Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

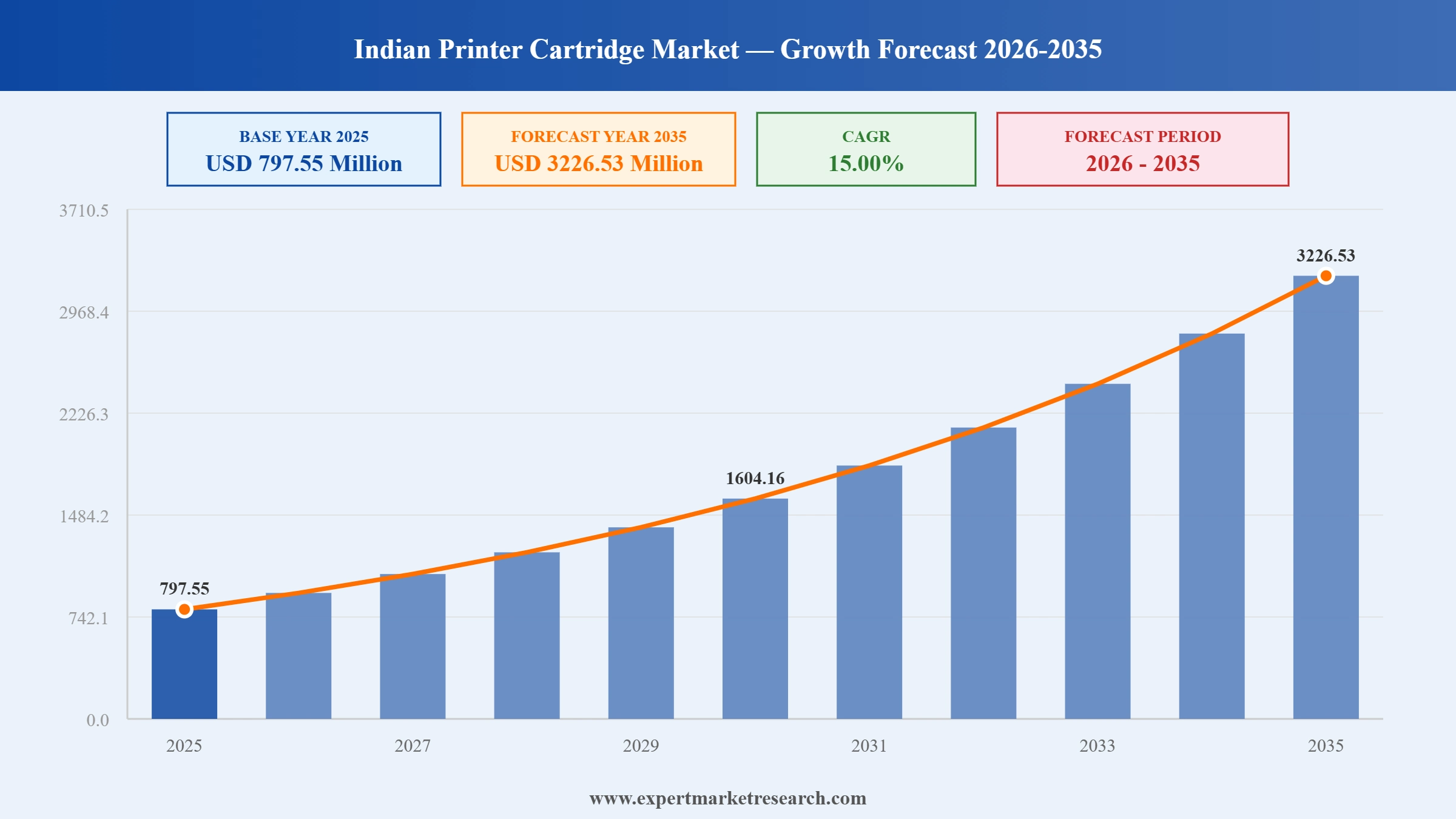

The Indian printer cartridge market reached a value of USD 797.55 Million at 2025 and is projected to expand at a CAGR of around 15.00% during the forecast period of 2026-2035. With increasing penetration of printers across commercial and government sectors, growing popularity of ink tank printers among cost-conscious consumers, rising demand from India's expanding SME ecosystem, and greater adoption of digital documentation in educational institutions, the market is expected to reach USD 3226.53 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's printer cartridge market is undergoing significant transformation, driven by manufacturing investments from global OEMs, a surge in ink tank printer adoption displacing traditional cartridge models, and growing e-commerce penetration expanding access to both original and compatible cartridges. Government import duties introduced to support local manufacturing are reshaping supply dynamics for players operating in the organised segment.

HP India unveiled a comprehensive portfolio of over 20 new products spanning personal systems, print, and workforce solutions. The launch featured AI-optimised inkjet printers designed for home and business use, reinforcing HP's position as the leading printer brand in India. The product suite targets diverse consumer segments, from students to enterprise users, significantly expanding the cartridge consumption base in the Indian printer cartridge market.

Brother International India introduced six new high-efficiency ink tank printers at a press conference in Delhi. Designed for homes, professionals, and small businesses, the range features auto-duplex printing, wireless connectivity, and spill-free refilling. The launch strengthens Brother's competitive position against HP and Epson in the fast-growing ink tank segment, which is a key driver of cartridge and refill demand across the Indian printer cartridge market.

Seiko Epson Corporation inaugurated India's first high-capacity ink tank printer manufacturing facility in Chennai in partnership with RIKUN Manufacturing Pvt. Ltd., with mass production commencing in October 2025. Epson, which holds the top inkjet printer market share in India with over 8 million EcoTank units sold domestically, uses this facility to support local production and reduce import dependence, strengthening India's printer cartridge supply chain significantly.

