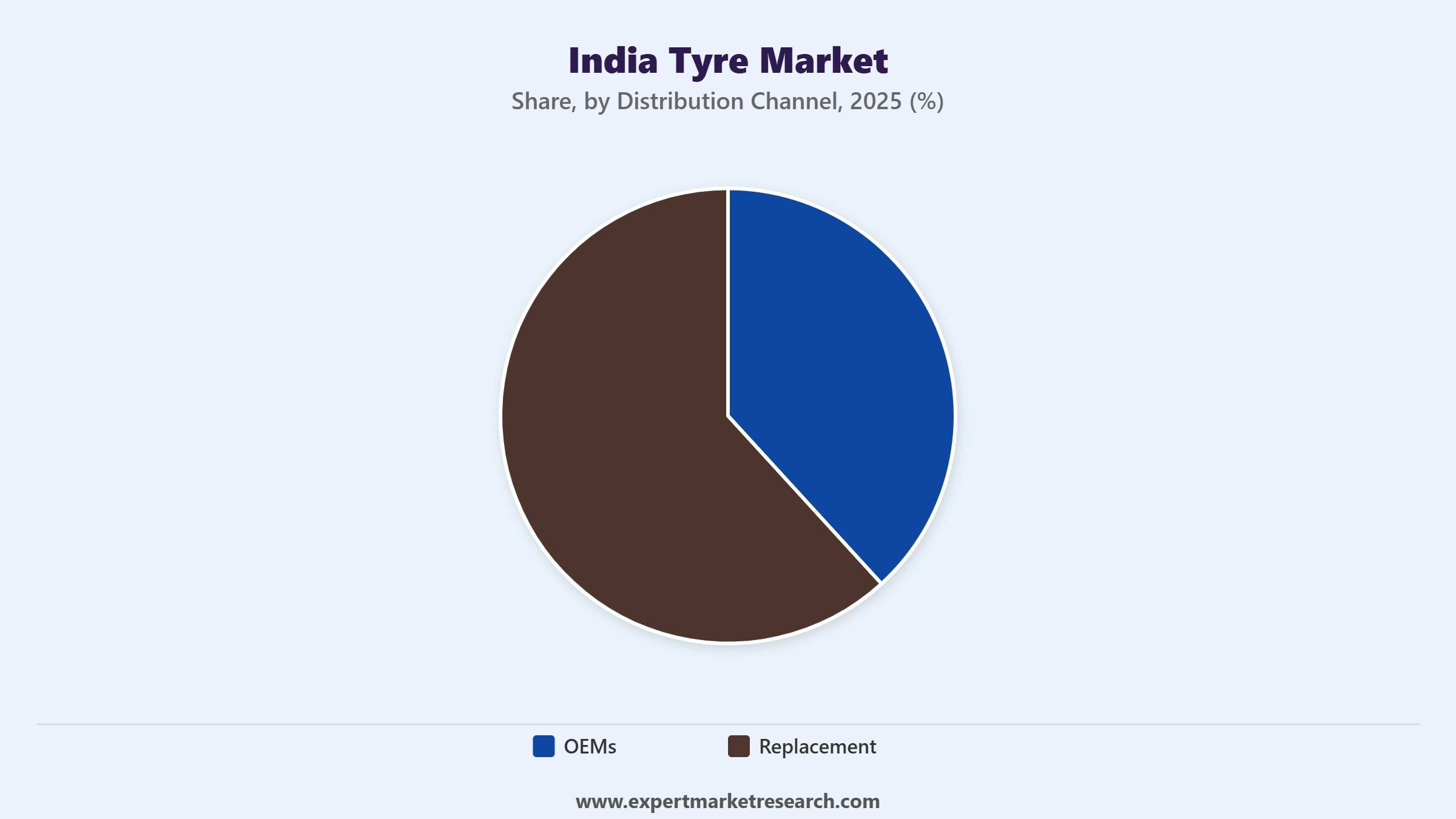

Market Breakup by Distribution Channel

Key Insight: Distribution channels are boosted by operational lifecycle and end-user sophistication. Replacement remains dominant, supported by the ageing vehicle stock and intense road usage that triggers high wear. B2B clients in state transport and mid-sized logistics now prefer structured replacement cycles, often under warranty or leasing contracts. On the other hand, OEMs are experiencing accelerated growth in the India tyre market with the rise of electric and connected vehicle manufacturing. Tyre makers are aligning with EV OEMs to pre-fit smart, sensor-rich tyres tailored to specific vehicle AI.

Market Breakup by Region

Key Insight: Regionally, the demand in the Indian market is shaped by industrial concentration, infrastructure maturity, and fleet diversity. The southern region leads the market due to strong OEM presence and EV innovation, with brands experimenting with digital tracking and low-noise tyre technology. Northern India sustains growth via logistics corridors but witnesses more conventional tyre usage. The east remains steady, driven by mining-centric demand requiring durable large tyres. Western India is growing at a fast pace, boosted by smart infrastructure projects and port logistics, which demand performance tyres with sensor-based durability checks.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Vehicle Type, Passenger Car Account for the Dominant Share of the Market

Passenger cars, which represent the dominant share in the market, is supported by both OEM and replacement demand. As per industry reports, India produced 58 million units of tyre for this category, and the trend is driven by urbanisation and mid-income car ownership. Tyre players are focusing on noise-reduction and performance-oriented tread patterns, especially in premium hatchbacks and sedans. For example, CEAT’s SecuraDrive and Apollo’s Amazer range are tailored to high-speed urban roads. With India's auto exports picking up pace, tyre firms are aligning with global quality benchmarks like EU labelling norms. Furthermore, the push for safer tyres, under AIS-142 standards by the government, is pushing innovation in tread design and wet grip for this segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Light Commercial Vehicles (LCVs) emerge to be the fastest-growing vehicle type in the tyre market in India. The rise in last-mile delivery, e-commerce logistics, and intercity goods movement are boosting demand for high-durability LCV tyres. In June 2024, JK Tyre launched ‘Jetway JUM’, a radial tyre tailored for city logistics. Government schemes such as PM Gati Shakti and Startup India are fuelling MSMEs in logistics, indirectly accelerating LCV tyre demand.

By Design, Radial Tyres Dominate the Indian Market

Radial tyres hold the dominant share in the market. These tyres offer better fuel efficiency, longer tread life, and reduced heat generation. Manufacturers like MRF and Michelin India are investing heavily in radial tyre capacity, particularly for trucks and buses. The government’s regulation to phase out bias tyres in new commercial vehicles has boosted radial adoption. Further, the increased preference for long-distance cargo and intercity mobility has made radial tyres the primary choice.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

As per the India industry report, bias tyres are witnessing renewed growth in specific B2B verticals like agriculture, mining, and construction. Their rugged build and low initial cost make them suitable for off-road environments with high impact and irregular terrain. The Government of India’s infrastructure push via the Bharatmala project and mining auctions has opened fresh demand for bias tyres. Players like BKT and TVS Eurogrip are innovating in tread depth and casing resilience for these applications.

By Type, Tubeless Tyres Account for the Largest Share of the Market

Tubeless tyres have become the dominant choice for both OEMs and fleet operators due to their lower puncture risk and longer lifespan. They offer superior safety and are particularly favoured in highways and long-distance logistics. With Indian roads improving and vehicle speeds rising, tubeless tyres have gained traction. Brands like Bridgestone and Apollo have expanded their tubeless offerings across commercial fleets. The government’s push for road safety under the National Road Safety Policy has further propelled the India tyre market expansion.