Kyocera Document Solutions India partnered with TechNova to expand its inkjet printing solutions across the Indian market, reinforcing availability of cost-effective and flexible printing options for businesses. The collaboration broadens Kyocera's reach into segments beyond its traditional laser printing stronghold, contributing to growing competition in the ink cartridge segment and driving increased cartridge consumption across India's organised printer sector.

India's ongoing push toward paperless governance and digital documentation across schools, banks, and public offices continues to stimulate structured procurement of printers and cartridges by government agencies. Growing deployment of multi-function printers under schemes targeting e-governance and document digitisation is generating consistent, high-volume demand for both ink and toner cartridges, supporting the Indian printer cartridge market growth across the government end-use segment.

The Government of India implemented an 11% basic customs duty plus a 1% cess on imported printer cartridges to encourage domestic manufacturing and reduce import dependence. This policy shift accelerates localisation by OEMs and third-party suppliers, increases the cost competitiveness of domestically produced cartridges, and supports the organised sector's expansion within the Indian printer cartridge market across both ink and toner categories.

India's printer market is experiencing a structural shift as ink tank printers with integrated refillable reservoirs displace conventional cartridge-based models. With over 8 million EcoTank printers sold in India, consumers are drawn to the lower cost-per-page and reduced cartridge replacement frequency. This trend is reshaping demand patterns within the Indian printer cartridge market, accelerating growth in the compatible and refilled cartridge segments.

The rapid growth of e-commerce platforms in India has significantly improved the accessibility and affordability of printer cartridges, particularly for compatible and remanufactured options. Platforms such as Amazon India and Flipkart enable price comparison and direct-to-consumer delivery, expanding the reach of both branded and non-branded cartridge suppliers and intensifying competition within the unorganised and organised segments of the Indian printer cartridge market.

India's thriving small and medium enterprise sector is a primary engine of recurring printer cartridge demand, with printing essential for invoicing, documentation, and compliance across millions of businesses. As SME formation accelerates through government support programmes and formalisation initiatives, the consistent requirement for ink and toner cartridges is reinforcing commercial segment growth and expanding the organised distributor network in the Indian printer cartridge market.