Despite the dominance of the tubeless category, tube tyres continue to observe growth in rural mobility and budget commercial applications. They are easier to manufacture, cheaper to replace, and hence, they continue to be dominant in tractors, old-model LCVs, and government tenders. State-run rural transport schemes and agricultural credit financing have also supported their use in semi-urban regions. Their lower upfront cost makes them appealing for buyers focused on affordability over technology.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Tyre Size, Medium Tyres Occupy a Significant Share of the India Tyre Market

Medium-sized tyres are seeing strong adoption in India’s mid-duty commercial vehicles, driven by expanding logistics networks and the surge in rural and urban goods movement. The recent shift toward smart radial tyres in 16-20-inch range, embedded with RFID tags for fleet-level tracking has resulted in the category’s continued dominance. JK Tyre's May 2025 launch of AI-powered smart tyres for passenger cars, linked directly with their mid-size tyre models, is gaining strong interest from logistics fleet operators. OEMs are also tuning vehicle platforms around this category to allow real-time tread data access. This trend is creating a unique space where technology meets tyre wear optimisation, especially in fleet-heavy zones like Punjab, UP and Maharashtra.

The country’s high demand for construction, mining, and high-tonnage vehicles has made large-sized variants heavy demand in the India tyre market. Innovations like nitrogen-inflated tyre systems in 22.5-inch and above tyre categories are gaining rapid popularity. BKT and Apollo Tyres have been testing graphene-infused compounds in these tyres for better wear resistance and fuel efficiency. With infrastructure-heavy projects like Bharatmala and Smart City programmes picking up pace, large tyres equipped with pressure monitoring sensors and self-cooling technology are becoming a B2B procurement preference. Fleets in Rajasthan and Odisha, where extreme terrain impacts tyre life, are turning to these enhanced builds for longer lifecycle assurance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Price Segment, Medium Price Tyres Secure the Bigger Share of the Market

Mid-priced tyres are striking the right balance between affordability and high-performance metrics. Their dominance is being bolstered by rising demand from Tier 2 and Tier 3 fleet operators who seek durability without high investment. Companies like CEAT and MRF are bundling these tyres with basic telematics offerings. In addition, the rise of tyre-as-a-service models across mid-size transport businesses is lending scalability to this category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

High-end tyres have led to increased sales due to electric buses, high-speed luxury fleets, and long-haul container logistics, as per the India tyre industry report. Leading players are developing high-silica blends for extreme road grip and energy efficiency. Tyre brands are partnering with OEMs to embed IoT into premium tyre models, delivering live updates on tyre stress and real-time inflation. B2B buyers in sectors like tech-parks and government bus fleets are increasingly prioritising these top-tier offerings. Apollo and Continental are also offering dynamic load-balancing systems integrated into tyres, making them ideal for safety-intensive applications in metro cities.

By Distribution Channel, the Replacement Category Clocks in the Major Market Share

Replacement tyres account for the maximum share in the Indian market revenue as ageing fleets and used vehicles remain central to mobility in mid and low-income zones. B2B buyers, such as state transport bodies and independent logistics companies, are leaning towards structured replacement contracts bundled with warranty analytics. Meanwhile, re-treading services bundled with replacements in commercial vehicles are creating a lifecycle value. The opportunity lies in subscription-based tyre maintenance models that are being increasingly launched in Tamil Nadu and Gujarat.

OEMs are seeing a spike in tyre procurement in India, especially as electric and hybrid vehicle production rises. Tyre manufacturers are collaborating closely with EV OEMs to engineer lightweight, high-load endurance tyres with ultra-low rolling resistance. Startups like Pirelli are entering this space with custom-designed OEM tyres featuring noise-cancellation layers and bio-sourced rubber compounds. OEM tie-ups, particularly in Karnataka and Maharashtra, are focused on co-developing smart tyres that respond to vehicle AI, offering real-time feedback on performance metrics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Region Holds the Leading Position in the Market

The South Indian market boasts of states like Tamil Nadu and Karnataka that lead to the region’s dominance due to their strong OEM manufacturing hubs and the rise of EV-centric industrial belts. Moreover, the integration of green tyres in fleet transitions has accelerated demand in this particular region. Brands are leveraging the proximity to technology clusters to offer tyres embedded with RFID and blockchain-backed service records.