The report of the Expert Market Research's titled "Indian Printer Cartridge Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

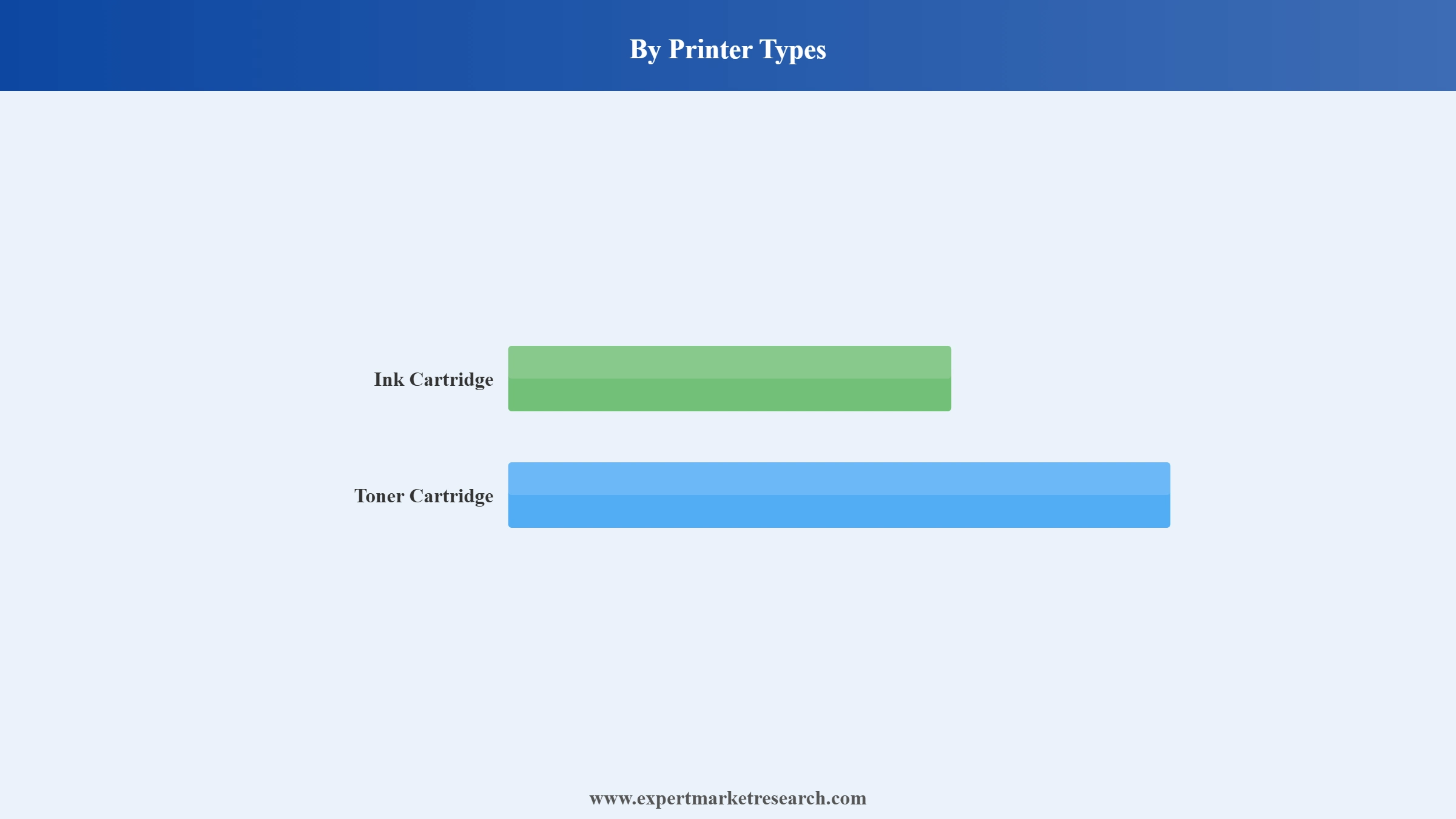

Market Breakup by Printer Types

Key Insight: Ink cartridges dominate the Indian printer cartridge market, reflecting the widespread use of inkjet printers across households, small offices, and educational institutions in India. The segment benefits from a large base of installed inkjet printers, particularly the rapidly growing ink tank printer category from brands such as Epson India and HP. Original cartridges hold the highest revenue share due to quality assurance, but compatible and refilled cartridges are capturing increased share on cost sensitivity grounds.

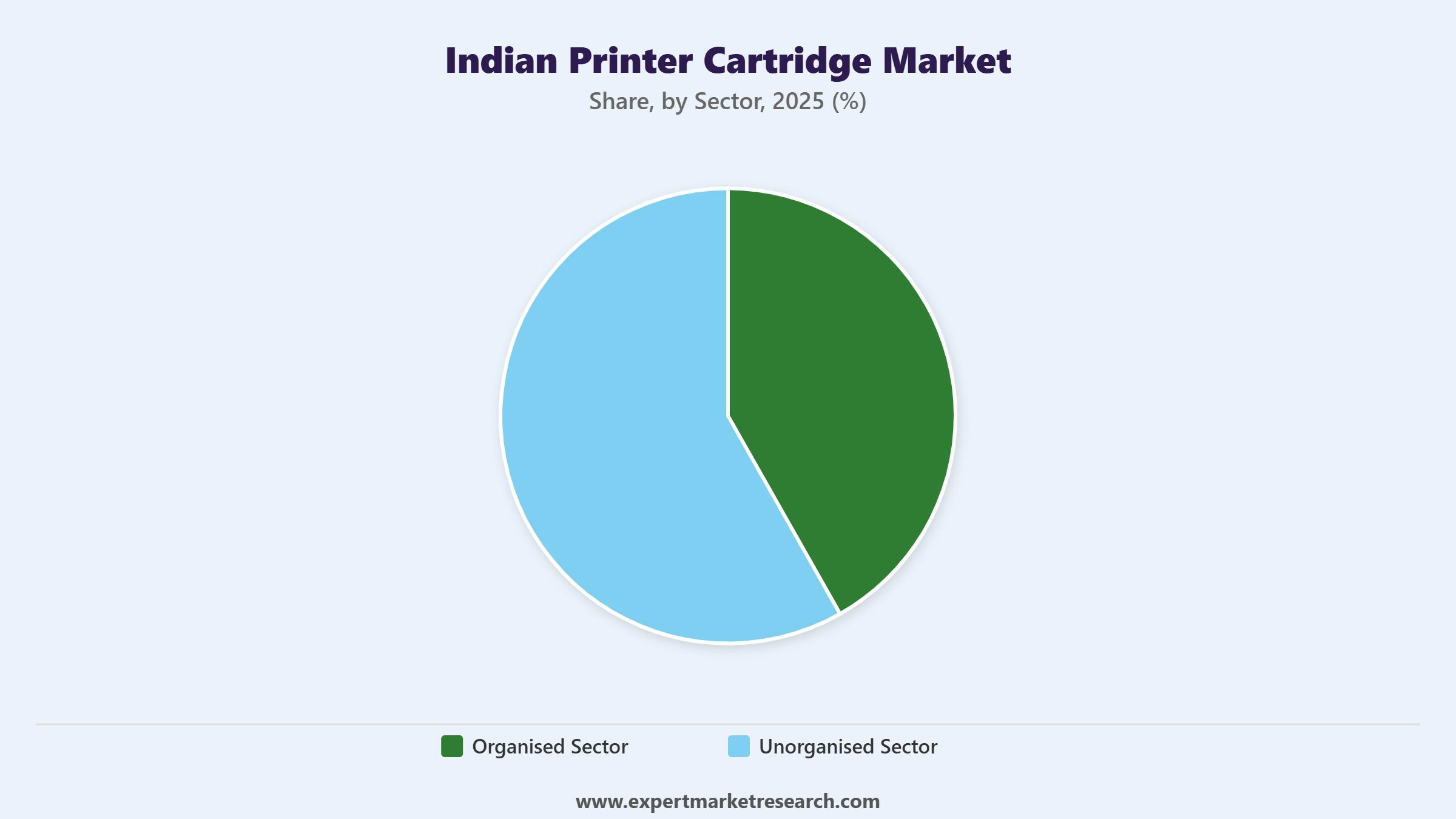

Market Breakup by Sector

Key Insight: The organised sector leads the Indian printer cartridge market, driven by the presence of established multinational brands operating authorised distribution and service networks. Key players such as HP Development Company, Epson India Pvt. Ltd., and Brother International (India) Pvt. Ltd. command significant share through branded products, warranty support, and quality consistency. The unorganised sector remains significant, serving price-sensitive buyers through local refilling shops and compatible cartridge distributors across tier-II and tier-III cities.