The western region, particularly Gujarat and Maharashtra, boosts the India tyre demand growth with the surge in port connectivity, warehousing expansion, and smart infrastructure projects. The demand for long-haul radial tyres with quick-replace modular features is surging. Companies like TVS Eurogrip are also introducing quadrazone compound technology features 4 zones of compound working together to ensure optimal dynamical performances and extended tyre durability.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India tyre market players like MRF, Apollo, and JK Tyre are shifting focus toward digital integration, offering B2B clients predictive analytics, subscription-based tyre monitoring, and data-driven warranties. There is also a notable surge in collaborations with EV and smart vehicle OEMs to co-develop sensor-laced tyres that communicate directly with vehicle control systems. While the replacement market continues to be dominant, players are finding margin advantages in bespoke service models for fleet operators.

New age India tyre companies are entering with AI-powered re-treading diagnostics and blockchain-enabled supply chain tracking. Export opportunities via ports like Mundra are also attracting global partnerships. The next phase of competition is expected to revolve around sustainability metrics and embedded technology. Moreover, sensor-integrated tyres, AI-backed replacement cycles, bio-based compounds, graphene treading, and blockchain for tyre traceability are some of the key trends that companies can focus on, in the coming years.

MRF Limited, headquartered in India and founded in 1946, offers a diverse range of tyres catering to various types of vehicles, including heavy and light commercial vehicles, passenger cars, tractors, earthmovers, and motorsport vehicles. Some of its key brands include MUSCLE LIFT, STEEL MUSCLE, SHAKTI LIFE, SHAKTI SUPER, SUPER LUG, and SAVARI, among others.

Established in 1972 and based in Haryana, India, Apollo Tyres Ltd is a prominent player in the tyre industry, manufacturing and distributing quality tyres worldwide. Its product line includes several renowned brands such as ALNAC, AMAZER, APTERRA, ASPIRE, ALTRUST, MANCHESTER UNITED, and QUANTUM.

Headquartered in India and founded in 1858, CEAT offers a comprehensive selection of tyres suitable for all types of vehicles, ranging from heavy-duty trucks and buses to light commercial vehicles, earthmovers, forklifts, tractors, trailers, cars, motorcycles, scooters, and even auto-rickshaws. The company is committed to producing top-quality tyres for cars, bikes, and scooters.

Headquartered in India and founded in 1951, the company has introduced innovative 'Smart Tyre' technology in India, with Tyre Pressure Monitoring Systems (TPMS) and TREEL Sensors that enable real-time monitoring of a tyre's critical parameters, such as pressure and temperature.

Other key players in the market are Birla Tyres, Balkrishna Industries, TVS Srichakra, and Goodyear India, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

December 2025 - JK Tyre & Industries formally completed the amalgamation of its subsidiary Cavendish Industries Ltd. in December 2025, with the merger becoming effective from December 22, following NCLT approval. Cavendish, acquired by JK Tyre in 2016 from Kesoram Industries, held manufacturing capacity for truck and bus radial, truck and bus bias, and two- and three-wheeler tyres. At the time of acquisition the plant operated at barely 30% capacity; under JK Tyre's stewardship that figure climbed to 95%, and the consolidation is expected to further strengthen the company's commercial vehicle tyre positioning, balance-sheet efficiency, and operational scale.

January 2026 - JK Tyre inaugurated Phase III of its capacity expansion and modernisation programme at the passenger car radial tyre manufacturing facility in Banmore, Madhya Pradesh, in January 2026. The phase forms part of a multi-phase investment plan exceeding ₹1,000 crore aimed at strengthening the company's domestic PCR manufacturing footprint. The commissioning marks a significant milestone in JK Tyre's multi-year capital expenditure cycle and bolsters its ability to meet rising demand from both OEM and replacement channels.