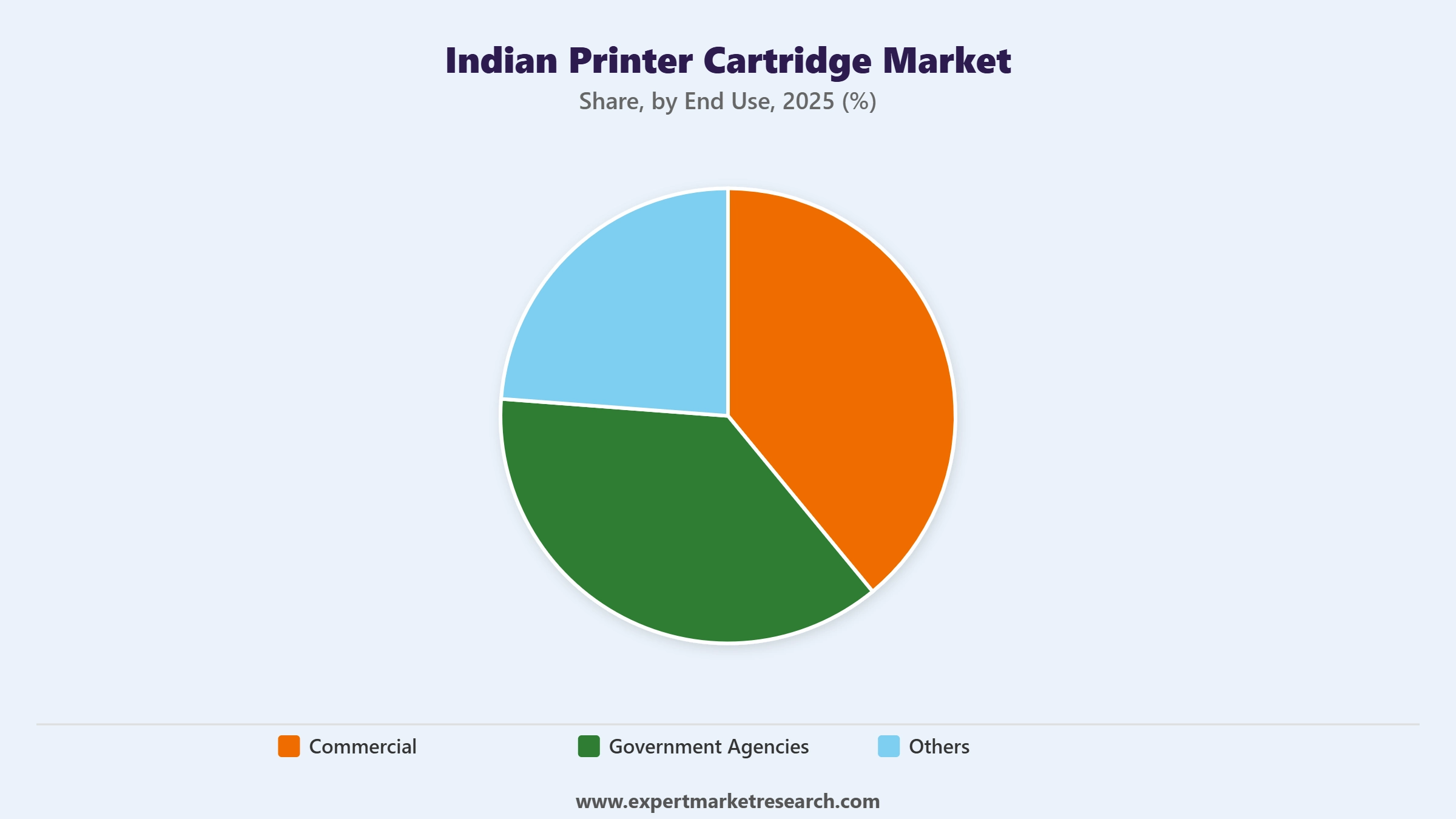

Market Breakup by End Use

Key Insight: Commercial end use accounts for the dominant share of the Indian printer cartridge market, as businesses across retail, BFSI, logistics, and professional services maintain constant demand for printing documentation, invoices, and marketing materials. The government agencies segment is a growing driver of toner cartridge demand, with procurement digitalisation strengthening structured purchasing. Rising home office setups post-2020 have expanded the others category, which includes residential and educational institution use across India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Printer Types, ink cartridge accounts for the dominant share of the market due to the large installed base of inkjet printers across homes, offices, and institutions in India.

Ink cartridges hold the majority share in the Indian printer cartridge market, supported by the widespread adoption of inkjet printers across home users, small offices, and educational segments. The cost-effectiveness of inkjet printers at point of purchase, combined with ongoing cartridge replacement requirements, sustains consistent demand. OEM players like Epson India and HP dominate the original ink segment, while the refilled and compatible sub-segments serve a vast base of budget-sensitive consumers. India's rapidly growing ink tank printer segment adds incremental demand for bulk ink refills.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Toner cartridges represent the second major segment, driven by the demand for laser printers in corporate offices, banking institutions, and government agencies where high-volume printing is essential. The laser printing market in India is steadily expanding as businesses prioritise speed, lower cost per page at high volumes, and sharp text quality for professional documentation. Original toner cartridges from brands such as HP and Brother maintain strong share due to quality requirements, though compatible alternatives are gaining traction in the cost-conscious commercial segment.

By Sector, the organised sector accounts for the dominant share of the market due to strong brand presence, certified product quality, and structured distribution by multinational OEMs.

The organised sector leads the Indian printer cartridge market by value, anchored by the distribution and marketing investments of global OEM brands. Authorised dealers, hypermarkets, and e-commerce platforms are the primary channels through which organised sector cartridges reach consumers and businesses. Quality assurance, warranty backing, and compatibility guarantees make organised sector products preferred for commercial and institutional buyers. Dell's distribution network expansion across India in 2025 exemplified the continued investment by OEM players in deepening organised sector reach across the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The unorganised sector, comprising local cartridge refilling businesses and compatible product distributors, serves a large and price-sensitive user base concentrated in small businesses and individual consumers across India. This segment benefits from significantly lower price points and is particularly strong in tier-II and tier-III cities where authorised OEM service centres have limited reach. However, the Government of India's import duty measures on cartridges are encouraging more suppliers to formalise operations, gradually increasing the share of the organised segment in the Indian printer cartridge market.

By end Use, commercial accounts for the dominant share of the market due to the high-frequency printing requirements of India's large and growing business ecosystem.

Commercial end use leads the Indian printer cartridge market, driven by India's expanding base of small and medium enterprises, corporate offices, BFSI institutions, and retail businesses that generate consistent daily printing requirements. Invoice printing, compliance documentation, marketing collateral, and operational paperwork collectively sustain high cartridge replacement rates across commercial settings. HP India's launch of more than 20 AI-powered printer products in May 2026 specifically targeted this commercial segment with solutions optimised for small and medium business environments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The government agencies segment is emerging as a structurally growing end-use category in the Indian printer cartridge market, driven by procurement of laser printers for documentation, record-keeping, and compliance-related printing across central and state government offices. The government sector implements stringent regulations and monitors the refurbished copier market tightly, creating strong demand for original toner cartridges from brands with established government supply partnerships. Controlled procurement frameworks make this a high-value, recurring demand segment for organised sector cartridge suppliers.