February 2026 - Apollo Tyres announced a ₹5,810 crore investment in February 2026 to significantly expand manufacturing capacity at its Andhra Pradesh facility, targeting completion by FY2029. The expansion plan envisages a 52% increase in passenger car radial capacity, adding 3.7 million units annually, and an 82% boost in truck and bus radial capacity, adding 1.3 million units per year. Funding will be drawn from a combination of internal accruals and debt. The announcement came alongside a strong Q3 FY2026 performance, where consolidated net profit rose 40% year-on-year to ₹471 crore on 12% revenue growth to ₹7,743 crore.

March 2026 - MRF signed a Memorandum of Understanding with the Tamil Nadu government in March 2026 to establish a greenfield manufacturing facility for automotive tyres and allied products at the SIPCOT Industrial Park in Sivaganga district the company's fourth manufacturing unit in the state. The proposed project involves an estimated investment of approximately ₹5,300 crore over 12 years and is expected to generate direct employment for around 1,000 persons, with broader indirect employment across ancillary industries in the region. The MoU, non-binding in nature, is contingent on the state government sanctioning a customised incentive package and statutory approvals.

April 2026 - CEAT reported robust performance for the January-March 2026 quarter, with growth across all segments including its international business, and declared a ₹35 per share dividend (350%) for FY26, reflecting confidence in the company's financial health. Management acknowledged short-term pressure from rising raw material costs and global supply chain disruptions stemming from the West Asia conflict, but indicated plans to navigate these through targeted price adjustments and continued cost rationalisation while pressing ahead with its capacity expansion programme.

May 2026 - India's tyre industry was grappling with a returning wave of input cost inflation, driven by elevated natural rubber prices and rising crude oil derivatives. With raw material costs resuming an upward trajectory, major tyre manufacturers began signalling the likelihood of further price increases to protect operating margins. The rural replacement market also showed signs of modest softening, adding complexity to the demand outlook. Despite near-term margin pressures, the industry's long-term investment momentum anchored by large-scale capacity commitments from MRF, Apollo Tyres, and JK Tyre continues to signal sustained confidence in structural demand growth.

Explore the latest trends shaping the India tyre market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on India tyre market trends 2026.

South Korea Airless Tyres Market

India Passenger Car Tyre Market

Australia Tyre Market

Run Flat Tyre Market

Airless Tyres Market

Green Tyre Market

Farm Tyre Market

Tyre Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India tyre market reached an approximate volume of 203.12 Million Units.

The market is projected to grow at a CAGR of 6.60% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach around 384.88 Million Units by 2035.

Key strategies driving the market include investing in tyre-as-a-service models, co-developing with EV OEMs, expanding AI-enabled re-treading, offering digital warranties, and launching predictive analytics tools.

The key trends aiding the market include growing demand for electric vehicles and increasing adoption of technologically advanced tyres.

The different vehicle types include passenger car, light commercial vehicle, medium and heavy commercial vehicle, two wheelers and three wheelers, and off road, among others.

The major distribution channels in the market include OEMs and Replacement.

The key players in the market include MRF Limited, Apollo Tyres, JK Tyre & Industries, CEAT Limited, Birla Tyres, Balkrishna Industries, TVS Srichakra, and Goodyear India, among others.

The decline in automotive sales impacted the distribution of tyres amid COVID-19.

Rising vehicle production and sales boost tyre demand in the country.

North India holds the largest share of the market.

The key challenges are volatile raw material pricing, limited EV tyre readiness, technology adoption gaps among Tier 2 fleets, counterfeit product circulation, and lack of skilled manpower in predictive tyre maintenance.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Vehicle Type |

|

| Breakup by Design |

|

| Breakup by Type |

|

| Breakup by Tyre Size |

|

| Breakup by Price Segment |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.