The Indian printer cartridge market features a moderately consolidated competitive landscape dominated by global OEM brands operating through well-established distribution networks. HP Development Company, Epson India, Brother International India, and Dell collectively hold a dominant position in the organised segment through brand strength, quality assurance, and after-sales support infrastructure. These companies continue to invest in product innovation, including ink tank printer technology and subscription-based ink services, to strengthen customer retention and reduce share erosion to compatible and refilled alternatives.

Founded in 1939 and headquartered in Palo Alto, California, HP Development Company, L.P. is a global technology company and the undisputed market leader in India's printer and cartridge industry. HP holds the largest share of the Indian printer market and offers an extensive portfolio of ink and toner cartridges for inkjet, LaserJet, and Smart Tank printer lines. In May 2026, HP India unveiled over 20 new AI-powered products including inkjet printers, reinforcing its dominance in the Indian printer cartridge market.

Founded in 1942 and headquartered in Suwa, Japan, with India operations based in Bengaluru, Epson India Pvt. Ltd. is India's leading inkjet printer brand by market share. Epson pioneered the EcoTank ink tank printer category, with over 8 million units sold domestically. In July 2025, Epson inaugurated India's first ink tank printer manufacturing facility in Chennai, underlining its commitment to local production and its pivotal role in driving ink-based cartridge demand in the Indian printer cartridge market.

Brother International (India) Pvt. Ltd. is the Indian subsidiary of Brother Industries, Ltd., founded in 1908 and headquartered in Nagoya, Japan. Brother India offers a broad portfolio of ink tank printers, laser printers, and multi-function devices serving home, SME, and corporate users. In September 2025, Brother India launched six new ink tank printers in Delhi, expanding its competitive offering against HP and Epson. Brother is a key player in both the ink cartridge and toner cartridge segments of the Indian printer cartridge market.

Founded in 1984 and headquartered in Round Rock, Texas, Dell Technologies is a global technology company that distributes laser printers and toner cartridges in India through its enterprise sales channels and authorised partner network. Dell primarily serves the commercial and government segments with high-capacity toner cartridges for office environments. In 2025, Dell expanded its printer consumables distribution network across India, strengthening its availability in organised retail and B2B procurement channels within the Indian printer cartridge market.

Other key players in the market are Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain comprehensive intelligence on India's printer cartridge industry from 2026 with our latest market report. Stay ahead of rapidly evolving consumer preferences, OEM investment patterns, and policy-driven supply chain shifts. Whether you are a manufacturer, distributor, or investor, this report equips you with the clarity needed to capture growth. Download your free sample today and uncover the key opportunities shaping the Indian printer cartridge industry through 2035.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The Indian printer cartridge market was driven by the Indian ink and toner cartridge market, which reached a value of nearly USD 797.55 Million in 2025.

The market is expected to be aided by the ink and toner cartridge industry in India, which is anticipated to at a CAGR of nearly 15.00% in the forecast period of 2026-2035.

The market is expected to be driven by the ink and toner cartridge industry in India, which is likely to reach a value of USD 3226.53 Million by 2035.

The major drivers of the industry include the rising disposable incomes, increasing population, growing electronics sector, and the increasing demand for printers.

The rising popularity of refilled and non-OEM cartridges and their growing demand can be attributed to factors like the high cost of OEM cartridges combined with the emergence of refills and remanufacturers with better equipment and good quality raw material (inks and so on) in recent years. This is expected to be a key trend guiding the growth of the industry.

Ink cartridge and toner cartridge are the leading printer types in the industry.

The significant sectors of printer cartridge in the market are organised sector and unorganised sector.

The major end-use sectors of the industry include commercial and government agencies, among others.

The leading players in the market are HP Development Company, L.P, Epson India Pvt. Ltd., Brother International (India) Pvt. Ltd., and Dell, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Printer Types |

|

| Breakup by Sector |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.